Market Overview: Graphite Electrode Demand Anchored in EAF Steelmaking and UHP Performance

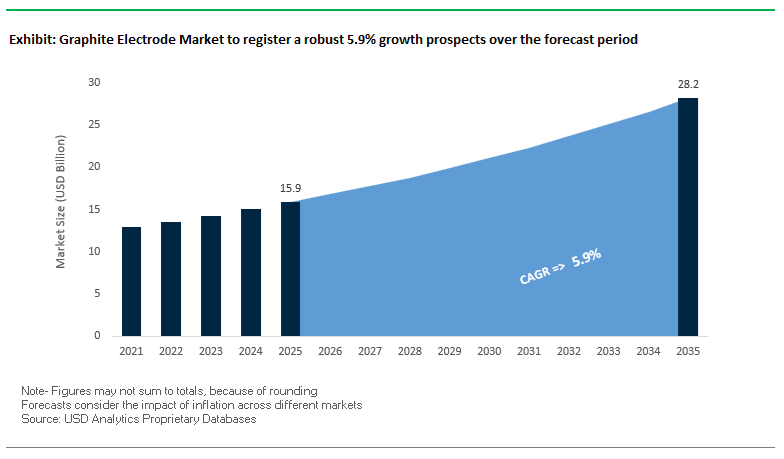

The global Graphite Electrode Market is projected to grow from USD 15.9 billion in 2025 to approximately USD 28.2 billion by 2035, registering a steady CAGR of 5.9% (2025–2035). This expansion is closely linked to the accelerating shift toward Electric Arc Furnace (EAF) steelmaking, where graphite electrodes are an irreplaceable consumable, and to the premiumization of demand toward Ultra-High Power (UHP) graphite electrodes. For graphite electrode manufacturers and needle coke suppliers, the decade is characterized by capacity realignment, technology upgrades for higher current densities, and intensified competition for raw materials driven by the fast-growing battery anode industry. Vendors that can consistently deliver large-diameter, high-density UHP grades with low specific consumption will be best positioned to capture value as green steel and mega-EAFs scale globally.

Key insights for graphite electrode manufacturers and vendors:

- EAF steelmaking penetration: Around 30% of global crude steel production in 2025 is based on EAF routes that exclusively rely on graphite electrodes, underscoring structural, long-term demand for electrodes in scrap-based and low-carbon steelmaking.

- Premium UHP performance benchmark: Modern UHP graphite electrodes for high-intensity EAFs are designed to withstand continuous current densities above 25 A/in², delivering robust thermal shock resistance and electrical stability in extremely harsh furnace conditions.

- Mega-EAF and large-diameter trend: The industry shift toward mega EAF units is driving demand for 600 mm and above electrode diameters (including 700–800 mm), which support higher power input, shorter tap-to-tap times, and improved furnace productivity.

- Needle coke supply risk: The reliance on petroleum needle coke for UHP grades is increasingly exposed to competition from the rapidly expanding lithium-ion battery anode segment, resulting in persistent raw material price volatility and strategic sourcing pressures.

- Consumption optimization: Advanced electrode formulations and AI-enabled EAF control systems are reducing specific electrode consumption, with leading mills achieving less than 1.6 kg of graphite electrode per ton of steel, pushing suppliers to differentiate on life extension and performance consistency.

Market Analysis: Capacity Rationalization, Indian Expansions, and Energy-Transition Diversification

The global graphite electrode industry is entering a structurally tighter yet more technology-driven phase, shaped by capacity closures in some regions and aggressive expansions in others. In July 2025, Resonac Holdings (formerly Showa Denko) announced the closure of selected graphite electrode units in China and Malaysia, explicitly to optimize its global footprint and concentrate on higher-margin, high-spec UHP products. Similarly, Tokai Carbon unveiled a production optimization plan in July 2024, reducing graphite electrode capacity in Japan and Europe from 56,000 tons to 32,000 tons by July 2025, and later finalized the divestiture of its subsidiary Tokai Erftcarbon GmbH (TEG) in 2025. These moves collectively signal a disciplined supply-side response to fluctuating steel cycles and raw material pressures, while strengthening focus on technologically advanced, value-added electrode grades.

On the growth side, India is emerging as one of the most dynamic centers for graphite electrode capacity expansion, aligned with the surge in EAF steel projects and green steel policies. HEG Limited announced in August 2025 a major expansion of 15,000 TPA for its graphite electrode and related products, directly targeting rising global demand for large-diameter UHP electrodes. In parallel, Graphite India Limited revealed a capacity expansion of 25,000 TPA in August 2025, boosting its total graphite electrode capacity to 105,000 TPA, backed by an investment of around INR 600 crore. These expansions position Indian producers as critical suppliers for both domestic and export EAF markets, particularly as global steelmakers accelerate decarbonization and shift from basic oxygen furnaces to electric furnaces.

At the same time, leading players are strategically diversifying their carbon expertise toward energy-transition and battery-related applications, which will influence long-term graphite electrode market dynamics. GrafTech International has been strengthening its operational footprint, expanding its presence in Dubai in April 2023 and broadening its technical and commercial support across the U.S. in November 2025, while executing a dedicated CapEx program of around USD 40 million in 2025 to align its UHP electrode output with new EAF projects. HEG Limited secured initial approval in May 2024 to demerge its graphite business into a separate entity (expected completion by end-2025), unlocking value and enabling sharper strategic focus. Graphite India acquired a 31% stake in GODI India in 2025 for INR 50 crore, leveraging its carbon and process expertise to participate in lithium-ion and sodium-ion battery materials. Together, these developments underscore that the Graphite Electrode Market is no longer just a cyclical steel-input market but a strategic node at the intersection of green steel, EV batteries, and advanced carbon materials.

Breakthrough Trends Enhancing Ultra-High-Power (UHP) Electrode Performance and Extending Furnace Productivity

Market Trend 1: Global Expansion of Large-Diameter UHP Graphite Electrode Capability to Support High-Power EAF Steelmaking

A defining technological trend in the graphite electrode industry is the rapid expansion of large-diameter ultra-high-power (UHP) electrode capacity, driven by the shift toward high-efficiency Electric Arc Furnace (EAF) steelmaking. Graphite electrodes remain the only industrial material capable of withstanding arc core temperatures that exceed their sublimation point of ≈3,800°C (≈6,872°F). This extraordinary thermal resilience secures their indispensability for UHP operations, where electrical and mechanical stresses are extreme.

UHP electrodes are engineered for exceptionally stable electrical resistivity that remains nearly constant even at temperatures approaching 1,400°C, enabling consistent current flow and improved EAF energy efficiency. Their mechanical structure improves with heat: tensile strength increases by ≈1.6× at 2,000°C, ensuring structural integrity during intense arc cycles and mechanical shock events.

The adoption of large-diameter electrodes—600 mm and above—combined with high-power transformers allows operators to shorten tap-to-tap cycles. Studies show a ≈13% reduction in single-furnace refining time, enabling higher melt throughput, higher energy efficiency, and significant operational cost reductions. As global steelmaking shifts toward low-carbon pathways, these high-performance UHP electrodes become essential for maximizing productivity and supporting green steel ambitions.

Market Trend 2: Advancements in Anti-Oxidation Coatings and Raw Material Engineering to Extend Electrode Service Life

A second major trend is the acceleration of R&D into coating technologies and raw material optimization, which directly address the largest consumption factor for graphite electrodes: side oxidation. Advanced ceramic and inorganic coatings have demonstrated the ability to reduce electrode oxidation losses by 15% to over 50%, depending on furnace conditions. These technologies directly translate to substantial reductions in electrode consumption and furnace downtime.

Field results confirm that protective coatings can extend electrode service life by 22% to 60%, significantly improving asset utilization and lowering operating expenses for steel producers. Material innovations are also contributing: Mg(OH)₂-based coatings decompose at high temperatures into MgO with a melting point of ≈2,850°C, forming a dense physical barrier that seals pores and prevents oxygen ingress during furnace exposure.

Simultaneously, breakthroughs in baking, graphitization, and carbon-structure engineering—including nano-additives and carbon-fiber reinforcement—have delivered 10% to 15% improvements in mechanical strength, making electrodes more resistant to breakage, thermal shock, and electrode tip consumption. These advancements are creating a new generation of high-durability electrodes aligned with modern EAF operational demands.

Strategic Opportunities Supporting Battery-Grade Graphite Development and Closed-Loop Electrode Recycling

Market Opportunity 1: Engineering of Specialty Graphite Electrodes for Synthetic Graphite Production in Lithium-Ion Battery Manufacturing

The global shift toward electric mobility and gigafactory-scale battery production is generating a major opportunity for specialized graphite electrodes designed for synthetic graphite (SG) anode manufacturing. Graphitization furnaces used in lithium-ion battery (LIB) production routinely operate at 2,800–3,000°C, requiring ultra-high-power electrode performance and consistent electrical conductivity to achieve the crystal ordering required for high-capacity anode materials.

LIB anode graphite must reach >99.9% purity, as even trace contaminants can damage electrolyte stability, disrupt the Solid Electrolyte Interphase (SEI), and degrade cycle life. Electrodes used in SG production therefore must provide ultra-clean arc conditions and maintain low electrical resistivity to ensure uniform carbon transformation.

Particle size optimization is also essential: battery-grade producers demand graphite particles in the 10–25 μm range, with low surface area to minimize first-cycle irreversible capacity loss. These stringent requirements are spurring demand for high-performance, consistent, thermally stable electrodes, opening new revenue streams for electrode manufacturers aligned with the global LIB boom.

Market Opportunity 2: Establishment of Closed-Loop Recycling Platforms for High-Purity Electrode Butt Reclamation

The push toward circular production models in steelmaking is driving strong opportunities for closed-loop recycling of spent graphite electrode butts. Electrode consumption in EAFs typically ranges from 1.4–1.7 kg per tonne of steel, and butt ends can represent 10–20% or more of each electrode’s original mass. With global steel production expanding, the supply of recoverable high-purity graphite scrap is increasing rapidly.

Over 100,000 tonnes of used electrodes were recycled in 2023 for lower-grade applications such as carbon raisers—demonstrating a large, established reclamation flow. Moving toward high-grade recycling, however, presents a transformative opportunity: synthetic graphite recycling has already shown >30× reduction in Global Warming Potential (GWP) compared to producing virgin material. Applying similar principles to electrode butts could drastically reduce the carbon footprint of electrode manufacturing.

Electrode butt material retains the high-purity graphitized structure and low ash content of the original UHP electrode, making it superior to standard coke or low-grade carbon sources. With advancements in purification, milling, and graphitization reprocessing, reclaimed electrode materials can be upgraded for reuse in premium applications, enabling closed-loop, low-emission electrode manufacturing ecosystems.

Graphite Electrode Market Share Analysis

Market Share by Grade: Ultra-High Power (UHP) Electrodes Secure Dominance in Modern EAF Steelmaking

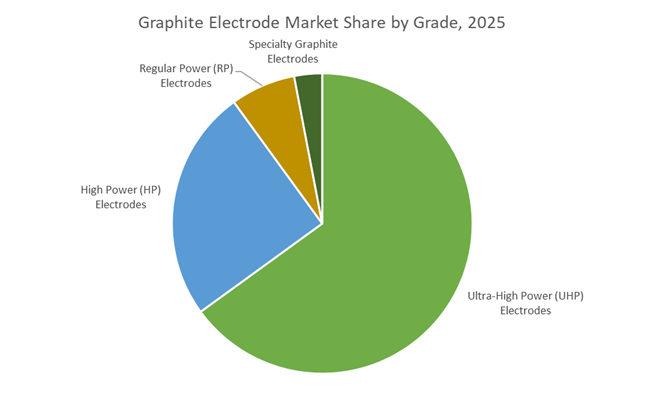

Ultra-High Power (UHP) graphite electrodes command the largest market share—approximately 65% in 2025—driven by their indispensable role in high-capacity Electric Arc Furnace (EAF) steel production, which is rapidly becoming the global standard for low-emission steelmaking. UHP electrodes are engineered to withstand extreme operating conditions, including current densities up to 25 A/in² and temperatures exceeding 3,000°C, making them the only commercially viable choice for maximizing furnace throughput and energy efficiency. Their superior electrical conductivity, thermal shock resistance, and structural integrity enable shorter tap-to-tap cycles and lower electricity consumption per ton of steel, offering steel manufacturers a significant operational cost advantage. Additionally, UHP electrodes exhibit the lowest consumption rate—typically 1.5–2.0 kg per ton of steel—owing to the use of premium needle coke and advanced graphitization processes. As global steelmakers invest heavily in expanding or transitioning to EAF-based production to decarbonize operations, the demand for UHP electrodes continues to surge, reinforcing their dominant share relative to High Power (HP), Regular Power (RP), and specialty electrode grades. Their combination of high performance, long service life, and compatibility with next-generation high-capacity furnaces solidifies UHP electrodes as the backbone of the graphite electrode market.

Market Share by End-User Industry: Steel Industry Drives Over Four-Fifths of Global Electrode Consumption

The steel industry accounts for roughly 82% of total graphite electrode demand, firmly establishing it as the dominant end-user due to the essential role electrodes play in both Electric Arc Furnace (EAF) and Ladle Furnace (LF) operations. As EAF steelmaking accelerates globally—fueled by rising scrap availability, lower carbon emissions compared to the Blast Furnace–Basic Oxygen Furnace (BF–BOF) route, and policy-driven decarbonization mandates—the consumption of electrodes continues to increase proportionately. Graphite electrodes are non-substitutable in EAFs, where they generate the high-intensity arc required to melt scrap steel, and in LFs, where they maintain temperature and facilitate alloying processes. With EAF’s share of global steel output projected to rise toward 35–40% by 2030, electrode demand is expanding in parallel, particularly in regions prioritizing low-carbon steel production. The steel industry’s large market share is also supported by continuous capacity additions in India, the Middle East, and Southeast Asia, along with modernization of scrap-based mini-mills in Europe and North America. As a result, steelmaking remains the central driver of graphite electrode consumption, consistently accounting for more than 80% of global volume and revenue, and ensuring its position as the largest and most influential application segment in the market.

Country Analysis: Global Drivers in the Graphite Electrode Ecosystem

China: Rapid EAF Transition, UHP Electrode Manufacturing Strength, and Expanding Carbon Materials Innovation

China represents the most influential global hub in the Graphite Electrode Market, driven by its aggressive transition from Blast Furnace (BF) to Electric Arc Furnace (EAF) steelmaking and its unmatched production capacity for Ultra-High Power (UHP) Graphite Electrodes. The country’s environmental regulations continue to tighten, accelerating the shift toward cleaner steelmaking technologies and generating sustained demand for UHP electrodes capable of supporting high-temperature EAF operations. Domestic manufacturers—including Fangda Carbon and Kaifeng Carbon Co., Ltd.—are expanding graphitization capacities and modernizing UHP production lines to meet both domestic and export demand. These investments position China as the world’s leading supplier of graphite electrodes, with significant export volumes recorded throughout October 2023–September 2024.

China is also advancing carbon material independence by developing domestic needle coke production technologies, reducing reliance on imported petroleum needle coke, which remains a strategic raw material for high-quality electrode manufacturing. Furthermore, China’s rapidly expanding electric vehicle (EV) sector adds synergy to the market: synthetic graphite for lithium-ion battery anodes is produced using similar raw material inputs and manufacturing expertise as graphite electrodes. This shared supply chain enhances economies of scale and strengthens China’s role as a vertically integrated powerhouse in the carbon materials ecosystem.

India: Steel Decarbonization Momentum, Major Electrode Capacity Expansions, and Strategic Global Investments

India is emerging as a high-growth market for Graphite Electrodes due to rising crude steel output, rapid industrialization, and government-backed infrastructure expansion. According to WSA data, India’s crude steel production grew 12.3% year-over-year in Q1 CY2024, reinforcing the increasing reliance on graphite electrodes for expanding EAF and Ladle Furnace (LF) operations. Domestic manufacturers are scaling aggressively: HEG Limited approved the demerger of its graphite business in May 2024 and committed INR 650 crore (USD 77 million) to expand graphite electrode capacity by 15,000 MT, aiming to reach 115,000 MT by FY28. Such investments reflect India’s long-term steel decarbonization roadmap and the rise of EAF steelmaking as a competitive, lower-emission alternative to traditional BF routes.

Strategic international investments further strengthen India’s market position. Graphite India Limited acquired a stake in U.S.-based GrafTech International in September 2025, expanding its global footprint and enhancing vertical integration capabilities. To reduce energy costs—one of the most critical variables in electrode manufacturing—Graphite India has also begun commissioning its first wind power captive plant, with full deployment targeted for Q1 FY25. This renewable energy integration not only reduces production costs but also contributes to a lower-carbon manufacturing footprint, aligning with global sustainability demands.

United States: EAF Steelmaking Dominance, Domestic Supply Reinforcement, and Needle Coke Processing Innovation

The United States remains one of the world’s most advanced EAF steelmaking regions, driving consistent demand for large-diameter, Ultra-High Power (UHP) Graphite Electrodes. The U.S. steel industry, supported by high recycling rates and strong demand for low-carbon steel, continues to expand its EAF footprint. This has resulted in long-term procurement agreements for electrodes, particularly as new EAF steel mills come online following significant investment announcements in 2025. GrafTech International—a major U.S. electrode supplier—allocated $40 million in CAPEX for FY2025 to enhance its UHP electrode production capacity, ensuring sufficient availability for new steelmaking expansions.

From a supply chain perspective, U.S. manufacturers are increasingly prioritizing security of raw materials and regional compliance advantages. GrafTech’s Monterrey, Mexico facility is fully USMCA compliant, enabling tariff-free exports to U.S. steelmakers, bolstering domestic sourcing resilience against global volatility. Additionally, U.S. firms continue to invest in advanced needle coke processing capabilities—critical for producing the premium-grade electrodes required for EAF operations. These technological improvements support greater independence from international raw material markets and improve the nation’s ability to maintain stable, high-strength electrode production.

Japan: High-Performance UHP R&D, AI-Optimized EAF Systems, and Strategic Production Rationalization

Japan’s Graphite Electrode Market is characterized by advanced materials research, highly automated steelmaking facilities, and a renewed focus on operational efficiency. Companies such as Tokai Carbon are intensifying R&D toward ultra-high-power (UHP) electrode formulations that provide superior oxidation resistance, conductivity, and mechanical integrity required by Japan’s technologically advanced EAF operations. As Japanese steelmakers increasingly deploy AI-driven EAF process automation—improving melt efficiency and reducing consumption variability—the performance requirements for graphite electrodes continue to rise, making high-end UHP electrodes essential to the modernization of Japan’s steel industry.

To maintain profitability amid rising energy and raw material costs, Japanese manufacturers are also consolidating global production footprints. Tokai Carbon announced a reduction in GE capacity from 56,000 tons to 32,000 tons by July 2025, affecting facilities in Japan and Europe. Additionally, the company divested Tokai Erftcarbon GmbH (TEG) in 2025 to streamline operations and reinforce its "Vision 2030" strategic plan. These moves reflect Japan’s strategy to prioritize high-value, high-performance electrodes while optimizing global supply chain efficiency.

South Korea: Specialty Steel Expansion, Battery Graphite Synergies, and High-Purity Electrode Demand

South Korea’s advanced industrial ecosystem—spanning specialty steel, semiconductors, and electric vehicle batteries—creates a dynamic and synergistic demand base for high-purity Graphite Electrodes. Steelmakers like POSCO are intensifying their focus on specialty and premium-grade steels, which require stable, large-diameter UHP electrodes to support high-performance EAF and Ladle Furnace operations. This shift toward specialized steelmaking elevates the need for electrodes with consistent consumption rates and high thermal shock resistance.

Korea’s booming EV battery industry adds another layer of opportunity. Both graphite anode materials and graphite electrodes rely heavily on high-quality needle coke and advanced graphitization technologies. Shared expertise across these industries enables Korean firms to leverage raw material synergies, cost efficiencies, and technological cross-over benefits. This convergence places South Korea in a strategically advantageous position, strengthening domestic demand for premium electrode materials and enabling greater integration between steelmaking and battery manufacturing supply chains.

GCC Region (Middle East): EAF Steel Capacity Boom, Long-Term Electrode Sourcing, and Infrastructure-Driven Steel Demand

The GCC region is experiencing one of the world’s fastest expansions in EAF-based steelmaking, driven by megaprojects, construction growth, and energy-efficient manufacturing advantages. Major economies—including Saudi Arabia and the UAE—are expanding their electric arc furnace capacities to support regional infrastructure initiatives such as NEOM and large-scale urban development plans. These expansions create sustained demand for graphite electrodes, particularly UHP variants used in high-temperature EAF operations.

To mitigate global supply volatility, GCC steel producers are increasingly entering long-term electrode procurement agreements with major manufacturers, securing stable cost structures and reliable inventory. Regional industrial strategies emphasizing energy efficiency and circular steel production further support the shift toward EAF-based steelmaking. As GCC nations continue diversifying their economies and ramping up infrastructure development, the region will remain a significant and rapidly growing consumer of graphite electrodes.

Competitive Landscape: Leading Graphite Electrode Producers Reshaping Global Supply

The competitive landscape of the global Graphite Electrode Market is dominated by a mix of Japanese, American, European, and Indian producers that collectively control the bulk of UHP and HP capacity serving EAF steelmakers worldwide. Companies such as Resonac Holdings, Tokai Carbon, GrafTech International, HEG Limited, and Graphite India Limited are pursuing differentiated strategies ranging from capacity optimization and portfolio rationalization to vertical integration into needle coke and diversification into battery-grade carbon. For industry professionals, understanding each player’s manufacturing footprint, technology positioning, and capital allocation priorities is critical to assessing supply security, pricing trends, and partnership opportunities across key steelmaking regions.

Resonac Holdings: UHP Graphite Electrode Leader Optimizing Global Capacity

Resonac Holdings, formerly Showa Denko K.K., remains one of the most influential suppliers in the UHP graphite electrode segment, supplying high-performance products to major EAF steelmakers worldwide. The company operates as a top-tier manufacturer of UHP electrodes used in high-intensity melting, supported by a global manufacturing footprint and technological expertise built over decades. In July 2025, Resonac announced the closure of specific graphite electrode units in China and Malaysia to optimize asset utilization and shift resources toward higher-value, technologically advanced products. Its competitive strength is reinforced by the earlier acquisition of SGL Carbon’s graphite electrode business, which expanded its reach across Asia, Europe, and the Americas. Under the Resonac brand, the company is aligning its carbon division with broader ambitions to become a global functional chemical leader, leveraging synergies with advanced materials used in semiconductors and electronics.

Tokai Carbon: Carbon Materials Specialist Streamlining Electrode Operations

Tokai Carbon Co., Ltd. is a long-established specialist in carbon materials, offering a full range of graphite electrodes—including RP, HP, and UHP grades—alongside fine carbon and carbon black products. The firm has embarked on a strategic optimization initiative, cutting graphite electrode production capacity in Japan and Europe from 56,000 tons to 32,000 tons by July 2025 and, in 2025, completing the divestiture of its subsidiary Tokai Erftcarbon GmbH (TEG) to streamline operations in line with its Vision 2030 and T-2024 plans. Tokai Carbon’s core strength lies in its strong R&D base, particularly at the Fuji Research Laboratory, where proprietary technologies are developed to enhance thermal shock resistance, mechanical strength, and electrical conductivity of UHP electrodes. With a manufacturing footprint spanning key regions, including North America via previous acquisitions, Tokai Carbon can deliver customized electrode solutions and responsive service to EAF operators across the globe.

GrafTech International: Vertically Integrated UHP Electrode Producer with Captive Needle Coke

GrafTech International Ltd. stands out in the global graphite electrode industry due to its vertically integrated model, including captive petroleum needle coke production, which historically provides a cost and supply security advantage in UHP electrode manufacturing. The company focuses exclusively on high-quality, large-diameter UHP electrodes that serve as critical consumables in modern EAF steelmaking. GrafTech has been expanding its commercial and technical presence, opening or enhancing operations in Dubai in April 2023 and extending its footprint in the United States in November 2025, aimed at supporting new EAF steel projects and strengthening customer proximity. A dedicated CapEx program of around USD 40 million in 2025 underscores its strategy to fine-tune electrode capacity in line with green steel investments and rising demand from mega-EAF installations. This integrated approach positions GrafTech as a strategic partner for steelmakers seeking long-term supply reliability and performance consistency.

HEG Limited: Indian UHP Graphite Electrode Exporter Scaling for Green Steel Demand

HEG Limited, based in India, is a major global producer and exporter of UHP graphite electrodes, serving leading steelmakers in more than 30 countries. The company manufactures large-diameter electrodes, including sizes up to 800 mm, tailored to high-power EAF operations that underpin green steel initiatives. In August 2025, HEG announced a significant 15,000 TPA capacity expansion, reflecting strong confidence in rising global UHP electrode demand. Earlier, in May 2024, it secured initial approval for the demerger of its graphite business into a separate entity, expected to be completed by end-2025, with the intent to unlock shareholder value and give sharper strategic focus to its core carbon operations. HEG’s portfolio is heavily geared to high-efficiency EAF steelmaking, positioning it as a key beneficiary of the shift from BOF to EAF-based production and the broader decarbonization of the steel industry.

Graphite India Limited: Capacity Expansion and Battery-Materials Diversification

Graphite India Limited is another leading Indian player with a strong footprint in the global graphite electrode export market, manufacturing RP, HP, and UHP electrodes for steel and non-ferrous metallurgy customers. In August 2025, the company announced an ambitious capacity increase of 25,000 TPA, taking total electrode capacity to 105,000 TPA, backed by an investment of about INR 600 crore to improve its competitive scale and global reach. Strategically, Graphite India is diversifying beyond traditional steel inputs, acquiring a 31% stake in GODI India in 2025 for INR 50 crore to access R&D capabilities in lithium-ion and sodium-ion battery and supercapacitor materials, thereby aligning with the broader energy storage transition. Its operational strengths include robust process optimization and raw material management practices, which help maintain high yields and competitive production costs while supporting a broad customer base across international EAF markets.

Graphite Electrode Market Report Scope

Graphite Electrode Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.9 Billion

|

|

Market Size (2035)

|

$28.2 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Grade (Ultra-High Power Electrodes, High Power Electrodes, Regular Power Electrodes, Specialty Graphite Electrodes), By Electrode Diameter (Small, Medium, Large), By End-User Industry (Steel Industry, Automotive, Foundries, Chemical Processing, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

GrafTech International, Showa Denko/Resonac, Tokai Carbon, Graphite India, HEG Limited, SGL Carbon, Nippon Carbon, Fangda Carbon, Kaifeng Carbon, SEC Carbon, Sinosteel Jilin Carbon, Gansu Himo Carbon, SANGRAF International, Misano Group, Oriental Carbon & Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Graphite Electrode Market Segmentation

By Grade

- Ultra-High Power (UHP) Electrodes

- High Power (HP) Electrodes

- Regular Power (RP) Electrodes

- Specialty Graphite Electrodes

By Electrode Diameter

- Small (Up to 400 mm)

- Medium (400–600 mm)

- Large (Above 600 mm)

By End-User Industry

- Steel Industry

- Automotive (Specialty Steel for EVs)

- Foundries

- Chemical Processing

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Graphite Electrode Market

- GrafTech International

- Showa Denko / Resonac

- Tokai Carbon

- Graphite India

- HEG Limited

- SGL Carbon

- Nippon Carbon

- Fangda Carbon

- Kaifeng Carbon

- SEC Carbon

- Sinosteel Jilin Carbon

- Gansu Himo Carbon

- SANGRAF International

- Misano Group

- Oriental Carbon & Chemicals

*- List not Exhaustive

Research Coverage: Graphite Electrode Market

The latest Graphite Electrode Market study from USDAnalytics delivers a detailed industry blueprint that spans technology, capacity, and regional competitiveness, as this report investigates how rising EAF steelmaking penetration, UHP performance benchmarks, and raw material constraints are reshaping value pools across the carbon ecosystem. It tracks major breakthroughs in large-diameter ultra-high-power electrodes, anti-oxidation coatings, and needle coke optimization while providing structured analysis reviews of capacity rationalization in Japan and Europe, aggressive expansions in India, and strategic diversification into battery-grade carbon. The study highlights how shifting steel decarbonization policies, circular recycling models for electrode butts, and the convergence with lithium-ion anode manufacturing are influencing pricing power, contract structures, and long-term supply security. With rigorous coverage of grades, diameters, end-use sectors, and leading producers, this report is an essential resource for steelmakers, electrode manufacturers, trading houses, financial investors, and technology partners seeking to benchmark performance, de-risk procurement, and capture upside from the next decade of green steel and advanced carbon materials growth, all underpinned by USDAnalytics’ data-driven market intelligence and scenario modelling.

Scope Highlights

- Segmentation:

- By Grade: Ultra-High Power (UHP) Electrodes, High Power (HP) Electrodes, Regular Power (RP) Electrodes, Specialty Graphite Electrodes

- By Electrode Diameter: Small (Up to 400 mm), Medium (400–600 mm), Large (Above 600 mm)

- By End-User Industry: Steel Industry, Automotive (Specialty Steel for EVs), Foundries, Chemical Processing, Aerospace & Defense

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, capturing both mature mini-mill hubs and fast-growing EAF build-out regions.

- Time Horizon: Includes historical datasets from 2021–2025 and forward-looking forecasts from 2026–2034, enabling long-range planning, capex assessment, and contract strategy calibration.

- Companies Covered: In-depth analysis and profiles of 15+ key graphite electrode manufacturers and carbon players, mapped by capacity, product mix, integration in needle coke, regional exposure, and green-steel alignment.