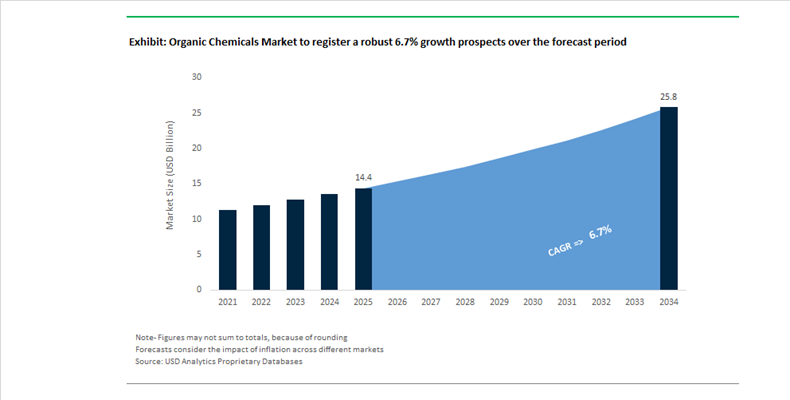

Organic Chemicals Market Valued at $14.4 Billion in 2025, Forecast to Reach $25.8 Billion by 2034 at 6.7% CAGR Driven by Olefins, Methanol, and Circular Feedstocks

The Organic Chemicals Market is valued at $14.4 billion in 2025 and is projected to reach $25.8 billion by 2034, expanding at a CAGR of 6.7%. Growth is anchored in rising demand for petrochemical intermediates such as ethylene, propylene, methanol, benzene, and acetic acid, alongside specialty organic additives for energy, coatings, and performance materials. Structural shifts in global feedstock economics, energy pricing disparities between regions, and the commercialization of chemical recycling technologies are redefining competitiveness across the value chain. The market is increasingly characterized by upstream consolidation, downstream divestments, and capital reallocation toward high-margin organic intermediates and sustainable feedstocks.

In July 2025, SLB finalized its acquisition of ChampionX, consolidating a major share of specialty organic production chemicals used in upstream oil and gas operations. The transaction integrates ChampionX’s surfactants, corrosion inhibitors, and biocides into SLB’s digital infrastructure, reinforcing pricing power and supply chain control in energy-focused organic chemicals. In October 2025, BASF SE completed the sale of its decorative paints business to Sherwin-Williams, exiting consumer-facing segments to intensify focus on essential organic intermediates including ethylene, propylene, and benzene. In June 2025, BASF also launched a bio-based Rheovis® product line utilizing renewable ethyl acrylate, delivering a 30% reduction in carbon footprint across organic rheology modifiers.

Capacity realignments accelerated in Q4 2025 when LyondellBasell Industries began construction of its Channelview Olefins project in Texas, designed to convert ethylene into approximately 882 million pounds of propylene annually. This expansion addresses tightening propylene supply for polypropylene, acrylic acid, and acetic acid derivatives. In 2026, LyondellBasell prioritized the operational ramp-up of its MoReTec-1 catalytic pyrolysis plant, converting plastic waste into circular liquid organic feedstocks to re-enter the monomer value chain. Meanwhile, Methanex Corporation completed the $2.05 billion acquisition of OCI Global’s international methanol business in mid-2025, solidifying its leadership in methanol supply, a critical precursor for formaldehyde and acetic acid synthesis.

Geographic production shifts intensified as Dow Inc. announced in early 2026 the shutdown of three upstream European assets by 2027 due to high energy and feedstock costs. This signals a migration of organic chemical production toward the U.S. Gulf Coast and Asia-Pacific. In India, government approval of large-scale PCPIR investments in 2025 attracted multinational players including Lubrizol and Celanese to establish greenfield plants and technical centers, reinforcing India’s role in specialty and bulk organic chemicals. In July 2025, Shell plc finalized the acquisition of Raj Petro Specialities to localize specialty organic lubricant and process oil production in India.

Upstream technology consolidation also accelerated. In H1 2025, Honeywell International Inc. completed its $2.2 billion acquisition of Johnson Matthey’s Catalyst Technologies division, strengthening catalyst innovation that underpins hydrogen, methanol, and olefin production. By early 2026, Chinese producers including Sinopec and PetroChina achieved near self-sufficiency in polypropylene through aggressive propane dehydrogenation capacity additions, significantly altering global trade flows of organic monomers and reinforcing Asia’s dominance in intermediate chemicals.

Organic Chemicals Market Trends and Opportunities

Trend: Feedstock Transition to Bio-Based Platform Chemicals for Drop-In Polymer Production

The global organic chemicals market is undergoing a decisive feedstock transition as corporate decarbonization mandates and the European Union Chemicals Industry Action Plan announced in 2025 accelerate the commercialization of bio-based platform chemicals. Bio-ethylene, bio-monoethylene glycol, and bio-para-xylene are gaining traction because they are chemically identical to fossil-derived counterparts, allowing polymer producers to decarbonize without retooling existing assets. This “drop-in” compatibility is particularly attractive to polyethylene, PET, and polyester value chains where capital efficiency and product consistency are non-negotiable.

A major inflection point occurred in October 2025 when Braskem approved an estimated R$4.2 billion investment to expand its Rio de Janeiro complex by 220,000 tons of ethylene capacity using sugarcane ethanol as feedstock. This expansion directly supports global demand for its I’m green™ bio-based polyethylene, particularly from EU and North American consumer brands seeking Scope 3 emissions reduction. Market pricing reinforces this momentum. In July 2025, FOB Northwest Europe bionaphtha traded at a premium of nearly USD 850 per metric ton over fossil naphtha, reflecting higher HVO feedstock costs but also strong voluntary offtake agreements in cosmetics, textiles, and specialty packaging.

Commercial proof points are also emerging beyond packaging. At K 2025 in Düsseldorf, carbon-neutral sports infrastructure products made with bio-based polyethylene demonstrated how organic chemical producers are successfully moving from niche sustainability showcases into scalable, high-visibility end markets such as urban infrastructure and professional sports facilities. Collectively, these developments position bio-based platform chemicals as a structural growth pillar rather than a discretionary green alternative.

Trend: Geographic Realignment and Supply Chain Consolidation in the Acetyls Value Chain

The acetyls segment of the organic chemicals market is experiencing rapid geographic realignment as producers seek cost leadership through scale, integration, and access to lower-cost energy. High power and carbon costs in Europe continue to compress margins for standalone plants, accelerating a shift toward large, integrated complexes in China and India that can efficiently serve global demand for acetic acid, vinyl acetate monomer, and acetate esters.

A defining transaction finalized during 2024–2025 was Ineos’s acquisition of BP’s acetyls and aromatics business. This consolidation gives Ineos controlling stakes in strategically located Chinese assets, including a majority interest in acetic acid and acetate ester units in Chongqing and near-total ownership of a major PTA site in Zhuhai. The move underscores a broader industry retreat from fragmented Western production toward Asia-centric hubs supplying polyester, coatings, and adhesive markets worldwide.

Pricing data from November 2025 illustrates the resulting regional divergence. Acetic acid prices in China increased by 1.5% due to tighter utilization rates and resilient demand from packaging and textiles, while German prices declined by 1% amid inventory overhangs and a seasonal slowdown in construction. India is positioning itself as a counterbalance within Asia. In 2024–2025, Indian Oil Corporation advanced a USD 7.39 billion investment at its Paradip complex to produce monoethylene glycol and phenol domestically, aiming to reduce import dependence and emerge as a competitive exporter of organic intermediates to ASEAN markets.

Opportunity: High-Purity Organic Electrolytes for Sodium-Ion and Solid-State Batteries

The emergence of sodium-ion and next-generation solid-state batteries is opening a high-margin specialty segment for ultra-pure organic chemicals. As battery OEMs diversify away from lithium to mitigate supply risk, sodium-ion technology is gaining momentum in stationary energy storage and grid-scale applications. While sodium relies on abundant raw materials, its electrochemistry places stringent demands on electrolyte purity and solvent stability to offset inherently lower energy density.

Battery material suppliers are now qualifying Grade 5 and Grade 6 purity levels for organic solvents such as ethylene carbonate and dimethyl carbonate. These specifications are critical to maintaining stable cycle life and suppressing parasitic reactions in advanced cathode systems. The first commercial sodium-ion grid projects entering operation in late 2025 have accelerated qualification cycles at Gigafactory scale, creating sustained demand for high-purity organic intermediates and functional additives. For organic chemical producers, this represents an opportunity to move up the value chain from commodity solvents into application-critical energy materials with long-term supply contracts.

Opportunity: Advanced Organic Formulations Powering the Agricultural Biologicals Surge

Agricultural biologicals are rapidly reshaping crop input markets, creating a parallel growth pathway for organic chemical producers. By 2025, biostimulants, biopesticides, and biofertilizers are projected to reach USD 11.8 billion, driven by regulatory pressure to reduce synthetic chemical use and by farm-level demand for sustainable yield enhancement. This shift is generating strong demand for advanced organic stabilizers, surfactants, encapsulation binders, and synergists.

One of the most acute challenges in biologicals is microbial stability. Beneficial organisms such as Bacillus thuringiensis require protection from UV radiation, desiccation, and temperature stress. This is driving innovation in organic micro-encapsulation systems and low-toxicity surfactants that preserve microbial viability without harming soil ecosystems. At the same time, biostimulant formulations based on amino acids and seaweed extracts are being paired with digital geospatial tools to enable variable-rate application, directly supporting the EU Green Deal objective of reducing synthetic fertilizer use by 20% by 2030.

In Latin America, particularly Brazil and Argentina, biological seed treatments are expanding rapidly. Organic chemical suppliers are capturing premium margins by providing specialized polymers and “stickers” that ensure biological actives remain adhered to seeds during mechanical planting. As adoption scales through 2026, agricultural biologicals are set to become a durable demand engine for high-value organic chemical formulations.

Organic Chemicals Market Share and Segmentation Insights

Alcohols and Amines Lead Organic Chemical Production as Versatile Industrial Intermediates

Alcohols and amines accounted for 32.80% of the Organic Chemicals Market by type in 2025, making them the most widely produced and utilized category of organic chemical intermediates. Their versatility as solvents, chemical intermediates, and reaction building blocks supports extensive use across pharmaceuticals, agrochemicals, plastics manufacturing, and personal care product formulation. High-volume chemicals such as methanol, ethanol, ethylene glycol, and methylamines underpin large-scale industrial chemical supply chains. A major 2025 development is the expansion of bio-based alcohol production, where fermentation-derived ethanol, bio-methanol, and bio-ethylene glycol are gaining market traction as sustainable feedstocks that enable renewable carbon content and support green chemistry initiatives across multiple chemical manufacturing sectors.

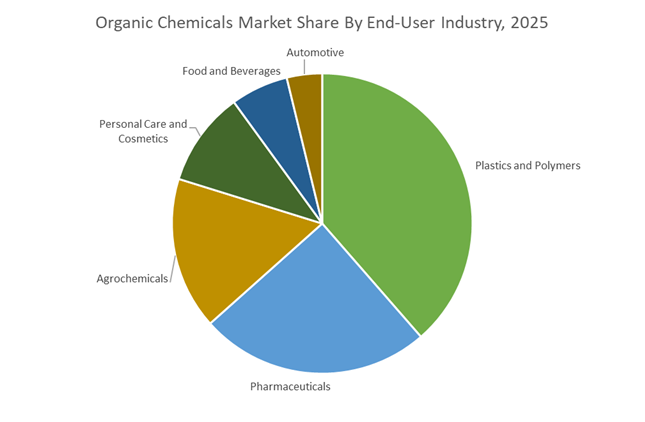

Plastics and Polymers Industry Drives Organic Chemical Demand Through Large-Scale Monomer Production

Plastics and polymers represented 38.60% of the Organic Chemicals Market by end-user industry in 2025, reflecting the central role of organic chemical intermediates in global polymer manufacturing. Organic chemicals serve as essential feedstocks for monomer synthesis, polymerization processes, and plastic additive production used in packaging, construction materials, consumer goods, and automotive components. The scale of global plastics production significantly influences demand for aliphatic compounds, aromatic intermediates, alcohol derivatives, and carbonyl chemicals. In 2025, the industry is increasingly shaped by circular economy initiatives, where chemical manufacturers develop monomers compatible with chemical recycling technologies while expanding bio-based feedstocks to reduce reliance on fossil-derived raw materials.

Organic Chemicals Market Competitive Landscape

The organic chemicals market in 2026 is shaped by margin compression, asset rationalization, and circular feedstock integration. Leading players are prioritizing Verbund-scale production, advanced recycling technologies, and bio-attributed chemicals to meet CBAM regulations, EPA compliance, and growing demand for low-carbon, high-purity chemical intermediates.

BASF strengthens integrated chemical dominance through Verbund 2.0 and aggressive cost restructuring

BASF is reinforcing its leadership in organic chemicals through its “Winning Ways” strategy, focusing on integrated production and portfolio optimization. The Zhanjiang Verbund complex provides a low-cost, world-scale manufacturing hub for Asia, enhancing feedstock flexibility and operational efficiency. With a 2026 EBITDA target of €6.2–€7.0 billion, BASF is addressing margin pressure through €2.3 billion in cost reductions. The company is streamlining European operations while strengthening core segments such as Chemicals and Materials. Its Ultrason® PPSU portfolio expansion aligns with regulatory compliance for food-contact safety. This integration-driven model positions BASF strongly in high-performance and sustainable organic chemicals.

Dow drives structural margin recovery through AI-led transformation and bio-circular chemical expansion

Dow is executing its “Transform to Outperform” plan to navigate industry overcapacity, targeting $2 billion in EBITDA improvement through automation and workforce optimization. The startup of Poly-7 and new EO capacity supports demand in home care, pharma, and energy sectors. ISCC PLUS certification for its Freeport MDI facility enables production of bio-attributed organic chemicals aligned with ESG requirements. Strategic shutdown of high-cost European assets is expected to deliver $200 million in annual savings. With advanced digitalization and circular chemistry integration, Dow is enhancing operational efficiency. This positions the company as a key player in next-generation sustainable chemical manufacturing.

SABIC enhances global competitiveness with AI-enabled operations and large-scale petrochemical integration

SABIC is leveraging its Transformation Program to optimize its portfolio and strengthen integration with Saudi Aramco’s energy value chain. With SAR 2.1 billion net income and SAR 7.2 billion free cash flow in 2025, the company maintains strong financial resilience. The commissioning of its 1 million ton MTBE plant enhances its position in fuel additives and chemical intermediates. Nearly 45% of its facilities now utilize AI-driven models, improving efficiency and predictive maintenance. The Fujian petrochemical complex in China strengthens its footprint in high-growth Asian markets. This scale and digital integration position SABIC as a major force in global organic chemicals.

ExxonMobil scales circular feedstock integration with advanced recycling and refinery-chemical synergy

ExxonMobil is leveraging its vertically integrated model and record upstream output to strengthen its organic chemicals portfolio. Its China Chemical Complex and Singapore Resid Upgrade enable efficient conversion of low-value feedstocks into high-value chemical intermediates. The company has scaled advanced recycling capacity to over 250 million pounds annually, supporting circular polymer mandates. With $15.1 billion in cost savings since 2019 and a target of $20 billion by 2030, ExxonMobil maintains strong cost leadership. Integration of refining and chemical operations enhances margin resilience. This positions ExxonMobil at the forefront of circular and high-efficiency chemical production.

LyondellBasell advances chemical recycling leadership with MoReTec technology and asset rationalization strategy

LyondellBasell is strengthening its competitive position through its Cash Improvement Plan, exceeding 2025 targets and aiming for $1.3 billion in cumulative savings by 2026. The MoReTec-1 plant in Germany represents a major step in catalytic chemical recycling, enabling conversion of plastic waste into high-quality feedstocks. Strategic divestment of European assets is optimizing its portfolio toward higher-margin regions. The company’s updated 2030 target of 800,000 metric tons of recycled and renewable polymers underscores its sustainability commitment. This balanced approach between cost discipline and innovation supports long-term growth. LyondellBasell is emerging as a key player in circular organic chemicals.

China – Policy-Led Stabilization and Specialty-Oriented Capacity Rebalancing

China’s organic chemicals industry is entering a managed stabilization phase anchored by coordinated industrial policy and targeted upgrading of the value chain. In late 2025, the Ministry of Industry and Information Technology, together with six central departments, issued the Work Plan for Stabilizing Growth in the Petrochemical and Chemical Industry (2025–2026), setting a clear mandate to sustain steady expansion in industry value addition while curbing volatility. A defining feature of this plan is strict control over incremental refining capacity paired with accelerated investment into higher-value organic chemical derivatives, including ethylene, paraxylene, and advanced polyolefins. This approach reflects a deliberate shift away from volume-driven commodity output toward specialty and performance-oriented organic chemicals with stronger margins and export resilience.

Green transformation and digitalization are being deployed as structural enablers. In early 2025, Beijing announced a dedicated investment package of approximately USD 1.5 billion to advance bio-based chemicals, prioritizing sustainable solvents and biodegradable polymer precursors. At the same time, national “AI plus petrochemicals” programs launched in 2025 are mandating the integration of exascale computing and advanced analytics into large-scale organic chemical production, improving yield control, energy efficiency, and emissions management. Export strategy is also evolving. China is aligning domestic organic chemical standards with international decarbonization frameworks by prioritizing green methanol and ammonia for marine fuels. Parallel policy targets for 2026 aim to lift domestic self-sufficiency in critical intermediates such as polycarbonate and high-performance fibers beyond 90%, reinforcing supply security amid tightening global trade conditions.

United States – Feedstock Advantage and Regulatory-Driven Realignment

The United States organic chemicals sector continues to benefit from structural feedstock competitiveness while navigating regulatory recalibration and reshoring priorities. In July 2025, a presidential proclamation granted a two-year compliance extension for the Synthetic Organic Chemical Manufacturing Industry HON Rule, citing national security considerations and the absence of commercially scalable emissions-control technologies. This regulatory relief has provided producers with near-term operational flexibility, allowing capital to be redirected toward modernization and emissions-reduction R&D rather than immediate retrofits.

Decarbonization remains a long-term policy anchor. The U.S. Department of Energy allocated approximately USD 500 million during 2024–2025 to accelerate research into bio-based organic chemicals, with an explicit objective of reducing sector-wide carbon intensity over the coming decade. Feedstock economics continue to favor domestic synthesis. According to the Energy Information Administration, U.S. crude oil output is projected to reach 13.4 million barrels per day in 2025, supporting cost-advantaged ethane and naphtha streams for organic intermediates. Regulatory pressure is also reshaping product portfolios. The Environmental Protection Agency’s tighter analytical standards for PFAS are forcing reformulation across surfactants and fluoropolymers, while federal reshoring initiatives are prioritizing domestic production of organic intermediates critical to semiconductors and medical sterilization, strengthening the strategic relevance of the sector.

India – Import Substitution and Infrastructure-Led Scale-Up

India’s organic chemicals industry is being repositioned through fiscal support, quality enforcement, and large-scale infrastructure build-out. The Union Budget 2025–26 allocated roughly USD 18.7 billion to the Ministry of Chemicals and Fertilizers, signaling strong central backing for domestic manufacturing expansion. Trade data underscores the urgency of this push. During April to July 2025, India’s organic chemical exports totaled USD 2.75 billion, while imports reached USD 5.30 billion, reinforcing policy focus on import substitution across key intermediates and specialty chemicals.

Execution is increasingly infrastructure-centric. The government is targeting more than USD 100 billion in sectoral investment by 2025–2026 through Petroleum, Chemicals and Petrochemical Investment Regions and a network of dedicated plastic parks. Quality control has become a parallel lever. In February 2025, India implemented Quality Control Orders covering over 150 chemical products, mandating Bureau of Indian Standards compliance for imports and leveling the competitive landscape for domestic producers. Strategic consolidation is also reshaping global positioning. In March 2025, Sudarshan Chemical Industries completed the acquisition of Heubach Group, creating a globally diversified organic pigment platform. At the state level, Odisha is advancing plans to emerge as a petrochemical hub, with phased investments scheduled to come online from 2026 onward.

Germany – Portfolio Rationalization Amid Energy and Cost Pressures

Germany’s organic chemicals industry is operating under pronounced structural stress driven by energy costs, carbon pricing, and subdued demand. The industry association VCI projects continued pressure on volumes and production into 2026, with average capacity utilization hovering near historic lows. In response, leading producers are executing decisive portfolio restructuring. BASF SE agreed in late 2025 to divest a majority stake in its coatings business to Carlyle Group, a move designed to refocus capital and management attention on core organic chemical clusters and higher-return segments.

Innovation remains a strategic counterweight to cost challenges. Germany is at the forefront of alternative feedstock development, with the FlowPhotoChem project demonstrating solar-driven production of chemical intermediates at pilot scale in 2025. At the same time, high-cost exits are reshaping the landscape. Ineos confirmed the shutdown of its allylics unit in Rheinberg in late 2025, citing uncompetitive energy and emissions costs. Research momentum is also being reinforced by global scientific recognition. The 2025 Nobel Prize in Chemistry for advances in metal-organic frameworks has accelerated German R&D in carbon capture, gas separation, and toxic containment technologies relevant to semiconductor and petrochemical applications.

Saudi Arabia – Capital-Backed Downstream Expansion and Circular Carbon Integration

Saudi Arabia is positioning its organic chemicals industry as a cornerstone of downstream diversification under Vision 2030. The updated National Industry Strategy targets a fourfold increase in downstream chemical output by 2035, supported by large-scale job creation and cluster-based development. Progress on flagship projects is central to this ambition. The Amiral complex, a joint venture between Aramco and TotalEnergies, is designed to supply nearby specialty chemical manufacturers with feedstocks from a high-capacity mixed-feed steam cracker, anchoring a new wave of organic chemical production.

Policy incentives are reinforcing capital deployment. The Standard Incentives Programme launched in 2025 provides substantial funding support for high-value chemical projects, lowering entry barriers for global and regional investors. Sustainability integration is also gaining traction. Saudi Arabia is embedding carbon capture, utilization, and storage into organic chemical clusters in Jubail and Yanbu, enabling the production of low-carbon methanol and blue ammonia. This circular carbon economy framework positions the Kingdom as a competitive supplier of lower-emissions organic chemicals to export markets increasingly shaped by carbon intensity benchmarks.

Comparative Country Snapshot – Organic Chemicals Industry

Organic Chemicals Market County Level Snapshot

|

Country

|

Core Policy Driver

|

Strategic Focus Area

|

Competitive Positioning

|

|

China

|

Growth stabilization and self-sufficiency

|

Specialty derivatives, bio-based chemicals

|

Scale leader transitioning up the value chain

|

|

United States

|

Feedstock advantage and reshoring

|

Bio-based R&D, strategic intermediates

|

Cost-competitive and security-focused

|

|

India

|

Import substitution and infrastructure

|

PCPIRs, quality compliance

|

Rapidly scaling domestic manufacturing base

|

|

Germany

|

Cost pressure and portfolio rationalization

|

Advanced feedstocks, CCUS technologies

|

Innovation-led, high-cost market

|

|

Saudi Arabia

|

Vision 2030 downstream expansion

|

Steam cracking, circular carbon

|

Capital-backed emerging global hub

|

Organic Chemicals Market Report Scope

Organic Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.4 Billion

|

|

Market Size (2034)

|

$25.8 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Type (Aliphatic Compounds, Aromatic Compounds, Carbonyl Compounds, Alcohols and Amines), By Source (Petrochemical-Based, Bio-Based, Coal-Based), By End-User Industry (Pharmaceuticals, Agrochemicals, Plastics and Polymers, Food and Beverages, Personal Care and Cosmetics, Automotive)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Sinopec, Dow, SABIC, ExxonMobil Chemical, LyondellBasell Industries, INEOS, Mitsubishi Chemical Group, LG Chem, Reliance Industries, PetroChina, Formosa Plastics, Wanhua Chemical, Shin-Etsu Chemical, Evonik Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Chemicals Market Segmentation

By Type

- Aliphatic Compounds

- Aromatic Compounds

- Carbonyl Compounds

- Alcohols and Amines

By Source

- Petrochemical-Based

- Bio-Based

- Coal-Based

By End-User Industry

- Pharmaceuticals

- Agrochemicals

- Plastics and Polymers

- Food and Beverages

- Personal Care and Cosmetics

- Automotive

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Organic Chemicals Industry

- BASF

- Sinopec

- Dow

- SABIC

- ExxonMobil Chemical

- LyondellBasell Industries

- INEOS

- Mitsubishi Chemical Group

- LG Chem

- Reliance Industries

- PetroChina

- Formosa Plastics

- Wanhua Chemical

- Shin-Etsu Chemical

- Evonik Industries

*- List not Exhaustive