Market Overview: High-Conductivity, Lightweight Carbon Foams Powering Thermal Management & Advanced Composites

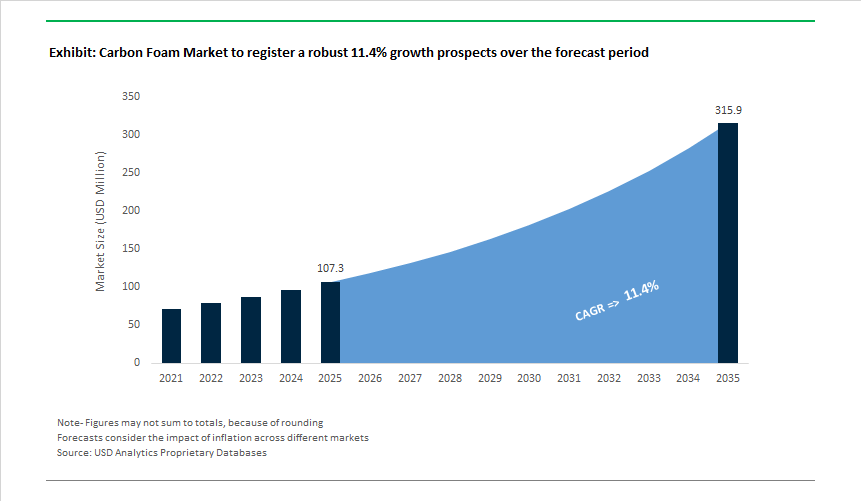

The Carbon Foam Market is valued at USD 107.3 million in 2025 and is projected to reach USD 315.8 million by 2035, expanding at an 11.4% CAGR as thermal management, lightweighting, and high-temperature performance become binding constraints across aerospace, defense, semiconductors, and advanced energy systems. Today, carbon foam is no longer treated as an experimental carbon form; it is being specified as a performance-enabling material in applications where conventional metals, alloys, and ceramics fail to balance heat dissipation, mass reduction, and thermal stability.

Growth is being anchored first by thermal management intensity. As power densities rise in semiconductors, EV battery packs, power electronics, and LED systems, heat removal has become a system-level bottleneck rather than a packaging challenge. Graphitic carbon foams, with thermal conductivity typically in the 150-300 W/m·K range, are increasingly adopted as heat spreaders, cold plates, and thermal cores because they outperform many metals on a weight-normalized basis while maintaining dimensional stability at elevated temperatures. For OEMs, this translates into higher power throughput, longer component life, and simplified cooling architectures, directly impacting reliability and total cost of ownership.

A second structural driver is extreme lightweighting combined with functional integration. Carbon foams offer commercially viable density ranges from ~0.05 to 0.6 g/cm³, enabling dramatic mass reduction without sacrificing thermal or electrical functionality. Aerospace and defense platforms increasingly use carbon foam in sandwich cores, radar systems, and thermal-structural components where every kilogram removed improves payload efficiency, range, or survivability. Unlike polymer foams, carbon foams retain integrity under high thermal loads, making them suitable for environments where temperature and vibration coexist.

Energy storage and electrochemical systems represent a high-value expansion vector. Engineered carbon foams with 80-95% open porosity are being designed into bipolar plates, flow battery electrodes, and emerging 3D current collector architectures, where surface area, fluid permeability, and electrical conductivity directly determine system efficiency. As battery and hydrogen technologies evolve toward higher current densities and thicker electrodes, carbon foam architectures are increasingly favored over planar metal designs due to their three-dimensional charge transport and thermal dissipation advantages.

From a manufacturing and competitive standpoint, value creation is shifting toward process control and customization, not raw material availability. Producers are investing in precursor selection (pitch vs resin), high-purity graphite sourcing, controlled graphitization, and additive-manufacturing-enabled geometries to tailor density, pore size, and mechanical strength for specific end uses. Importantly, modest density adjustments can significantly enhance mechanical performance-allowing suppliers to offer application-specific strength-weight trade-offs rather than one-size-fits-all products.

At the high-performance extreme, carbon foams derived from pitch and advanced resins maintain structural stability at temperatures exceeding 2,000°C in non-oxidizing environments, reinforcing their relevance in aerospace propulsion, defense systems, and next-generation energy infrastructure. These characteristics position carbon foam not as a substitute material, but as a capability unlocker where traditional design envelopes are being pushed outward.

Market Analysis: R&D Acceleration, Additive Manufacturing Adoption & New Precursor Pathways Strengthen Carbon Foam Commercialization

Recent developments indicate rising momentum in material innovation, manufacturing method diversification, and high-performance composite engineering. In October 2025, global research teams demonstrated that Carbon Foam-based 3D current collectors can boost battery areal capacity by up to 4.3 mAh/cm², validating its pivotal role in next-generation energy storage. By November 2025, industry reports highlighted increased integration of carbon nanotubes (CNTs) and graphene into Graphitic Carbon Foams, enabling dramatic improvements in mechanical strength while retaining exceptional thermal conductivity-an important shift for aerospace and EV thermal structures.

In July 2025, Entegris POCO Materials expanded its EDM-AF5® Angstrofine graphite line, signaling ongoing investment into high-purity, fine-grain graphite precursors essential for premium Carbon Foam manufacturing. On the other hand, May 2025 marked significant adoption of additive manufacturing techniques to create customized Carbon Foam geometries for complex cooling systems-particularly relevant for aerospace, hypersonics, and advanced electronics packaging. Researchers also demonstrated in March 2025 the viability of producing Carbon Foam from biomass waste, such as bamboo powder, providing a scalable, sustainable pathway that reduces dependence on coal- or pitch-derived precursors.

Geographically, the market saw expansion initiatives that reinforce supply chain maturity. In February 2025, SGL Carbon invested in its Meitingen facility to expand high-purity graphite production-materials that share processing routes with Graphitic Carbon Foam. Earlier developments in November 2024 revealed increased use of Carbon Foam in EV battery thermal barriers, addressing rising safety and heat dissipation requirements. On the other hand, September 2024 highlighted Koppers’ strategic emphasis on Carbon Materials for defense applications requiring extreme temperature tolerance and lightweight structural integrity.

Carbon Foam Market Trends and Opportunities

Trend 1: High-Thermal-Conductivity Graphitic Foams for Satellite and Spacecraft Thermal Control

Space systems are increasingly constrained by power density rather than payload mass, forcing spacecraft designers to rethink passive thermal architectures.

Structural heat spreading is replacing discrete heat sinks. In 2025, NASA TechPort documentation highlights that mesophase pitch-derived graphitic foams enable double-digit percentage mass reductions when integrated as multifunctional structural cores. Instead of bolting aluminum heat sinks onto electronics, carbon foam is embedded directly into load-bearing panels, distributing heat laterally while preserving stiffness.

Specific thermal conductivity is the decisive metric. Research from Oak Ridge National Laboratory confirms that aligned graphitic ligaments inside carbon foam exhibit intrinsic thermal conductivity of 700–1,200 W/m·K. When normalized for density (~0.5 g/cm³), this gives carbon foam a thermal conductivity-to-weight ratio several times higher than aluminum or copper, making it ideal for smoothing transient heat loads from radar, power conditioning units, and electric propulsion subsystems.

Space qualification is accelerating adoption. Aerospace-grade foams such as POCO FOAM® demonstrate exceptionally low outgassing (TML ≈ 0.031% under ASTM E595), a non-negotiable requirement for optical payloads and infrared sensors. This performance positions carbon foam as a default material for next-generation satellite constellations where thermal stability, vacuum compatibility, and contamination control intersect.

Trend 2: Conductive Carbon Foam as Metal-Free Electrodes in Long-Duration Energy Storage

As grid operators pivot toward 8–24 hour storage durations, electrochemical efficiency and lifetime are overtaking raw energy density as procurement priorities.

Electrode architecture is being redefined. Studies published during 2024–2025 show that carbon-foam-based electrodes can replace both the electrode and current collector in vanadium redox flow batteries. Nitrogen-doped and surface-engineered foams have demonstrated voltage efficiencies above 73% at 200 mA/cm², outperforming conventional graphite felt by more than 11 percentage points at industrially relevant current densities.

Three-dimensional conductivity reduces system losses. Carbon foam’s continuous, open-cell network dramatically lowers ohmic resistance, enabling zero-gap cell designs that minimize electrolyte and membrane losses. This is particularly valuable for grid-scale systems, where even single-digit efficiency gains compound into material reductions across megawatt-hour installations.

Durability aligns with grid economics. Advanced carbon foams offer surface areas exceeding 4 m²/g while maintaining structural integrity across 500+ high-current cycles in laboratory testing. This stability directly addresses the expectation that stationary storage assets must operate for 15,000–20,000 cycles with minimal performance degradation, a threshold where metallic current collectors become corrosion-limited.

Opportunity 1: Fire-Safe, Low-Smoke Core Materials for Rail and Maritime Transport

Regulatory shifts are creating a clear opening for inherently non-combustible structural cores that reduce reliance on chemical flame retardants.

Rail safety standards are a catalyst. Under EN 45545-2, materials used in European rolling stock must meet stringent smoke toxicity and heat release limits. Carbon foam qualifies for HL3 (Hazard Level 3) applications—the most demanding category—due to its negligible smoke generation and thermal stability. This positions it for ceilings, wall panels, and equipment housings in long-tunnel and underground rail systems.

Maritime regulations favor non-polymeric solutions. Amendments to SOLAS Chapter II-2 and the HSC Code, effective January 2026, emphasize structural fire safety while discouraging materials associated with PFAS-based flame retardants. Carbon foam’s inorganic nature allows it to withstand extreme temperatures without releasing toxic combustion byproducts, making it attractive for passenger vessel bulkheads and offshore accommodation modules.

Impact resistance adds secondary value. Composite studies from 2025 show foam-based structures absorbing ~28 J/g of puncture energy, vastly exceeding steel on a mass-normalized basis. This opens additional use cases in armored transport, battery enclosures, and hazardous-goods containment where fire safety and impact tolerance must coexist.

Opportunity 2: Ultra-High-Temperature Insulation for Semiconductor Crystal Growth

The expansion of SiC, GaN, and SOI wafer production is driving demand for furnace materials that combine extreme thermal stability with chemical purity.

PVT SiC growth requires non-contaminating insulation. Silicon carbide sublimation processes operate above 2,000°C (≈2,273 K), where conventional ceramics degrade and metallic shields contaminate the growth environment. Carbon foam is increasingly specified as the primary thermal insulation surrounding graphite crucibles because it remains dimensionally stable while avoiding foreign elemental introduction.

Purity thresholds are tightening. Semiconductor-grade carbon foams are now refined to <10 ppm total impurities, with some grades achieving <9 ppm. This is critical to prevent trace boron or nitrogen contamination that can unintentionally dope SiC crystals and degrade device yield.

Capacity expansion mirrors chip onshoring. In 2025, suppliers such as Entegris (POCO Graphite) announced expansions in high-performance graphite and carbon foam manufacturing. These investments are directly linked to the onshoring of wide-bandgap semiconductor supply chains and the surge in demand for consumables capable of surviving repeated high-temperature growth cycles.

Market Share Analysis: Carbon Foam Market

Market Share by Product Form: Blocks & Billets Anchor Precision-Driven Carbon Foam Demand

Blocks and billets account for approximately 45% of the carbon foam market because they are the only product form that supports monolithic, precision-machined thermal structures at scale—a non-negotiable requirement in aerospace, defense, and high-end industrial systems. In 2024–2025 alone, global output of carbon foam blocks exceeded 4,200 metric tons, largely driven by aerospace tooling programs and battery shielding platforms that require tight dimensional tolerances rather than cut-and-fit insulation. Despite their ultra-high porosity, these blocks deliver compressive strengths in the 3.5–5 MPa range, enabling 10× tighter machining precision than fibrous or bonded alternatives. This machinability allows engineers to carve integrated heat spreaders, EMI/Faraday enclosures, and structural thermal barriers from a single billet—eliminating joints, adhesives, and thermal weak points. Scale further reinforces dominance: standardized large-format billets (~97 × 46 × 5+ cm) have become the industry default because they reduce bond-line count in shipboard, reactor, and aerospace thermal shields, directly improving reliability under thermal cycling. At a density of roughly 0.5–0.55 g/cc, these blocks deliver metal-like thermal performance at one-fifth the weight of aluminum, making them structurally and economically irreplaceable for buyers optimizing weight, reliability, and lifecycle cost simultaneously.

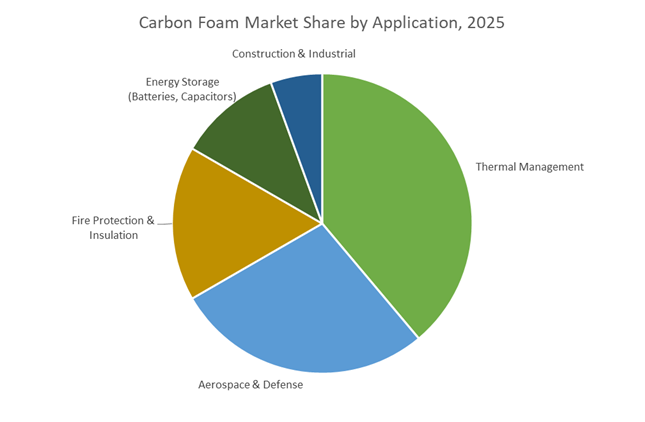

Market Share by Application: Thermal Management Leads Through Extreme Heat-Flux Control

Thermal management represents around 35% of total carbon foam demand because carbon foam uniquely functions as a “thermal sponge”, capable of absorbing, spreading, and dissipating extreme heat loads faster than any competing lightweight material. In 2025-spec systems, graphite-based foams demonstrate bulk thermal conductivity of 120–180 W/m·K, outperforming aluminum foams by an order of magnitude and redefining cooling architectures for EV inverters, power electronics, and high-density data infrastructure. This performance translates directly into system-level value: EV pilot programs integrating carbon foam into battery modules reported a 15% extension in cell life, driven by faster heat evacuation during aggressive fast-charging regimes (≥4C). At the high end, foam-based heat exchangers have demonstrated heat-flux handling above 2,200 W/cm², a threshold that positions carbon foam as a critical enabler for next-generation laser systems, GaN/SiC RF modules, and compact 5G base stations. Equally important for aerospace and defense buyers is fluid efficiency—carbon foam’s up to 96% open-cell porosity reduces pressure drop in liquid-cooled systems by as much as 300%, allowing smaller pumps, lower parasitic losses, and lighter thermal loops. These combined thermal, fluidic, and weight advantages explain why thermal management remains the largest and most value-dense application segment in the carbon foam market.

Competitive Landscape: Advanced Graphite Processing, Energy Storage Integration & High-Temperature Solutions Define Market Leadership

The competitive landscape of the Carbon Foam Market is shaped by companies that excel in graphite purification, precursor material engineering, high-temperature carbon processing, and application-specific foam architectures. Leading manufacturers differentiate through vertical integration, proprietary carbonization technologies, and strong positioning in thermal management and aerospace-grade composites.

SGL Carbon SE - Global Graphite Leader Driving High-Performance Energy Storage and Lightweight Composites

SGL Carbon remains a dominant force in specialty graphitic materials, supplying key products such as SIGRACELL® graphite plates for bipolar energy storage systems-sharing technological synergies with Graphitic Carbon Foams. These composites achieve ultra-high thermal conductivity of up to 350 W/m·K, reinforcing SGL’s relevance in advanced thermal applications. With full control over raw material sourcing and purification (>99.7% purity), the company ensures consistent quality for semiconductor, aerospace, and automotive applications. Its strategic footprint spans advanced lightweighting and thermal systems, positioning SGL at the center of next-generation Carbon Foam demand.

Entegris (POCO Materials) - Precision Graphite Specialist Enabling High-Purity Carbon Foam Precursors

Entegris’ POCO Graphite line is recognized for its uniform microstructure, precise porosity control, and superior mechanical stability-key attributes for Carbon Foam precursor consistency. The company supplies ultra-high-purity graphite and SiC materials for semiconductor equipment, aerospace systems, and glass forming, all requiring extreme thermal and dimensional stability. Ongoing investment in its Arkansas plant strengthens production capacity for critical graphite grades used in EDM machining, high-temperature components, and foam precursor manufacturing, aligning with the global shift toward fine-grain Graphitic Carbon Foams.

Koppers Inc. - Major Precursor Supplier With Strong Industrial Carbon Materials Capability

Koppers is a leading provider of coal tar pitch, the primary precursor for many industrial-grade, pitch-based Graphitic Carbon Foams. Its expertise in high-temperature carbon processing supports large-scale production of anodes for aluminum smelting and graphite electrodes, demonstrating mastery of carbon conversion chemistry. The company leverages its Carbon Materials & Chemicals segment to supply railroad, utility, and emerging battery markets, while also investigating enhanced carbon materials for lightweight composites and energy storage. Its established logistics and supply chain scale give it competitive advantage for high-volume Carbon Foam precursors.

CFOAM Ltd. - Niche Producer Specializing in Cost-Effective, Fire-Resistant Carbon Foams For High-Temperature Insulation

CFOAM focuses on pitch- and coal-derived Carbon Foams optimized for structural rigidity, fire resistance, acoustic dampening, and high-temperature insulation. Its products serve construction, industrial heating, and aerospace segments requiring lightweight, non-flammable thermal barriers. The company’s rigid Carbon Foam materials provide strong vibration damping and excellent compressive strength, making them suitable for machinery bases and protective structures. CFOAM is actively expanding into automotive and industrial sectors where cost-effective thermal and structural performance is essential.

The United States is shaping the commercial backbone of the global carbon foam market, driven by federal decarbonization goals and defense-led procurement. In October 2025, the Department of Energy’s $625 million Coal-to-Products funding program formally elevated carbon foam from a research material to a priority industrial product. The program is designed to convert domestic coal feedstock into high-value carbon foam blocks for construction formwork, aerospace tooling, and thermal management systems, enabling coal-state regions to pivot toward advanced materials manufacturing.

Parallel defense demand has accelerated adoption. Graphite One Inc. advanced its $4.7 million Defense Logistics Agency (DLA) contract to develop graphite-based carbon foam fire suppressants, positioning carbon foam as a PFAS-free alternative for military and civil fire safety. Meanwhile, CFOAM LLC, headquartered in West Virginia, expanded production of large-format structural carbon foam panels for electromagnetic interference (EMI) shielding and blast mitigation on U.S. Navy platforms. Collectively, these initiatives anchor the U.S. as the technology and standards setter for defense-grade and structural carbon foam applications.

China: EV Battery Thermal Management and Electronics Cooling Scale

China is leveraging its dominance in graphite resources to scale micro-porous carbon foam for electronics and electric mobility. Under the MIIT Green Standardization Plan (June 2025), carbon footprint benchmarks for telecom and electronics infrastructure accelerated adoption of carbon foam in passive cooling systems for 5G base stations, where thermal conductivity of 120–180 W/mK materially outperforms aluminum and polymer alternatives.

The most significant pull, however, comes from electric vehicles. By 2024–2025, carbon foam had been integrated into over 1.6 million EV battery packs, improving thermal dissipation and extending battery life by up to 15%—a decisive advantage for high-density packs used by domestic OEMs. Complementing scale, research clusters in Nanjing and Shanghai reported early-2025 breakthroughs in bio-based carbon foam synthesis using agricultural waste, targeting ~20% cost reductions. This positions China to dominate cost-optimized, high-volume carbon foam supply for EVs and electronics.

Germany: Euro 7 Lightweighting and Industrial Decarbonization

Germany’s carbon foam strategy is tightly coupled with Euro 7 compliance and automotive lightweighting. As emission standards tightened in 2025, German OEMs accelerated the use of carbon-foam core sandwich structures in vehicle underbodies. These components combine high crash-energy absorption with 2.3–4.5% vehicle weight reduction, directly supporting fleet CO₂ targets without compromising safety.

At the materials level, BASF’s Performance Materials roadmap emphasizes recycled-content and hybrid foam structures, pairing carbon foam with polymer-derived ceramics for high-temperature furnace linings. Simultaneously, federal industrial decarbonization grants have prioritized “Green Refractories,” funding carbon foam as a lower-energy alternative to ceramic bricks in kilns and metallurgical furnaces. Germany thus emerges as the automotive and industrial decarbonization reference market for structural carbon foam.

Australia: Export-Oriented Value Addition and Aerospace Tooling

Australia is repositioning carbon foam within its critical-minerals and defense-ready industrial strategy, shifting from raw exports toward high-value processed carbon products. While production is largely offshore, CFOAM Limited (ASX: CFO) maintains its strategic hub in Australia and, in 2025, expanded aerospace tooling partnerships. Coal-derived carbon foam tooling boards are increasingly specified for carbon-fiber composite molds due to matched thermal expansion coefficients and superior dimensional stability.

Government policy reinforces this pivot. Australia’s Critical Minerals Strategy explicitly recognizes high-purity carbon materials as essential for sovereign defense capability, supporting domestic qualification of carbon foam for maritime thermal shields and aerospace tooling. This positions Australia as a value-added exporter rather than a commodity supplier in the carbon foam ecosystem.

India: Carbon Credit Trading and Industrial Efficiency Pull

India’s carbon foam demand is being catalyzed by regulation rather than defense or EV scale. The Carbon Credit Trading Scheme (CCTS) 2025, notified in October, imposed binding emission-intensity targets across nine heavy industries, including cement and aluminum. Facilities that fail to comply face penalties set at twice the prevailing carbon credit price, creating immediate economic incentives to deploy carbon foam insulation for furnaces, kilns, and heat-intensive processes.

In parallel, the “Make in India” advanced materials agenda has prioritized specialty carbon under PLI frameworks, encouraging domestic development of carbon-foam heat sinks for electronics manufacturing. As a result, India is emerging as a regulation-driven growth market for industrial-grade carbon foam, particularly in thermal insulation and energy-efficiency retrofits.

Japan: Precision Thermal Management for Semiconductors and Robotics

Japan’s carbon foam market is defined by precision engineering rather than scale. In 2024–2025, Japanese electronics and robotics firms increased consumption of specialty carbon foams to ~180 metric tons, primarily for IC chip protection, semiconductor packaging, and high-speed robotic arms where low inertia and thermal stability are critical performance metrics.

Looking forward, Japan’s METI GX 2040 Vision is funding R&D into pitch-based carbon foam for liquid hydrogen storage tanks, targeting enhanced thermal safety during transport and storage. This aligns carbon foam with Japan’s hydrogen economy ambitions, positioning the country as a leader in high-purity, application-specific carbon foam for semiconductors, robotics, and hydrogen infrastructure.

2025 Strategic Matrix: Carbon Foam National Comparison

Carbon Foam Strategic Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material Focus

|

|

United States

|

Defense & coal-to-products

|

$625M DOE coal revitalization funding

|

Large-format blocks, fire-suppressant foams

|

|

China

|

EVs & electronics cooling

|

1.6M EV battery packs integrated

|

Micro-porous thermal heat sinks

|

|

Germany

|

Automotive (Euro 7)

|

Carbon-foam underbody lightweighting

|

Recycled carbon & structural foams

|

|

Australia

|

Aerospace tooling

|

Expansion of CFOAM aerospace partnerships

|

Coal-based tooling boards

|

|

India

|

CCTS regulatory compliance

|

Binding emission-intensity mandates

|

Industrial thermal insulation foams

|

|

Japan

|

Robotics & semiconductors

|

GX 2040 hydrogen storage R&D

|

Pitch-based, high-purity foams

|

Carbon Foam Market Report Scope

Carbon Foam Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$107.3 Million

|

|

Market Size (2035)

|

$315.8 Million

|

|

Market Growth Rate

|

11.4%

|

|

Segments

|

By Material Type (Coal-Based, Graphite-Based, Asphalt-Based, Pitch-Based, Nanocomposite-Enhanced), By Product Form (Blocks, Sheets/Plates, Customized Molded Parts, Powders/Particles), By Application (Thermal Management, Aerospace & Defense, Fire Protection, Energy Storage, Construction)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Koppers Inc., ERG Aerospace Corporation, CFOAM LLC, Graphite One Inc., Pithore Alloys Pvt. Ltd., Sinotek Materials Co. Ltd., Ultramet, Poco Graphite, American Elements, VARTA AG, Samsung SDI, Mitsubishi Chemical Group, Xiamen Zopin New Material Limited, AvCarb Material Solutions, Tata Steel (Advanced Materials Division)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Carbon Foam Market Segmentation

By Material Type

- Coal-based Carbon Foam

- Graphite-based Carbon Foam

- Asphalt-based Carbon Foam

- Pitch-based Carbon Foam

- Nanocomposite-enhanced Carbon Foam

By Product Form

- Blocks

- Sheets/Plates

- Customized Molded Parts

- Powders/Particles

By Application

- Thermal Management

- Aerospace & Defense

- Fire Protection

- Energy Storage

- Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Carbon Foam Market

- Koppers Inc.

- ERG Aerospace Corporation

- CFOAM LLC

- Graphite One Inc.

- Pithore Alloys Pvt. Ltd.

- Sinotek Materials Co., Ltd.

- Ultramet

- Poco Graphite

- American Elements

- VARTA AG

- Samsung SDI

- Mitsubishi Chemical Group

- Xiamen Zopin New Material Limited

- AvCarb Material Solutions

- Tata Steel (Advanced Materials Division)

*- List not Exhaustive