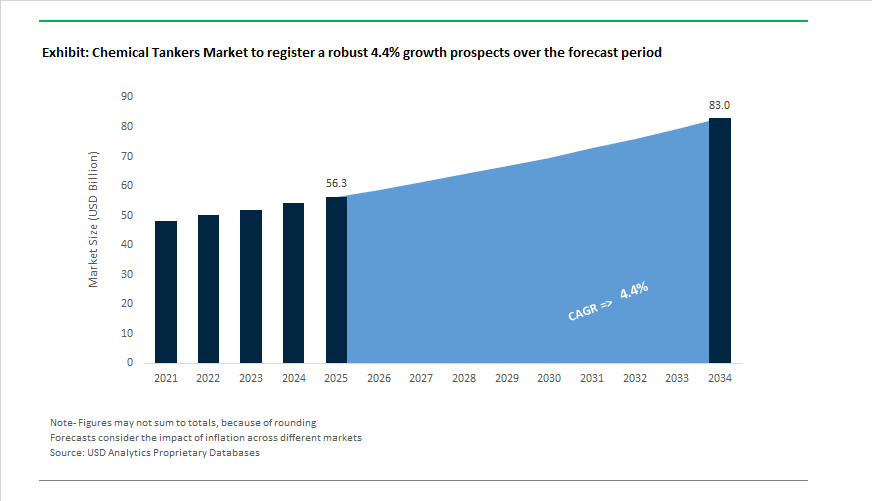

Chemical Tankers Market Overview 2025–2034: $56.3 Billion to $82.9 Billion at 4.4% CAGR Driven by Fleet Modernization and Decarbonization

The global chemical tankers market is projected to grow from $56.3 billion in 2025 to $82.9 billion by 2034, registering a CAGR of 4.4% over the forecast period. Market expansion is underpinned by rising seaborne trade in specialty chemicals, petrochemical intermediates, edible oils, and clean petroleum products, alongside structural investments in fleet renewal, alternative propulsion systems, and integrated logistics models. Demand for stainless steel and coated tankers capable of handling multi-grade cargoes remains strong as global chemical supply chains reconfigure to accommodate regional manufacturing shifts across Asia-Pacific and the Middle East.

Industry dynamics in 2024 and 2025 demonstrate clear momentum toward asset consolidation and scale optimization. In March 2024, MOL Chemical Tankers completed the $400 million acquisition of Fairfield Chemical Carriers, creating a combined fleet of 117 vessels and reinforcing its position as one of the largest commercial operators of multi-segregated stainless steel chemical tankers. In September 2024, Maersk Tankers launched a specialized chemical and oil pool, enhancing fleet utilization in volatile spot markets. By November 2024, Navig8 took delivery of the final vessel in its MR product and chemical tanker newbuild series, incorporating air lubrication systems and exhaust gas scrubbers to improve fuel efficiency and regulatory compliance.

Strategic capital deployment accelerated in 2025. In January 2025, ADNOC Logistics & Services completed a $1.04 billion acquisition of an 80% stake in Navig8, adding 32 modern tankers and strengthening its footprint across 15 global cities. In February 2025, Odfjell SE formed a joint venture with Nissen Kaiun in Bergen, securing access to high-specification Japanese-built stainless-steel tonnage for high-purity chemical trades. In October 2025, Fratelli Cosulich launched the world’s first methanol-powered IMO II chemical bunker tanker in Singapore, highlighting rapid decarbonization in bunker logistics. During the same month, Odfjell inaugurated the first operational deep-sea green corridor between Brazil and Europe using certified sustainable biofuels. In December 2025, Union Maritime integrated Rotor Sails on newbuild chemical tankers under construction in China. In January 2026, SDHI secured India’s first major $227 million order for six 18,000 DWT IMO Type II chemical tankers, reflecting geographic diversification of shipbuilding capabilities. These developments underscore a market characterized by sustainability-driven retrofits, alternative fuel adoption, and vertical supply chain integration.

From an industry structure perspective, the chemical tankers market is transitioning toward higher technical complexity. Ice Class 1A vessels, dual-fuel LNG-ready propulsion, methanol-capable engines, wind-assisted technologies such as Rotor Sails and VentoFoils, and AI-driven fleet optimization systems are increasingly embedded in newbuild specifications. Fleet operators are prioritizing emission reduction pathways in line with IMO carbon intensity targets, while chemical producers demand higher segregation flexibility and purity standards. The competitive landscape is consolidating around operators capable of combining commercial pooling, stainless steel tonnage, digital fleet management, and integrated ISO tank logistics, positioning the sector for moderate but resilient long-term growth through 2034.

Trends and Opportunities in the Chemical Tankers Market

Geopolitical Re-routing and Regionalization of Chemical Trade

The global chemical logistics network is restructuring as manufacturers prioritize regional resilience and tariff insulation over purely cost-led routing. Transatlantic and intra-Asia cargo flows are strengthening, with U.S. polyethylene gaining ground in Europe due to domestic ethane cost advantages. India’s 2025 import tariffs on Chinese intermediates have also redirected Asian chemical spot volumes, reshaping tanker deployment across Singapore, South Korea, and India-bound corridors.

Freight exposure remains elevated due to conflicts in the Black Sea and Red Sea, which have driven voyage detours toward safer lanes such as the Vertical Corridor through Bulgaria and Romania. These diversions are shifting significant petrochemical and natural gas volumes from land-based infrastructure to maritime transport, reinforcing chemical tanker demand even amid pricing volatility.

Regulation-Driven Fleet Renewal Under IMO CII and EU ETS

Older fleets built before 2010 are losing commercial relevance as IMO’s Carbon Intensity Indicator enforcement increases the cost burden of non-compliance. Vessels rated D for three years or E for one year must now execute corrective action plans, making them less attractive for long-term charters.

Simultaneously, the EU Emissions Trading System is moving toward full emissions cost inclusion by 2026. Leading owners piloting hybrid propulsion, wind-assist systems, and low-carbon fuel retrofits are cutting carbon-related operational costs by up to 15%. As a result, charterers are prioritizing tankers with improved EEDI ratings to meet Scope 3 reporting commitments across chemical value chains.

Dual-Fuel Newbuilds and Long-Term Sustainable Transport Contracts

Demand for LNG- and methanol-ready tankers is expanding as chemical producers shift procurement toward Net-Zero Logistics agreements. Data from DNV shows that alternative fuel vessel orders surpassed 230 units in the first eleven months of 2025, with methanol solutions capturing one-fifth of the market. The delivery of Vietnam’s first methanol dual-fuel MR2 vessel, ASP Rainbow, demonstrates operational confidence in new propulsion technologies and growing investor appetite for future-proof fleets.

Bunker infrastructure capacity is following suit. China executed its first bio-LNG bunkering operation in Dalian in December 2025, signaling strong regional readiness to support alternative fuel voyages on long-haul chemical trades. These developments enable shipowners to secure multi-year time charters with major chemical producers like BASF and Dow that are actively selecting carriers with verifiable GHG reductions.

Specialized Chemical Logistics for EV Battery Supply Chains

Electrification is driving a surge in seaborne volumes of hazardous battery chemicals such as lithium salts, electrolytes, and precursor solutions. These cargoes require stainless steel Type II and Type III tank configurations with inerting, thermal control, and enhanced corrosion resistance to meet new IMDG Code classifications effective January 2025 (UN3556 and UN3551).

Case studies such as Maersk’s temperature- and charge-controlled bulk lithium battery shipments show the broader shift toward precision chemical logistics. Reflecting this trend, Den Hartogh Logistics and Nissin Corporation entered a joint venture in December 2025 to serve specialized battery-chemical transport routes in Asia and Europe, highlighting a fast-expanding premium niche within the chemical tankers market.

Chemical Tankers Market Share and Segmentation Insights

Organic Chemical Cargoes Anchor Global Chemical Tanker Utilization as Methanol Trade Accelerates

Organic chemicals command 52% of the global chemical tankers market in 2025, making this the largest cargo category by transported volume. Core products include methanol, benzene, toluene, xylene, styrene, ethylene dichloride, acrylonitrile, and acetic acid, typically carried on IMO Class II and Class III chemical tankers. Demand is tightly linked to global petrochemical capacity additions, with Asia-Pacific leading consumption, driven by China’s coal-to-chemicals complexes and expanding downstream manufacturing in India and Southeast Asia. Methanol shipping is a standout growth driver, supported by rising MTO (methanol-to-olefins) capacity and its emerging role as a low-carbon marine fuel. Inorganic chemicals represent the second-largest segment, led by phosphoric acid, sulfuric acid, caustic soda, and ammonia, while vegetable oils and fats support steady food and biodiesel trade. Specialty liquid cargo remains small but premium, requiring high-spec stainless tanks and temperature-controlled logistics.

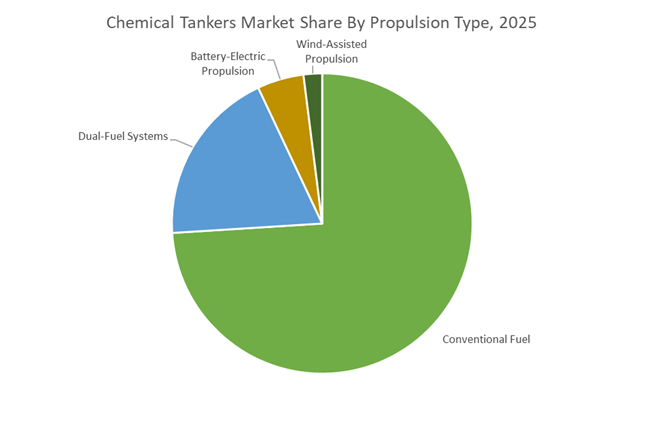

Conventional Fuel Dominates Fleet Propulsion as Dual-Fuel Tankers Gain Strategic Momentum

Conventional fuel propulsion accounts for 78% of the chemical tanker fleet in 2025, reflecting the long operational life of existing vessels powered by VLSFO, MGO, and scrubber-equipped HFO. IMO 2020 compliance, alongside EEXI and CII efficiency rules, is driving retrofits and selective fleet renewal, but legacy tonnage continues to dominate near-term capacity. Dual-fuel chemical tankers are the fastest-growing propulsion segment, with LNG-powered vessels delivering immediate reductions in CO₂, SOₓ, NOₓ, and particulate emissions. Expanding LNG bunkering infrastructure in Rotterdam, Singapore, and Houston is accelerating adoption, while methanol-ready and ammonia-ready newbuilds are reshaping orderbooks. Battery-electric propulsion remains limited to short-sea and inland chemical transport, led by Northern Europe and China. Wind-assisted technologies, including Flettner rotors and rigid sails, are emerging as auxiliary efficiency solutions, supporting charterer decarbonization strategies and ESG-driven freight procurement.

Competitive Landscape of the Chemical Tankers Market

The Chemical Tankers Market is dominated by asset-heavy operators combining stainless steel fleets, integrated terminals, and low-carbon shipping strategies to capture high-margin specialty chemical trade lanes. Market leaders are prioritizing fleet modernization, dual-fuel propulsion, green corridors, and digital pooling platforms to improve vessel utilization and carbon intensity indicators. Strategic expansion into Asia-Pacific, EV chemicals, and ammonia-ready tonnage reflects rising demand for sustainable chemical logistics. Competitive differentiation increasingly centers on super-segregated tank designs, ship-to-shore integration, and biofuel adoption, while geopolitical disruptions and newbuild deliveries continue reshaping spot rates and EBITDA outlooks across global operators.

Stolt-Nielsen leads integrated chemical logistics with parcel tanker dominance

Stolt-Nielsen, via Stolt Tankers, operates the world’s largest sophisticated chemical tanker fleet with 162 vessels totaling 3.1 million DWT, transporting high-grade chemicals, edible oils, and acids. Its Stolt-Nielsen Parcel Tankers model integrates seamlessly with Stolthaven Terminals and Stolt Tank Containers, delivering end-to-end ship-to-shore chemical logistics. In early 2026, the company issued conservative EBITDA guidance of USD 600 to 750 million, citing market stabilization alongside geopolitical trade risks and incoming vessel supply in 2H26. Strategically, Stolt targets a 50% reduction in carbon intensity by 2030 versus 2008 through hull optimization and biofuel trials.

Odfjell scales energy-efficient stainless steel tankers with green corridor leadership

Odfjell is widely recognized as the most energy-efficient deep-sea chemical tanker operator, specializing in high-spec stainless steel vessels and Super Segregator tankers with up to 28 separate cargo tanks. In late 2025, Odfjell ordered six advanced newbuildings ranging from 25,000 to 40,000 DWT from Japanese yards, with deliveries starting 1H2026. The company launched the first operational Brazil–Europe Green Corridor in 2025 using B24 biofuels. It also expanded Antwerp and Houston terminals by roughly 180,000 cbm, deploying automated Smart Pits to enhance turnaround safety and speed.

MOL Chemical Tankers accelerates consolidation with ammonia-ready fleet strategy

A subsidiary of Mitsui O.S.K. Lines, MOL Chemical Tankers rapidly expanded scale after acquiring Fairfield Chemical Carriers for USD 400 million in 2025, increasing fleet size from 85 to 121 vessels and strengthening its stainless steel tanker leadership. Entering Phase 2 of its Blue Action 2035 strategy in April 2026, MOL is shifting from asset acquisition toward monetization and execution. The company ordered nine ammonia-powered or ammonia-ready vessels with CMB.TECH, with deliveries starting late 2026. In January 2026, MOL also formed a joint venture with ONGC to develop the world’s largest ethane carrier fleet for US–India trade.

Hafnia grows chemical tanker exposure through methanol propulsion and digital pooling

Hafnia, part of BW Group, is the world’s largest product tanker operator and is rapidly expanding into IMO II/III chemical transport. In early 2026, Hafnia received its fourth dual-fuel methanol MR tanker under a joint venture with Socatra and TotalEnergies. The company is retrofitting ten Bird-class vessels with Wärtsilä EnergoFlow and EnergoProFin systems to cut fuel burn and underwater noise, improving CII scores. Hafnia also launched Seascale Energy, a bunker procurement JV now supplying green methanol. Its Hafnia Pool digitally aggregates third-party tonnage to maximize utilization and earnings.

Scorpio Tankers leverages scrubber-fitted fleet for margin advantage in easy chemicals

Scorpio Tankers is increasingly active in the IMO II/III easy chemical segment using its modern Handymax and MR fleet of 93 vessels with an average age of just 9.8 years. A key advantage is that 87% of its fleet is scrubber-equipped, enabling lower-cost high-sulfur fuel usage while remaining compliant, boosting margins in 2026. In Q1 2026, Scorpio finalized contracts for four MR newbuildings and entered the VLCC segment with two vessels scheduled for 2028 delivery. Capital strategy focuses on debt reduction and shareholder returns, supported by elevated spot rates driven by Red Sea and Atlantic disruptions.

Bahri strengthens Middle East chemical exports under Saudi Vision 2030 logistics push

Bahri Chemicals operates one of the world’s largest IMO II chemical tanker fleets, primarily transporting basic chemicals and polymers for SABIC and Aramco. Aligned with Saudi Vision 2030, Bahri is positioning itself as a global logistics hub connecting Asia, Europe, and Africa. The company is expanding aggressively into Asia-Pacific, opening regional offices to manage last-mile chemical distribution across China and India. Recent innovation includes Fleet Performance Monitoring Centers using satellite analytics to optimize hull cleaning schedules and reduce biofouling-related fuel penalties, strengthening Bahri’s competitiveness in long-haul petrochemical export corridors.

China Chemical Tanker Market: Shipbuilding Dominance and High-End Petrochemical Shift Driving Stainless Steel Parcel Tanker Demand

China remains the epicenter of global chemical tanker market growth, leveraging its leadership in shipbuilding capacity and petrochemical output expansion. In September 2025, the Ministry of Industry and Information Technology introduced the “Work Plan for Stabilizing Growth in the Petrochemical and Chemical Industry (2025 to 2026),” targeting 5% annual value-added output growth. Simultaneously, the National Development and Reform Commission enforced a 1 billion tonne crude oil refining capacity cap as of 2025, accelerating the strategic pivot from conventional refining to high-end chemical production. This structural shift is materially increasing demand for IMO Type II and IMO Type III stainless steel chemical tankers optimized for specialty chemicals, paraxylene, ethylene derivatives, and renewable feedstocks.

Fleet expansion reinforces this momentum. In October 2025, the joint venture between NYK-Stolt Tankers contracted Nantong Xiangyu Shipyard to construct two 38,000 DWT parcel chemical tankers featuring stainless steel cargo tanks and shore-side electricity systems for 2028 to 2029 delivery. Infrastructure upgrades at Huizhou Dayawan Petrochemical Industrial Park are expanding ethylene and PX output, increasing short-haul coastal chemical tanker rotations. Chinese shipyards are also integrating carbon capture and storage ready designs to compete in high-spec tanker segments traditionally dominated by South Korea. Rapid growth in Sustainable Aviation Fuel transport between Chinese production hubs and European ports further strengthens China’s strategic position in the global chemical tanker trade flow.

United States Chemical Tanker Market: Gulf Coast Export Expansion Reshaping MR Tanker Supply Dynamics

The United States chemical tanker market is experiencing structural transformation driven by shale gas feedstock advantages and surging methanol and ethylene exports from the Gulf Coast. Multibillion dollar methanol plant expansions have intensified parcel tanker traffic at the Port of Houston, tightening Medium Range chemical tanker availability and supporting elevated freight rates. Following European sanctions on Russian energy, the Gulf Coast to Europe route recorded a 107% increase in Suezmax and chemical freight rates in late 2025, signaling a long-term realignment of global chemical tanker trade routes.

Strategic infrastructure investments are consolidating U.S. export competitiveness. In March 2025, Mitsui O.S.K. Lines announced a $1.715 billion acquisition of LBC Tank Terminals, strengthening liquid bulk storage capacity across Houston, Freeport, and Baton Rouge. U.S.-based operators are accelerating adoption of IMO-certified stainless steel chemical tankers to support semiconductor and pharmaceutical grade chemical transport. Additionally, enhanced U.S. Coast Guard inspection protocols for vapor recovery systems are reshaping compliance standards for chemical tanker operators. The introduction of Cargo Flexibility tankers capable of multi-parcel transport further improves freight efficiency for specialty chemical producers, reinforcing the United States as a high-margin export hub within the global chemical tanker market.

Singapore Chemical Tanker Market: Digital Bunkering Leadership and Ammonia Infrastructure Acceleration

Singapore continues to function as the digital and decarbonization nerve center of the global chemical tanker market. Effective April 2025, the Maritime and Port Authority of Singapore mandated digital bunkering services and Electronic Bunker Delivery Notes as default requirements, eliminating paper documentation and saving an estimated 40,000 man-days annually. Beginning January 2025, AI-driven certificate renewal systems reduced processing times from three days to minutes, materially enhancing port call efficiency for chemical tankers.

Singapore is also positioning itself as a global ammonia bunkering hub with a planned 100,000 tonnes per year capacity to support zero-carbon chemical tankers. Regulatory reforms in April 2025 reduced Mass Flow Meter verification requirements from twice to once annually, saving operators approximately S$300,000 per year. Capital inflows into the Maritime Singapore Green Initiative are incentivizing vessels that exceed IMO carbon intensity standards through tax rebates. Collectively, these digitalization, green bunkering, and regulatory optimization measures strengthen Singapore’s competitive advantage in chemical tanker fleet management, bunkering efficiency, and alternative fuel adoption.

South Korea Chemical Tanker Market: High-Spec Shipbuilding and Alternative Fuel Innovation

South Korea’s chemical tanker market strategy centers on high value shipbuilding, alternative fuel propulsion systems, and complex cargo handling technologies. HD Korea Shipbuilding & Offshore Engineering established an ambitious $18 billion order target for 2025, prioritizing greener ships and specialized chemical carriers. The Port of Ulsan has been designated a hydrogen fuel cell vessel hub, targeting development of a universal hydrogen platform by end 2025, reinforcing South Korea’s leadership in next-generation tanker propulsion.

Technological innovation extends to materials engineering, where POSCO and Hanwha Ocean are co-developing high-manganese steel liquid hydrogen storage tanks for large energy tankers. The 2026 merger of business units within HD Hyundai Mipo and HD Hyundai Heavy Industries streamlines Small and Medium chemical tanker production. South Korean yards are pioneering onboard ammonia cracking systems that enable ammonia storage with hydrogen combustion, aligning with decarbonization mandates. A selective order-taking strategy prioritizes high-margin stainless steel parcel chemical tankers, reinforcing South Korea’s premium positioning within the global chemical tanker order book.

Norway Chemical Tanker Market: CCS Logistics and Zero-Emission Short-Sea Shipping Leadership

Norway operates as a live laboratory for decarbonized chemical tanker operations and Carbon Capture and Storage logistics. In August 2025, the Northern Lights project led by Equinor, Shell, and TotalEnergies began injecting CO2 into subsea reservoirs, catalyzing demand for a dedicated fleet of liquid CO2 carriers. A NOK 7.5 billion investment announced in March 2025 will triple injection capacity to 5 million tonnes annually, creating a new high growth sub-segment within the chemical tanker market.

State enterprise Enova awarded over $120 million in December 2025 to support hydrogen and ammonia powered bulk and chemical carriers. GC Rieber Shipping signed an LOI in June 2025 for a fully electric battery powered freighter optimized for coastal trade, while LH2 Shipping secured $29 million to expand its liquid hydrogen carrier fleet featuring 3.5 MW PEM fuel cells. Norway is also establishing ammonia bunkering stations at Mongstad, Florø, and Risavika, each with up to 2,000 cubic meters storage capacity. These initiatives position Norway at the forefront of zero-emission chemical tanker operations and CCS-enabled maritime logistics.

Germany Chemical Tanker Market: Hydrogen Import Infrastructure and EU ETS Compliance Transformation

Germany is emerging as Europe’s primary gateway for green hydrogen, ammonia, and synthetic fuel imports, fundamentally reshaping the European chemical tanker market. In February 2026, the German Bundestag is expected to pass the Hydrogen Acceleration Law, fast-tracking permitting for ammonia, methanol, and Liquid Organic Hydrogen Carrier import terminals. The federal Maritime Agenda 2025 provides funding for converting the Rhine River inland tanker fleet to low-emission propulsion systems, reinforcing Germany’s inland chemical logistics modernization.

Germany targets 10 GW of electrolysis capacity by 2030, necessitating substantial increases in chemical tanker calls to import hydrogen derivatives from Norway and North Africa. Wilhelmshaven and Brunsbüttel terminals are being expanded for cryogenic chemical transport, strengthening Germany’s role in ammonia and methanol trade flows. Research by the German Maritime Centre into Mobile Carbon Capture for tankers operating in the North Sea aligns with 2030 EU ETS requirements. The transition from traditional fuel oil cargoes to synthetic aviation fuels and methanol-based energy carriers further accelerates Germany’s integration into the future low-carbon chemical tanker value chain.

Chemical Tankers Market Report Scope

Chemical Tankers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$56.3 Billion

|

|

Market Size (2034)

|

$82.9 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Cargo Type (Organic Chemicals, Inorganic Chemicals, Vegetable Oils and Fats, Specialty Liquid Cargo), By Vessel Class (IMO Type 1, IMO Type 2, IMO Type 3), By Tank Material (Stainless Steel Tanks, Coated Tanks), By Fleet Type (Parcel Tankers, Product and Chemical Tankers, Inland and Coastal Tankers), By Propulsion Type (Conventional Fuel, Dual-Fuel Systems, Battery-Electric Propulsion, Wind-Assisted Propulsion)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Stolt-Nielsen Limited, Odfjell SE, Mitsui O.S.K. Lines, Ltd., Bahri Chemicals, Navig8 Group, Iino Kaiun Kaisha, Ltd., Sinochem Shipping Company Limited, Team Tankers International Ltd., Stena Bulk AB, Hansa Tankers Management AS, Wilmar International Limited, M.T.M. Ship Management Pte. Ltd., Ace Tankers Management B.V., Unibaltic Shipping Company, Womar Holdings Pte. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chemical Tankers Market Segmentation

By Cargo Type

- Organic Chemicals

- Inorganic Chemicals

- Vegetable Oils and Fats

- Specialty Liquid Cargo

By Vessel Class

- IMO Type 1

- IMO Type 2

- IMO Type 3

By Tank Material

- Stainless Steel Tanks

- Coated Tanks

By Fleet Type

- Parcel Tankers

- Product and Chemical Tankers

- Inland and Coastal Tankers

By Propulsion Type

- Conventional Fuel

- Dual-Fuel Systems

- Battery-Electric Propulsion

- Wind-Assisted Propulsion

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Chemical Tankers Industry

- Stolt-Nielsen Limited

- Odfjell SE

- Mitsui O.S.K. Lines, Ltd.

- Bahri Chemicals

- Navig8 Group

- Iino Kaiun Kaisha, Ltd.

- Sinochem Shipping Company Limited

- Team Tankers International Ltd.

- Stena Bulk AB

- Hansa Tankers Management AS

- Wilmar International Limited

- M.T.M. Ship Management Pte. Ltd.

- Ace Tankers Management B.V.

- Unibaltic Shipping Company

- Womar Holdings Pte. Ltd.

*- List not Exhaustive