Organic Solvents Market Reshaped by Methanol Consolidation, Bio-Based Alternatives, and Regulatory Realignment

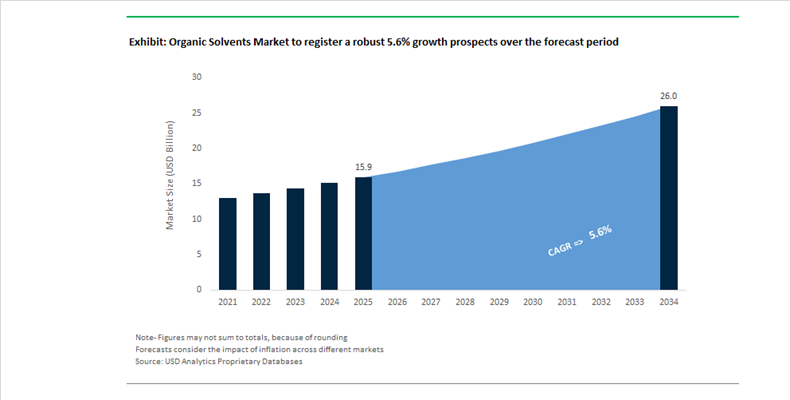

The Organic Solvents Market Valued at $15.9 Billion in 2025 Projected to Reach $26 Billion by 2034 at 5.6% CAGR is entering a structurally transformative phase defined by feedstock consolidation, circular solvent recovery technologies, and tightening environmental regulations across North America and Europe. Organic solvents—including methanol, ethanol, isopropanol, acetonitrile, toluene, and glycol ethers—remain foundational to pharmaceuticals, coatings, agrochemicals, electronics, and specialty polymer production. Between 2024 and 2026, strategic acquisitions and sustainability-driven product innovation have begun to redefine supply chain architecture and long-term investment flows within the sector.

In June 2025, Methanex Corporation finalized a $2.05 billion acquisition of OCI Global’s international methanol assets, including two world-scale facilities in Beaumont, Texas, and an idled European plant. This transaction solidifies Methanex’s position as the world’s largest methanol supplier, reinforcing its influence over one of the most critical organic solvent feedstocks. Methanol functions not only as a standalone solvent but also as a precursor for acetic acid, formaldehyde, and methyl tert-butyl ether (MTBE). In parallel, ExxonMobil advanced its proprietary methanol-to-jet (MTJ) pathway in 2025, repurposing renewable methanol into Sustainable Aviation Fuel (SAF). This pivot signals a broader repositioning of solvent molecules from conventional dissolvers toward strategic low-carbon intermediates in the energy transition.

Regional manufacturing shifts further illustrate market recalibration. In July 2025, Shell completed its acquisition of Raj Petro Specialities in India, adding approximately 350,000 tonnes per annum of specialty hydrocarbon solvent capacity. This strengthens Shell’s foothold in pharmaceutical, personal care, and transformer oil solvent applications within South Asia. Meanwhile, Dow Inc. initiated a strategic review of its European solvent and upstream chemical assets in late 2025, citing energy cost disadvantages and feedstock imbalances. The review aligns with capital redeployment toward cost-competitive geographies such as the U.S. Gulf Coast and the Terneuzen Path2Zero project. In early 2026, BASF announced the opening of its global Digital Hub in Hyderabad to integrate AI-driven supply chain optimization across its organic solvent portfolio, enhancing predictive production efficiency and logistics transparency.

Sustainability-driven innovation is accelerating in high-purity and pharmaceutical-grade solvents. Nitto Denko Corporation, in collaboration with Crysalis Biosciences, commercialized plant-derived bio-based acetonitrile through 2025, offering a renewable alternative to the traditional acrylonitrile byproduct route. Acetonitrile remains critical for DNA/RNA synthesis and high-performance liquid chromatography (HPLC). Concurrently, Asahi Kasei introduced a membrane dehydration system for pharmaceutical solvents, enabling energy-efficient recovery and reuse of ethanol and isopropanol without thermal distillation. These process innovations directly reduce solvent lifecycle emissions while improving operational economics for pharmaceutical manufacturers.

Regulatory pressures continue to influence formulation strategies. In December 2025, the European Union initiated consultations to ban additional persistent organic pollutants (POPs), including medium-chain chlorinated paraffins. Simultaneously, European Chemicals Agency postponed its opinion on ethanol’s classification as a biocidal active substance until 2026, temporarily stabilizing regulatory conditions for disinfectant-grade solvent producers. In Asia-Pacific, rising feedstock costs prompted BASF to implement a $200/MT price increase for Lupranate® TDI in February 2026, reflecting broader supply tightness in solvent-borne polyurethane intermediates.

Organic Solvents Market Trends and Opportunities

Trend: Accelerated Phase-Out of NMP and High-Hazard Solvents in Electronics Manufacturing

The organic solvents market is undergoing a structurally forced transformation as regulatory pressure intensifies across semiconductor fabrication, battery manufacturing, and advanced electronics. Traditional high-performance solvents such as 1-Methyl-2-pyrrolidone (NMP), long valued for their solvency power in photoresist stripping, electrode coating, and polymer processing, are now viewed as regulatory liabilities rather than enablers of yield. The enforcement of EU REACH Annex XVII Entry 71 during 2024–2025 has effectively ended the transition window for unrestricted NMP use. Under the regulation, NMP concentrations at or above 0.3% are prohibited unless manufacturers can guarantee worker exposure below 14.4 mg per cubic meter, a requirement that has proven costly and operationally complex for most fabs.

In parallel, the U.S. Environmental Protection Agency’s 2024 TSCA risk management rule introduced mandatory Workplace Chemical Protection Programs for NMP. These rules require continuous exposure monitoring, engineering controls, and detailed compliance documentation, significantly increasing the total cost of ownership for NMP-based processes. As a result, electronics manufacturers are actively qualifying safer drop-in alternatives such as gamma-Valerolactone and dimethyl sulfoxide, which offer comparable solvency with substantially lower toxicological risk. This shift is not discretionary; suppliers that fail to provide NMP-free formulations increasingly risk exclusion from European and North American supply chains.

The regulatory push is also accelerating innovation under the Safe and Sustainable by Design framework. The launch of EU-funded initiatives in late 2025 to develop bio-based solvents such as 2-MeTHF and ethyl lactate from organic waste streams underscores a strategic realignment. These solvents are being engineered specifically for high-hazard applications, allowing electronics and pharmaceutical manufacturers to meet compliance, worker safety, and sustainability targets simultaneously while maintaining process reliability.

Trend: Decarbonization Through Bio-Based Capacity Expansion and CBAM Alignment

Carbon intensity is rapidly becoming a commercial differentiator in the organic solvents market, driven by the expansion of the EU Carbon Border Adjustment Mechanism into chemicals. From 2026 onward, importers of organic basic materials will be required to account for embedded emissions, with certificate purchases beginning for 2026 imports by early 2027. This policy shift is forcing solvent producers to rethink feedstock strategies, as fossil-derived solvents carry a growing carbon cost that directly impacts pricing competitiveness in Europe.

In response, leading producers are investing aggressively in bio-based and carbon-captured solvent capacity. Large-scale investments announced during 2024–2025 demonstrate a clear pivot toward low-carbon production routes for ethylene carbonate, dimethyl carbonate, and other core solvents used in batteries, coatings, and polymers. These facilities are designed not only to meet purity requirements but also to materially reduce Scope 1 and Scope 2 emissions, allowing downstream customers to manage Scope 3 exposure more effectively.

The commercial relevance of this transition is reinforced by the rapid scaling of biorefineries producing wood-based bio-monoethylene glycol and renewable functional fillers. These materials offer direct substitution pathways for fossil-derived inputs in paints, coatings, and adhesives without requiring reformulation. As CBAM compliance moves from reporting to financial obligation, bio-ethanol- and bio-glycerin-derived solvents are increasingly commanding a sustainability premium, reshaping procurement strategies across Europe and influencing global pricing benchmarks.

Opportunity: Ultra-High-Purity Solvents for the Battery-Grade Manufacturing Ecosystem

The global gigafactory buildout is transforming organic solvents from broadly traded commodities into specification-driven specialty inputs. Battery-grade solvents used in lithium-ion, silicon-anode, and emerging solid-state cells must meet purity thresholds at the parts-per-billion level to prevent parasitic reactions that degrade cycle life and safety. This requirement has created a structurally attractive niche characterized by long qualification cycles, multi-year offtake agreements, and reduced exposure to short-term commodity price volatility.

Regionalization is a defining feature of this opportunity. New purification facilities commissioned during 2025 in North America illustrate the strategic necessity of producing ultra-high-purity solvents close to battery assembly lines, minimizing contamination risks during transport. Ethylene carbonate and related solvents are now routinely specified at 99.99% purity, with tight controls on water content, metal ions, and organic impurities.

Beyond volume growth, next-generation battery chemistries are expanding the functional demands placed on solvents. Silicon-dominant anodes and solid-state architectures require higher dielectric constants, improved low-temperature performance, and optimized viscosity profiles to enhance ionic conductivity. This is opening a high-margin innovation pathway for solvent producers capable of combining molecular design with advanced purification technologies, positioning battery-grade solvents as one of the most strategically attractive segments within the broader organic solvents market.

Opportunity: Food-Safe and GRAS Solvent Systems for Cannabis and Botanical Extraction

The gradual professionalization of the cannabis and botanical extraction industry is unlocking a new demand frontier for high-purity, food-safe organic solvents. Regulatory momentum in the United States, accelerated by late-2025 executive action to complete marijuana rescheduling, is aligning extraction standards more closely with pharmaceutical and nutraceutical manufacturing practices. This shift strongly favors Generally Recognized as Safe solvents such as USP-grade ethanol and tightly specified hydrocarbon blends over industrial-grade alternatives.

Regulatory enforcement at the state level is reinforcing this trend. Jurisdictions with stringent residual solvent limits are compelling extractors to adopt certified extraction-grade solvents that guarantee ultra-low residuals and zero contamination from heavy metals or pesticides. These requirements are driving a structural price premium, with certified solvent systems commanding 20 to 30% higher pricing than conventional industrial grades.

The expansion of federal testing standards under the updated Farm Bill has further widened the addressable market. By imposing uniform contaminant and residual solvent thresholds for ingestible cannabinoid products, the legislation effectively pushes hemp extractors into the same compliance framework as pharmaceutical manufacturers. For organic solvent producers, this convergence creates a durable growth opportunity centered on formulation expertise, certification, and supply reliability

Organic Solvents Market Share and Segmentation Insights

Alcohol-Based Organic Solvents Lead Market Demand Due to Versatile Solvency and Industrial Compatibility

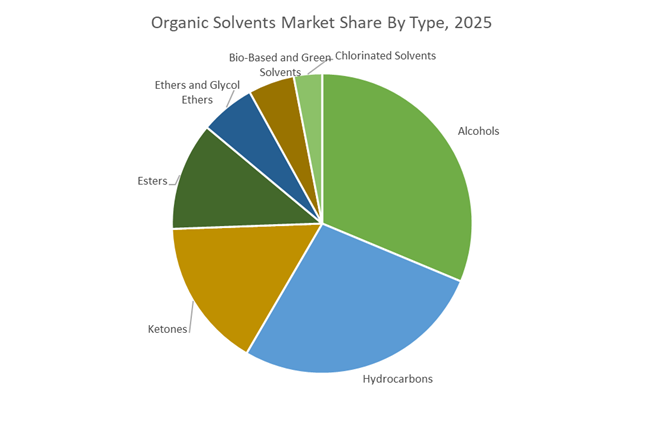

Alcohols accounted for 32.80% of the Organic Solvents Market by type in 2025, making them the most widely used solvent category across industrial and specialty chemical applications. Major alcohol solvents such as methanol, ethanol, isopropanol, and butanol are widely utilized in paints and coatings, pharmaceutical manufacturing, and personal care formulations due to their strong solvency, controlled volatility, and compatibility with both aqueous and organic systems. Established global production infrastructure and efficient supply chains further support their large-scale consumption. In 2025, the expansion of bio-alcohol production is influencing market dynamics, with fermentation-derived ethanol, bio-methanol, and bio-butanol gaining adoption as renewable solvent alternatives that support green chemistry initiatives and corporate sustainability goals across solvent-intensive industries.

Paints and Coatings Segment Drives Organic Solvent Consumption Across Industrial and Architectural Coating Production

Paints and coatings represented 38.60% of the Organic Solvents Market by application in 2025, reflecting the critical role solvents play in coating formulation and application performance. Organic solvents dissolve coating resins, adjust viscosity, and enable uniform film formation in solvent-borne coatings while also functioning as coalescing agents in waterborne paint systems. The global scale of architectural, industrial, and automotive coatings production continues to sustain strong solvent demand. A key industry development in 2025 is the high-solids and waterborne coating transition, where solvent usage per unit of coating is reduced, although total solvent consumption remains substantial due to overall coatings market growth and the ongoing need for specialty solvents in advanced industrial coating systems.

Organic Solvents Market Competitive Landscape

The Organic Solvents Market is undergoing structural transformation driven by bio-circular feedstocks, high-purity oxygenated solvents, and large-scale Asia-Pacific capacity expansion. Leading manufacturers are optimizing portfolios, investing in low-carbon technologies, and advancing specialty solvent innovation to meet demand across coatings, electronics, pharmaceuticals, and industrial applications.

BASF strengthens oxygenated solvents leadership through Verbund expansion in China

BASF SE is reinforcing its dominance in oxygenated solvents, particularly alcohols and glycols, by leveraging its integrated Verbund production model and strategic expansion in Asia-Pacific. The operationalization of its Zhanjiang Verbund site marks a multi-billion euro investment targeting high-growth coatings and adhesives demand in China. Concurrently, BASF achieved €1.7 billion in cost savings in 2025, with a €2.3 billion target by 2026 to offset European energy volatility. Its decarbonization roadmap projects CO2 emissions at 17.2–18.2 million metric tons in 2026, balancing capacity expansion with asset de-fossilization. The divestment of its decorative paints business to Sherwin-Williams sharpens its focus on upstream chemical intermediates and high-performance industrial solvents. This integrated strategy enhances cost efficiency, supply reliability, and regional competitiveness.

Dow advances high-purity functional solvents for electronics and sustainable applications

Dow Inc. is positioning itself as a leader in high-purity organic solvents for electronics, aerospace, and medical applications through its Transform to Outperform strategy. The launch of DOWSIL™ DS-2025, a non-flammable silicone cleaning solvent, highlights its focus on specialty functional solvents free from aromatic and halogenated compounds. Dow’s ISCC PLUS certification at its Freeport facility strengthens its bio-circular solvent portfolio, enabling lower-carbon production pathways. The establishment of its Cooling Science Studio in Shanghai supports innovation in semiconductor and EV thermal management fluids. Additionally, a CAD $1.62 billion financial inflow in 2026 enhances liquidity for R&D in renewable-based solvents. This combination of innovation, sustainability, and regional investment strengthens Dow’s competitive positioning in advanced materials markets.

Shell restructures portfolio toward low-carbon and high-purity hydrocarbon solvents

Shell Chemicals is undergoing a strategic portfolio transformation, exiting traditional refinery-integrated assets to prioritize low-carbon performance chemicals and high-purity hydrocarbon solvents. The divestment of its Singapore Chemicals & Refinery complex reflects a shift toward higher-margin, lower-emission projects. Under CEO Wael Sawan, Shell has achieved $5 billion in structural cost savings since 2022, including $2 billion in 2025 through operational simplification. Its 2026 capital expenditure guidance of $20–22 billion focuses on integrated gas and upstream value chains that secure feedstock supply for solvent production. Shell’s global supply chain strength enables consistent delivery of high-purity solvents while maintaining a 52% shareholder distribution rate. This strategic realignment enhances capital efficiency and long-term profitability.

ExxonMobil scales CCS-integrated solvent production and closed-loop recycling systems

ExxonMobil Product Solutions is leveraging its scale and proprietary technologies to lead in low-emission organic solvents production. Its updated 2030 Plan targets $4 billion in earnings growth, with 60% driven by projects coming online by 2026. The deployment of Carbon Capture and Storage (CCS) across major production hubs is expected to enable early achievement of 2030 GHG intensity targets. ExxonMobil’s Proxxima™ systems and advanced recycling technologies support a closed-loop solvent recovery model, enhancing sustainability for industrial customers. Strong financial positioning, including a $20 billion annual share repurchase program, underpins its capital-intensive transition. This integration of CCS, advanced materials, and recycling strengthens its competitive edge in sustainable solvent manufacturing.

Eastman leverages molecular recycling to produce high-value specialty solvents

Eastman Chemical Company is differentiating itself through molecular recycling and specialty materials innovation in the organic solvents market. Its Kingsport methanolysis facility, the world’s largest polyester recycling plant, generated $60 million in incremental earnings in 2025 while converting plastic waste into high-value chemical intermediates. With 55% of revenue generated outside North America, Eastman is heavily exposed to high-growth Asian markets, particularly in automotive and construction solvents. The company is targeting $125–$150 million in cost reductions in 2026 to maintain margin resilience. Its Chemical Intermediates segment is shifting toward differentiated, high-margin applications in agriculture and pharmaceuticals, moving away from commodity solvents. This strategy enhances profitability and positions Eastman in premium solvent segments.

LyondellBasell advances circular solvent feedstocks and European portfolio optimization

LyondellBasell (LYB) is executing a value-driven strategy centered on circular economy initiatives and operational streamlining. Investments in MoReTec-2 chemical recycling and Flex-2 propylene expansion aim to generate sustainable feedstocks for oxygenated solvent production. The company is simultaneously divesting four European assets by mid-2026 to focus on high-performing core segments. With $8.1 billion in liquidity at the end of 2025 and planned capital expenditure of $1.2 billion in 2026, LYB maintains strong financial flexibility. CEO Peter Vanacker’s strategic pivot emphasizes markets with proven demand and regulatory support for sustainable solvents. This balanced approach of circular innovation and portfolio optimization strengthens LYB’s long-term competitiveness.

China – Policy-Led Green Transition and High-Purity Specialization

China’s organic solvents industry is undergoing a rapid structural shift driven by state-backed green investment, specialty chemical expansion, and tightening emission controls. In March 2024, the central government earmarked USD 1.5 billion for bio-based chemicals, with sustainable organic solvents prioritized to lower carbon intensity across industrial parks. This funding has accelerated substitution away from aromatic solvents toward oxygenated and bio-derived alternatives in coatings, electronics, and advanced materials. Capacity expansion is reinforcing this transition. In March 2025, Arkema completed a large-scale expansion at its Changshu site, increasing specialty chemicals capacity by 250 percent to serve electric vehicle batteries and solar photovoltaic manufacturing, both of which demand high-purity, low-residue solvent systems.

Industrial policy is tightening execution. The Ministry of Industry and Information Technology is enforcing a local-for-local production model, prompting multinational producers such as BASF SE to localize low-VOC dispersions and solvent-borne resins in Shanghai to ensure supply security and regulatory compliance. Innovation intensity has increased following the 2025 Nobel Prize recognition of Metal-Organic Frameworks, with Chinese institutes fast-tracking MOF-enabled solvent recovery for semiconductor fabs. Looking ahead, stricter VOC caps scheduled for 2026 in the Yangtze River Delta are accelerating the phase-down of toluene and xylene, while energy mandates require 30% of new solvent facilities to run on non-fossil power by end-2026, embedding decarbonization into capacity planning.

United States – Semiconductor-Grade Purity and Regulatory Modernization

The United States organic solvents market is being reshaped by domestic sourcing priorities, ultra-high purity requirements, and regulatory modernization. In August 2024, Eastman Chemical Company launched a domestic electronic-grade solvent unit to secure a made-in-USA supply chain for semiconductor lithography and cleaning applications. This move aligns with federal support for reshoring critical materials. Complementing supply security, the Department of Energy allocated USD 500 million in 2024 to advance bio-based chemicals, targeting a 40% emissions reduction by 2035 for the solvents segment.

Regulatory updates are changing formulation choices across downstream industries. The Environmental Protection Agency’s January 2025 update to aerosol-coating reactivity limits is driving a decisive shift toward oxygenated solvents and less-reactive blends in paints and coatings. Market structure is also consolidating. In October 2025, Berkshire Hathaway completed the acquisition of OxyChem, consolidating U.S. chlorinated solvent and chlor-alkali production. Purity thresholds continue to rise. ExxonMobil announced plans to deliver 99.999% purity isopropyl alcohol by 2026 for next-generation 2 nm semiconductor fabs. In parallel, the USDA’s 2025 Sunset Review renewed allowances for synthetic ethanol and isopropanol in organic agriculture through 2030, stabilizing demand in agri-input applications.

India – Capacity Influx, Export Enablement, and Solvent Recovery

India’s organic solvents industry is scaling rapidly on the back of petrochemical investment, export facilitation, and stricter environmental enforcement. In late 2025, the country announced USD 37 billion in petrochemical investments, positioning India to capture a substantial share of global benzene and paraxylene additions by 2030. This feedstock influx is strengthening domestic solvent availability for pharmaceuticals, textiles, and coatings. Capacity expansion is visible at the specialty end. The Lubrizol Corporation doubled capacity at its Dahej facility in late 2025, focusing on solvent-based performance additives for South Asia.

Policy reforms are improving market access. In July 2025, the Directorate General of Foreign Trade simplified certification for organic textile exports, removing redundant transaction certificates and easing solvent-compliant processing. Environmental compliance is tightening. The Central Pollution Control Board’s enforcement of Zero Liquid Discharge norms for pharmaceutical clusters in 2026 is driving adoption of high-efficiency solvent recovery and reuse systems. Demand from food processing is also expanding. With the sector projected to grow sharply over the long term, government incentives are supporting domestic production of food-grade solvents such as hexane and ethanol to meet hygiene and residue standards.

Germany – Decarbonization, Portfolio Realignment, and Regulatory Tightening

Germany’s organic solvents market is characterized by aggressive decarbonization, portfolio restructuring, and stringent regulatory enforcement. In June 2025, BASF SE completed the transition of its Rheovis® and solvent-borne portfolios to bio-based mass-balance variants at Ludwigshafen, reducing product carbon footprints without altering performance. Strategic realignment followed. In October 2025, BASF agreed to sell a majority stake in its coatings business to Carlyle Group, a move expected to reshape solvent-borne coatings supply across Europe upon closing in 2026.

Energy economics are forcing structural exits. Ineos confirmed the closure of its allylics unit at Rheinberg in late 2025 due to uncompetitive energy costs, tightening regional supply for epoxy-related solvents. Germany is also leading enforcement of the EU Persistent Organic Pollutants Amendment 2025, which imposes strict limits on pentachlorophenol and its esters from April 2025, accelerating substitution toward safer solvent chemistries in wood treatment and specialty applications.

South Korea – Electronic-Grade Solvents and Circular Battery Chemistry

South Korea’s organic solvents industry is anchored in advanced R&D, electronic-grade purity, and circular battery manufacturing. During 2024–2025, the country allocated a record 5.2% of GDP to research and development, with a significant share directed toward high-purity solvents for semiconductors and battery electrodes. This investment is underpinning next-generation cleaning, photoresist stripping, and electrolyte processing capabilities required by leading fabs.

Battery manufacturing is a key demand driver. Korean producers are pivoting toward recycling and replacement pathways for N-methyl-2-pyrrolidone to address cost, safety, and sustainability pressures in battery hubs such as Cheongju and Ulsan. Regulatory facilitation is accelerating innovation. In 2025, the government streamlined patent approvals for levulinate-ketal solvents aimed at replacing silicones in cosmetics, positioning South Korea as a source of novel green solvent IP for consumer and specialty applications.

Comparative Country Snapshot – Organic Solvents

Organic Solvents Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Key Solvent Focus

|

Strategic Position

|

|

China

|

Bio-based funding and VOC caps

|

Oxygenated, electronic-grade solvents

|

Scale with green transition

|

|

United States

|

Semiconductor purity and reshoring

|

Ultra-pure IPA, bio-solvents

|

High-value, security-focused

|

|

India

|

Petrochemical investment and ZLD

|

Pharma and food-grade solvents

|

Fast-scaling manufacturing base

|

|

Germany

|

Decarbonization and POPs bans

|

Mass-balance bio-solvents

|

Compliance-led premium market

|

|

South Korea

|

R&D intensity and battery growth

|

Electronic-grade, recycled NMP

|

Innovation-driven niche leader

|

Organic Solvents Market Report Scope

Organic Solvents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.9 Billion

|

|

Market Size (2034)

|

$26 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Type (Alcohols, Hydrocarbons, Ketones, Esters, Chlorinated Solvents, Ethers and Glycol Ethers, Bio-Based and Green Solvents), By Application (Paints and Coatings, Pharmaceuticals, Electronics and Semiconductors, Printing Inks, Adhesives and Sealants, Agricultural Chemicals, Personal Care and Cosmetics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, ExxonMobil, Dow, Shell, LyondellBasell Industries, Eastman Chemical, Arkema, Huntsman, Celanese, Sinopec, Chevron Phillips Chemical, INEOS, Sasol, Mitsui Chemicals, Sudarshan Chemical Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Solvents Market Segmentation

By Type

- Alcohols

- Hydrocarbons

- Ketones

- Esters

- Chlorinated Solvents

- Ethers and Glycol Ethers

- Bio-Based and Green Solvents

By Application

- Paints and Coatings

- Pharmaceuticals

- Electronics and Semiconductors

- Printing Inks

- Adhesives and Sealants

- Agricultural Chemicals

- Personal Care and Cosmetics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Organic Solvents Industry

- BASF

- ExxonMobil

- Dow

- Shell

- LyondellBasell Industries

- Eastman Chemical

- Arkema

- Huntsman

- Celanese

- Sinopec

- Chevron Phillips Chemical

- INEOS

- Sasol

- Mitsui Chemicals

- Sudarshan Chemical Industries

*- List not Exhaustive