Dipropylene Glycol Market to Reach $9.7 Billion by 2034 at 3.1% CAGR Amid Asia Capacity Expansion and High-Purity Demand

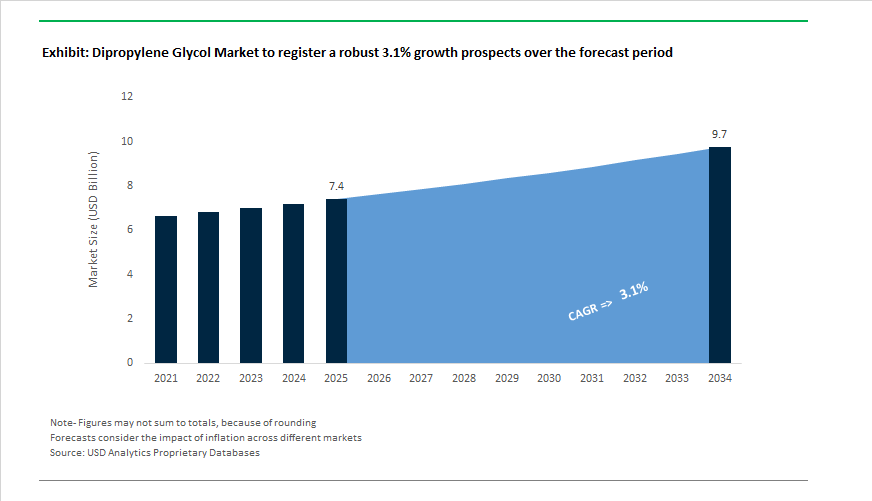

The Dipropylene Glycol (DPG) Market is projected to grow from $7.4 billion in 2025 to $9.7 billion by 2034, registering a CAGR of 3.1%. Market performance reflects steady demand from fragrance compounds, personal care solvents, industrial plasticizers, and pharmaceutical excipients, balanced against structural capacity adjustments in Europe and Asia. In May 2024, Dow completed an 80,000 tons per year expansion at its Map Ta Phut facility in Thailand, lifting total site capacity to 250,000 tons annually and establishing it as the largest propylene glycol complex in the Asia-Pacific region. The expansion directly strengthens DPG supply for high-growth fragrance and cosmetic markets in Southeast Asia and China. By late 2024, the same facility secured ISCC PLUS certification, enabling mass-balance tracking of bio-circular feedstocks and reinforcing demand from multinational FMCG brands seeking lower product carbon footprint DPG solutions.

European restructuring has reshaped the supply landscape. In September 2025, INEOS Oxide permanently shut down its Propylene Oxide and Propylene Glycol units at the Cologne (Dormagen) site in Germany, citing uncompetitive raw material costs and structural disadvantages associated with the chlorohydrin process. This exit tightened regional supply while accelerating import reliance. Simultaneously, Shell divested its Singapore refinery and petrochemical assets in May 2024, including Bukom and Jurong Island facilities that serve as critical nodes in the glycol value chain, signaling a broader retreat from merchant petrochemicals in favor of energy transition assets. Through 2025, LyondellBasell implemented multiple PG price increases across the Americas, including $0.04 per pound hikes in February and March and a $0.05 per pound adjustment effective September 1, reflecting feedstock volatility and distribution cost inflation. INEOS Oxide further announced a glycol-related price increase effective February 15, 2026, highlighting persistent raw material pressure entering the 2026 fiscal cycle.

Product specification upgrades and sustainability positioning are emerging as primary competitive differentiators. Between 2024 and 2025, demand for high-purity DPG (>99%) intensified, particularly for injectable pharmaceutical carriers and premium cosmetic formulations where low toxicity and odor neutrality are mandatory. In November 2025, Repsol updated its Fragrance Grade DPG specifications, reinforcing GMP+ and FSSC 22000 compliance to secure high-end perfumery and personal care contracts. BASF implemented its Winning Ways strategy in 2025, transitioning glycol portfolios toward biomass-balanced production using ISCC PLUS-certified inputs. The company further streamlined its operations by completing the sale of its decorative paints business to Sherwin-Williams in October 2025, refocusing on integrated Verbund efficiency. The launch of BASF’s global Digital Hub in Hyderabad in Q1 2026 is designed to optimize glycol manufacturing and logistics using AI-driven analytics, improving cost competitiveness and supply reliability for specialty glycols, including fragrance-grade and pharmaceutical-grade Dipropylene Glycol.

Trends and Opportunities Shaping the Dipropylene Glycol (DPG) Market

Regulatory-Led Reformulation in Fine Fragrances and Personal Care Products

- Regulatory pressure in cosmetics and fragrances is redefining acceptable quality thresholds for Dipropylene Glycol. As of October 30, 2025, all fragrance compounds marketed in the European Union must comply with the IFRA 51st Amendment, which places strong emphasis on dermal sensitization prevention. This requirement is accelerating the transition toward low-odor, high-purity DPG that can function as a neutral carrier for allergen-compliant fragrance systems without contributing to skin irritation or scent distortion.

- Simultaneously, the revised Classification, Labelling, and Packaging Regulation implemented in June 2025 has intensified scrutiny on excipient-grade solvents used in personal care. Under this framework, suppliers are increasingly evaluated for narrow isomer distributions and ultra-low peroxide residuals to ensure oxidative stability during storage. Global consumer goods manufacturers are responding by rationalizing their supplier base and prioritizing DPG grades that support longer shelf life for premium body sprays, deodorants, and fine mists. This trend is particularly visible in Europe and Japan, where clean-label positioning and regulatory transparency directly influence brand competitiveness.

DPG as a Reactive Diluent for Low-VOC Composite and Resin Systems

- In industrial applications, Dipropylene Glycol is evolving from a conventional glycol into a strategic enabler of low-emission resin technologies. Within the Unsaturated Polyester Resin sector, DPG is increasingly specified as a reactive diluent rather than a passive modifier. Resin curing studies published in 2025 confirm that DPG-based UPR formulations deliver improved hydrolytic stability and enhanced flexibility compared with traditional propylene glycol systems.

- Because DPG chemically cross-links into the polymer backbone during curing, it reduces free monomer emissions and lowers overall volatile organic compound output by up to 12% in marine gel coats and transport composites. This performance is driving adoption in applications subject to green building and occupational exposure standards, including marine hull fabrication and automotive body panels. Additionally, DPG’s high boiling point and low vapor pressure make it particularly suitable for low-styrene and low-odor resin systems, improving worker safety in open-molding environments and reducing ventilation-related operating costs.

Next-Generation, Low-Toxicity Aircraft Anti-Icing and De-Icing Fluids

- The aviation industry is emerging as a high-value growth channel for Dipropylene Glycol, driven by the global push to replace toxic ethylene glycol in airfield operations. In 2025, airports are increasingly transitioning toward Type IV anti-icing fluids, which offer extended holdover times under freezing rain and snow conditions. DPG’s high boiling point and film-forming persistence make it well-suited for these formulations, where maintaining aerodynamic performance during prolonged ground exposure is critical.

- Environmental performance is a decisive factor in this transition. Government guidance issued in January 2025 on airport effluent management indicates that more than 60% of major European hubs are prioritizing glycol recycling systems and lower aquatic toxicity profiles. Compared with ethylene glycol, DPG exhibits higher biodegradability and lower biological oxygen demand, positioning it as a preferred component in the $1.24 billion aviation fluids market as airports align with eco-certification and discharge compliance targets.

Coalescing Aid and Performance Enhancer in Waterborne Polymer Dispersions

- The continued shift toward waterborne technologies in architectural and industrial coatings is opening a durable opportunity for Dipropylene Glycol as a coalescing aid. Research published in October 2025 demonstrates that DPG and its dimethyl ether derivatives play a critical role in achieving uniform film formation in low-VOC acrylic and polyurethane dispersions. Acting as a temporary plasticizer, DPG enables polymer particles to fuse effectively during water evaporation, resulting in smoother finishes and reduced surface defects.

- From a performance standpoint, DPG-based formulations extend open time for professional applicators by 20 to 30 %, improving workability without compromising drying speed or hardness. Beyond coatings, this same solvency profile is driving DPG adoption in precision aqueous cleaning solutions. In late 2025, manufacturers of electronic and medical device cleaners highlighted DPG as a safer alternative to chlorinated solvents, capable of dissolving both polar and non-polar contaminants while supporting stringent residue and safety requirements.

Dipropylene Glycol (DPG) Market Share and Segmentation Insights

Fragrances Anchor Demand While Electronics Emerges as a High-Growth Application

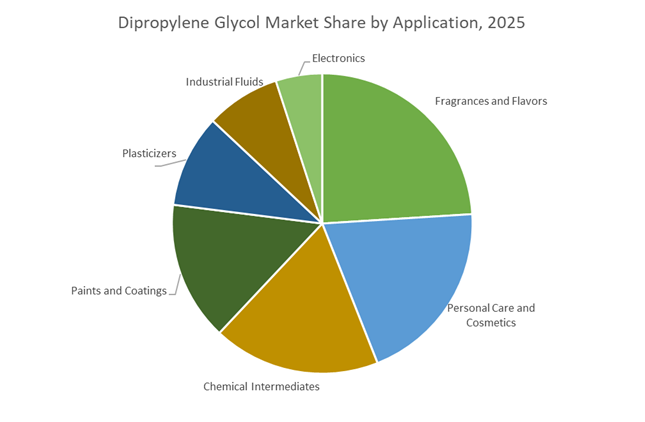

Fragrances and flavors lead the Dipropylene Glycol (DPG) market in 2025 with 24% share, reinforcing DPG’s role as a preferred low-odor solvent and fixative in fine perfumery and functional fragrances, where it enhances scent longevity across personal care and household products. Personal care and cosmetics follow closely, using DPG as a humectant, solvent, and viscosity modifier in skincare, haircare, and color cosmetics, driven by demand for mild, high-performance formulations. Chemical intermediates represent a significant segment, consuming DPG in unsaturated polyester resins, specialty esters, and plasticizer production. Paints and coatings leverage DPG as a coalescing agent in low-VOC waterborne systems, improving flow, film formation, and freeze-thaw stability. Plasticizers maintain steady uptake in flexible polymers, while industrial fluids remain niche. Electronics is a fast-growing application, adopting high-purity DPG in solder fluxes, photoresists, and precision cleaning where ultra-low residue profiles are critical.

Cosmetics Lead End-Use as Construction and Pharma Sustain Volume Growth

Cosmetics and personal care dominate DPG consumption with 32% market share, supported by premiumization trends and rising demand for fragrance carriers and skin-compatible solvents. Building and construction is a major end-user, incorporating DPG into architectural coatings, sealants, and construction chemicals to deliver durable, low-VOC building materials. Pharmaceuticals and healthcare account for a significant share, using DPG as an excipient, humectant, and solvent in topical formulations and oral liquids where regulatory compliance is essential. Automotive and transportation maintain important demand through coatings, interior plasticizers, and industrial fluids that require thermal stability and compatibility. Food and beverage applications remain steady, relying on DPG as a carrier for flavors and additives approved for food contact. Electrical and electronics continue to expand, driven by semiconductor manufacturing and PCB processing that increasingly specify high-purity DPG for cleaning and materials processing.

Competitive Landscape of the Dipropylene Glycol Market

The Dipropylene Glycol (DPG) market in 2026 is shaped by feedstock integration, specialty-grade innovation, fragrance and personal care demand, and rising polyurethane consumption, with competition increasingly centered on low-odor grades, bio-based DPG, and regional supply security. Global leaders are differentiating through propylene oxide backward integration, sustainable production pathways, and application-specific formulations.

Dow Inc. sets the global benchmark for low-odor and bio-based DPG

Dow Inc. anchors the global propylene derivatives ecosystem, leveraging full vertical integration into propylene oxide (PO) to stabilize pricing and availability during 2026 raw material volatility. Its flagship DPG LO+ (Low Odor) grade is the industry standard for premium perfumery and cosmetics, prized for its near-neutral odor profile. In late 2025, Dow expanded its bio-based propylene glycol capacity, enabling drop-in replacement of fossil-derived DPG in sustainable consumer products. Holding roughly 20–22% of the global specialty DPG market, Dow dominates North America and Europe while advancing greener solvent platforms for fragrances, personal care, and high-end formulations.

BASF SE drives European DPG demand through PU resins and net-zero manufacturing

BASF SE commands the European DPG landscape through its Verbund-integrated production model, supplying polyurethane foams and alkyd resin manufacturers at scale. The 2025–2026 launch of Pluriol® A 2400 I targets reactive intermediates that exploit DPG’s solubility to improve waterborne coating stability. Strategically, BASF is transitioning Ludwigshafen toward a net-zero chemical park, with partial DPG output powered by offshore wind. In 2026, BASF intensified expansion across Vietnam and Indonesia, addressing surging demand from Southeast Asia’s home care and detergent hubs while reinforcing its leadership in flexible foams and high-durability paints.

LyondellBasell Industries scales industrial DPG via high-yield catalytic hydration

LyondellBasell Industries focuses on high-efficiency industrial glycol production, strengthened by its March 2025 propylene capacity expansion at Channelview, Texas, which directly lifted DPG co-product availability. The company applies advanced catalytic hydration to maximize yields of DPG isomers favored by plasticizer and UPR producers. Its Industrial Grade DPG is widely used as a textile lubricant and secondary solvent for unsaturated polyester resins. In 2026, LyondellBasell deployed AI-driven logistics optimization, shortening lead times for APAC customers and reinforcing its position as a volume-driven supplier to global construction and composites markets.

Huntsman Corporation integrates DPG into advanced automotive and fragrance formulations

Huntsman Corporation operates as a specialty performance player, embedding DPG into polyurethane catalysts and specialty polyols for automotive interiors, sound-dampening materials, and construction foams. A 2025 partnership with a leading fragrance house produced custom DPG carrier blends that enhance scent throw in luxury candles and reed diffusers. The company expanded Indian manufacturing in late 2025 to capture growth from the country’s rapidly accelerating EV sector, where DPG-derived resins support battery housings. Huntsman’s core advantage lies in downstream formulation expertise, delivering ready-to-use DPG blends for complex industrial applications.

Manali Petrochemicals Limited dominates India with pharma-grade and import-substitution DPG

Manali Petrochemicals Limited is South Asia’s primary glycol supplier, holding over 60% share of India’s domestic DPG market under the “Make in India” framework. The company is aggressively expanding high-purity DPG USP grades to replace costly imports used in pharmaceutical formulations and Ayurvedic personal care products. Its 2025 upgrades to effluent treatment and energy recovery systems align operations with India’s 2026 Green Industry standards. With a sharp focus on import substitution and healthcare-grade solvents, Manali has positioned itself as the regional gatekeeper for pharmaceutical and specialty DPG supply.

INEOS Oxide strengthens European supply through pipeline-fed oxide integration

INEOS Oxide operates as Europe’s efficiency-driven DPG powerhouse, completing a major debottlenecking project at Köln, Germany in 2025 to meet rising fragrance-sector demand. Its massive regional pipeline network delivers raw propylene gas directly to oxide plants, ensuring some of the lowest landed DPG costs in Europe. INEOS is also the primary supplier to agrochemical formulators, where DPG serves as a low-toxicity solvent for herbicides and pesticides. Known for rigorous REACH compliance, INEOS DPG is the preferred choice for EU multinationals seeking consistent, regulation-ready glycol supply.

China: Downstream Deepening and High-Purity Differentiation

China’s dipropylene glycol market is being reshaped by a deliberate policy shift away from volume-driven refining toward value-added downstream chemistry. In September 2025, the Ministry of Industry and Information Technology formalized the Work Plan for Stabilizing Growth in the Petrochemical and Chemical Industry, setting a 5% annual growth target in added value through 2026. Within this framework, specialty glycols such as dipropylene glycol LO+ are explicitly prioritized as strategic intermediates for fragrance, personal care, and electronics applications. By tightly controlling new refining capacity, the policy channels investment into converting propylene derivatives into higher-margin glycols rather than expanding base olefin output.

Demand-side momentum is equally structural. A 14.4% year-over-year increase in retail passenger vehicle sales as of March 2025 has intensified R&D around low-odor, low-VOC DPG grades used in automotive interior coatings and sealants to meet 2026 cabin air quality benchmarks. Parallelly, the High-Tech Supply Chain Initiative has accelerated domestic production of electronic-grade DPG for photoresist stripping and semiconductor precision cleaning, supporting China’s goal of 90% self-sufficiency in electronic chemicals by 2026. Export pricing volatility has moderated since Q4 2025 as stricter environmental enforcement forced smaller, high-emission glycol plants in Zhejiang and Jiangsu to exit, restoring discipline to domestic supply.

United States: Regulatory Preference and Decarbonized Supply Chains

In the United States, the dipropylene glycol market is anchored by regulatory clarity and strategic pricing discipline. Effective November 6, 2025, Dow implemented a $0.05 per pound price increase across all DPG grades, including DPG LO+ and PURAGUARD PG USP/EP, reflecting persistent raw material and energy volatility. This move was closely followed by Indovinya, signaling coordinated industry alignment rather than isolated supplier action.

From a regulatory standpoint, the U.S. EPA’s classification of DPG as a low-risk preference solvent under the updated TSCA framework throughout 2025 has materially strengthened its substitution case against higher-toxicity ethers in industrial degreasers and cleaning formulations. Producers are also leveraging Inflation Reduction Act incentives to integrate mass-balanced and circular feedstocks into Gulf Coast glycol operations, linking DPG production to broader decarbonization narratives. Structurally, the rapid expansion of the Arizona semiconductor corridor is creating a forward demand pipeline for electronic-grade DPG as a carrier solvent in advanced lithography processes, tying market growth to capital-intensive chip manufacturing rather than cyclical construction demand.

India: Capacity Build-Out and Trade Protection Dynamics

India’s dipropylene glycol market is transitioning from import dependence toward domestic capacity-led growth. In July 2025, Manali Petrochemicals Ltd commissioned a major expansion of its propylene glycol and DPG facility, adding 50,000 KTPA of capacity to support the Make in India agenda. This expansion materially improves domestic availability for downstream paints, textiles, and fragrance manufacturers. Regulatory easing has further supported smaller formulators. The November 2025 withdrawal of Quality Control Orders for multiple industrial inputs removed mandatory BIS certification for several chemical precursors, reducing compliance friction for MSME-scale DPG users.

Trade policy remains a defining variable. In late 2025, the Directorate General of Trade Remedies proposed anti-dumping duties of $102–$173 per ton on glycol imports from Gulf countries and Singapore, aiming to shield domestic producers such as Reliance Industries Limited from low-cost imports. While contested by yarn and textile stakeholders, the proposal underscores the strategic importance India assigns to glycol self-sufficiency. On the demand side, India’s expanding fragrance and personal care sector recorded a 12% increase in DPG consumption in 2025, driven by the growing popularity of alcohol-free, odor-neutral fragrance oils in premium domestic brands.

Saudi Arabia: Integrated Exports and Cost Leadership

Saudi Arabia continues to function as a structurally important global supply hub for dipropylene glycol, underpinned by fully integrated feedstock economics. As of 2025, the national chemical manufacturing base is valued at $47.1 billion, with SABIC and Sadara Chemical Company pivoting from bulk petrochemical exports toward higher-performance glycols and polyols in line with Vision 2030. Internal transformation programs reported in Q4 2025 optimized DPG production costs by approximately 8%, reinforcing Saudi Arabia’s position in the lowest global cost quartile.

Sadara’s Al-Jubail complex remains the primary export node for DPG shipments into Asia-Pacific markets, benefiting from direct integration with Saudi Aramco refineries. This structural advantage allows Saudi producers to maintain margin resilience despite global overcapacity in basic chemicals, positioning DPG as a strategic export product rather than a commoditized by-product.

Germany: Compliance-Driven Substitution and Bio-Based Innovation

Germany’s dipropylene glycol market is shaped by regulatory evolution and sustainability-led innovation. The forthcoming REACH revision, expected by the end of 2025, will introduce mandatory Digital Product Passports requiring detailed disclosure of carbon footprint and toxicity data across the DPG supply chain from 2026. This requirement is accelerating investments in traceability systems and favoring producers with transparent, regionally integrated operations.

On the innovation front, BASF expanded its European portfolio in May 2025 with new Pluriol-branded products while intensifying R&D into bio-based DPG derivatives sourced locally to reduce lifecycle emissions. Regulatory pressure is also reshaping solvent choices. Under Regulation (EU) 2025/1090, restrictions on solvents such as DMAC and NEP have accelerated industrial substitution toward DPG and DPGME in man-made fiber and film production, embedding dipropylene glycol into the EU’s safer-solvent transition rather than discretionary consumption.

Dipropylene Glycol Market: Country-Level Strategic Summary

Dipropylene Glycol Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Demand Anchors

|

Market Positioning

|

|

China

|

Downstream deepening, self-sufficiency

|

Automotive interiors, electronics

|

Policy-led specialization

|

|

United States

|

TSCA preference, decarbonization

|

Industrial cleaning, semiconductors

|

Regulation-backed substitution

|

|

India

|

Capacity expansion, trade defense

|

Paints, fragrances, textiles

|

Import replacement growth

|

|

Saudi Arabia

|

Integrated cost leadership

|

APAC exports, polyols

|

Global supply hub

|

|

Germany

|

REACH compliance, bio-based R&D

|

Fibers, films, coatings

|

Sustainability-driven market

|

Dipropylene Glycol Market Report Scope

Dipropylene Glycol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.4 Billion

|

|

Market Size (2034)

|

$9.7 Billion

|

|

Market Growth Rate

|

3.1%

|

|

Segments

|

By Grade (Fragrance Grade, Pharmaceutical Grade, Industrial Grade, Electronics Grade), By Application (Fragrances and Flavors, Personal Care and Cosmetics, Chemical Intermediates, Paints and Coatings, Plasticizers, Industrial Fluids, Electronics), By End-User Industry (Cosmetics and Personal Care, Pharmaceuticals and Healthcare, Automotive and Transportation, Building and Construction, Electrical and Electronics, Food and Beverage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., BASF SE, SABIC, LyondellBasell Industries N.V., Shell Chemicals, INEOS Oxide, Manali Petrochemicals Limited, LG Chem Ltd., Sadara Chemical Company, Indovinya, Huntsman Corporation, SKC Co., Ltd., Repsol S.A., China Petroleum & Chemical Corporation, OQ Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dipropylene Glycol Market Segmentation

By Grade

- Fragrance Grade

- Pharmaceutical Grade

- Industrial Grade

- Electronics Grade

By Application

- Fragrances and Flavors

- Personal Care and Cosmetics

- Chemical Intermediates

- Paints and Coatings

- Plasticizers

- Industrial Fluids

- Electronics

By End-User Industry

- Cosmetics and Personal Care

- Pharmaceuticals and Healthcare

- Automotive and Transportation

- Building and Construction

- Electrical and Electronics

- Food and Beverage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dipropylene Glycol Industry

- Dow Inc.

- BASF SE

- SABIC

- LyondellBasell Industries N.V.

- Shell Chemicals

- INEOS Oxide

- Manali Petrochemicals Limited

- LG Chem Ltd.

- Sadara Chemical Company

- Indovinya

- Huntsman Corporation

- SKC Co., Ltd.

- Repsol S.A.

- China Petroleum & Chemical Corporation

- OQ Chemicals

*- List not Exhaustive