Market Overview: Caprylic Capric Triglycerides Market Expansion Driven by Clean Beauty Reformulation, Enzymatic Processing, and Pharma-Grade Demand

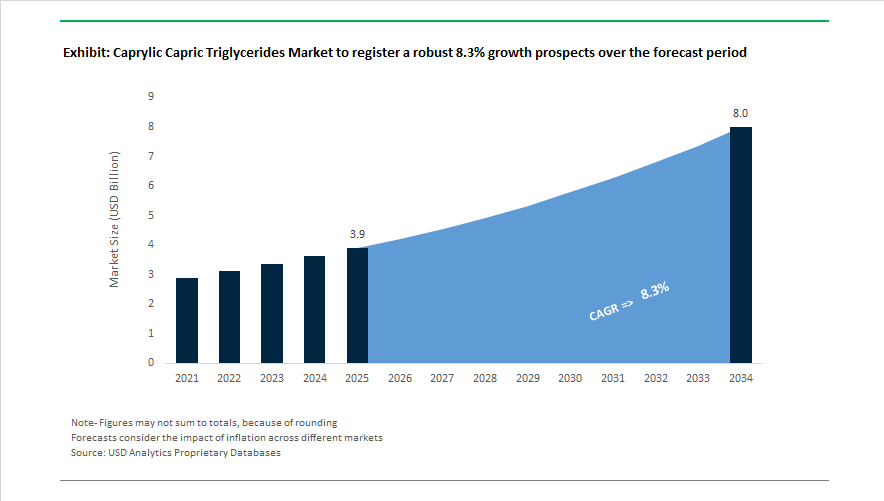

The Caprylic Capric Triglycerides market is projected to grow from USD 3.9 billion in 2025 to USD 8.0 billion by 2034, advancing at a CAGR of 8.3% as lipid-based emollients replace petrochemical and silicone ingredients across personal care, nutraceutical, and pharmaceutical applications. In 2024, Croda International launched a B2B e-commerce platform to serve indie beauty brands with low-volume CCT procurement, accelerating formulation cycles for clean-label skincare. During the same year, KLK OLEO released an updated cosmetic-grade MCT technical brochure emphasizing renewable vegetable glycerine feedstocks and oxidative stability, while Berg + Schmidt introduced digital traceability systems to provide cradle-to-gate transparency for palm and coconut derivatives. These supply chain upgrades reinforced the position of CCT as a biodegradable, high-purity ester aligned with sustainability reporting requirements.

Margin stabilization and manufacturing innovation characterized 2025. In May 2025, Stepan Company reported margin recovery within its medium-chain triglyceride lines, supported by improved pricing discipline and normalized raw material availability. By mid-2025, producers such as Croda and Oleon advanced enzymatic catalysis routes for CCT synthesis, achieving higher ester purity and lower process energy consumption than conventional esterification. September 2025 market data from Tradeasia International indicated that more than 2,500 new cosmetic SKUs adopted CCT as a primary emollient, representing a 20% year-on-year increase as formulators phased out synthetic silicones. Late 2025 industry shifts showed pharmaceutical and nutraceutical uses rising to 30% of total demand, with pharma-grade CCT commanding up to a 40% price premium as a carrier for lipid-soluble actives.

Regulatory and strategic developments continued into 2026. New United States import duties on MCT feedstocks in 2025 encouraged domestic fractionation investments to secure North American supply resilience. In November 2025, Solabia Group introduced a CCT-based texturizing agent at in-cosmetics Asia, delivering dry-touch sensory profiles in sunscreens and facial care. January 2026 leadership changes at BASF signaled a stronger focus on renewable esters within its Care Chemicals division, complemented by the opening of BASF’s Global Digital Hub in Hyderabad to optimize ester supply chains through AI modeling. February 2026 presentations from Croda at in-cosmetics Global highlighted PEG-free emulsification systems using CCT as a carrier to replicate silicone-like skin feel with high sensory accuracy.

Trends and Opportunities Accelerating Growth in the Caprylic Capric Triglycerides (CCT) Market

The Global Caprylic Capric Triglycerides (CCT) Market is experiencing sustained momentum as clean beauty reformulations, pharmaceutical-grade lipid delivery systems, and deforestation-free sourcing requirements reshape demand across cosmetics, personal care, nutraceuticals, and drug delivery. Manufacturers are increasingly prioritizing plant-derived MCT oils, high-purity CCT excipients, and RSPO-certified sustainable triglycerides as brands move away from mineral oils and silicones toward biodegradable, traceable emollients. At the same time, biotechnology-driven alternatives are emerging as strategic hedges against palm oil volatility and tightening environmental regulations.

Clean Beauty Reformulations Accelerate Adoption of Plant-Derived CCT as a Core Emollient

The global clean beauty movement is no longer niche and is now driving large-scale substitution of synthetic emollients with naturally derived caprylic capric triglycerides. Industry analysis from early 2025 indicates that the clean beauty segment is expanding at approximately 10% annually, triggering widespread reformulations where CCT is replacing up to 15% of legacy silicone and mineral oil applications in premium skincare and haircare products. This shift is reinforcing CCT’s position as a preferred lightweight, non-greasy emollient with strong sensory performance and clean-label appeal.

Beyond cosmetics, pharmaceutical demand is rising sharply. Specialty ingredient suppliers such as Gattefossé reported in February 2025 increased adoption of high-purity CCT grades, including Labrafac™, in nanoemulsion systems for oral and topical drug delivery, citing superior solubilization and biocompatibility versus fossil-based carriers. Performance benchmarks published in November 2025 further show that CCT-based formulations now achieve 24+ month oxidative stability without synthetic antioxidants, directly supporting preservative-free and minimalist ingredient claims that dominate modern clean beauty positioning.

EUDR and RSPO Standards Force Full Traceability Across Palm-Derived CCT Supply Chains

Regulatory and consumer pressure for sustainable palm sourcing is fundamentally restructuring CCT procurement strategies. Under the EU Deforestation Regulation (EUDR), large operators must provide plot-level geolocation traceability for all palm-derived products by December 30, 2025, with penalties reaching up to 4% of annual EU turnover for non-compliance. This requirement is accelerating investment in digital traceability systems and verified sustainable sourcing across the caprylic capric triglycerides value chain.

Parallel changes are unfolding within the Roundtable on Sustainable Palm Oil framework. Following its 22nd General Assembly in November 2025, implementation of the RSPO P&C 2024 standard was deferred to May 31, 2026, compelling CCT producers to realign audits with the new Certification Systems 2025 requirements effective May 14, 2026. Corporate buyers are moving quickly. In October 2025, International Flavors & Fragrances announced a revised Sustainable Palm Oil Policy committing to 100% Deforestation- and Conversion-Free supply chains by 2030, with traceability to plantation level for derivative portfolios, including MCT oils and CCT-based esters.

Segregated RSPO-Certified CCT Creates a Sustainability Premium in EU and Global Markets

A high-value opportunity is emerging around Segregated (SG) and Identity Preserved (IP) RSPO-certified caprylic capric triglycerides. As market dynamics shift from volume-driven procurement to verifiable ESG performance, suppliers capable of delivering fully traceable CCT are capturing pricing premiums. Market intelligence from September 2025 confirms that sustainability compliance has evolved into a financial risk management imperative, particularly as global ESG-linked assets are projected to exceed $53 trillion by 2026.

The RSPO Supply Chain Certification Standard Review (2025 to 2026), launched in February 2025, is expected to finalize stricter distributor and processor requirements by September 2026. Early adopters securing certification under the forthcoming “2025 System” stand to gain preferential access to European retail channels. Operators achieving SG-certified CCT ahead of late-2026 EUDR enforcement are positioned for first-mover advantage, as EU retailers increasingly delist products unable to demonstrate zero-deforestation origin.

Biotechnology-Derived and Palm-Free MCTs Open a New Frontier for Sustainable CCT Production

To mitigate palm oil price volatility and regulatory exposure, the industry is rapidly investing in enzymatic esterification and microbial lipid platforms to produce next-generation medium-chain triglycerides. In September 2024, Evonik commissioned a new multi-million-euro facility in Steinau, Germany, dedicated to enzymatic emollient manufacturing, reducing ester production carbon footprint by over 60% versus conventional chemical catalysis.

Biotech innovation is accelerating further. At the Tech Tour Bio-based Industries event in November 2025, COLIPI showcased carbon-to-oil technology that converts industrial CO2 emissions into lipids structurally identical to palm-derived CCT, with commercial launches planned for 2026. Meanwhile, Mycolever and peer startups are advancing precision fermentation routes using fungal biocompounds to produce biodegradable, palm-free MCTs. These alternative CCT pathways allow formulators to bypass deforestation risk entirely while meeting clean beauty, pharmaceutical excipient, and sustainable packaging requirements.

Caprylic Capric Triglycerides (MCT Oil) Market Share and Segmentation Insights

Market Share by Source: Coconut-Derived MCTs Lead on Clean Label and Stability

Coconut-derived MCT oil holds 68% of market share in 2025, favored for its high natural content of caprylic and capric triglycerides, neutral flavor, oxidative stability, and non-GMO positioning. Production centers in the Philippines, Indonesia, and India support global supply, with Rainforest Alliance and Fair Trade certifications commanding price premiums in nutraceutical and personal care channels. Palm-derived MCTs rank second, offering cost advantages through palm kernel oil, though RSPO certification requirements and EUDR compliance are reshaping sourcing strategies, particularly for large-scale manufacturers in Asia. Other sources remain niche, including babassu oil, fermentation-derived vegan MCTs, and dairy-based MCTs for premium infant formula, constrained by higher production costs and limited scale.

Market Share By Source, 2025.png)

Market Share by Application: Personal Care Leads While Nutraceuticals Drive Fastest Growth

Personal care represents 37% of MCT oil consumption in 2025, leveraging caprylic/capric triglycerides as lightweight emollients and solubilizers in moisturizers, sunscreens, serums, and color cosmetics, supported by COSMOS and NATRUE-certified clean beauty formulations. Nutraceuticals form the second-largest and fastest-growing segment, fueled by ketogenic diets, metabolic health awareness, and demand for quick-release energy supplements delivered via liquids, softgels, and powders. Food and beverages integrate MCTs into sports drinks, coffee creamers, meal replacements, and infant nutrition, emphasizing non-GMO and clean-label claims. Pharmaceuticals utilize MCTs as excipients in lipid-based drug delivery systems and medical foods, requiring USP and EP compliance, while industrial applications remain limited to lubricants and release agents with modest, cycle-driven volumes.

Competitive Landscape of the Caprylic Capric Triglycerides Market

The global Caprylic Capric Triglycerides (CCT) market in 2026 is defined by a shift toward high-purity green emollients, pharma-grade excipients, keto nutrition carriers, and microbiome-friendly cosmetic ingredients. Competition centers on C8/C10 ratio control, RSPO-compliant sourcing, lipid fractionation technology, and vertically integrated plantation-to-product models. Market leaders are differentiating through certified natural-origin CCT, patented enzymatic esterification, QR-based sustainability traceability, pharmacopeia-grade compliance, and circular glycerin integration. Demand growth is strongest across premium skincare, lipid-based drug delivery systems (LBDDS), sports nutrition, infant formula, and clean-label food applications, positioning CCT as a strategic ingredient for both beauty and life sciences.

Microbiome-friendly green emollients powered by BASF SE

BASF remains a dominant force in 2026 by embedding caprylic capric triglycerides within its Care Chemicals division, emphasizing certified natural-origin and microbiome-friendly formulations. Its Myritol® 312 and 318 grades are flagship green emollients carrying COSMOS, NaTrue, and EU Ecolabel certifications for premium skincare. Showcased at the 35th IFSCC Congress, BASF’s CCT-based galenic ingredients are engineered to protect healthy skin microflora in leave-on products. Strategically, BASF positions CCT as a bio-active carrier, using solid lipid particle technology to stabilize sensitive actives like retinol. Advanced lipid fractionation units in Germany and Asia enable precise C8/C10 control, supporting the 2026 “speed-to-skin” absorption trend.

Pharma-grade triglyceride precision from Croda International Plc

Croda enters 2026 as a leader in high-purity, patented CCT chemistry for medical and prestige beauty markets. Its Crodamol™ GTCC line delivers ultra-low color, odor, and moisture content, ideal for anhydrous serums and lipsticks. A patented lipase-catalyzed process commercialized in 2025/2026 boosts triglyceride purity while cutting energy use by 20% . Croda’s Super Refined™ CCT grades are widely adopted as pharma excipients for lipid-based drug delivery systems, supporting the surge in oral and topical peptide therapies. Strategically, Croda emphasizes deforestation-free compliance, implementing RSPO Identity Preserved supply chains to ensure full plantation-level traceability for ESG-driven cosmetic and pharmaceutical customers.

Plantation-to-product CCT scale leadership by KLK OLEO

KLK OLEO stands out in 2026 as a vertically integrated powerhouse, leveraging upstream plantations to deliver cost-competitive, traceable caprylic capric triglycerides globally. Following its Temix Oleo acquisition, KLK now provides local-to-local CCT supply for European personal care brands. PALMERA™ and PALMESTER™ grades dominate food and beverage applications as vitamin carriers and clouding agents. Direct access to C8/C10 fatty acids from Malaysian and Indonesian refineries lowers logistics emissions while improving carbon performance. In early 2026, KLK expanded its sustainability traceability platform, enabling QR-based batch-level carbon impact visibility, reinforcing its leadership in transparent, plantation-backed CCT manufacturing.

Pharmacopeia-grade CCT innovation from IOI Oleo GmbH

IOI Oleo leads Europe’s life sciences-grade CCT segment with its MIGLYOL® and WITARIX® portfolios. MIGLYOL® 812 N remains the gold standard for injectable formulations and nutritional supplements in 2026, while WITARIX® MCT Powder AC8CN supports ketogenic and metabolic health markets through fiber-enriched delivery systems. The company’s Lipid Excellence Center in Germany acts as a co-development hub for customized triglyceride blends with pharma and nutraceutical startups. With FDA approval, GMP certification, and HACCP compliance, IOI Oleo serves infant formula and medical nutrition customers requiring the highest safety benchmarks, positioning itself as a cornerstone supplier for regulated CCT applications.

Performance nutrition and keto-focused CCT from Stepan Company

Stepan is a leading North American producer specializing in high-stability CCT for keto nutrition and performance energy. Its NEOBEE® series delivers rapid ketone generation without glucose spikes, making it a preferred ingredient in 2026 ketogenic formulations. Derived from coconut and palm kernel oil, Stepan’s proprietary multi-stage purification eliminates flavor interference, preserving organoleptic integrity in dairy alternatives and baked goods. The company also introduced STEPAN® 108 in 2026, expanding CCT use into technical fibers and bio-plastics as a lubricant and mold-release agent. Stepan’s strength lies in organoleptic purity and multifunctional performance across food and industrial markets.

Plant-based CCT and circular ester platforms by Oleon NV

Oleon positions itself in 2026 as Europe’s green specialist, supplying 100% plant-based CCT through its RADIA® series, including RADIA 7102K for sports nutrition and alcohol-free fragrances. Backed by Avril Group’s Triple Performance strategy, Oleon operates Belgian esterification plants on renewable energy, aligning economic growth with environmental impact. Its CCT is widely used in sun care and color cosmetics as a pigment dispersant, ensuring even zinc and titanium spread without white cast. Oleon’s integrated glycerin-to-triglyceride platform maximizes resource efficiency by valorizing fatty acid byproducts, reinforcing its leadership in low-impact, circular CCT manufacturing for cosmetics and nutrition.

Malaysia’s RSPO-Driven Vertical Integration and Life-Science Rebranding Strengthen Caprylic Capric Triglycerides Exports

Malaysia remains a structural cornerstone in the global Caprylic Capric Triglycerides (CCTG) industry, leveraging palm kernel oil (PKO) integration, sustainability certification, and export-oriented oleochemical infrastructure. In late 2025, KLK OLEO unveiled a refreshed global identity to reinforce its transformation into a life-science-focused organization, prominently positioning its PALMESTER CCTG series for high-end European cosmetics and pharmaceutical excipient markets. As a founding member of the RSPO, Malaysian producers have achieved nearly 98% traceability to the oil mill level for PKO used in fractionated C6–C10 fatty acid production, significantly enhancing supply chain transparency for EU buyers.

Manufacturing resilience is reinforced through global integration. The KLK Emmerich facility, strategically linked to Malaysian feedstock flows, expanded Pharma Grade MCT oil capacity in 2025 while ensuring Halal and Kosher certification compliance for cross-border exports. Under Malaysia’s National Energy Transition Roadmap (NETR), oleochemical plants have adopted biomass-based cogeneration to reduce the carbon footprint of energy-intensive CCTG distillation and esterification. The Port Klang petrochemical cluster recorded a 12% increase in specialized liquid ester bulk handling in 2025, accelerating deliveries to East Asian “Clean Beauty” production hubs. Responsible Sourcing Reports published during 2024–2025 highlight significant growth in “Mass Balance” certified triglycerides, ensuring compliance with the EU Deforestation Regulation (EUDR) and strengthening Malaysia’s premium CCTG positioning.

Indonesia’s B40 Mandate and Oleochemical 2.0 Strategy Expand C8–C10 Ester Production

Indonesia’s Caprylic Capric Triglycerides industry is structurally supported by biodiesel mandates and large-scale palm oil output. In March 2025, the government formally implemented the B40 biodiesel mandate, reshaping domestic availability of PKO and glycerin—critical precursors for CCTG esterification. Palm oil production is projected to reach 47 million metric tons in the 2025/26 cycle, ensuring a stable and cost-competitive raw material base for producers such as Musim Mas and Apical.

In February 2025, the Ministry of Energy and Mineral Resources (ESDM) initiated B50 pilot testing, which is expected to further expand refinery capacity and lower C8 and C10 fatty acid production costs. Under the “Making Indonesia 4.0” framework, tax holidays for the “Oleochemical 2.0” phase are specifically targeting specialty esters rather than crude fatty acids, accelerating value-added CCTG manufacturing. A 2024–2025 sustainability partnership between Solidaridad and Fedepalma has improved certification compliance across 6,700 growers, securing traceable feedstock for export-grade triglycerides. Additionally, the PT Apical Kao Chemicals plant completed its capacity ramp-up in late 2024, stabilizing high-purity fractionated oil supply for Japanese and ASEAN personal care markets.

United States’ Specialty Product Surge and Pharmaceutical MCT Innovation Elevate CCTG Demand

The United States Caprylic Capric Triglycerides market is shaped by specialty chemical innovation, pharmaceutical demand, and pricing volatility. In late 2024, Stepan Company achieved operational milestones at its Pasadena, Texas alkoxylation facility, strengthening domestic production of high-performance surfactants and triglyceride-based emulsifiers. For the quarter ending September 2025, the U.S. Specialty Product segment—including CCTG—reported a 68% increase in net sales, largely driven by pharmaceutical excipient demand and order fluctuations.

Price dynamics remain sensitive: the North American CCTG Price Index rose in Q3 2025, influenced by a 2.6% increase in the Producer Price Index and higher natural gas costs affecting esterification margins. In parallel, 2025 research collaborations involving U.S. institutions identified Tricaprin (C10-rich MCT) as a breakthrough therapy for Triglyceride Deposit Cardiomyovasculopathy (TGCV), reinforcing pharmaceutical-grade CCTG utilization. Retail momentum also remains strong, with consumer spending up 5.42% in late 2025, driving demand for non-comedogenic, mineral-oil-free triglycerides in prestige skincare. Tariff pressures on coconut oil imports have further shifted formulators toward palm-derived C8/C10 blends sourced from Southeast Asia.

Germany’s Green Chemistry Lipids and Bioavailability Research Drive High-Purity CCTG Applications

Germany remains a European innovation hub for pharmaceutical-grade Caprylic Capric Triglycerides, emphasizing green chemistry, regulatory compliance, and high-purity production. BASF and IOI Oleo GmbH are advancing FDA-approved and GMP-certified CCTG for soft capsule fillings and nutraceutical formulations. In 2025, IOI Oleo demonstrated through technical data that its MIGLYOL® and WITARIX® MCT series enhance bioavailability of lipophilic active pharmaceutical ingredients, strengthening CCTG’s role as a carrier lipid.

Sustainability remains central. BASF’s Care Chemicals division achieved a 98.1% RSPO-certified palm footprint in 2024, setting a European benchmark in responsible sourcing. German production sites have integrated advanced distillation and purification systems capable of delivering purity levels suitable for high-sensitivity injectables and infant nutrition. In 2025, Croda International launched a B2B e-commerce platform enabling indie beauty brands in Germany to access small-volume, high-purity triglycerides. BASF’s €5.2 billion capital investment forecast for 2025 prioritizes “Verbund” site optimization, reinforcing carbon-neutral fatty acid ester production and strengthening Germany’s premium CCTG supply chain.

China’s Competitive Pricing Environment and Verbund-Style Expansion Influence CCTG Export Flows

China’s Caprylic Capric Triglycerides market is defined by competitive pricing, manufacturing scale, and export-oriented regulatory reforms. In Q3 2025, the domestic CCTG Price Index declined amid a -2.3% year-over-year drop in the Producer Price Index, intensifying margin pressure but enhancing export competitiveness. Despite a 6.5% increase in industrial production, the specialty chemicals Manufacturing Index faced contraction, creating a temporary surplus of food-grade CCTG for international markets.

New 2025 draft regulations issued by the Ministry of Agriculture and Rural Affairs (MARA) streamlined export registration for chemical agents, benefiting large exporters such as Hubei Qifei Pharmaceutical. While mid-2025 cosmetics retail sales improved, a Consumer Confidence Index of 89.6 has shifted domestic demand toward value-based, locally manufactured triglyceride formulations. The commissioning of new Verbund-style petrochemical complexes by multinational corporations in China is expected to reduce costs for organic co-stabilizers and esterification catalysts by 2026, further strengthening domestic CCTG production economics.

India’s Fastest-Growing Cosmetics Market and PLI Incentives Accelerate C8–C10 Triglyceride Adoption

India’s Caprylic Capric Triglycerides industry is gaining momentum, supported by rapid cosmetic consumption growth and pharmaceutical innovation. As the world’s fastest-growing cosmetics market, India is attracting international triglyceride producers planning localized CCTG production within the next five years to meet escalating demand for non-greasy emollients and clean-label skincare ingredients.

The Indian pharmaceutical sector is increasingly incorporating medium-chain triglyceride oils as excipients to enhance oral drug bioavailability, particularly for poorly soluble active ingredients. Under the Production Linked Incentive (PLI) Scheme for specialty chemicals, domestic oleochemical firms are upgrading fractionation towers to produce high-purity caprylic (C8) acid, a critical precursor for pharmaceutical-grade CCTG. Simultaneously, a 2025 surge in keto-based dietary supplements has amplified domestic demand for C6–C10 triglycerides, with refineries prioritizing Food Grade certifications to capture nutraceutical and wellness segment growth. This convergence of cosmetics, pharma, and functional nutrition applications positions India as a high-growth CCTG demand center within Asia-Pacific.

Caprylic Capric Triglycerides (MCT Oil) Market Report Scope

Caprylic Capric Triglycerides Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$8 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Source (Coconut Derived, Palm Derived, Other Sources), By Form (Liquid, Emulsion, Powder), By Grade (Pharmaceutical Grade, Food and Nutraceutical Grade, Cosmetic Grade, Industrial Grade), By Application (Personal Care, Nutraceuticals, Pharmaceuticals, Food and Beverages, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Croda International, IOI Oleo, KLK OLEO, Wilmar International, Oleon, Stepan Company, Berg and Schmidt, Ecogreen Oleochemicals, Emery Oleochemicals, Lonza Group, Procter and Gamble, DSM, Musim Mas, Platinum Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Caprylic Capric Triglycerides Market Segmentation

By Source

- Coconut Derived

- Palm Derived

- Other Sources

By Form

By Grade

- Pharmaceutical Grade

- Food and Nutraceutical Grade

- Cosmetic Grade

- Industrial Grade

By Application

- Personal Care

- Nutraceuticals

- Pharmaceuticals

- Food and Beverages

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Caprylic Capric Triglycerides Industry

- BASF SE

- Croda International

- IOI Oleo

- KLK OLEO

- Wilmar International

- Oleon

- Stepan Company

- Berg and Schmidt

- Ecogreen Oleochemicals

- Emery Oleochemicals

- Lonza Group

- Procter and Gamble

- DSM

- Musim Mas

- Platinum Industries

*- List not Exhaustive