Market Overview: Energy-Efficient and Smart Facade Systems Driving Growth

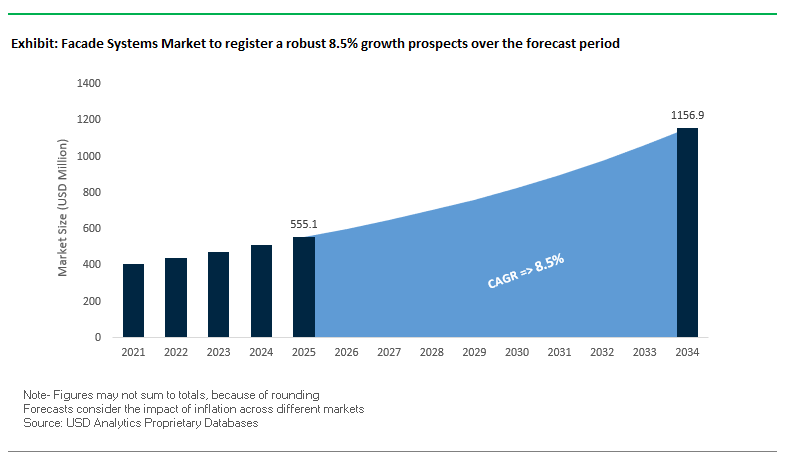

The Global Facade Systems Market is projected to expand from USD 555.1 million in 2025 to USD 1,156.7 million by 2034, growing at a CAGR of 8.5%. Facade systems have become one of the most critical elements of modern building design, balancing aesthetics, structural performance, energy efficiency, and sustainability. This market is closely linked with global construction trends and shifting regulatory landscapes that demand lower carbon footprints and greater building performance.

The adoption of prefabricated and unitized facade systems is reshaping project delivery by cutting on-site labor by up to 60%, reducing costs, and expediting timelines. Facades are also being redefined as active contributors to building energy performance, with ventilated systems and low-U-value glazing reducing HVAC loads by up to 25%. Moreover, smart facades integrated with photovoltaics and perovskite-coated solar glass are enabling buildings to generate renewable energy, aligning with net-zero carbon mandates.

Material innovation is another key driver. The increasing use of porcelain slabs, ceramic tiles, and fire-resistant composites offers both design flexibility and resilience against extreme weather. This trend reflects the dual priority of safety and visual appeal in high-performance facades.

Key Insights for Industry Professionals:

- Market Value: USD 555.1M (2025) → USD 1,156.7M (2034), CAGR 8.5%.

- Prefabricated facade panels reduce on-site labor by 60%, boosting efficiency.

- Growing adoption of low-U-value glass and ventilated cavities to meet strict energy codes.

- Smart facades with BIPV and solar coatings emerging as revenue-generating surfaces.

- Porcelain and ceramic cladding gaining popularity for durability and aesthetics.

Market Analysis: Recent Developments in the Global Facade Systems Industry

The Facade Systems Market is undergoing rapid transformation, with recent M&A activity, sustainability initiatives, and product innovations shaping its growth trajectory.

In August 2025, Innovators Façade Systems Limited announced an AI-powered market expansion strategy, using predictive analytics to identify new geographies with high demand potential. The same month, industry reports highlighted the rise of uPVC in door and window segments, achieving nearly 35% market share due to durability and cost advantages, indirectly influencing facade system designs.

In July 2025, the merger between LIXIL and GROHE was finalized, creating a new global leader with an expanded product portfolio in housing and water systems, strengthening integration opportunities in facade applications. In the same month, JELD-WEN released its 2024 Sustainability Report, marking progress in Cradle to Cradle® certifications across its product portfolio.

In June 2025, Saint-Gobain completed its USD 3 billion acquisition of CSR Limited, enhancing its Asia-Pacific presence and expanding access to facade insulation and materials. That month, a construction report highlighted a growing preference for certified fire doors, with 30% of UK housing authority projects adopting such solutions for safety compliance.

In May 2025, Owens Corning acquired Masonite International Corporation in a USD 3.9 billion deal, strengthening its building materials portfolio and enhancing its role in integrated facade systems. Earlier in April 2025, Parallel Architectural Products introduced aluminum self-mating battens, an innovation simplifying facade installation with multi-orientation adaptability.

Emerging Trends and Untapped Opportunities Reshaping the Global Façade Systems Market

Integration of Building-Integrated Photovoltaics (BIPV) as a Multifunctional Cladding Material

The façade systems market is witnessing a paradigm shift with the seamless incorporation of building-integrated photovoltaics (BIPV) into cladding materials, turning façades into active energy-generating assets. Unlike traditional solar panels, BIPV technology integrates directly into glass curtain walls, spandrels, terracotta panels, and rainscreen systems, enabling buildings to generate renewable energy while maintaining aesthetic and functional integrity. The dual advantage of energy efficiency and sustainable design is propelling this trend, with case studies such as the Danish energy community project—featuring more than 30,000 square meters of BIPV installations supporting a 4 MW project—proving large-scale viability. Manufacturers are rapidly commercializing transparent and semi-transparent thin-film photovoltaic glass that allows natural light penetration while delivering solar power output. For developers and architects, BIPV represents a high-value growth avenue, offering not only compliance with green building codes but also a measurable ROI through energy savings and carbon reduction. This positions BIPV as a cornerstone technology in the evolution of high-performance façade systems.

Adoption of Prefabricated, Unitized Façade Modules for Construction Efficiency

The demand for prefabricated, unitized façade modules is rising as the construction industry grapples with labor shortages and the urgent need for faster project delivery. In the façade systems market, developers and contractors are increasingly specifying factory-assembled, pre-glazed façade units that can be transported and installed directly onsite, minimizing weather disruptions and reducing project risks. Publications highlight that prefabricated modular construction can accelerate timelines by up to 30%, cutting weeks or months off delivery schedules while ensuring higher quality through controlled factory production. Industry leaders are offering unitized façade systems compatible with a wide range of structural requirements, emphasizing adaptability across high-rise commercial, residential, and institutional projects. The impact on the value chain is transformative, requiring early collaboration between architects, engineers, and façade manufacturers to ensure modular compatibility from the design phase. This trend presents a significant growth opportunity, as prefabricated façades lower material waste, reduce on-site labor requirements, and provide developers with greater predictability in cost and schedule management.

Development of Dynamic and Adaptive Glazing Systems for Carbon Reduction

A key opportunity in the façade systems industry lies in advancing dynamic and adaptive glazing technologies capable of automatically adjusting tint levels in response to solar heat gain, daylight, or occupant preferences. Unlike static high-performance glass, dynamic glazing enables real-time optimization of building energy use, drastically reducing cooling loads and HVAC demand. Studies highlight that energy losses through windows account for nearly 30% of building heating and cooling consumption in the U.S., making this innovation highly impactful. Research has shown that advanced dynamic glazing prototypes can lower heating power demand by 2.2 W/m² at -20°C and deliver 15–20% overall energy savings compared to conventional glazing systems. Beyond energy efficiency, this technology significantly improves occupant comfort and productivity—studies report office workers in dynamic glazing environments experience 21.7% higher productivity and 25.3% better moods compared to manual shading systems. For façade manufacturers, dynamic glazing represents a premium growth segment, aligning with global net-zero targets, stricter building codes, and rising demand for occupant-centric designs.

Implementation of Lifecycle Assessment (LCA) and Digital Material Passports

The growing emphasis on embodied carbon reduction and circular construction practices is creating an opportunity for façade manufacturers to differentiate by offering Lifecycle Assessment (LCA) data, Environmental Product Declarations (EPDs), and digital material passports. These tools document the full material composition, carbon footprint, and recyclability of façade systems, enabling architects and builders to make informed sustainability decisions. Regulatory shifts like the EU’s Green Deal and Digital Product Passport (DPP) framework are accelerating adoption, mandating transparency and circularity in building materials. Industry collaborations such as HolyGrail 2.0, though focused on packaging, are providing a technological blueprint for applying digital watermarking and traceability in construction materials. Case studies show that brick façades outperform metal panels in long-term carbon performance over a 150-year lifecycle, underscoring the value of LCA-based design choices. For manufacturers, offering verified digital passports for façade products opens a new revenue stream by enabling compliance with LEED, BREEAM, and other green building certifications. This not only strengthens brand reputation but also creates a long-term competitive edge in sustainable construction markets.

Competitive Landscape: Key Players Transforming the Facade Systems Market

The Facade Systems Market is dominated by global building materials leaders and specialized facade solution providers. Companies are pursuing strategic acquisitions, product innovations, and sustainable practices to reinforce their competitive positions.

Saint-Gobain strengthens Asia-Pacific facade portfolio with CSR acquisition

Saint-Gobain is a leader in sustainable construction materials, offering glazing, insulation, and fire-resistant facade solutions. In June 2025, it acquired CSR Limited for USD 3 billion, expanding its reach in the Asia-Pacific. Its strategic focus remains on decarbonization and energy-efficient building solutions, particularly low-U-value glazing and sustainable cladding.

Permasteelisa expands North American footprint through Benson Industries acquisition

Permasteelisa specializes in curtain wall and unitized facade systems for iconic commercial buildings worldwide. In early 2025, it acquired key assets from Benson Industries, strengthening its U.S. presence. Known for high-performance sealing and weather resistance, Permasteelisa’s focus is on combining aesthetics with sustainability in large-scale projects.

Apogee drives smart glass innovation with electrochromic glazing

Apogee Enterprises is a major player in architectural glass and framing systems. Its innovation in electrochromic smart glass allows facades to dynamically adjust to sunlight, reducing cooling costs and improving occupant comfort. Apogee’s strategy is to provide integrated design-to-installation solutions, catering to commercial and institutional projects demanding energy efficiency.

Reynaers Aluminium focuses on ventilated facades and circular economy

Reynaers Aluminium develops sustainable aluminum systems for facades, windows, and doors. It has pioneered ventilated facade systems that enhance thermal efficiency and indoor air quality. With a strong focus on recycled aluminum and reusable designs, Reynaers aligns its strategy with circular economy principles while serving diverse residential and commercial projects.

LIXIL launches high-performance hybrid windows for Japanese housing

LIXIL Group combines housing and water products with a strong presence in Asia. In September 2025, it launched a new hybrid window series designed to improve thermal insulation for the Japanese residential market. Its strategic focus is on energy-efficient and aesthetically advanced solutions, contributing to decarbonized housing initiatives.

Facade Systems Market Share Insights

Curtain Walls Dominate Market Share by Product Type in Facade Systems

Curtain walls command 40% of the facade systems industry market, making them the clear leader by product type. Their dominance is anchored in the architectural requirements of modern high-rise and mid-rise commercial projects, where developers prioritize glazed exteriors for aesthetics, natural daylighting, and energy efficiency. Curtain walls deliver not only a premium look but also superior scalability, as they allow for rapid assembly on large footprints such as corporate headquarters, airports, and institutional complexes. With advancements in unitized systems, thermally broken frames, and double-skin facades, curtain walls continue to address rising energy performance standards while reducing installation time. Their high value-per-square-foot ensures strong demand, positioning them as the defining facade solution in commercial construction worldwide.

Commercial Buildings Secure the Largest Market Share by End-Use in Facade Systems

The commercial sector accounts for 65% of the facade systems market, reflecting its role as the primary demand engine. Large-scale projects such as retail complexes, office towers, healthcare facilities, and hotels require expansive facade coverage, making them the most lucrative and technologically demanding applications. Developers in this sector prioritize facades that balance aesthetics with performance—seeking solutions that improve energy efficiency, reduce operational costs, and enhance occupant comfort. The adoption of curtain walls and rainscreen cladding is particularly strong here, as these systems combine design flexibility with long-term durability and compliance with tightening green building codes. The sheer surface area and architectural prominence of commercial projects secure their overwhelming market share, setting the benchmark for innovation across the industry.

United States Facade Systems Market Expanding Through Energy Efficiency Standards and Smart Facade Technologies

The United States facade systems market is heavily shaped by federal and state-level building codes, including the Department of Energy's updated energy efficiency standards for commercial buildings. These regulations are driving demand for high-performance facade solutions that improve thermal efficiency and meet sustainability goals. Technological advancements, such as insulated glass units (IGUs) with low-emissivity (Low-E) coatings and smart facades integrated with building management systems, are increasingly being adopted to enhance energy efficiency and operational control.

Corporate investments are also accelerating market growth. In January 2025, Enclos Corporation partnered with CarbonCure Technologies to develop low-carbon building facades tailored for urban retrofits, demonstrating a strategic focus on sustainable urban infrastructure. Key applications include residential and commercial renovations as well as new constructions, with growing interest from property developers aiming for LEED certification and energy-efficient design. Federal incentives, tax rebates, and urban zoning policies are further bolstering adoption, making the U.S. a dynamic market for innovative and sustainable facade systems.

Germany Facade Systems Market Leading Through Circular Economy and Advanced Double-Skin Facade Technologies

Germany’s facade systems industry operates under the European Union’s Energy Performance of Buildings Directive (EPBD), mandating energy-efficient building designs. This stringent regulatory framework drives demand for premium, insulated facade solutions. The market also benefits from Germany’s circular economy initiatives, which encourage the use of recycled materials and products designed for end-of-life recycling.

Technological innovation is a hallmark of the German market, with double-skin glass facades (DSFs) emerging as an effective solution to combat heat loss, overheating, and noise issues associated with curtain walls. Collaborations, such as the partnership between Fischer and Solarwatt, are enabling seamless integration of photovoltaic modules into building facades. Key applications span residential and commercial construction, where consumers seek durable, energy-efficient, and aesthetically pleasing facade solutions. Germany’s focus on digitalization and automation under “Plattform Industrie 4.0” enhances manufacturing productivity, while companies like RAK Ceramics cater to the demand for facades that balance functionality with aesthetic appeal.

China Facade Systems Market Driven by Green Initiatives and Prefabrication Innovations

China’s facade systems market is expanding rapidly, supported by governmental initiatives such as the “dual carbon” goal and the Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement. These policies encourage the adoption of sustainable materials and energy-saving technologies in the building sector. Technological advancements in automation, AI, and “5G plus industrial internet” are improving manufacturing efficiency and enabling flexible production capacities.

Domestic manufacturing is gaining momentum, with companies like China State Construction Development enhancing capacity to meet rising demand for high-quality, circular facade products. Key applications include residential and commercial buildings, driven by urbanization, rising disposable incomes, and government-led infrastructure projects. Innovation in prefabrication and complex curved surfaces is helping reduce construction waste and improve safety. Energy-saving facade systems that regulate light, temperature, and humidity are increasingly popular, offering up to 20% energy reduction in buildings.

India Facade Systems Market Expanding Through Smart City Initiatives and Aesthetic Innovations

India’s facade systems industry is being propelled by governmental initiatives such as “Housing for All,” smart city projects, and the “Make in India” program, which promote local manufacturing and technological development. Corporate investments are significant, exemplified by Saint-Gobain’s 2024 acquisition of UP Twiga Fiberglass Ltd., strengthening its portfolio of energy-efficient facade solutions.

Technological advancements, including automated fabrication and UPVC systems suitable for harsh climates, are increasing market efficiency. Expanding residential and commercial construction, including multi-story and mixed-use buildings, is driving demand for modern, high-performance facade solutions. Aesthetics are a major consideration, with middle-class buyers and developers seeking distinctive, high-end materials and designs. Industry events such as the 155th edition of Zak World of Facades India in 2025 highlight trends toward intelligent, sustainable facade innovations, positioning India as a growing market for advanced architectural solutions.

Brazil Facade Systems Market Strengthened by Regulatory Compliance and Ventilated Facade Technologies

Brazil’s facade systems market is influenced by ABNT and INMETRO certifications, which drive manufacturers to comply with fire safety and quality standards. The incorporation of robotics and AI in construction is transforming facade manufacturing, enabling smarter, more automated production. Corporate investments focus on creating products aligned with sustainability objectives, with new production facilities supporting local demand.

Key applications include residential and commercial new construction and renovation projects, with ventilated facades emerging as a solution for Brazil’s high temperatures and humidity. Sustainable materials and energy-efficient systems are increasingly being adopted, reflecting the market’s growing emphasis on green construction practices. The trend toward environmentally friendly, high-performance facade systems is positioning Brazil as a promising market for modern architectural solutions.

Facade Systems Market Report Scope

Facade Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$555.1 Million

|

|

Market Size (2034)

|

$1156.7 Million

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Material Type (Glass, Metal, Wood, uPVC, Ceramic & Stone), By Product Type (Curtain Walls, Rainscreen Cladding, EIFS, Siding), By End-Use Industry (Commercial, Residential, Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ASSA ABLOY AB, LIXIL Group Corporation, Saint-Gobain S.A., JELD-WEN, Inc., Pella Corporation, Andersen Corporation, YKK AP Inc., Aluplex, Enclos Corp., Reynaers Aluminium, Schüco International KG, Kingspan Group plc, DS Smith plc, WestRock Company, International Paper Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Facade Systems Market Segmentation

By Material Type

- Glass

- Metal

- Wood

- uPVC

- Ceramic & Stone

By Product Type

- Curtain Walls

- Rainscreen Cladding

- EIFS

- Siding

By End-Use Industry

- Commercial

- Residential

- Industrial

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Facade Systems Market

- ASSA ABLOY AB

- LIXIL Group Corporation

- Saint-Gobain S.A.

- JELD-WEN, Inc.

- Pella Corporation

- Andersen Corporation

- YKK AP Inc.

- Aluplex

- Enclos Corp.

- Reynaers Aluminium

- Schüco International KG

- Kingspan Group plc

- DS Smith plc

- WestRock Company

- International Paper Company

* List Not Exhaustive

Methodology

USDAnalytics utilized a comprehensive and systematic research approach to analyze the Global Facade Systems Market, combining both primary and secondary research methods to ensure accuracy and relevance for industry professionals. Primary research involved in-depth interviews with key stakeholders, including façade system manufacturers, construction companies, architects, engineers, and regulatory authorities, to capture insights on market drivers, innovations, and sustainability adoption. Secondary research included reviewing company reports, press releases, government regulations, industry publications, and patent databases to validate market trends, competitive landscapes, and material innovations. Quantitative modeling was applied to forecast market growth, including segmentation by material type, product type, and end-use industry, while qualitative assessments highlighted emerging technologies such as Building-Integrated Photovoltaics (BIPV), prefabricated unitized modules, dynamic glazing, and digital material passports. Regional dynamics across the U.S., Germany, China, India, and Brazil were evaluated with a focus on regulatory frameworks, green building initiatives, smart city programs, and urbanization-driven demand. This methodology ensures that USDAnalytics delivers a reliable, data-driven market outlook, equipping stakeholders with actionable insights for strategic, operational, and investment decisions in the evolving façade systems industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.