Crocetin Esters Market Expansion to $0.7 Million by 2034 at 5.5% CAGR Driven by Clinical Validation, AI-Verified Saffron Supply, and Advanced Delivery Technologies

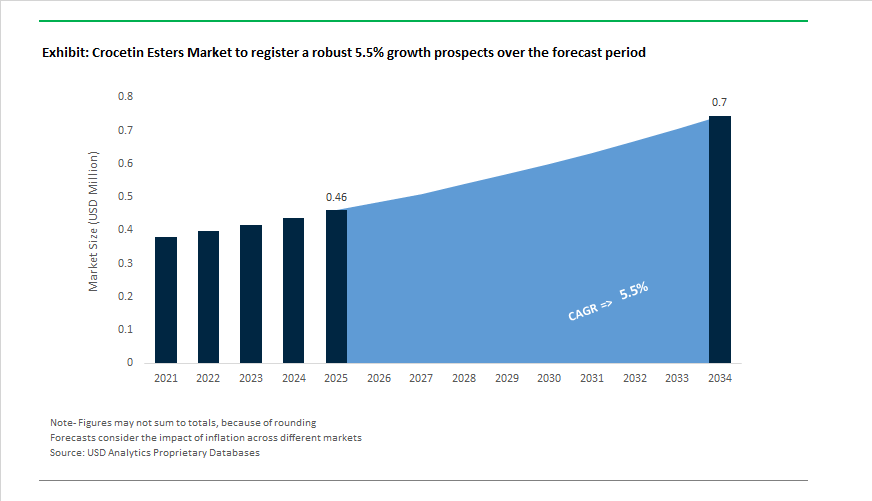

The Crocetin Esters Market is projected to grow from $0.46 Million in 2025 to $0.7 Million by 2034, reflecting a CAGR of 5.5%. Crocetin esters, primarily derived from saffron stigmas, are increasingly positioned as high-value bioactive carotenoids across nutraceuticals, pharmaceuticals, functional foods, eye-health supplements, and premium wellness beverages. Market expansion is supported by clinical validation in sleep and myopia control applications, the integration of AI-driven quality assurance systems, adoption of microencapsulation technologies for stability enhancement, and scaling of controlled-environment saffron cultivation to ensure pharmaceutical-grade consistency.

Innovation momentum accelerated through 2024 and early 2025. In 2024, Kemin Industries launched Organic KEM GLO, a USDA-certified carotenoid pigment platform supporting clean-label animal nutrition, indirectly strengthening demand for natural pigment sources including saffron-derived carotenoids. Between 2024 and 2025, Givaudan extended its collaboration with Novozymes to expand sustainable botanical ingredients within its Taste & Wellbeing portfolio, aligning crocetin-derived colorants with clean-label food and beverage formulations. In March 2025, Saffron Tech initiated pilot operations at its fully automated vertical farming facility, deploying robotics and climate-controlled systems to optimize crocetin, safranal, and picrocrocin concentrations for Active Pharmaceutical Ingredient applications. In April 2025, Tata Consumer Products introduced premium Kashmiri saffron with AI-enabled verification of crocetin ester and picrocrocin levels, addressing adulteration risks and reinforcing traceability standards in the high-end consumer segment. The same month, LNS AgriTech began large-scale aeroponic saffron cultivation in India, stabilizing year-round yields and mitigating climate-driven volatility in traditional soil-based production.

Clinical validation and consumer-facing product launches intensified market visibility during mid to late 2025. In May 2025, Starbucks India introduced saffron-infused beverages, signaling the migration of crocetin esters from therapeutic positioning into functional indulgence within premium food service. Updated multicenter clinical data released in mid-2025 in Japan and China reinforced the efficacy of dietary crocetin in suppressing myopia progression in children, catalyzing eye-health supplement launches across East Asia. In August 2025, Mibelle Biochemistry received the BeautyMatter Breakthrough Technology Award for its PhytoCellTec™ Exosomes platform, highlighting synergistic use of plant-derived carotenoids such as crocetin in dermal regeneration and collagen support. In October 2025, Activ’Inside expanded its patented Safr’Inside™ extract into the sleep sector following two 2025 clinical studies demonstrating improved sleep quality via modulation of the gut–sleep–brain axis at a 20 mg dose, earning finalist recognition at the NutraIngredients Awards. In the same month, Pharmactive Biotech showcased enhanced clinical data for affron® at SupplySide Global 2025, emphasizing bioavailability advantages of crocetin esters for retinal health and digital eye strain mitigation.

Technological enhancement entered a new phase in January 2026 as global ingredient manufacturers reported expanded adoption of microencapsulation and nano-delivery systems to protect crocetin esters against heat, light, and oxidative degradation. These systems enable stable incorporation into gummy supplements and Ready-to-Drink formulations where traditional saffron extracts often exhibit volatility and flavor interference. The Crocetin Esters Market is increasingly characterized by pharmaceutical-grade quality control, AI-verified sourcing, vertical farming scalability, clinically substantiated health positioning, and advanced stabilization technologies tailored for next-generation nutraceutical and functional beverage applications.

Trends and Opportunities in the Global Crocetin Esters Market

Structural Shift from Saffron to Gardenia jasminoides as a Scalable Source

- The long-standing reliance on saffron stigmas as the primary source of crocetin esters is rapidly declining due to cost instability and supply constraints. Saffron prices frequently exceed USD 5,000 per kilogram, creating margin pressure and limiting its suitability for mass-market applications. As a result, manufacturers are pivoting toward Gardenia jasminoides, which offers a more predictable, high-yield, and agriculturally scalable alternative. Industrial extraction assessments published in December 2025 indicate that gardenia fruit pulp delivers crocin concentrations of approximately 12.76 milligrams per gram, with select high-yield cultivars reaching up to 36.97 milligrams per gram. This yield advantage materially improves unit economics and supports consistent large-batch production, particularly across Asia Pacific functional food manufacturing hubs.

- Process innovation is reinforcing this transition. In August 2025, advances in reversed-phase medium-pressure liquid chromatography enabled producers to achieve crocin-1 purity levels of 60.8% from gardenia extracts. This level of standardization significantly improves dosing accuracy and batch-to-batch consistency compared with saffron-derived material, where variability in stigma quality remains a persistent challenge. As regulatory scrutiny around label claims and active content intensifies, gardenia-based crocetin esters are increasingly preferred by nutraceutical and pharmaceutical formulators.

Enhanced Bioavailability Through Advanced Phytosome and Lipid-Based Delivery Systems

- Poor aqueous solubility has historically limited the bioefficacy of crocetin esters in oral formulations. To overcome this constraint, the market is rapidly adopting phospholipid-based and nanoscale delivery technologies that enhance intestinal absorption and stability. Technical reports released in September 2025 confirm that phytosome formulations, which complex plant actives with phospholipids, significantly improve the release and solubility profile of hydrophobic compounds. In comparable botanical applications, phytosome systems have demonstrated release rates up to three times higher than conventional powder or oil-based formats, supporting higher bioavailability at lower dosages.

- Parallel innovation is occurring at the nanoscale. Research initiatives disclosed in January 2025 highlighted the development of crocin selenium nanoparticles, known as Cor@SeNs. These structures protect crocetin esters from gastrointestinal degradation while enabling controlled release. Clinical evaluations linked these formulations to measurable improvements in cognitive performance, including verbal learning and delayed recall, in populations exhibiting oxidative stress biomarkers. Collectively, these delivery technologies are shifting crocetin esters from commodity antioxidant status toward clinically differentiated bioactives.

Clinical Expansion into CNS and Ocular Therapeutics

- Crocetin esters are increasingly transitioning from general wellness ingredients to adjunct therapeutic agents in neurology and ophthalmology. In July 2025, clinical updates on age-related macular degeneration reported that daily oral supplementation of 15 milligrams of crocetin esters led to significant improvements in best-corrected visual acuity and reductions in central macular thickness among patients with refractory diabetic macular edema. These outcomes position crocetin esters as a non-invasive alternative to intravitreal injections, addressing a major patient compliance barrier in ophthalmic care.

- Neuroinflammatory disorders represent another high-impact opportunity. A 2025 review of multiple sclerosis research demonstrated that crocetin suppresses microglial activation, a key driver of neurodegeneration. Clinical trials using daily doses of 30 milligrams showed significant reductions in high-sensitivity C-reactive protein levels, signaling lower systemic inflammation. These findings also correlated with improvements in anxiety-related symptoms, expanding the therapeutic relevance of crocetin esters beyond purely neurological endpoints.

Mainstream Integration into Functional Foods and Sports Nutrition

- The functional food and sports nutrition segments offer a scalable commercialization pathway for crocetin esters, particularly within the active lifestyle consumer cohort. Consumer analytics published in December 2025 indicate that more than 50% of functional food buyers prioritize products delivering mental acuity and sustained energy. This demand is driving innovation in fortified chocolates, nutrition bars, and cognitive support snacks that leverage crocetin’s anti-inflammatory and neuroprotective properties without introducing bitterness or off-notes.

- To enable broader beverage and ready-to-drink applications, manufacturers are investing in bitterness masking and encapsulation technologies. Vacuum impregnation and advanced microencapsulation methods now allow crocetin esters to be incorporated into clear functional beverages, targeting a global functional drink market valued at approximately USD 314 billion. By pairing encapsulated crocetin with citrus and berry flavor systems, brands are meeting clean-label expectations among Gen Z and Millennial consumers while unlocking high-volume distribution channels previously inaccessible to botanical antioxidants.

Crocetin Esters Market Share and Segmentation Insights

Product Type Distribution: Crocin Leads Commercial Adoption While Trans-Isomers Anchor Pharma Research

Crocin accounts for 52% of crocetin ester demand in 2025, driven by its superior water solubility, high bioavailability, and commercial scalability from saffron and gardenia sources. Its compatibility with liquid formulations makes crocin the preferred ingredient for functional beverages and dietary supplements targeting cognitive health, mood balance, and eye wellness. Trans-crocetin esters represent a significant secondary segment, reflecting their status as the dominant natural isomer in saffron stigmas and their strong antioxidant profile, which supports use in pharmaceutical R&D and premium nutraceutical products emphasizing natural sourcing. Cis-crocetin esters remain a smaller but high-value category, gaining attention for distinct bioactivities including potential neuroprotective effects, though isolation complexity and stability challenges constrain volume growth. Isomer balance is increasingly critical, as light-induced trans-to-cis conversion impacts color stability and biological performance, prompting manufacturers to invest in controlled processing and packaging technologies.

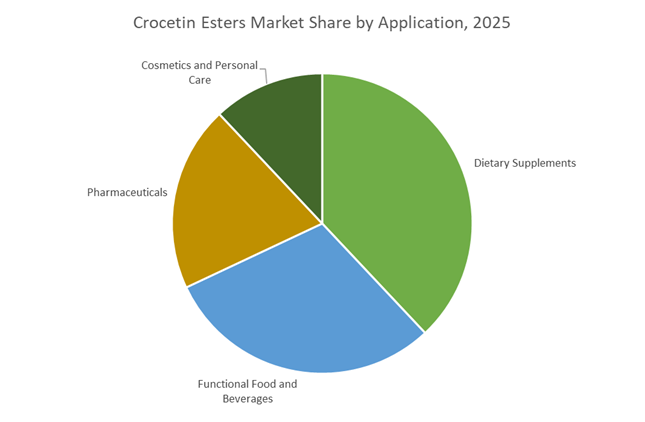

Application Landscape: Dietary Supplements Dominate as Functional Beverages Accelerate Growth

Dietary supplements capture 38% of crocetin ester consumption, supported by rising consumer preference for plant-derived antioxidants positioned for memory support, sleep quality, and visual health. Capsules and tablets containing crocin and trans-crocetin esters dominate this segment due to standardized dosing and shelf stability. Functional food and beverages represent the fastest-growing application, leveraging crocin’s water solubility and natural golden hue in wellness shots, functional waters, and energy drinks marketed for stress reduction and mental clarity. Pharmaceuticals form a smaller but strategic segment focused on clinical development for age-related macular degeneration, Alzheimer’s disease, and sleep disorders, demanding ultra-high purity grades and validation. Cosmetics and personal care round out demand, integrating crocetin esters into anti-aging serums and brightening formulations aligned with clean beauty trends, although premium ingredient costs continue to limit mass-market penetration.

Competitive Landscape of the Crocetin Esters Market

The Crocetin Esters Market is shaped by vertically integrated saffron sourcing, pharma-grade botanical extraction, and rising demand for clinically validated carotenoids across nutraceutical, cosmetic, and functional beverage applications.

Sabinsa drives bio-standardized crocetin esters through farm-to-formula integration

Sabinsa Corporation (Sami-Sabinsa Group) leads the market with its integrated cultivation-to-formulation model, supplying standardized saffron extracts rich in crocetin esters and picrocrocin, including Saffr’Activ®. In late 2025, the company expanded cultivation partnerships across the Middle East to secure sustainable, non-GMO raw material supplies. Sabinsa’s core strength lies in its extensive IP portfolio, holding multiple patents covering carotenoids for metabolic health and cognitive support. Strategically, the company is advancing “Bio-Standardization,” applying HPLC fingerprinting to every batch to meet 2026 transparency requirements in nutraceuticals. This quality-first approach positions Sabinsa as a preferred supplier for premium crocetin ester formulations.

Givaudan (Naturex) integrates crocetin esters into global food, beauty, and wellness systems

Following its acquisition of Naturex, Givaudan has become a dominant botanical actives supplier, embedding crocetin esters into large-scale F&B and personal care platforms. In 2025, the company partnered with Novozymes to develop enzymatic crocin extraction from saffron waste and gardenia fruits, improving yield efficiency. Early 2026 saw the launch of its Frontier Health hub, focused on functional beverages and mood-support teas. Givaudan also leads cosmetic applications, leveraging crocetin esters’ antioxidant activity in anti-pollution and UV-defense skincare. Its key differentiator is full-stack integration, delivering natural color, flavor, and bioactive crocetin esters within a single ingredient solution.

Pharmactive builds clinical credibility around high-potency saffron extracts

Spain-based Pharmactive Biotech Products specializes in high-strength saffron extracts, anchored by its Affron® platform standardized to Lepticrosalides®, containing elevated crocetin ester levels. In April 2025, Pharmactive secured a new patent positioning Affron® dosages as a natural mood-support therapeutic, bridging nutraceutical and pharmaceutical markets. Crocetin-rich ingredients contributed significantly to its double-digit North American revenue growth in 2025. The company’s strategy centers on clinical validation, with three major 2026 trials underway evaluating neuroprotective benefits in adolescent mental health. Pharmactive’s science-backed positioning and regional saffron expertise make it a leading player in evidence-driven crocetin ester applications.

Indena advances pharma-grade crocetin esters with enhanced bioavailability

Indena operates at the pharmaceutical end of the crocetin esters spectrum, focusing on ≥98% purity compounds for clinical research and APIs. In early 2026, it strengthened R&D dedicated to high-purity crocetin ester manufacturing, reinforcing its role in cardiovascular and oncology research supply chains. A key 2025 innovation was its Phytosome® delivery system, significantly improving crocetin bioavailability and overcoming traditional absorption challenges. Indena’s core strength lies in advanced isolation technologies and pharma-botanical expertise, positioning crocetin esters as science-backed alternatives to synthetic antidepressants. This precision-driven model supports Indena’s leadership in therapeutic-grade botanical ingredients.

Chengdu Biopurify scales reference-grade crocetin esters for APAC research markets

Chengdu Biopurify Phytochemicals dominates the Asia-Pacific research segment through high-volume production of pure crocetin ester isomers, including trans-crocin and cis-crocin. In February 2026, the company completed a new large-scale isolation facility in Chengdu to support 10% annual growth in botanical intermediates demand. Biopurify offers Contract Research and Manufacturing Services (CRAMS), enabling global brands to outsource customized crocetin profiles. Its primary strength is production efficiency at laboratory and pilot scale, making it the leading supplier of crocetin ester reference standards for early-stage drug discovery and formulation development.

China: Industrial-Scale Biomanufacturing and Export-Oriented Purity Standards

China has emerged as the structural backbone of global crocetin ester supply, primarily through the scalable use of Gardenia jasminoides as an alternative feedstock to saffron. By late 2025, this model had enabled China to deliver cost-efficient, high-volume crocetin esters without the labor intensity and yield volatility associated with saffron stigma harvesting. The shift has materially altered global pricing benchmarks while ensuring consistent supply for food colorants, nutraceuticals, and pharmaceutical intermediates. Under the 2025 Industrial Digitalization Roadmap, the Ministry of Industry and Information Technology funded five advanced facilities across Anhui and Zhejiang to deploy AI-driven enzymatic extraction platforms. These upgrades reduced solvent waste by an estimated 18 %, strengthening China’s positioning in low-residue, sustainability-aligned carotenoid production.

Export sophistication is accelerating alongside volume leadership. In January 2026, Chinese authorities introduced updated export quality protocols for so-called electronic-grade crocetin esters, targeting applications in optical filters and high-stability precision colorants used in advanced instrumentation. This marks a strategic move beyond food and supplement markets into specialty industrial domains. Supporting this transition, the Shanghai Chemical Industry Park announced a $45 million expansion in 2025 to establish a dedicated bio-based colorant cluster focused on water-soluble crocetin glycosides. Collectively, these developments position China not only as a low-cost producer but as a technology-driven exporter capable of serving pharmaceutical, nutraceutical, and electronics-grade specifications.

Spain: Pharmaceutical Traceability and Patented Saffron Extract Leadership

Spain’s crocetin ester industry is defined by traceability, intellectual property, and premium saffron positioning rather than scale. In 2025, the Spanish Ministry of Agriculture, Fisheries and Food mandated blockchain-based traceability for Grade I saffron threads, ensuring documented crocetin ester consistency across the supply chain. This initiative is particularly relevant for European pharmaceutical exporters, where batch-level validation and origin transparency are becoming prerequisites for market access.

Spain’s innovation advantage is reinforced through proprietary formulations. Pharmactive Biotech Products expanded U.S. and EU patent filings in mid-2025 for its Affron® saffron extract, with claims centered on pediatric emotional support and sleep quality enhancement. These filings strengthen Spain’s role in clinically positioned crocetin ester applications rather than commodity trade. Sustainability alignment is also improving. Several Spanish production sites achieved ISCC PLUS certification in late 2025, validating the use of bio-circular raw materials and enhancing acceptance in regulated nutraceutical and pharmaceutical markets across Europe and North America.

Iran: Upgrading the World’s Primary Saffron Origin

Iran remains indispensable to the crocetin ester value chain as the origin of more than 90% of global saffron production. In 2025, producers in the Khorasan region began integrating modern vacuum-drying systems to address a long-standing challenge in traditional saffron processing, namely crocetin ester degradation during open-air drying. This technological upgrade has materially improved ester stability and extract quality, enabling Iranian producers to move up the value curve.

Trade dynamics are also evolving. Following new 2025 trade agreements, cooperatives such as Esfedan Saffron Co. transitioned from bulk stigma exports toward standardized crocetin ester extracts supplied directly to pharmaceutical customers in the Middle East and Asia. This shift reduces dependence on intermediary processors and allows Iranian suppliers to capture a greater share of value in high-margin medical and nutraceutical applications.

India: Origin Protection and Nutraceutical Manufacturing Incentives

India’s crocetin ester industry is anchored in origin-based differentiation and downstream formulation growth. In 2025, the Government of India reinforced enforcement of the Geographical Indication tag for Kashmiri saffron, strengthening price realization for crocetin esters derived from single-origin, hand-harvested crops. This move enhances India’s credibility in premium export channels where authenticity and provenance are critical purchasing criteria.

Policy support is extending into manufacturing. In 2026, the Department of Pharmaceuticals classified bioactive carotenoids as a priority segment under the Production Linked Incentive scheme. This designation is expected to accelerate localized production of crocetin-based dietary supplements, shifting India from a raw material supplier toward a formulation and branded product hub serving domestic and export nutraceutical markets.

United States: Clinical Validation and Functional Nutrition Pull

The United States crocetin ester market is increasingly driven by clinical research and functional health positioning. In late 2025, the U.S. Food and Drug Administration granted Fast Track designation to Trans Sodium Crocetinate, a crocetin ester derivative, for use as a radiosensitizer in newly diagnosed glioblastoma. This regulatory milestone significantly elevates the medical credibility of crocetin esters and could catalyze broader pharmaceutical interest in carotenoid-based therapeutics.

Parallel demand is emerging from cognitive health research. A 2025 study published by Taylor & Francis linked crocetin to mitigation of Western diet-induced cognitive dysfunction, stimulating product development in brain health beverages and functional nutrition. This convergence of clinical oncology research and preventive wellness applications positions the U.S. as a high-value demand center rather than a volume producer.

Comparative Snapshot: Strategic Positioning of the Crocetin Esters Industry by Country

Crocetin Esters Market County Level Snapshot

|

Country / Region

|

Core Feedstock Strategy

|

Primary Demand Focus

|

Strategic Role in Global Value Chain

|

|

China

|

Gardenia-based scalable extraction

|

Food colorants, electronics-grade esters

|

Volume leader with rising purity standards

|

|

Spain

|

Traceable premium saffron

|

Pharmaceutical and patented nutraceuticals

|

IP-driven, high-margin supplier

|

|

Iran

|

Traditional saffron with modern processing

|

Pharma and medical extracts

|

Upstream origin upgrading

|

|

India

|

GI-protected saffron and PLI incentives

|

Nutraceutical formulations

|

Premium origin and formulation hub

|

|

United States

|

Imported actives with clinical validation

|

Oncology and brain health

|

Demand-side innovation leader

|

Crocetin Esters Market Report Scope

Crocetin Esters Market

|

Parameter

|

Crocetin Esters Market

|

|

Market Size (2025)

|

$0.46 Million

|

|

Market Size (2034)

|

$0.7 Million

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Trans-Crocetin Esters, Cis-Crocetin Esters, Crocin), By Source (Crocus Sativus, Gardenia Jasminoides, Secondary Botanical Sources), By Form (Powder, Liquid, Encapsulated), By Application (Pharmaceuticals, Functional Food and Beverages, Dietary Supplements, Cosmetics and Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Givaudan SA, Evonik Industries AG, Pharmactive Biotech Products S.L., Sami-Sabinsa Group Limited, Chengdu Biopurify Phytochemicals Ltd., Esfedan Saffron Co., Grupo Natac S.L.U., Hamiast Global Private Limited, Koppers Inc., Tokyo Chemical Industry Co., Ltd., Cayman Chemical Company, Plamed Green Science Group Co., Ltd., Swanson Health Products Inc., Gohar Saffron Company, Hunan Jiahang Pharmaceutical Technology Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Crocetin Esters Market Segmentation

By Product Type

- Trans-Crocetin Esters

- Cis-Crocetin Esters

- Crocin

By Source

- Crocus Sativus

- Gardenia Jasminoides

- Secondary Botanical Sources

By Form

- Powder

- Liquid

- Encapsulated

By Application

- Pharmaceuticals

- Functional Food and Beverages

- Dietary Supplements

- Cosmetics and Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Crocetin Esters Industry

- Givaudan SA

- Evonik Industries AG

- Pharmactive Biotech Products S.L.

- Sami-Sabinsa Group Limited

- Chengdu Biopurify Phytochemicals Ltd.

- Esfedan Saffron Co.

- Grupo Natac S.L.U.

- Hamiast Global Private Limited

- Koppers Inc.

- Tokyo Chemical Industry Co., Ltd.

- Cayman Chemical Company

- Plamed Green Science Group Co., Ltd.

- Swanson Health Products Inc.

- Gohar Saffron Company

- Hunan Jiahang Pharmaceutical Technology Co., Ltd.

*- List not Exhaustive