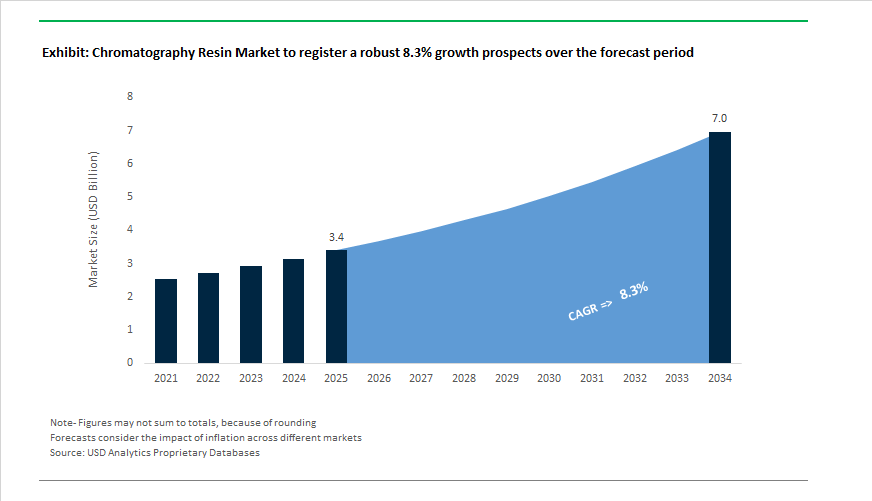

Chromatography Resin Market Outlook 2025–2034: $3.4 Billion to $7 Billion at 8.3% CAGR Driven by Biologics and Gene Therapy Scale-Up

The global Chromatography Resin Market is projected to grow from $3.4 billion in 2025 to $7 billion by 2034, registering a CAGR of 8.3%. Market expansion is closely linked to the rapid scale-up of monoclonal antibody production, mRNA platforms, viral vector manufacturing, and next-generation biotherapeutics. Chromatography resins, particularly Protein A, ion exchange, affinity, hydrophobic interaction, and size exclusion resins, remain central to downstream bioprocessing workflows. Increasing molecule complexity and higher purity requirements are pushing biopharmaceutical manufacturers to adopt high-capacity, alkali-stable, and sustainable resin platforms capable of withstanding multiple cleaning-in-place cycles while maintaining binding performance.

Strategic acquisitions and portfolio consolidation intensified in 2024–2026, reinforcing competitive positioning in downstream purification. In October 2025, Merck KGaA signed an agreement to acquire JSR Life Sciences’ chromatography business, strengthening its Protein A resin capabilities through the Amsphere™ platform. In June 2025, Cytiva completed its $1.6 billion global expansion program initiated in 2019, adding new chromatography and filtration facilities in the United States, Sweden, the UK, and Florida to secure resin supply capacity through 2026. Earlier, in February 2024, Danaher announced a $500 million dedicated chromatography resin manufacturing facility in Massachusetts to support North American bioprocessing demand. Tosoh Corporation expanded Toyopearl and TSKgel resin production capacity in Japan in February 2024, reflecting strong global demand for large-scale biologics purification. These investments indicate a supply-side push to address persistent capacity constraints in high-value affinity and ion-exchange resins.

Innovation in resin chemistry and bead architecture is accelerating differentiation. In April 2025, Cytiva introduced MabSelect™ SuRe 70 and MabSelect™ PrismA X resins produced from renewable agarose, targeting high-capacity monoclonal antibody purification while reinforcing sustainability credentials. Repligen launched convective AVIPure® HiPer™ resins for AAV9, AAV8, and anion exchange applications in December 2025, leveraging DuloCore™ base bead technology to improve viral vector processing speed and molecule stability. In December 2024, Repligen introduced AVIPure® dsRNA Clear OPUS® columns designed to remove double-stranded RNA impurities critical to mRNA therapeutic safety. DuPont expanded into oligonucleotide purification with AmberChrom™ TQ1 in May 2025, addressing growing RNA-based therapeutic demand. These developments reflect the transition from traditional porous diffusion-based resins to advanced convective and affinity technologies optimized for large biomolecules.

Operational efficiency and lifecycle performance remain core competitive levers. In June 2024, Ecolab launched DurA Cycle™ Protein A resin engineered to withstand extended sodium hydroxide cleaning cycles, reducing cost per gram of antibody purified. In July 2025, Ecolab Life Sciences introduced Purolite™ AP+50 affinity resin to enhance yield and throughput in regulated biopharmaceutical purification. Shimadzu strengthened its chromatography systems integration strategy in October 2024 through investment in Sepragen Corporation, expanding access to radial-flow chromatography platforms across Asia. Sunresin broadened application scope in September 2024 with medicinal powder resins designed for ion-exchange functionality in oral drug delivery. Collectively, these capacity expansions, affinity resin innovations, viral vector-focused chemistries, and sustainability-driven material advancements position the chromatography resin market for sustained mid-to-high single-digit growth through 2034.

Chromatography Resin Market Trends and Drivers

Rapid Industrial Shift Toward Continuous Multi-Column Chromatography (MCC) Resins to Maximize Productivity

One of the most transformative trends in the chromatography resin market is the industrial pivot away from batch purification toward continuous Multi-Column Chromatography (MCC) — a move driven by rising biomanufacturing costs, biologics volume growth, and facility footprint pressures. As of late 2025, MCC systems such as Sartorius Resolute® BioSMB have demonstrated the ability to reduce resin usage volumes by up to 80%, without compromising biologic purity or yield. This operational shift is essential for managing high-titer monoclonal antibody (mAb) streams, where traditional single-column systems would require oversized columns and excessive buffer inventory.

New MCC-compatible resin portfolios launched in 2024–2025, including JSR Life Sciences’ Amsphere A+, are engineered with fast-cycling ligand chemistry and advanced alkali resistance, enabling hundreds of reuse cycles while maintaining high binding capacity and mechanical stability. These resin formats are becoming a strategic procurement priority for CDMOs, particularly those targeting lean downstream economics, COGS reduction, and flexible scale-out models for biologics.

High-Selectivity Mixed-Mode Resins Gain Traction for Complex Modalities such as AAV, Bispecific Antibodies, and Viral Vectors

As biologics pipelines diversify beyond monoclonal antibodies into AAV gene therapies, bispecific antibodies, fusion proteins, and oncolytic vectors, manufacturers require mixed-mode chromatography resins that go beyond size- or charge-only separation. In January 2025, Bio-Rad Laboratories introduced Nuvia wPrime 2A Media, a multimodal resin combining weak anion-exchange (AEX) and hydrophobic interaction chromatography (HIC), engineered to remove host cell proteins and high-molecular-weight aggregates while preserving target viral particles.

Meanwhile, research published in February 2025 (PMC) confirms that consecutive affinity and ion-exchange workflows can deliver >90% full-to-empty capsid ratios for AAV9 vectors. These results underscore why downstream technologists are transitioning toward mixed-mode formats that leverage ionic, hydrogen-bonding, and hydrophobic interactions to resolve increasingly complex biomolecular products.

GMP-Ready Chromatography Resins for mRNA and Plasmid DNA (pDNA) Commercial Manufacturing

A significant commercial expansion opportunity lies in GMP-grade chromatography resins designed for mRNA purification and plasmid DNA (pDNA) production, driven by global supply chain diversification of RNA-based medicines.

mRNA clinical platforms have accelerated demand for Oligo dT affinity resins, which streamline purification by selectively capturing polyadenylated mRNA, removing DNA templates and enzymes in a single downstream step. CDMOs such as Biomay AG have expanded GMP footprint capacity across 2024–2025, signaling continued demand for end-to-end RNA manufacturing services.

Likewise, plasmid DNA is scaling from research volumes into commercial drug-substance capacity. In June 2024, bioprocessing suppliers committed US$100 million to dedicated pDNA synthesis infrastructure. Suppliers that can deliver lot-to-lot resin consistency, validated extractables & leachables compliance, and GMP documentation will secure multi-year supply agreements with RNA program sponsors.

Specialty Resins for GLP-1 Peptide Drugs and RNA Oligonucleotide Therapeutics

The chromatography resin market is being reshaped by new demand pockets — particularly anti-obesity GLP-1 peptide drugs and RNA-based oligonucleotide therapeutics, including antisense oligonucleotides (ASOs) and siRNA.

At the GLP-1 & Oral Peptides Conference (April 2025), innovators showcased Fast-Flow Solid Phase Peptide Synthesis (FF-SPPS) platforms, which rely on high-temperature, solvent-resistant synthetic resins capable of scaling production from 0.05 mmol to 15 mmol while maintaining stable crude purity. This scale-throughput capability is accelerating resin adoption by peptide API manufacturers. In May 2025, DuPont expanded its bioprocessing portfolio with AmberChrom TQ1, an agarose-based AEX resin developed specifically for oligonucleotide purification. Featuring improved loading capacity and reduced pressure-build-up, these formats support industrial-scale ASO and siRNA production.

Chromatography Resin Market Share and Segmentation Insights

Resin Type Performance: Synthetic Polymer Resins Lead Industrial Adoption While Natural Media Sustain Biopharma Precision

Synthetic polymer chromatography resins command 48% market share in 2025, driven by their superior mechanical strength, chemical resistance, and ability to withstand high flow rates and aggressive clean-in-place (CIP) protocols in large-scale bioprocessing. Polystyrene and acrylic-based resins are widely deployed across capture and polishing steps for monoclonal antibodies and recombinant proteins, making them indispensable in modern downstream processing. Natural polymer resins such as agarose and dextran maintain steady demand, particularly in biopharmaceutical purification, where high biocompatibility and large pore sizes enable efficient separation of complex biomolecules like mAbs. Inorganic media, including silica and hydroxyapatite, represent the smallest segment but play a critical role in high-resolution analytical chromatography and specialized purification workflows. Their unique surface chemistry supports niche applications such as plasmid DNA and antibody fractionation, reinforcing their strategic importance despite lower overall volume.

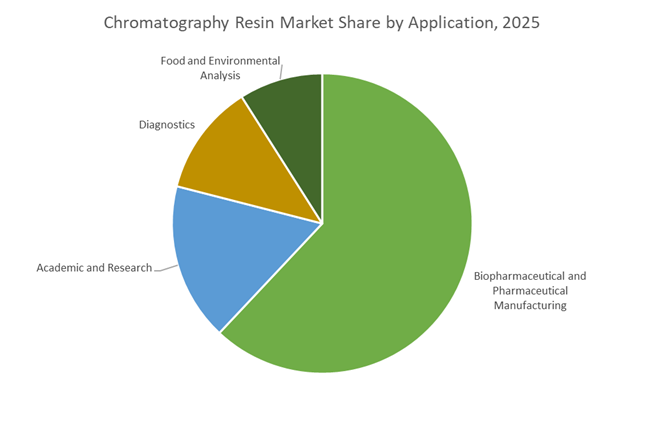

Application Landscape: Biopharmaceutical Manufacturing Drives Resin Demand Across Global Supply Chains

Biopharmaceutical and pharmaceutical manufacturing dominates chromatography resin consumption with 62% market share, fueled by surging production of monoclonal antibodies, insulin, vaccines, and advanced biologics. Each therapeutic batch requires multiple chromatography stages, including capture and polishing, significantly increasing resin replacement cycles and lifecycle demand. Academic and research institutions form the second-largest segment, supported by expanding proteomics, genomics, and translational life science programs, although usage typically centers on smaller columns and prepacked formats. Diagnostics represents a growing application area, where chromatography resins enable critical quality control and reagent purification in diagnostic kit production. Food and environmental analysis accounts for the smallest share but remains structurally stable, driven by regulatory requirements for detecting pesticides, mycotoxins, and contaminants in complex matrices. Together, these applications sustain long-term growth across analytical, preparative, and industrial-scale chromatography resin markets.

Competitive Landscape of the Chromatography Resin Market

The Chromatography Resin Market is led by bioprocessing specialists and life science majors accelerating resin capacity, continuous downstream processing, and high-binding affinity technologies. Competitive differentiation centers on Protein A resins, intensified chromatography, multi-column workflows, and AI-driven purification optimization for monoclonal antibodies, gene therapies, vaccines, and biosimilars. Market leaders are expanding manufacturing footprints, launching next-generation high-capacity resins, and integrating single-use systems to support continuous biomanufacturing. Strategic priorities increasingly include security of supply, pre-packed columns, sustainable regeneration protocols, and scalable solutions for emerging modalities such as mRNA, viral vectors, and plasmid DNA.

Cytiva drives intensified chromatography with high-capacity MabSelect PrismA resins

Formerly GE Healthcare Life Sciences, Cytiva dominates large-scale bioprocess resin manufacturing, anchored by its MabSelect™ and Capto™ platforms for monoclonal antibody and therapeutic protein purification. In 2025, Cytiva scaled MabSelect PrismA, delivering binding capacities up to 80 g/L with enhanced alkaline stability, enabling aggressive cleaning cycles without performance loss. The company is advancing intensified chromatography by integrating resins with ÄKTA™ ready single-use systems to support continuous manufacturing. To meet surging biosimilar demand, Cytiva expanded its Uppsala, Sweden facility, boosting resin production capacity by 40%, reinforcing its leadership in industrial-scale downstream processing.

Merck strengthens Protein A leadership through Eshmuno innovation and JSR acquisition

Operating as MilliporeSigma in North America, Merck leads advanced filtration and multimodal chromatography resins with its Eshmuno® and Fractogel® product lines for high-throughput ion exchange and polishing steps. In late 2025, Merck announced a definitive agreement to acquire JSR Life Sciences’ chromatography business (Amsphere™), expected to close in Q2 2026, significantly expanding its Protein A market share. Recent innovation includes Eshmuno® CP-FT, a first-of-its-kind cation exchange resin designed for flow-through aggregate removal in mAb processing. Merck’s Template approach delivers pre-validated resin and buffer sets for mRNA and viral vector workflows.

Thermo Fisher advances gene therapy purification with AI-guided resin selection

Thermo Fisher Scientific leverages deep R&D to supply specialized chromatography resins for complex modalities such as gene and cell therapies. Its POROS™ high-flow beads and CaptureSelect™ nanobody-based affinity ligands enable precise purification of AAV vectors, bispecific antibodies, and hormones where traditional Protein A underperforms. In 2025, Thermo integrated AI-driven resin screening, allowing customers to identify optimal resin-ligand combinations for hard-to-purify proteins in under 48 hours. Strategically, Thermo is expanding its Lab-in-the-Loop initiative with NVIDIA, automating chromatography method development using real-time sensor data to accelerate downstream process optimization.

Tosoh boosts continuous bioprocessing with GigaCap resins and MCC workflows

Tosoh Bioscience is the global leader in polymer-based chromatography resins, valued for mechanical rigidity and lot-to-lot consistency across TOYOPEARL® and TSKgel® platforms. In 2026, Tosoh opened a Customer Applications Center in Hyderabad, India, targeting the region’s fast-growing vaccine and biosimilar manufacturing sector. Recent innovation includes TOYOPEARL GigaCap® S-650M, a cation exchange resin delivering dynamic binding capacities above 90 g/L, reducing purification skid footprints. Tosoh is also spearheading Multi-Column Chromatography adoption, supplying resins engineered for high-velocity cycles in continuous downstream processing environments.

Repligen accelerates bioprocess intensification with pre-packed columns and HiPer beads

Repligen has evolved from a ligand supplier into a leader in pre-packed chromatography and intensified bioprocessing. Its OPUS® pre-packed columns and NGL-Impact® Protein A ligands, co-developed with Purolite, allow manufacturers to bypass manual column packing and move directly to purification. Recent acquisitions of Metenova and Astrea Bioseparations expanded Repligen’s portfolio into mixing systems and nanofiber chromatography. In 2026, Repligen launched HiPer™ macroporous bead technology, improving mass transfer for large biomolecules such as plasmids and genomic DNA, strengthening its position in next-generation biologics manufacturing.

Purolite expands sustainable Protein A production with ultra-durable Praesto resins

Following its acquisition by Ecolab, Purolite rapidly scaled its bioprocessing footprint with Praesto® agarose-based Protein A resins used in blockbuster monoclonal antibody production. In 2024 to 2025, Purolite introduced DurA Cycle, engineered for ultra-large-scale purification while maintaining performance beyond 200 caustic cleaning cycles. Leveraging Ecolab’s global supply chain, Purolite now offers security-of-supply guarantees, a critical differentiator amid recent raw material shortages. Its Sustainability-as-a-Service model helps biomanufacturers cut water and chemical usage by up to 20% through optimized resin regeneration protocols.

United States Chromatography Resin Market: Biologics Scale-Up, Protein A Affinity Media Expansion, and Continuous Downstream Processing

The United States Chromatography Resin Market represents the largest global concentration of R&D and production capacity for high-performance bioprocess chromatography media, driven by a mature biopharmaceutical ecosystem and aggressive investment in monoclonal antibody and cell and gene therapy manufacturing. In June 2025, Cytiva finalized a $1.6 billion multi-year capacity expansion program initiated in 2019, significantly increasing production of Protein A affinity resins and high-capacity agarose-based chromatography media at its Michigan and other global facilities. This scale-up directly supports rising demand for large-volume biologics manufacturing and advanced downstream purification workflows.

In May 2025, DuPont launched AmberChrom TQ1 resin engineered for high-purity purification of oligonucleotides and peptides, addressing growth in nucleic acid therapeutics and novel drug modalities. The U.S. market is also witnessing horizontal integration across Protein A resin supply chains to mitigate supply volatility for mAb purification. A technological shift toward continuous chromatography systems is accelerating adoption of pressure-stable, long-life resins capable of sustaining high-throughput operations while optimizing cost of goods sold. Plug-and-play biomanufacturing facilities increasingly utilize standardized pre-packed chromatography columns to reduce changeover times and minimize cross-contamination. Affinity resins tailored for viral vector purification in cell and gene therapy represent one of the fastest-growing application segments, reinforcing the United States as the epicenter of global chromatography resin innovation.

Germany Chromatography Resin Market: Multimodal Resin Innovation, GMP Alignment, and Bioprocessing Integration

Germany anchors the European Chromatography Resin Market through technological leadership in multimodal chromatography resins, mixed-mode media, and integrated downstream bioprocessing solutions. In October 2025, Merck KGaA announced the acquisition of the chromatography business of JSR Life Sciences, integrating Amsphere A3 and A+ Protein A resins into its purification portfolio. This strategic consolidation strengthens Germany’s position in next-generation monoclonal antibody purification and large-scale downstream processing.

German manufacturers maintain strict compliance with EU Good Manufacturing Practice directives, particularly in leachables and extractables testing for chromatography resins used in pharmaceutical production. Initiatives led by CLIB - Cluster Industrial Biotechnology focus on developing bio-based and biodegradable resin matrices and buffers to reduce the environmental footprint of large purification campaigns. German CDMOs are deploying high-throughput screening platforms using 96-well filter plates packed with chromatography resins to accelerate process development timelines. Expansion of advanced chemical parks is fostering plug-and-play infrastructure for resin developers, enhancing collaboration between media suppliers and biotech manufacturers across Europe.

China Chromatography Resin Market: High-End Synthetic and Affinity Resin Scaling Under National Industrial Policy

China’s Chromatography Resin Market is rapidly transitioning from commodity media production to high-value synthetic and affinity resin development, aligned with national industrial self-sufficiency objectives. Dedicated chemical parks supported by 2026 national industrial strategies are providing shared utilities and infrastructure to resin manufacturers, reducing reliance on imported Protein A and specialty chromatography media.

Industrial hubs in Nantong and Huizhou have established dedicated lines for LC-MS grade and bioprocess-grade resins tailored to the expanding domestic biosimilar and innovative biologics market. Chinese firms are scaling production of agarose-based chromatography beads to deliver cost-efficient antibody purification solutions. Advanced AI-driven quality control platforms integrated with chromatography systems enable real-time monitoring of resin degradation and impurity profiles, strengthening manufacturing consistency. The National Medical Products Administration has tightened batch-to-batch consistency requirements, compelling domestic resin producers to upgrade polymerization, functionalization, and purification processes. These reforms position China as a fast-growing supplier of specialty chromatography resins with improving global competitiveness.

India Chromatography Resin Market: Bulk Drug Parks, Biosimilar Expansion, and Cost-Competitive Affinity Media

India’s Chromatography Resin Market is expanding in parallel with its transformation into a high-value generic and biosimilar manufacturing hub. Government-backed Bulk Drug Parks are catalyzing downstream processing investments, increasing domestic demand for ion-exchange resins, affinity chromatography media, and high-capacity purification platforms. Significant foreign direct investment in India’s biopharma sector is facilitating adoption of premium downstream purification technologies, including standardized imported pre-packed chromatography columns.

Regulatory reforms in 2025 that revoked certain redundant Quality Control Orders for industrial chemicals have streamlined the scaling of domestic resin-related manufacturing operations. Growth in complex generic biologics production is generating demand for reliable and cost-efficient chromatography resins capable of competing with established Western brands. Collaboration between Indian laboratories and global technology providers such as Agilent Technologies is strengthening local technical support infrastructure, including refurbishment centers and analytical system optimization services. This ecosystem is positioning India as an emerging supplier of competitively priced yet quality-compliant chromatography resins for global biosimilar supply chains.

Japan Chromatography Resin Market: Precision UHPLC Media, Chiral Stationary Phase Leadership, and Green Manufacturing

Japan maintains global leadership in precision chromatography media and high-resolution analytical resins, particularly in chiral stationary phases and ultra-high-performance liquid chromatography compatible materials. Shimadzu Corporation and other domestic innovators continue advancing UHPLC-compatible resin technologies utilized in stringent quality control of complex therapeutics.

Japanese manufacturers are developing resins optimized for purification of large-scale peptide therapeutics and nucleic acid medicines, leveraging proprietary bead fabrication technologies that ensure uniform particle size distribution and superior binding capacity. Integration of Digital Twin laboratory management systems enables simulation of purification runs, optimizing resin life cycle and buffer utilization before physical implementation. Under Japan’s Green Transformation strategy, companies are investing in long-life, regenerable chromatography resins that reduce replacement frequency and overall carbon footprint. Strategic partnerships with biotech hubs across Asia-Pacific and North America ensure that Japanese high-precision chromatography media remain the benchmark for demanding pharmaceutical purification and analytical applications, reinforcing Japan’s dominant position in the global chromatography resin market.

Chromatography Resin Market Report Scope

Chromatography Resin Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$7 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Resin Type (Natural Polymers, Synthetic Polymers, Inorganic Media), By Technology (Affinity Chromatography, Ion Exchange Chromatography, Hydrophobic Interaction Chromatography, Size Exclusion Chromatography, Mixed-Mode Chromatography), By Application (Biopharmaceutical and Pharmaceutical Manufacturing, Academic and Research, Diagnostics, Food and Environmental Analysis), By Scale of Operation (Analytical Scale, Preparative Scale, Process Scale)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cytiva, Merck KGaA, Bio-Rad Laboratories, Inc., Thermo Fisher Scientific Inc., Tosoh Corporation, Ecolab Inc., Sartorius AG, Repligen Corporation, Pall Corporation, JSR Corporation, Mitsubishi Chemical Corporation, Agilent Technologies, Inc., Waters Corporation, Asahi Kasei Corporation, Kaneka Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chromatography Resin Market Segmentation

By Resin Type

- Natural Polymers

- Agarose

- Cellulose

- Dextran

- Synthetic Polymers

- Polystyrene

- Styrene-Divinylbenzene

- Polymethacrylate

- Polyacrylamide

- Inorganic Media

- Silica Gel

- Alumina

- Hydroxyapatite

By Technology

- Affinity Chromatography

- Ion Exchange Chromatography

- Hydrophobic Interaction Chromatography

- Size Exclusion Chromatography

- Mixed-Mode Chromatography

By Application

- Biopharmaceutical and Pharmaceutical Manufacturing

- Academic and Research

- Diagnostics

- Food and Environmental Analysis

By Scale of Operation

- Analytical Scale

- Preparative Scale

- Process Scale

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Chromatography Resin Industry

- Cytiva

- Merck KGaA

- Bio-Rad Laboratories, Inc.

- Thermo Fisher Scientific Inc.

- Tosoh Corporation

- Ecolab Inc.

- Sartorius AG

- Repligen Corporation

- Pall Corporation

- JSR Corporation

- Mitsubishi Chemical Corporation

- Agilent Technologies, Inc.

- Waters Corporation

- Asahi Kasei Corporation

- Kaneka Corporation

*- List not Exhaustive