Market Overview: Strategic Outlook of the Advanced Carbon Materials Industry to 2035

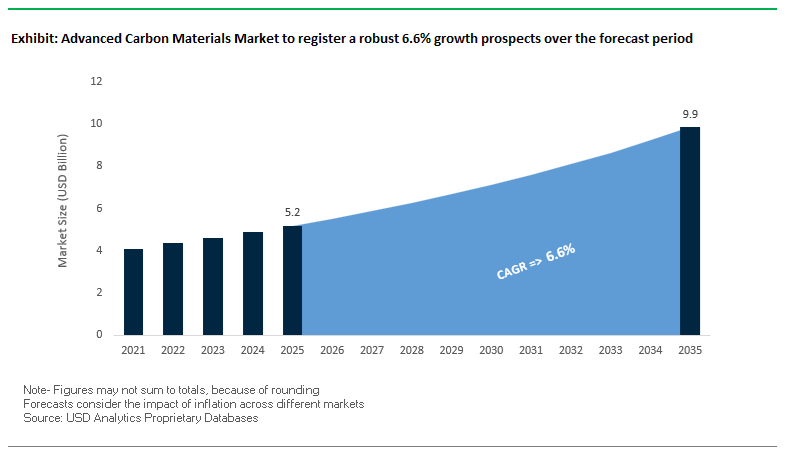

The Global Advanced Carbon Materials Industry, valued at USD 5.2 Billion in 2025, is projected to reach USD 9.9 Billion by 2035, expanding at a steady CAGR of 6.6% (2025–2035). As the market evolves beyond conventional carbon applications, industry buyers are increasingly prioritizing performance, purity, energy efficiency, and supply reliability across Carbon Fiber, Graphene, and Carbon Nanotubes (CNTs). This shift is driven by the growing technological requirements of aerospace, EVs, semiconductors, renewable energy, filtration systems, and quantum research-each demanding materials with superior strength-to-weight ratios, controlled defect levels, thermal conductivity, and long-term durability.

Industry professionals are asking critical questions: How fast is production efficiency advancing? What technological barriers constrain mass adoption? Which materials will dominate high-value applications, and how will national strategies reshape graphite supply chains? The answers point toward rising R&D intensity, expansion of AI-enabled production systems, and major geopolitical initiatives aimed at securing anode-grade graphite for lithium-ion batteries. The significant energy input required to produce Carbon Fiber, the extremely low defect tolerance needed for Graphene electronics, and the accelerating integration of CNT additives into EV batteries all underscore the sector’s increasing technical complexity.

Key Consumer Insights for Advanced Carbon Materials Vendors

- High Energy Barrier for CFRP: Producing 1 kg of Carbon Fiber Reinforced Polymer consumes >$12 in thermal and electrical energy, encouraging research into microwave-assisted and plasma carbonization to reduce cost per kilogram.

- AI in Nanomaterial Quality: Graphene defect levels are being reduced to below 0.1% through AI-driven inspection systems, unlocking next-gen flexible electronics and carbon-based sensors.

- Aerospace Durability Standards: Carbon Fiber composite components now carry >30-year operational lifespan expectations, intensifying R&D in nanotube-enhanced resins.

- Activated Carbon Demand Surge: Global water treatment projects require specialty activated carbon with engineered pore structures to remove micro-contaminants.

- Strategic Graphite Security: Major economies aim to localize ≥50% of anode-grade graphite supply by 2030 to secure EV battery manufacturing.

Market Analysis: Key Developments Reshaping Advanced Carbon Materials Production, Regulation & Innovation

The Advanced Carbon Materials Industry witnessed transformative developments across circular manufacturing, nanomaterial production, quantum research, sustainability regulation, renewable energy infrastructure, and battery innovation. In December 2025, Holcim acquired three recycling operations in the UK, Germany, and France, signaling the growing incorporation of Recovered Carbon Black (rCB) and circular carbon additives in the building materials sector. This move highlights how ECOCycle® technology and construction-sector sustainability mandates are expanding industrial demand for carbon-based materials derived from recycled streams-an important trend for carbon material producers seeking new downstream applications.

In November 2025, a leading Asian manufacturer secured $150 million to double production capacity for Single-Walled Carbon Nanotubes (SWCNTs), reflecting explosive demand from the EV battery industry, where CNTs enhance anode conductivity and cycling stability. Earlier, in September 2025, researchers in Europe announced a breakthrough method for observing Floquet states in Graphene, accelerating the development of programmable electronic behavior for quantum computing, optoelectronics, and ultra-responsive circuit architectures. The finding underscores how Graphene continues to move beyond lab-scale science toward a programmable, application-ready material platform.

In July 2025, Toray Industries expanded its U.S. facility to scale large-tow Carbon Fiber optimized for wind turbine blades, a critical driver in renewable energy. This investment supports utility-scale wind installations that require longer, lighter blades engineered from advanced composites. Regulatory forces also influenced the industry when, in May 2025, the EU introduced its draft Strategy for Sustainable and Circular Textiles, mandating sustainable inputs and recycling adaptability-thereby increasing demand for functionalized carbon materials used in dyes, coatings, and high-durability textile fibers.

Technological commercialization accelerated further in February 2025, when Innovate UK awarded over US$1.1 million to the Graphene Electrode Technology for Perovskite Solar Cells (GETPSC) project involving Taiwan Perovskite Solar Corporation. This supports the development of graphene-based transparent electrodes targeted at high-efficiency solar modules. Additionally, in January 2025, Tiannai Technology confirmed supplying SWCNTs to solid-state battery manufacturers, solidifying CNTs as a pillar for next-generation battery safety and conductivity. Meanwhile, U.S. federal initiatives in Q4 2025, allocating $3.5+ billion toward Direct Air Capture (DAC) hubs, are accelerating the development of specialized porous carbons and adsorbents-materials poised to become high-volume industrial commodities in carbon capture markets.

Major Trends Reshaping the Advanced Carbon Materials Market

Trend 1: Onshoring of Battery-Grade Graphite and Rise of Giga-Scale Anode Production Outside China

The most consequential trend currently shaping the Advanced Carbon Materials Market is the surge in onshoring efforts for synthetic and natural graphite refining, driven by EV battery sourcing rules and escalating geopolitical constraints. The U.S. tariff increase—from 0% to 160% on Chinese synthetic graphite anodes as of June 2024—has fundamentally shifted the cost structure of anode procurement. This abrupt price shock has granted North American and European graphite producers an immediate competitive advantage, dramatically accelerating localization plans for spherical graphite, synthetic graphite, and purification facilities.

The International Energy Agency’s latest analysis reinforces the urgency: by 2024, the top three refining nations controlled 86% of global output for critical energy minerals. Graphite remains among the most concentrated, with China responsible for over 95% of global anode production. While diversification is underway at the mining stage, the refining and processing bottleneck remains severe. This concentrated supply dynamic explains why OEMs are investing billions to develop vertically integrated, non-China graphite supply chains capable of supporting EV gigafactories. In parallel, the Synthetic Graphite Market is set to expand by $3.4 billion from 2025 to 2030, powered by the explosive demand for lithium-ion battery anodes.

Trend 2: High-Performance Carbon Materials Integrated into Traditional Infrastructure for Strength and Decarbonization

A second defining trend is the rapid integration of advanced carbons—particularly carbon nanotubes (CNTs), graphene, and high-strength carbon fibers—into established industrial materials to unlock performance gains without requiring new manufacturing infrastructure. In the construction sector, CNT-enhanced concrete formulations are gaining meaningful traction. Studies confirm that embedding just 0.1%–0.5% MWCNTs into cement mortar can increase flexural strength by 30%–40%, a substantial improvement for structural applications. CNTs act as nanoscale reinforcement bridges that control micro-cracking and improve fracture toughness; optimal CNT loading has been shown to increase mortar fracture energy by over 47%.

This approach allows the construction industry to achieve durability improvements and lower life-cycle emissions without changing production processes—an advantage critical for ESG-aligned infrastructure investment. In parallel, automotive lightweighting efforts are accelerating the use of advanced carbon reinforcements. Companies such as SGL Carbon are focusing R&D on next-generation composite solutions incorporating graphitic materials to meet automakers’ weight reduction, performance, and uncertainty-buffering requirements for new EV models.

High-Value Opportunities Emerging in the Advanced Carbon Materials Market

Opportunity 1: Advanced Carbon Additives Enabling Beyond-Graphite Lithium Battery Chemistries

As the battery industry pushes beyond conventional graphite to higher-energy-density systems, advanced carbon additives are emerging as critical enablers. Carbon Nanotubes (CNTs) are rapidly becoming the preferred conductive additive because they deliver exceptional electron mobility at ultra-low loading—far outperforming traditional carbon black. Their ability to maximize conductivity while allowing greater fractions of active material (such as silicon) is essential for next-generation anode performance.

The role of conductive carbon additives is expanding beyond electron transport. Engineered carbons are now designed to provide mechanical reinforcement, enhance thermal stability, and support safer solid-electrolyte interphase (SEI) formation—all crucial for fast-charging and high-power applications. Electrolyte innovation also plays a key role, with Fluoroethylene Carbonate (FEC) emerging as the fastest-growing carbon-based electrolyte additive due to its ability to stabilize silicon-rich anodes and perform well in high-voltage cell environments. These additive-driven improvements are making advanced carbons indispensable across new lithium battery formats, including silicon-dominant, lithium-sulfur, and semi-solid-state chemistries.

Opportunity 2: Scaling Carbon Fiber Recycling and Reclamation for Circular Composite Markets

A second major opportunity is unfolding around carbon fiber recycling as first-generation composite products from aviation, wind energy, and high-performance industries reach end-of-life. Regulatory pressure, circular economy commitments, and the persistently high cost of virgin carbon fiber are converging to create strong incentives for commercially viable reclamation. Companies like SGL Carbon have already begun restructuring their businesses, discontinuing unprofitable segments (as of Feb 2025) and signaling an industry-wide pivot toward profitable recycling ecosystems that support both sustainability and cost competitiveness.

Recycled carbon fiber that retains 80–90% of the mechanical properties of virgin fiber at a lower price point could unlock vast secondary markets—ranging from automotive structural components and mobility applications to consumer electronics and sports goods. Achieving cost-effective, high-quality thermal or chemical reclamation at scale would fundamentally reshape material economics, reduce supply reliance on early-stage production assets, and position recycling as a strategic pillar of the advanced carbon materials industry.

Advanced Carbon Materials Market Share Analysis

Market Share by Product Type: Carbon Fibers Lead with 54.2% Share

Carbon Fibers hold a commanding 54.2% share of the Advanced Carbon Materials Market in 2025, reflecting their entrenched position as the high-performance material backbone for aerospace, automotive, industrial, and wind energy applications. Their dominance is driven by an unmatched combination of exceptional strength-to-weight ratio, fatigue resistance, and thermal stability, which makes carbon fiber composites indispensable for lightweighting strategies across mobility and renewable energy sectors. The segment is uniquely bifurcated: high-volume industrial grades fuel adoption in automotive platforms, pressure vessels, and large-scale wind blades, while premium aerospace and defense grades deliver high-value growth through stringent performance and safety requirements. Supporting product categories continue to influence market dynamics—carbon nanotubes (CNTs) scale rapidly as EV battery cathode additives, graphene gains traction through graphene oxide and nanoplatelets used as performance enhancers, specialty graphite remains integral for steelmaking, silicon processing, and semiconductor equipment, and carbon foams and other engineered carbons serve thermal management and lightweight structural applications.

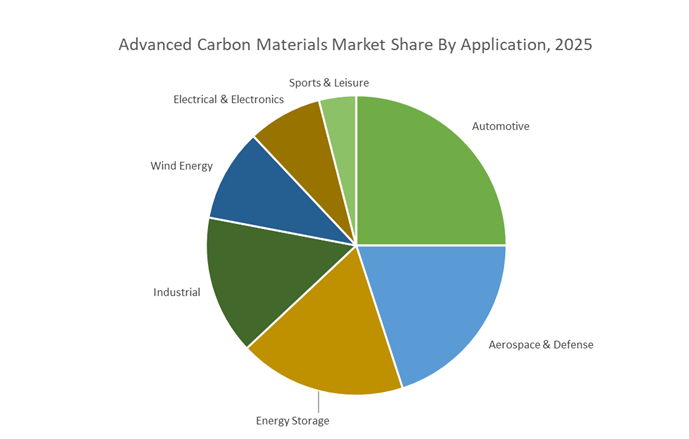

Market Share by Application: Automotive Leads with 25.7% Share

Automotive dominates the market with a 25.7% share in 2025, underpinned by accelerating global trends in electric vehicle (EV) adoption, platform lightweighting, and advanced battery material integration. Carbon fibers enable major reductions in structural mass, extending EV driving range and improving fuel efficiency in hybrid and ICE platforms, while CNTs emerge as critical conductive additives in lithium-ion battery cathodes, dramatically improving energy density and charge rates. Specialty graphite also plays a pivotal role in fuel-cell bipolar plates and battery anodes, tying the automotive sector directly to the evolution of clean mobility technologies. Other key applications reinforce the market’s expansion trajectory: Aerospace & Defense continues to command the highest value per kilogram with ultra-high-modulus fibers and specialty graphite components; Energy Storage represents the fastest-growing segment as Li-ion batteries, supercapacitors, and hydrogen fuel cells drive exponential material demand; Wind Energy scales consumption of standard-modulus carbon fibers as turbine blades exceed 100 meters; Industrial applications rely on graphite and engineered carbons for thermal management, durability, and high-temperature processes; and Sports & Leisure remains a premium, innovation-driven niche where advanced carbon fiber weaves often debut before transitioning into mainstream industrial use.

Country Analysis: Global Advanced Carbon Materials Market Innovation Hubs

United States: Dominance in Aerospace-Grade Carbon Materials and Carbon Utilization Technologies

The United States continues to lead the global advanced carbon materials market through extensive federal research programs, accelerated commercialization of carbon utilization technologies, and sustained demand from aerospace and defense manufacturing. A core catalyst in 2024 is the Department of Energy’s ARPA-E Vision OPEN program, which allocated $147 million across 49 projects aimed at breakthrough pathways for carbon utilization in chemicals and materials—establishing the US as a pioneer in carbon-to-material innovation. Complementing this, the NSF’s multi-year $104 million Engineering Research Center initiative targets next-generation carbon materials as part of the national strategy to address the “carbon challenge,” enabling novel synthesis routes, performance-optimized nanocarbon structures, and carbon-negative manufacturing.

In addition to federal R&D programs, the US continues to advance infrastructure-centric carbon materials innovation. Ohio University’s development of an ultra-conductive carbon aluminum composite (UCAC) cable, supported by nearly $3 million from ARPA-E, represents a major leap in power transmission technologies utilizing high-performance carbon materials. The aerospace sector remains a major driver of carbon composites demand, with Hexcel Corporation maintaining long-term supply agreements for carbon fiber prepreg and honeycomb structures for critical defense platforms including the F-35. Moreover, NSF-backed semiconductor research involving novel carbon nanostructures underscores the US ambition to integrate carbon materials into next-gen microelectronics for improved chip efficiency. Together, these strategic investments significantly reinforce America’s leadership in advanced carbon materials manufacturing, defense-grade composites, and carbon utilization technologies.

China: Accelerating Self-Sufficiency in New-Generation Carbon Materials Through Standardization and Green Manufacturing

China is rapidly strengthening its position in the global advanced carbon materials market by aligning national strategy with its dual carbon goals—achieving peak emissions by 2030 and carbon neutrality by 2060. A major regulatory shift is the government’s plan to issue 70 national standards by end-2024, covering carbon accounting, carbon footprint measurement, and CCUS technologies. These standards aim to unify and scale the use of advanced carbon materials across energy, industrial, and mobility sectors, while supporting domestic self-sufficiency targets. China is also accelerating the issuance of national carbon footprint standards for NEVs and lithium batteries, enforcing quality benchmarks for anode materials, conductive carbon additives, and energy storage components to bolster global export competitiveness.

Green manufacturing is becoming a central economic driver, supported by a March 2024 policy directive targeting over 40% of total manufacturing output from green factories by 2030. This transition is increasing demand for recycled, low-carbon, and specialty carbon materials across sectors like petrochemicals, iron and steel, and power generation. China is also deploying new carbon-based catalysts and specialty graphite materials to decarbonize heavy industries. Together, these initiatives position China as one of the fastest-growing markets for standardized, scalable, and sustainability-aligned carbon material production.

Japan: Innovating Carbon Nanomaterials for High-Performance Batteries and Next-Gen Electronics

Japan continues to dominate high-precision carbon materials, particularly carbon fiber, carbon nanotubes (CNTs), and graphene-based nanomaterials, driven by its leadership in electronics, electric mobility, and energy storage technologies. In late 2024, 3DC announced a major joint research agreement to commercialize silicon-based anode materials enhanced by its proprietary Graphene MesoSponge® (GMS)—a breakthrough carbon material enabling higher-capacity, longer-cycle lithium-ion batteries. The company’s launch of mass production for GMS conductive additives in February 2024 marks a pivotal moment for Japan’s battery materials supply chain, enabling high-rate charging and improved energy density for electric vehicles and stationary storage systems.

Japan is also pushing advancements in high-purity CNT synthesis, focusing on controlled chirality and defect reduction to integrate CNTs into flexible electronics, high-performance semiconductors, and structural composites. Leading manufacturers such as Toray Industries are investing in cost-effective, high-strength PAN precursor technology, which remains the backbone of the global carbon fiber supply chain. These innovations reinforce Japan’s role as a hub for next-generation carbon materials tailored for aerospace, energy storage, and advanced electronic applications.

Germany (Europe): Pioneering CFRP Manufacturing and Carbon Fiber Recycling Technologies

Germany serves as Europe’s powerhouse for advanced carbon materials, backed by its industry leadership in automotive engineering, wind energy, and precision manufacturing. The country’s strong push toward renewable energy is driving robust demand for heavy-tow carbon fiber used in large wind turbine blades, a crucial requirement in scaling offshore and onshore wind deployment across the European Union. Automotive lightweighting—accelerated by electric vehicle adoption—is propelling collaborations between SGL Carbon and German OEMs to produce cost-efficient, high-volume CFRP components that offset battery weight while improving energy efficiency.

Germany is also emerging as a global center for carbon fiber recycling technologies, with European companies and research institutes pioneering pyrolysis and solvolysis processes that recover high-quality recycled carbon fiber (rCF). This recycled material is increasingly used in non-aerospace applications such as automotive parts, industrial components, and consumer goods, supporting the EU’s broader circular economy targets. Together, these developments position Germany as a critical innovation hub for industrial composites and sustainable carbon material ecosystems.

South Korea: Advancing Graphene-CNT Hybrid Technologies for Displays and high-performance Energy Storage

South Korea’s advanced carbon materials strategy centers on graphene and CNT hybridization, reflecting its dominance in displays, semiconductors, and high-performance batteries. Academic and corporate R&D efforts are making rapid progress in soft electronics and flexible electrode technology, demonstrating the potential of CNT-graphene hybrid materials to enable next-generation pressure sensors, strain sensors, and wearable devices. Korean display manufacturers are integrating these carbon nanomaterials into transparent conductive films, aiming to surpass indium tin oxide (ITO) with more flexible, durable, and conductive alternatives suited for foldable and rollable screens.

Carbon materials are also unlocking significant improvements in South Korea’s battery industry, particularly for high-nickel NMC/NCA lithium-ion cathodes, where CNT conductive additives enhance cycle life, structural stability, and rapid charging capability. This integrated approach to nanomaterial innovation ensures South Korea remains a key leader in carbon nanostructure commercialization for advanced electronics and energy storage.

United Kingdom: Advancements in Aerospace Carbon Composites and AI-Enabled Digital Manufacturing

The United Kingdom is emerging as a high-value innovation hub for aerospace-grade carbon composites and digital manufacturing, driven by strong demand from defense and commercial aviation. UK aerospace manufacturers continue to invest in premium carbon fiber prepregs and automated production methods such as automated tape laying (ATL) and automated fiber placement (AFP), accelerating the manufacturing of large, lightweight, high-specification CFRP components.

A defining trend in the UK is the commercialization of advanced 2D carbon materials. Companies like Haydale Graphene Industries are progressing the functionalization of graphene and CNTs for integration into polymers, coatings, and conductive inks, expanding their industrial and electronics applications. Additionally, UK advanced manufacturing centers are implementing AI and machine learning platforms to optimize carbon composite lay-up, curing cycles, and defect detection, reducing waste and production costs. This convergence of carbon materials science and digital manufacturing positions the UK as a rising innovation center in the global advanced carbon materials market.

Competitive Landscape - Strategic Positioning of Leading Companies in the Advanced Carbon Materials Market

The competitive environment for Advanced Carbon Materials is defined by rapid specialization across Carbon Fiber, CNTs, Graphene, Activated Carbon, and CCU-derived carbon products. Companies are intensifying investments in scalable manufacturing, carbon-neutral processes, EV-centric innovations, and high-purity materials for semiconductors, aerospace, and renewable energy. This landscape is shaped by a blend of material science innovation, circular economy adoption, and industrial automation, where leadership hinges on the ability to supply consistent, application-ready carbon materials at scale.

Toray Industries, Inc. - Global Leader in Aerospace-Grade Carbon Fiber

Toray Industries maintains industry leadership through its Torayca® Carbon Fiber portfolio, supported by extensive expertise in PAN precursor chemistry and aerospace-certified composite systems. The company is expanding aggressively into EV lightweighting, hydrogen storage applications, and renewable infrastructure-key areas poised for long-term demand. Toray’s materials form the structural backbone of major aircraft such as the Boeing 787, and its corporate roadmap includes a net-zero target by 2050, pushing the company to innovate lower-emission carbonization technologies.

Cabot Corporation - High-Purity Carbon Black & Activated Carbon for Energy and Filtration

Cabot Corporation is a global producer of Specialty Carbon Black, conductive carbons, and high-performance activated carbons used in filtration, polymers, and battery electrodes. Its current strategy centers on electrification, with R&D focused on carbon additives that enhance lithium-ion battery cathode and anode performance. Operating across 45 manufacturing sites, Cabot’s carbon blacks are essential in tire reinforcement, high-precision printing inks, and conductive polymers, giving it a strong position across industrial and mobility-related demand segments.

SGL Carbon SE - Integrated Supplier of Carbon Fiber, Graphite & Industrial Composites

SGL Carbon differentiates itself with a highly integrated portfolio covering Carbon Fiber, Technical Textiles, and Graphite Specialties. The company is channeling capital toward automating composite manufacturing for high-volume EV applications, enabling structural carbon components to enter mass automotive production. Its dominance in Isostatic and Extruded Graphite supports semiconductor fabrication, high-temperature furnaces, and precision tooling-markets where purity, thermal stability, and dimensional control are critical.

OCSiAl S.A. - Global Pioneer in Industrial-Scale SWCNT Production

OCSiAl leads the market for Single-Walled Carbon Nanotubes (TUBALL™), offering scalable CNT synthesis capabilities unmatched in industrial deployment. Its strategic collaborations with automotive and battery manufacturers aim to integrate CNT masterbatches into EV anodes, boosting conductivity, mechanical strength, and fast-charging performance. With high-volume SWCNT production capacity, OCSiAl delivers lightweight, conductive additives for polymers, metals, and energy storage materials across multiple industrial sectors.

Lanzatech Inc. - Transformational Carbon Utilization for Sustainable Carbon Material Production

Lanzatech leverages proprietary Carbon Capture and Utilization (CCU) biotechnology to convert industrial emissions into valuable chemical precursors. Recent strategic agreements focus on scaling biological conversion of steel mill emissions into sustainable ethylene alternatives, creating a disruptive pathway for producing bio-derived carbon material inputs. The company’s platform has potential to repurpose millions of tons of captured carbon annually, supporting the industry’s shift toward low-carbon, circular carbon materials.

Teijin Limited - High-Strength Carbon Fiber & Nanomaterial-Integrated Composites

Teijin is a key supplier of Tenax™ Carbon Fiber and advanced aramid fibers for aerospace, automotive, and industrial sectors. The company's R&D focus includes faster-curing prepregs designed for high-speed automotive manufacturing cycles, enabling broader CFRP adoption in mass-market vehicles. Teijin is also advancing CNT-dispersed carbon composites, improving electrical conductivity, mechanical strength, and durability, signaling a clear strategic commitment to next-generation nanomaterial integration.

Advanced Carbon Materials Market Report Scope

Advanced Carbon Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.2 Billion

|

|

Market Size (2035)

|

$9.9 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Product Type (Carbon Fibers, Carbon Nanotubes, Graphene, Carbon Foams, Others), By Application (Aerospace & Defense, Automotive, Energy Storage, Electrical & Electronics, Industrial, Wind Energy, Sports & Leisure), By Precursor Type (Polyacrylonitrile, Pitch-based, Rayon-based, Lignin-based), By Grade (Commercial Grade, Aerospace Grade)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries Inc., SGL Carbon, Teijin Limited, Mitsubishi Chemical Group Corporation, Showa Denko K.K., Tokai Carbon Co. Ltd., Hexcel Corporation, Cabot Corporation, GrafTech International Ltd., Toyo Tanso Co. Ltd., Nippon Graphite Fiber Corporation, Nanocyl SA, Global Graphene Group, Birla Carbon, Haydale Graphene Industries plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Carbon Materials Market Segmentation

By Product Type

- Carbon Fibers

- Carbon Nanotubes

- Graphene

- Carbon Foams

- Others

By Application

- Aerospace & Defense

- Automotive

- Energy Storage

- Electrical & Electronics

- Industrial

- Wind Energy

- Sports & Leisure

By Precursor Type

- Polyacrylonitrile (PAN)

- Pitch-based

- Rayon-based

- Lignin-based (Sustainable)

By Grade

- Commercial Grade

- Aerospace Grade

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Advanced Carbon Materials Market

- Toray Industries, Inc.

- SGL Carbon

- Teijin Limited

- Mitsubishi Chemical Group Corporation

- SHOWA DENKO K.K.

- Tokai Carbon Co., Ltd.

- Hexcel Corporation

- Cabot Corporation

- GrafTech International Ltd

- Toyo Tanso Co., Ltd.

- Nippon Graphite Fiber Corporation

- Nanocyl SA

- Global Graphene Group

- Birla Carbon

- Haydale Graphene Industries plc

*- List not Exhaustive

Research Coverage – Advanced Carbon Materials Market

This report by USDAnalytics investigates the Global Advanced Carbon Materials Market through a performance-centric and supply-chain–aware framework, focusing on how carbon fibers, graphene, carbon nanotubes, and specialty carbons are transitioning from niche materials into industrial enablers across aerospace, electric vehicles, energy storage, electronics, and infrastructure. The analysis reviews production breakthroughs, defect-control advancements, energy-intensive manufacturing economics, and circular carbon pathways that are redefining cost structures and scalability. This report highlights how geopolitical strategies around graphite security, battery localization mandates, and carbon-neutral manufacturing are reshaping global sourcing decisions. It also examines the integration of AI-enabled quality control, nanomaterial dispersion technologies, and recycling-driven feedstock innovation that are accelerating commercialization. Designed for OEMs, material suppliers, investors, and policy-linked industrial planners, this report is an essential resource for understanding where demand visibility is strongest, which carbon materials command pricing power, and how advanced carbon ecosystems are evolving through 2035.

Scope Includes

- By Product Type: Carbon Fibers, Carbon Nanotubes, Graphene, Carbon Foams, Others

- By Application: Aerospace & Defense, Automotive, Energy Storage, Electrical & Electronics, Industrial, Wind Energy, Sports & Leisure

- By Precursor Type: Polyacrylonitrile (PAN), Pitch-based, Rayon-based, Lignin-based (Sustainable)

- By Grade: Commercial Grade, Aerospace Grade

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data from 2021–2024 with forecasts from 2025–2035.

- Company Coverage: Competitive analysis and profiles of 15+ leading advanced carbon material producers and technology developers.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.