Market Overview: Hydrogen Leak Detection, AI-Driven Industrial Sensing, and Digital Twin Integration Accelerate Chemical Sensors Market

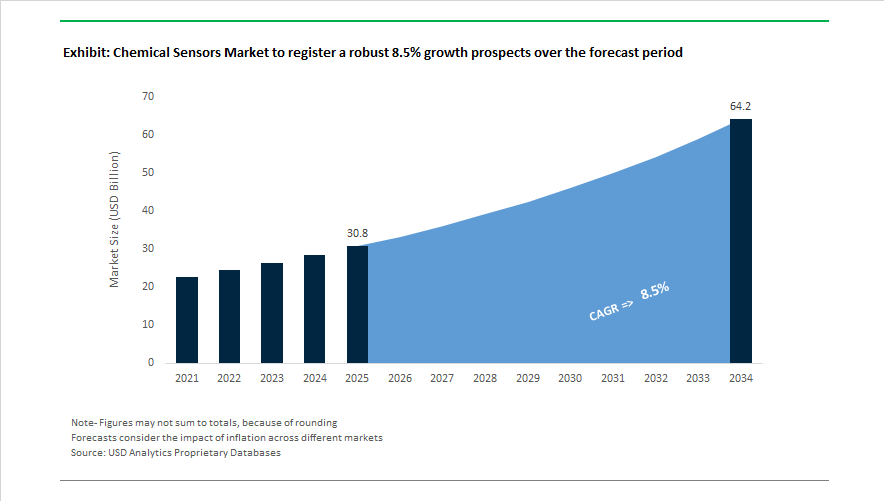

The Chemical Sensors Market is projected to expand from USD 30.8 billion in 2025 to USD 64.2 billion by 2034, registering a CAGR of 8.5% , driven by rapid adoption of industrial gas sensors, electrochemical sensors, optical sensing platforms, and AI-enabled environmental monitoring systems. Structural transformation began in January 2024 when ABB acquired an innovative optical sensor specialist to strengthen smart water quality monitoring solutions. Momentum continued in March 2024 as Clariant launched CLARITY Prime, an AI platform using real-time chemical sensor data for catalyst optimization and predictive maintenance in process industries. Hydrogen economy requirements shaped product innovation during 2024 when Baker Hughes introduced Druck hydrogen-rated pressure sensors, engineered with advanced barrier coatings for durability in hydrogen storage and fuel infrastructure. In October 2024, ABB reinforced emission monitoring capabilities by acquiring the Födisch Group, expanding continuous emission monitoring systems for industrial exhaust compliance.

Market direction shifted further in February 2025 when Honeywell announced a three-way corporate split, positioning its Automation business as a focused leader in industrial sensing, process automation, and AI-driven control. Product leadership was demonstrated in May 2025 with Honeywell’s industry-first 10-year hydrogen leak detector using thermal conductivity detection technology, capable of identifying leaks as small as 50 ppm without manual recalibration, a major advancement for fuel cell vehicles and hydrogen refueling stations. In parallel, NS2 advanced its NoxAqua biosensing technology during 2024–2025, enabling biological detection of nitrogen pollutants in water systems. Wearable sensing innovation gained traction in 2025 as EOXsense commercialized biochemical sensors that monitor lactate and glucose via sweat, bridging industrial biosensing and medical diagnostics.

Digitalization and AI integration define the current phase of market expansion. In January 2026, Emerson was named Industrial IoT Company of the Year for integrating intelligent field sensors with cloud analytics to enable AI-driven asset performance management. The same month, Siemens introduced Digital Twin Composer, linking live chemical sensor data with virtual plant models for physics-based simulation in industrial metaverse environments. Meanwhile, ABB’s previously announced robotics division spin-off, targeted for Q2 2026, enables sharper capital focus on sensing and automation.

Trends and Opportunities in the Chemical Sensors Market

Multi-Analyte Sensor Miniaturization Driven by Smart Environmental Monitoring

The market is advancing from single-gas detectors to chip-based multi-analyte chemical sensors capable of decoding complex VOC signatures. Q3 2025 benchmarking studies in nanotechnology confirm:

- 10–30 second response times for semiconductor–nanomaterial sensor arrays

- 90% reproducibility across hundreds of sensing cycles

- Single-chip detection of CO, NO₂, PM2.5, and explosive gases

This shift enables integrated “electronic nose” systems for Industrial IoT, smart mining ventilation, and connected public-safety infrastructure. Mining companies are deploying MOS- and PID-based sensor grids that automatically adjust ventilation airflow based on chemical exposure patterns, reducing energy consumption and improving worker protection.

Predictive Maintenance Adoption Through Chemical-Driven Digital Twins

Chemical sensors are becoming central to predictive maintenance (PdM) programs. In April 2025, Siemens reported that integrating chemical and physical indicators into its Senseye platform cut unplanned downtime by 12% in 12 weeks for a major automotive manufacturer.

Sensors track lubricant oxidation, coolant contamination, and corrosion chemistry that vibration analytics often miss. In semiconductor fabs, ultra-high-purity chemical sensing supports the U.S. SMART USA Institute (2025), ensuring ppt-level impurity monitoring in deposition and etching, which is vital for 3nm and 2nm chip yield optimization.

Dense Low-Cost Sensing Grids for Hyperlocal Environmental Compliance

Governments are adding low-cost sensor networks to augment sparse reference-grade monitors. December 2025 findings on Hyperlocal Source Apportionment show machine-learning models using LCS data achieve MAE < 5% for urban pollution source prediction.

WMO and UNEP deployments in Mumbai, Lagos, and other megacities are accelerating demand for cost-efficient, cloud-connected chemical sensors that can identify school- and community-level exposure hotspots and enforce air-quality policies in real time.

Miniaturized Wearable Sensors for Decentralized Biochemical Health Monitoring

Chemical sensors are rapidly expanding into wearables and smart textiles. MXene-based electrochemical biosensing patches provide:

- Non-invasive detection of glucose, cortisol, lactate

- Continuous personalized health analytics

- 10–30% lower cost manufacturing through India-based MedTech scaling

These flexible sensors accelerate the transition toward decentralized diagnostics and consumer wellness monitoring. Integration into clothing, medical bands, and adhesive patches is enabling microfluidic sweat analysis outside clinical labs, driving a major adoption wave from sports medicine to chronic disease management.

Chemical Sensors Market Share and Segmentation Insights

Gas-Phase Chemical Sensors Dominate Safety-Critical Deployments Across Industrial and Environmental Monitoring

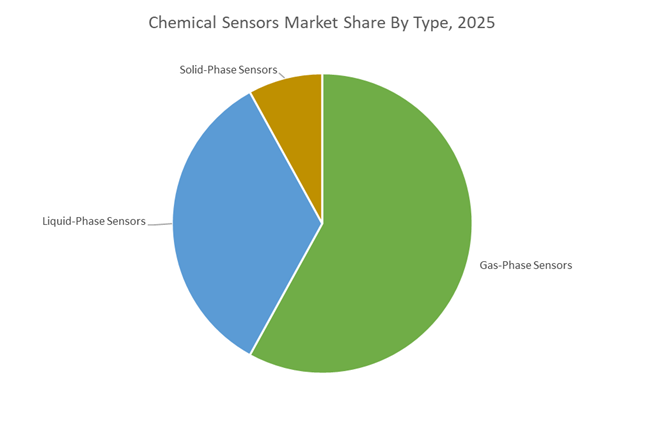

Gas-phase sensors account for 58% of the global chemical sensors market in 2025, reflecting their central role in industrial gas detection, toxic gas monitoring, and flammable gas detection systems. Electrochemical sensors, metal oxide semiconductor (MOS) sensors, non-dispersive infrared (NDIR), photoionization detectors (PID), and catalytic bead technologies are extensively deployed to monitor CO, H₂S, NH₃, Cl₂, methane, hydrogen, and oxygen deficiency in refineries, chemical plants, confined spaces, and wastewater facilities. Regulatory frameworks such as OSHA, ATEX, and IECEx are reinforcing mandatory gas detection, directly supporting segment dominance. Liquid-phase sensors represent the second-largest share, driven by pH sensors, ion-selective electrodes (ISE), dissolved oxygen sensors, and conductivity probes used in water quality monitoring, biopharmaceutical process control, and clinical diagnostics. Solid-phase sensors remain niche but are gaining traction through electronic nose (e-nose) platforms, soil contamination monitoring, and smart food freshness detection applications.

Industrial Safety Leads Application Demand as Environmental and Medical Sensing Accelerate Growth

Industrial safety and process control contribute 42% of total market demand, positioning this segment as the largest application area for chemical sensing technologies. Fixed and portable gas detectors are essential in oil and gas, petrochemicals, mining, and chemical manufacturing to ensure toxic gas detection, oxygen monitoring, and explosion prevention compliance. Integration of IoT-enabled gas sensors, wireless sensor networks, and predictive maintenance analytics is transforming plant safety architectures. Environmental monitoring is the fastest-growing segment, fueled by air quality monitoring systems (AQMS), water quality compliance under EPA and WFD standards, and global expansion of emission monitoring networks. Medical diagnostics remains a high-value segment, encompassing blood gas analyzers, glucose biosensors, electrolyte monitoring, and wearable chemical sensors such as continuous glucose monitors (CGM). Automotive applications are expanding into EV battery gas detection and hydrogen leak monitoring, while defense and homeland security sustain demand for chemical warfare agent detection and CBRN sensor platforms.

Competitive Landscape of the Chemical Sensors Market

The global Chemical Sensors Market in 2026 is being reshaped by hydrogen safety requirements, semiconductor fab expansion, smart infrastructure, and the rapid adoption of AI-enabled industrial automation. Market leaders are competing on selective gas detection, optical spectroscopy, real-time emissions monitoring, digital twins, and edge-to-cloud cybersecurity. Demand is accelerating across clean energy, lithium-ion battery safety, indoor air quality (IAQ), refinery automation, smart water, and semiconductor manufacturing, with vendors differentiating through laser-based sensing, autonomous operations, software-defined platforms, and ultra-high-purity process control. Strategic investments in US manufacturing, drone-mounted detection, OTA-enabled devices, and hydrogen-ready sensors are defining leadership in this highly regulated, high-growth sensor ecosystem.

Honeywell drives hydrogen safety and semiconductor-grade sensing with AI-enabled platforms

Honeywell International Inc. enters 2026 as a core architect of safety in the hydrogen economy, combining selective gas detection with cleanroom-grade precision. Its Hydrogen Leak Detection Sensor uses advanced compensation algorithms to identify trace hydrogen without cross-gas interference, supporting fuel cells and battery safety systems. The 13MM Pressure Sensor, launched in late 2025, maintains accuracy under extreme vacuum and thermal conditions, improving wafer yields in semiconductor fabs. Honeywell’s IPM Intelligent Particulate Matter Sensors apply laser light scattering for real-time IAQ and industrial hygiene. Strategically, the company is embedding chemical sensors directly into wafer fabrication, lithium-ion thermal runaway prevention, and clean-tech infrastructure, positioning itself at the intersection of safety, electronics manufacturing, and energy transition.

ABB leads autonomous emissions monitoring with laser optics and drone-based detection

ABB Ltd. dominates 2026 with ultra-sensitive optical technologies for oil & gas, utilities, and smart water. Its ACF5000 Continuous Emissions Monitoring System (CEMS) simultaneously measures up to 15 gas components via laser spectroscopy, enabling software-driven regulatory compliance. ABB’s MobileGuard™ and HoverGuard™ platforms deploy vehicle- and drone-mounted sensors with 1,000x higher leak sensitivity than conventional tools, mapping methane in real time using AI and GPS. A $110 million US manufacturing investment supports advanced sensor production for grid modernization and data centers. In water treatment, the UviTec optical analyzer delivers five-second BOD/COD readings, replacing lab-intensive workflows and accelerating adoption across environmental compliance, emissions control, and smart infrastructure.

Siemens connects chemical sensors to digital twins across the industrial metaverse

Siemens AG positions chemical sensors as the data backbone of its 2026 Industrial Metaverse strategy. Through Digital Twin Composer and NVIDIA Omniverse integration, Siemens merges real-world sensor inputs with virtual simulations, enabling manufacturers to validate upgrades before deployment. Its advanced CO₂ sensors anchor building automation and process control within the Xcelerator ecosystem, delivering 10 to 15% CAPEX optimization through design validation. Siemens’ SICAM Enhanced Grid Sensor strengthens smart grid visibility, while Industrial AI Operating Systems autonomously refine operations using live sensor data. With a massive installed base, Siemens excels at predictive maintenance, cloud-connected sensing, and AI-driven process optimization across energy, manufacturing, and smart cities.

Emerson accelerates autonomous operations with DeltaV-integrated analytical sensors

Emerson Electric Co. enters 2026 as a pure-play automation leader, tightly integrating chemical sensors into DeltaV™ Distributed Control Systems. Rosemount™ analytical sensors deliver high-accuracy pH, conductivity, and gas measurements for complex chemical and refining projects under Emerson’s Project Certainty framework. DeltaV v14/v15 platforms feature IEC 62443 cybersecurity from edge to cloud, safeguarding sensor networks in critical infrastructure. Emerson’s CHARMs-based electronic marshalling enables on-demand I/O without rewiring, accelerating plant expansions. Backed by a $12 billion free cash flow roadmap, Emerson is reinvesting heavily into software-defined sensing for LNG, semiconductors, and life sciences, reinforcing its leadership in secure, autonomous industrial operations.

MSA Safety expands gas analysis leadership through connected detection ecosystems

MSA Safety Incorporated strengthens its 2026 footprint with the acquisition of M&C TechGroup, adding premium gas analysis and sample conditioning to its portfolio. The ALTAIR® io four-gas detector anchors the MSA Grid ecosystem with OTA updates and NFC device assignment for large industrial fleets. Expanded manufacturing in Cranberry Township supports growth in fixed gas and flame detection. MSA also leads refrigerant management, launching monitoring systems aligned with low-GWP regulations showcased at AHR Expo 2026. With digital connectivity, fleet management, and process safety analytics, MSA delivers end-to-end gas detection for industrial hygiene, HVAC compliance, and critical infrastructure protection.

Figaro advances solid-state gas sensing for HVAC, hydrogen, and residential safety

Figaro Engineering Inc. remains the 2026 benchmark for solid-state semiconductor gas sensors used by global HVAC and automotive OEMs. Its FCM2630-L and CGM6812 modules lead detection of A2L mildly flammable refrigerants now mandated in modern air-conditioning systems. The upcoming TGS3870-F01 combines methane and carbon monoxide sensing in a compact format for residential safety. At Hyvolution Paris 2026, Figaro introduced hydrogen-ready alarms for EV and fuel-cell infrastructure. Known for exceptional material longevity and multi-decade reliability, Figaro supplies cost-effective, high-volume sensor components critical to building automation, hybrid mobility, and next-generation gas safety networks.

United States: Exposome Wearables, Microhotplate Arrays, and Hydrogen Hub Sensor Deployment

The United States chemical sensors industry is advancing rapidly across environmental monitoring, industrial safety, biopharmaceutical process control, and hydrogen infrastructure. In February 2026, the National Institute of Standards and Technology (NIST) awarded Phase II SBIR funding to MyExposome to commercialize silicone-based wearable chemical sensors designed for advanced “exposome” monitoring. These solvent-free extraction devices significantly expand the detection spectrum of environmental contaminants, including specialized PFAS compounds, positioning wearable chemical sensing as a high-growth subsegment in environmental health analytics. On February 12, 2026, NIST further allocated $3.2 million to eight small businesses, prioritizing semiconductor-integrated sensors and quantum-based photon sources for high-resolution chemical identification.

At the microfabrication frontier, NIST researchers finalized Microhotplate Gas Sensor Arrays featuring 100 μm x 100 μm suspended elements with millisecond-scale rapid thermal programming. Coupled with machine learning algorithms, these sensors can distinguish complex toxic industrial chemical (TIC) mixtures in real time—an essential capability for defense, emergency response, and refinery safety. In late 2025, Applied Imaging Solutions secured a $400,000 grant to develop short-wave infrared hyperspectral imaging sensors for AI-enabled, non-invasive bioreactor monitoring, enabling automated control of cell culture biomarkers in biopharma manufacturing. Simultaneously, the U.S. Department of Energy (DOE) prioritized hydrogen purity sensors across Hydrogen Hub rollouts, ensuring impurity levels remain below 0.1 ppm to protect fuel cell longevity. M&A activity in 2025 further consolidated “Smart Lab” sensor startups, aligning chemical detection platforms with federal “Buy Clean” data reporting frameworks.

China: Self-Sufficiency Milestones, Smart Environmental Networks, and AI-Optimized Catalyst Sensing

China’s chemical sensors market is expanding under state-directed industrial policy and green manufacturing mandates. Under the updated “Made in China 2025” roadmap (2023–2025 Green Book), China achieved 70% self-sufficiency in core basic components, including high-purity electrode materials for electrochemical sensors. In September 2025, Sinopec launched a major upgrade of the Tahe petrochemical complex, installing 16 new aromatics and ethylene units that serve as large-scale deployment sites for indigenous hazardous gas detection networks.

The Ministry of Industry and Information Technology (MIIT) introduced a two-year “Green Production” plan in late 2025 requiring automated sensing nodes across chemical facilities to support a 300 billion yuan green building materials revenue target. China’s chemical clusters are integrating platforms such as CLARITY Prime to feed AI models with real-time sensor data for catalyst optimization, reportedly reducing waste by 12% . Additionally, a national “Smart Environmental” network now deploys optical sensors to monitor NOx and VOC emissions across more than 100 industrial parks, reinforcing compliance with 15th Five-Year Plan air quality targets. These coordinated investments position China as a cost-competitive leader in industrial chemical sensing systems.

South Korea: Semiconductor-Embedded Sensors and TC2C Deployment under Strategic Tech Funding

South Korea has formally designated chemical sensors as a critical pillar within its 12 National Strategic Technologies portfolio. In early 2026, the Ministry of Science and ICT unveiled an €18.6 billion support package to embed sensing capabilities directly into advanced semiconductor packaging, accelerating convergence between chemical detection and wafer-level integration. Public-private commitments between 2025 and 2027 total €3.6 billion for commercialization of next-generation sensor materials, targeting global leadership in sensor-integrated electronics.

The $7 billion Shaheen project in Ulsan, led by S-Oil, will complete in late 2026 and deploy the world’s first large-scale thermal crude-to-chemicals (TC2C) sensor arrays for optimized intermediate production. These sensor networks enhance process efficiency while minimizing fuel by-product formation. At SEMICON Korea 2026, which attracted 70,000 visitors, 50 European SMEs integrated proprietary chemical-sensing IP into Korean wafer fabrication lines—further reinforcing South Korea’s role as a global nexus for high-precision industrial and semiconductor-grade chemical sensors.

European Union: OSOA Compliance, PFAS-Free Sensor Coatings, and Hydrogen Safety Monitoring

The European Union is reshaping the chemical sensors industry through regulatory harmonization and sustainability mandates. The “One Substance, One Assessment” (OSOA) framework entered into force on January 1, 2026, mandating a unified data platform for chemicals across pesticides, consumer goods, and food applications. This regulation compels manufacturers to deploy standardized, traceable chemical sensors for regulatory data reporting. In Germany, the Federal Ministry for the Environment (BMUV) released the draft 5th Amendment to the Chemicals Act (ChemG) in August 2025, requiring enhanced refrigerant leak detection sensors to comply with EU Regulation 2024/573 on F-gases.

PFAS restrictions under evaluation by the European Chemicals Agency (ECHA) are driving R&D into PFAS-free sensor coatings and ultra-trace detection technologies for persistent, mobile, and toxic (PMT) substances. In 2025, BASF inaugurated a 54 MW water electrolysis plant utilizing palladium-based hydrogen sensors to ensure safety and purity in green hydrogen pipelines. Concurrently, Digital Product Passport (DPP) implementation under the EU Circular Economy Act (planned 2026) requires embedded chemical sensors within industrial components to track composition across the product lifecycle, integrating sensing into decarbonized manufacturing ecosystems.

Singapore: IIoT Chemical Data Hubs and Jurong Island Digitalization

Singapore’s chemical sensors market is tightly linked to its Smart Nation strategy and Industrial IoT (IIoT) deployment. Approximately 20% of GDP-linked chemical operations now integrate advanced sensing systems, positioning Singapore as Asia’s primary IIoT business hub by late 2026. On Jurong Island, global manufacturers such as Denka and Afton Chemical expanded digital plant operations in 2025, deploying sensor networks on steam traps and pumps that reduce energy consumption by 7% and operational downtime by 25% .

Singaporean facilities generate approximately 144 terabytes of data per hour from distributed chemical sensing nodes, leveraging big data analytics to automate environmental compliance reporting and predictive maintenance. This data-scale infrastructure strengthens Singapore’s competitive advantage in real-time chemical monitoring and advanced process optimization.

Japan: NDIR Gas Sensor Leadership and ESG-Driven Workplace Monitoring

Japan’s chemical sensors industry is advancing through high-precision gas detection and regulatory transparency. In 2025, the Ministry of Health, Labour, and Welfare expanded mandatory workplace safety training requirements, driving adoption of portable multi-gas detectors across petrochemical plants and medical facilities. Japanese manufacturers continue to dominate the NOx and CO2 sensor segment using Non-Dispersive Infrared (NDIR) technology for automotive emissions compliance and building automation systems.

Corporate ESG disclosures in early 2026 increasingly highlight investments in advanced gas monitoring as a measurable workforce safety metric. This transparency aligns chemical sensor deployment with institutional investor scoring frameworks. Japan’s leadership in high-sensitivity air quality sensors and compact industrial gas detectors supports both domestic industrial compliance and export-driven growth in advanced environmental monitoring technologies.

Chemical Sensors Market Report Scope

Chemical Sensors Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$30.8 Billion

|

|

Market Size (2034)

|

$64.2 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Type (Gas-Phase Sensors, Liquid-Phase Sensors, Solid-Phase Sensors), By Technology (Electrochemical Sensors, Optical Sensors, Catalytic Bead Sensors, MEMS-Based Sensors, Flexible and Printed Sensors), By Application (Industrial Safety and Process Control, Environmental Monitoring, Medical Diagnostics, Automotive Systems, Defense and Homeland Security)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Honeywell International Inc., Siemens Aktiengesellschaft, Robert Bosch GmbH, Emerson Electric Co., ABB Ltd., Thermo Fisher Scientific Inc., 3M Company, Denso Corporation, ams-OSRAM AG, Sensirion AG, MSA Safety Incorporated, Infineon Technologies AG, Amphenol Corporation, STMicroelectronics N.V., Texas Instruments Incorporated

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chemical Sensors Market Segmentation

By Type

- Gas-Phase Sensors

- Liquid-Phase Sensors

- Solid-Phase Sensors

By Technology

- Electrochemical Sensors

- Optical Sensors

- Catalytic Bead Sensors

- MEMS-Based Sensors

- Flexible and Printed Sensors

By Application

- Industrial Safety and Process Control

- Environmental Monitoring

- Medical Diagnostics

- Automotive Systems

- Defense and Homeland Security

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Chemical Sensors Industry

- Honeywell International Inc.

- Siemens Aktiengesellschaft

- Robert Bosch GmbH

- Emerson Electric Co.

- ABB Ltd.

- Thermo Fisher Scientific Inc.

- 3M Company

- Denso Corporation

- ams-OSRAM AG

- Sensirion AG

- MSA Safety Incorporated

- Infineon Technologies AG

- Amphenol Corporation

- STMicroelectronics N.V.

- Texas Instruments Incorporated

*- List not Exhaustive