DLC Coatings Market Overview: Ultra-Low-Friction, High-Wear-Resistance Coatings Powering Next-Gen Automotive, Aerospace & Medical Systems

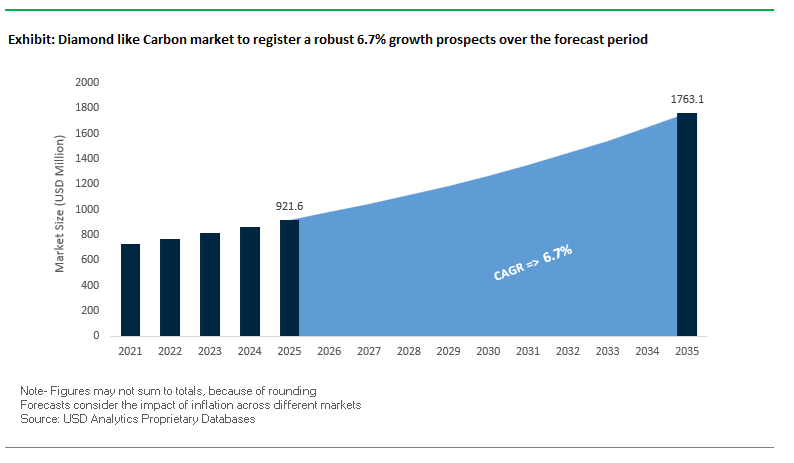

The Diamond-Like Carbon (DLC) Market, valued at USD 921.6 million in 2025 and projected to reach USD 1,762.7 million by 2035 at a strong 6.7% CAGR, is advancing rapidly as industries shift toward ultra-low-friction, high-hardness, and high-wear-resistance coatings to meet the escalating performance and reliability demands of modern engineering systems. As automotive OEMs intensify electrification and high-pressure fuel system innovation, aerospace suppliers seek lighter and more durable tribological interfaces, semiconductor firms pursue enhanced thermal and mechanical stability, and medical device manufacturers require biocompatible surfaces with extremely tight tolerances, DLC coatings—spanning a-C:H, metal-doped variants, and ultra-hard ta-C—have become essential material technologies.

DLC’s ability to reduce friction to the 0.05–0.15 range, withstand extreme cyclic loading, and maintain precision even at elevated temperatures makes it indispensable for piston pins, injector components, valve trains, bearings, wafers, implants, and ultra-precise surgical tools. As electrified powertrains, miniaturized semiconductor packaging, and advanced medical systems demand higher durability with lower environmental impact, DLC coatings deliver clear system-level advantages—improved efficiency, extended service life, reduced lubrication requirements, and lower maintenance costs.

For procurement teams and R&D leaders, the next decade requires a sharper focus on coating uniformity, hardness class, deposition method (PVD, PACVD, PECVD, HIPIMS+), adhesion performance, substrate engineering, and lifecycle reliability under high-load, high-frequency operation. With proven biocompatibility and expanding applicability across orthopedics and minimally invasive surgical systems, DLC is poised to become a foundational surface-engineering solution enabling high-performance, high-efficiency, and sustainability-aligned product architectures through 2035.

Market Analysis: Throughput Innovations, DLC Expansion in High-Stress Systems, and Strong Sector-Specific Adoption

The global DLC coating landscape is experiencing rapid scaling as manufacturers invest in equipment upgrades and high-volume production capacity. In October 2025, Oerlikon Balzers launched the INGENIA coating system, engineered for faster throughput and compact operation, directly targeting mass production needs in automotive and industrial components. This launch reflects a wider market shift toward high-throughput PACVD/PVD platforms as OEMs increasingly depend on DLC-coated components for friction loss reduction and enhanced engine efficiency. In parallel, the automotive sector reaffirmed its reliance on DLC technologies when, in February 2025, a major European OEM announced that its next-generation hybrid engine successfully passed 2000+ hours of accelerated wear testing using a-C:H:W DLC coatings on high-pressure fuel injector components-supporting the role of DLC as a critical enabler of durable, high-pressure, low-emission fuel systems.

Strategic investments continue to shape the market landscape. In July 2024, Morgan Advanced Materials announced global DLC production expansion to support aerospace and defense tribological applications, reflecting rising demand for coatings that combine hardness, low friction, and extreme-environment stability. By September 2025, the defense sector further underscored DLC’s strategic relevance when an Asian coating service provider secured a multi-year supply contract for DLC-coated optical sensor components in space and defense systems. Additionally, the medical device industry strengthened DLC adoption: in Q3 2025, a major orthopaedic implant manufacturer obtained regulatory approval for a DLC-coated knee component demonstrating 200% enhanced wear life, supporting growth in high-value medical DLC applications.

Innovation in deposition techniques remains a key market driver. In Q4 2024, IHI Hauzer unveiled a breakthrough dry DLC basecoat deposition process-significantly reducing reliance on traditional electrolytic plating. Similarly, BASF’s March 2024 collaboration with a semiconductor producer is advancing DLC for thermally demanding electronic packaging. Decorative and luxury industries are also showing rapid uptake, with a leading PECVD equipment provider reporting a 15% YoY demand increase in late 2024, driven by premium scratch-resistant finishes in watches and jewelry. These developments highlight DLC’s expansion across performance-critical, aesthetic, and sustainability-driven applications.

Key Trends: Multi-Layer DLC Engineering and Medical-Grade Surface Protection Expand High-Performance Applications

Trend 1: OEM Specification of Tiered, Multi-Layer DLC Systems to Reduce Friction Losses in ICE and Electrified Powertrains

A major structural shift in the DLC market is the formal specification of tiered, multilayer DLC architectures for high-wear powertrain components. Automotive OEMs now require coatings engineered with precise hardness, elasticity, and doping composition to meet aggressive warranty expectations and efficiency targets in both ICE and e-powertrain platforms.

Automotive leaders such as Nissan report that DLC-coated valve lifters and piston pins reduce overall engine friction by ~25%, with subsystem-level reductions as high as 40%—a major contributor to fuel-efficiency gains. The correlation is consistent: a 10% reduction in mechanical losses within an ICE corresponds to a 1.5% improvement in fuel consumption, explaining DLC’s rapid penetration into piston rings, bearings, tappets, and cam-following components.

In advanced applications, OEMs specify Si-doped or W-doped DLC layers, which optimize chemical compatibility with low-viscosity lubricants (0W-8, 0W-12) and modern friction modifiers such as MoDTC. Under boundary lubrication conditions, optimized DLC–lubricant systems achieve a super-low friction regime (μ < 0.01), unlocking efficiency gains essential for meeting global CO₂ reduction mandates.

Trend 2: Rapid Medical Device Industry Adoption of DLC for Corrosion-Free, Biocompatible Implant Surfaces

The medical device sector is increasingly adopting DLC coatings for orthopedic implants, prosthetic devices, cardiovascular components, and surgical tools, driven by the demand for corrosion resistance, low wear debris, and biocompatibility.

DLC films applied to CoCrMo orthopedic alloys reduce corrosion rates by 4–5 orders of magnitude in simulated body fluid environments—preventing ion release and addressing a critical failure mode associated with inflammation and implant rejection.

Its bioinert, hemocompatible surface chemistry supports use in vascular stents, prosthetic valves, and joint prostheses. Studies show that DLC-coated articulating components sliding against UHMWPE generate dramatically reduced wear volumes, which directly mitigates periprosthetic osteolysis, extending implant service life.

The combination of low wear, inert chemistry, and resistance to bacterial colonization positions DLC as a strategic material for next-generation implantable biomaterials.

Opportunities: DLC as a Precision Surface for Semiconductor Cleanrooms and a Barrier Layer for Fuel Cells and Advanced Batteries

Opportunity 1: Anti-Galling, Non-Contaminating DLC Coatings for Semiconductor Manufacturing and Cleanroom Tooling

The semiconductor industry presents one of the highest-value opportunities for DLC adoption due to its stringent demands on cleanliness, precision, and surface reliability. DLC mitigates galling, abrasion, particle shedding, and cold welding on critical components such as wafer chucks, end effectors, bearings, and handling arms.

In leading-edge semiconductor fabs, micro-scratches or particle defects can cause catastrophic yield loss. DLC's ultra-smooth, chemically inert surface significantly reduces particle generation, enabling fabs to maintain sub-micron positioning accuracy and stable long-term operation.

The introduction of laser-based PVD deposition technologies now enables extremely low roughness DLC layers suitable for cleanroom applications, ensuring that the coating itself does not become a particle source—an essential qualification for EUV lithography and leading-edge logic and memory production.

Opportunity 2: DLC as a High-Stability Barrier Layer for Next-Generation PEM Fuel Cells and Lithium-Ion Batteries

As electrification accelerates, DLC exhibits high potential as a corrosion-resistant, low-resistance barrier layer in fuel cell and battery systems.

In PEM fuel cells, metallic bipolar plates face challenges from corrosion and oxide formation, which increase Interfacial Contact Resistance (ICR). Graphitic DLC coatings achieve corrosion current densities as low as 10⁻⁸ A/cm², meeting stringent U.S. DOE requirements. Their low electrical resistance enables ICR < 3 mΩ·cm², preserving stack efficiency and durability.

In the battery sector, DLC coatings on silicon anodes help suppress uncontrolled SEI growth, improving cycle life and capacity retention. Its conformal, chemically inert nature provides a stable interface that protects high-capacity electrode materials from electrolyte degradation and mechanical pulverization—two major limitations of silicon-dominant anode chemistries.

DLC also supports thin barrier protection for high-voltage cathode systems and next-generation solid-state batteries, positioning it as a functional enabler for advanced energy storage performance.

Diamond-Like Carbon Market Share Analysis

Market Share by DLC Type: Hydrogenated DLC (a-C:H) Leads with 49.2% Share

Hydrogenated DLC (a-C:H) commands the largest share of the Diamond-Like Carbon Market at 49.2% in 2025, reflecting its position as the most commercially scalable and broadly adopted DLC variant. Its dominance stems from an optimal balance of low friction, high wear resistance, strong adhesion, and relatively low deposition cost, making it the default coating for high-volume, price-sensitive applications across automotive, industrial, and consumer sectors. a-C:H’s compatibility with a wide range of substrates—including steels, aluminum alloys, polymers, and carbides—further strengthens its leadership, enabling manufacturers to enhance component durability without major redesigns or complex process adjustments. While hydrogenated DLC anchors market volume, the broader technology landscape shows a clear progression toward performance specialization: ta-C (hydrogen-free DLC) delivers superior hardness and thermal stability for extreme-duty environments but remains limited to applications that justify its higher cost; metal-doped DLC improves friction behavior and adhesion for challenging interfaces; and silicon-doped DLC enhances heat resistance for high-temperature automotive and industrial components. This segmentation highlights a market transitioning from generic DLC coatings to application-specific engineered DLC systems as tribological and thermal requirements intensify across industries.

Market Share By Type, 2025.png)

Market Share by Application: Automotive Components Lead with 42.1% Share

Automotive Components represent the largest application segment with a 42.1% share in 2025, underscoring the automotive industry’s critical role in driving global DLC adoption. This leadership is fueled by the sector’s relentless focus on reducing friction losses, improving fuel efficiency, extending component life, and meeting stringent emissions regulations, all of which position DLC coatings as a cost-effective surface engineering solution. DLC-coated parts—including tappets, piston pins, fuel injector components, pump plungers, gears, and bearings—benefit from reduced wear, enhanced lubrication behavior, and longer maintenance intervals, making DLC integral to modern ICE, hybrid, and increasingly EV powertrains. High-volume automotive manufacturing also allows per-part DLC coating costs to be reduced to mere cents, reinforcing its economic viability at global scale. Beyond automotive, industrial tooling represents the performance frontier, where DLC coatings deliver dramatic improvements in tool life and machining efficiency; medical devices rely on DLC for biocompatibility, corrosion resistance, and low wear in implantable components; and electronics, aerospace, and optics leverage DLC’s optical transparency, hardness, and barrier properties.

Germany & Europe: Euro 7-Driven DLC Adoption and E-Mobility Tribology Leadership

Europe—particularly Germany—continues to be a global epicenter for advanced DLC coatings, driven by engineering excellence, stringent emissions policy, and the surge in electric mobility solutions. The upcoming Euro 7 emissions standards (2025–2026) are accelerating demand for friction-reducing DLC-coated components such as tappets, piston pins, camshafts, gear systems, and injector parts. Since Euro 7 requires substantial cuts in particulate emissions and improved real-world driving performance, OEMs increasingly rely on ta-C DLC films to reduce boundary friction, lower wear, and extend component life.

Germany also leads in HiPIMS DLC deposition technology, with companies like CemeCon AG expanding high-performance coating solutions that offer superior adhesion and customizable stress profiles. These HiPIMS-based DLC films are being rapidly integrated into industrial tooling, machining components, and EV drivetrain systems, where torque fluctuations and micro-pitting risks are significantly higher in electric powertrains. European Tier 1 suppliers are already installing dedicated ta-C and metal-doped DLC lines for electric motor bearings, e-axle gears, high-speed shafts, and synchronized transmission systems. Meanwhile, Europe’s aerospace and defense contractors continue adopting hydrogen-free DLC coatings to meet the durability demands of actuators, landing gears, and moving parts in low-lubrication, high-temperature environments. This positions Europe as a global hub for multi-industry deployment of premium, sustainability-aligned DLC tribology solutions.

United States: Semiconductor-Grade DLC Expansion and Defense/Aerospace Coating Innovation

The United States remains a high-innovation market for DLC coatings due to its strategic focus on semiconductors, aerospace, and next-generation defense platforms. The CHIPS and Science Act, mobilizing more than $52 billion, indirectly boosts demand for semiconductor-grade DLC coatings by expanding domestic wafer fabs where DLC-coated wafer handling parts, electrostatic chucks, and precision mechanical interfaces are critical due to their chemical resistance, ultra-low friction, and vacuum stability.

In July 2024, Morgan Advanced Materials announced major investment into U.S.-based DLC production centers, specifically targeting aerospace and defense customers demanding lightweight, high-wear coatings for missiles, UAV components, optical sensors, and energy-conversion systems subjected to high thermal and mechanical loads. The U.S. also leads in fusion reactor material research, where national labs and private sector ventures are evaluating DLC plasma-facing coatings for tokamaks and stellarators because of their low sputtering rates and resilience under extreme plasma bombardment.

Additionally, U.S. biomedical engineering research is advancing biocompatible DLC coatings for orthopedic implants, joint replacements, and cardiovascular systems, reducing wear debris and improving tissue integration. This positions the United States as a cross-sector leader in high-performance, application-specific DLC film development for critical aerospace, semiconductor, medical, and defense technologies.

Japan: Precision Tribology and Next-Generation Electronic Component DLC Films

Japan continues to hold a commanding position in high-end DLC coatings for precision electronics, tribology R&D, and industrial cutting tools. The country’s expertise in miniaturized consumer electronics has fueled demand for ultra-thin DLC coatings (≤100 nm) used in delicate components like HDD read–write heads, miniature hinges, actuator arms, micro-optical sensors, and compact mechanical interfaces. These thin DLC films significantly improve durability and reduce stiction, supporting Japan’s broader drive toward ultra-compact, long-life electronic devices.

Strategic collaboration—such as BASF SE’s March 2024 partnership with a leading Japanese semiconductor manufacturer—is accelerating next-generation DLC material development for high-heat, high-frequency device environments. Meanwhile, Japan’s tooling manufacturers are global leaders in applying DLC coatings to drill bits, milling cutters, and inserts for dry, high-speed machining of aluminum alloys, titanium, and composite materials. These DLC-coated tools enable better chip evacuation, reduced cutting forces, and extended tool life, meeting the demands of Japanese aerospace, robotics, and automotive sectors. This positions Japan at the technological forefront of precision DLC engineering, tribology optimization, and advanced machining solutions.

China: High-Capacity DLC Production and Large-Scale EV Component Integration

China’s enormous manufacturing ecosystem—especially in automotive, EV powertrains, and industrial tooling—is driving the rapid expansion of DLC coating capacity. As China’s EV production continues to climb at world-leading rates, DLC-coated bearings, gears, shafts, synchronizers, and piston components are increasingly standard in domestic EV models to enhance drivetrain efficiency and ensure long-term wear stability under high torque conditions.

Provincial governments across China are actively supporting the establishment of large-scale PVD/PECVD DLC coating facilities, designed for high throughput and cost efficiency to align with China’s manufacturing scale. The focus is on coating technologies optimized for mass-market adoption, enabling millions of powertrain and mechanical components to receive protective DLC layers.

Chinese research institutions are also advancing metal-doped DLC (Me-DLC) and silicon-doped DLC (Si-DLC) variants that enhance adhesion on steel substrates, improve corrosion resistance, and increase thermal stability—key requirements for harsh industrial environments, hydrogen storage components, and high-speed machining applications. Collectively, this positions China as a fast-scaling, domestically self-reliant leader in cost-effective, high-volume DLC coating deployment across automotive and industrial sectors.

Competitive Landscape: Leading DLC Coating Specialists Driving Hardness, Friction Reduction, and Deposition Innovation

The DLC market is shaped by global coating leaders, equipment manufacturers, and surface engineering innovators that specialize in PVD, PACVD, PECVD, HIPIMS+, and ta-C deposition technologies. Competitive advantage increasingly depends on coating hardness customizability, substrate versatility, throughput scalability, and friction performance tailored to automotive, aerospace, medical, semiconductor, and luxury goods sectors.

Oerlikon Balzers - Advancing high-throughput DLC systems for automotive and industrial markets

Oerlikon Balzers is a global leader in PVD/PACVD DLC coating technologies, offering the BALINIT series known for high hardness, low friction, and exceptional wear resistance. Its INGENIA system, launched in October 2025, increases throughput and process flexibility, targeting mass production customers who require consistent, scalable DLC coatings. The company delivers DLC hardness values from 15 GPa to >80 GPa, with friction coefficients below 0.1, supporting high-performance automotive and motorsport components.

IHI Ionbond - Global DLC provider with deep aerospace and medical specialization

Ionbond, part of the IHI Group, operates more than 30 coating centers worldwide, offering engineered DLC solutions for aerospace, medical, and automotive industries. The company’s Tribobond™ 48 ta-C coating, capable of reaching ≈8000 HV, is widely used in extreme wear applications. With a multi-year defense contract secured in September 2025, Ionbond continues to expand DLC usage in harsh-environment optical and actuator systems, benefiting customers needing long-term performance under high load and thermal stress.

HEF Group - Leader in duplex DLC systems combining nitriding and advanced surface engineering

HEF Group specializes in combining liquid nitriding with its CERTESS™ DLC coatings, enabling exceptionally high-load performance for automotive, industrial, and firearms components. The company’s DLC achieves 2500–4500 HV hardness with friction coefficients 200–500% lower than conventional coatings such as TiN. HEF's duplex solutions are particularly valued for extending fatigue life in high-contact stress components.

CemeCon AG - Expert in ta-C and PECVD equipment for ultra-hard DLC deposition

CemeCon supplies advanced coating equipment capable of producing hydrogen-free ta-C films with customizable sp3/sp2 bonding ratios, enabling coatings with very high hardness and low internal stress. The company focuses on optimized plasma control, supporting semiconductor, cutting tool, and precision engineering sectors. Its systems help OEMs produce high-purity, high-adhesion DLC layers tailored to specific wear and thermal-load conditions.

IHI Hauzer Techno Coating B.V. - Innovator in HIPIMS+ and advanced PACVD DLC technologies

Hauzer, part of the IHI Group, is a leading DLC equipment provider known for its Flexicoat® platforms and its pioneering work in hydrogen-free ta-C deposition for automotive engine components. In 2024 (Q4), the company introduced a dry DLC basecoat technology that reduces environmental impact and improves process efficiency. Hauzer’s systems are widely adopted in automotive piston ring production, achieving up to 20% friction reduction over legacy CrN coatings.

Diamond like Carbon market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$921.6 Million

|

|

Market Size (2035)

|

$1762.7 Million

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Type (Hydrogen-Free DLC, Hydrogenated DLC, Metal-Doped DLC, Silicon-Doped DLC, Fluorinated DLC), By Deposition Technology (PVD, CVD, PECVD, HiPIMS), By Application (Automotive Components, Industrial Tools, Medical Devices, Electronics & Semiconductors, Aerospace Components, Optical Systems), By Substrate Material (Metals, Ceramics, Polymers, Silicon Wafers), By Film Thickness (Thin Coatings, Thick Coatings)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Oerlikon Balzers, IHI Ionbond AG, CemeCon AG, Miba AG, Morgan Advanced Materials plc, Techmetals Inc., Richter Precision Inc., Calico Coatings Inc., Acree Technologies Inc., Stararc Coating Co. Ltd., Element Six, Sulzer AG, Nippon Pillar Packing Co. Ltd., Plasma Technology Inc., Hauzer Techno Coating B.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Diamond-Like Carbon (DLC) Market Segmentation

By Type

- Hydrogen-Free DLC

- Hydrogenated DLC

- Metal-Doped DLC

- Silicon-Doped DLC

- Fluorinated DLC

By Deposition Technology

- Physical Vapor Deposition (PVD)

- Chemical Vapor Deposition (CVD)

- Plasma-Enhanced Chemical Vapor Deposition (PECVD)

- High-Power Impulse Magnetron Sputtering (HiPIMS)

By Application

- Automotive Components

- Industrial Tools

- Medical Devices

- Electronics & Semiconductors

- Aerospace Components

- Optical Systems

By Substrate Material

- Metals (Steel, Aluminum Alloys, Titanium)

- Ceramics (Silicon Carbide, Al₂O₃)

- Polymers (Specialty Plastics)

- Silicon Wafers

By Film Thickness

- Thin Coatings (≤100 nm)

- Thick Coatings (>100 nm to ~10 μm)

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Diamond-Like Carbon (DLC) Market

- Oerlikon Balzers

- IHI Ionbond AG

- CemeCon AG

- Miba AG

- Morgan Advanced Materials plc

- Techmetals Inc.

- Richter Precision Inc.

- Calico Coatings, Inc.

- Acree Technologies Inc.

- Stararc Coating Co., Ltd.

- Element Six

- Sulzer AG

- Nippon Pillar Packing Co., Ltd.

- Plasma Technology Inc.

- Hauzer Techno Coating B.V.

*- List not Exhaustive