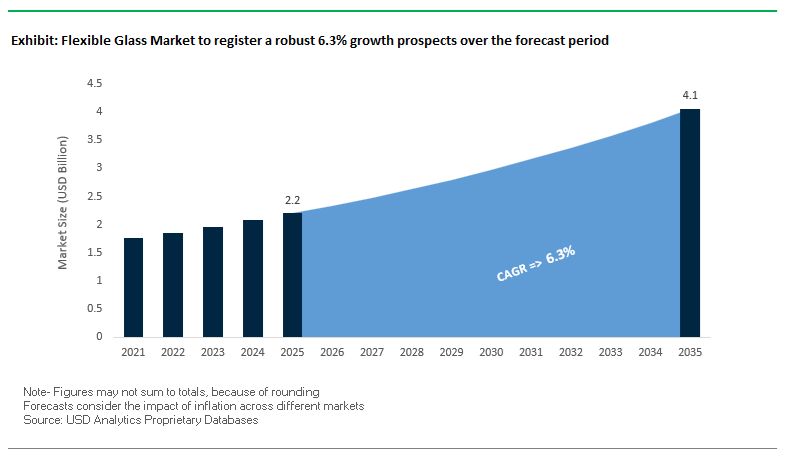

The Flexible Glass Market, valued at USD 2.2 billion in 2025, is expected to reach USD 4.1 billion by 2035, growing at a steady CAGR of 6.3%. The market is accelerating as ultra-thin glass (UTG) continues to replace polymer films in applications requiring superior thermal stability, mechanical robustness, optical clarity, and hermetic barrier performance. Industry professionals—particularly OLED display engineers, foldable device OEMs, and semiconductor packaging specialists—are increasingly evaluating flexible glass substrates based on bend radius performance, chemical strengthening depth, thermal endurance during TFT backplane fabrication, and compatibility with roll-to-roll (R2R) manufacturing. As flexible electronics evolve toward larger displays, foldable formats, rollable form factors, and ultra-thin encapsulation stacks, flexible glass is becoming a critical enabling material due to its combination of glass-like reliability and polymer-like flexibility.

The Flexible Glass Market is undergoing rapid technology-driven expansion, supported by advancements in ultra-thin substrate engineering, semiconductor packaging, and automotive interior design. A significant development occurred in December 2025, when AGC announced a breakthrough in curved automotive glazing, unveiling a UTG-based 3D cockpit display that is 30% lighter than conventional curved glass systems. The innovation marks a pivotal transition: flexible glass is no longer limited to foldable smartphones but is evolving into a key structural material for large-area, seamless automotive infotainment systems. Earlier in January 2025, AGC Glass Europe further expanded UTG-related capacity by investing in a new line for FINEO ultra-thin vacuum insulating glass—indicating rising demand for lightweight glazing across electronics and architecture.

Momentum in foldable electronics continues to strengthen. In November 2025, Corning reported a revenue uplift in its Display Technologies division, driven by mass commercialization of its Fusion-formed UTG for foldable smartphones. The validates the shift from niche innovation to mainstream adoption as foldable and rollable devices penetrate mid-to-premium consumer segments. Corning further underscored its leadership with the March 2025 launch of Gorilla® Glass Ceramic, offering enhanced durability by surviving 10 consecutive 1-meter drops on rough surfaces, addressing industry concerns about real-world damage resistance in flexible and rigid devices.

Flexible glass is also gaining momentum in semiconductor manufacturing. In September 2025, SCHOTT introduced its FLEXINITY® structured thin glass wafers—with Total Thickness Variation (TTV) <1 μm—supporting fan-out wafer-level packaging (FO-WLP) and advanced 3D integrated circuits. The positions flexible glass as a preferred substrate for high-density microelectronics, especially where polymer films lack dimensional stability. Additionally, May 2025 showcased broader application expansion when an IT hardware major presented a 17-inch rollable tablet prototype, signaling scalable UTG adoption in large-format IT devices including next-gen tablets, monitors, and foldable laptops.

Buyers are largely focusing on whether UTG can support the miniaturization demands of next-gen AMOLEDs, withstand flexural stresses exceeding 6 GPa, support precise lithography without dimensional drift, and deliver perfect water/oxygen impermeability—something plastic films cannot provide. Further, the growth of 3D automotive cockpit displays and large-format rollable devices is pushing manufacturers to innovate in curved UTG forming, structured thin glass wafers, and multi-functional coatings.

- UTG thickness below 100 μm enables tight bend radii (R1.5–R3 mm), essential for foldable smartphones and emerging rollable tablets.

- Chemical strengthening enables bend strength exceeding 6 GPa, enhancing survival under repeated flexing and extreme surface stress.

- Dimensional stability of 0.007% strain at 5 MPa tension ensures precise alignment during R2R semiconductor manufacturing.

- Thermal endurance up to 300°C allows flexible glass to support TFT backplane processing, outperforming polymer substrates.

- WVTR ≈ 0 (near-perfect hermetic barrier) extends operational life of OLED and quantum-dot displays, reducing failure risk from oxygen/moisture ingress.

Technology-Driven Market Shifts and High-Value Innovation Opportunities Reshaping the Flexible Glass Market

Trend 1 - Ultra-Thin Glass (UTG) Becomes the Preferred Substrate and Cover Window for Foldable & Rollable Display Devices

The transition from Colorless Polyimide (CPI) to Ultra-Thin Glass (UTG) marks the most significant materials shift in the flexible display industry to date. As global OEMs compete to deliver premium foldable smartphones, tablets, e-paper devices, and rollable displays, UTG is becoming indispensable due to its superior mechanical, optical, and tactile properties.

Leading manufacturers-most notably Corning-have explicitly stated that glass will remain the “key component of the ultimate cover solution” for foldable devices. This position is grounded in consumer expectations for scratch resistance, hardness, optical clarity, and durability, all of which remain inherent advantages of glass over plastic-based alternatives.

Commercial adoption validates the trend: numerous flagship foldable smartphones have already transitioned to UTG, driven by the need to eliminate CPI’s historical weaknesses such as creasing, surface micro-scratches, and reduced optical quality. UTG-based displays today undergo durability testing up to 200,000 folds, demonstrating the material’s ability to endure repetitive mechanical stress without thermal or optical degradation.

While UTG is still more delicate than the high-hardness cover glass used in flat smartphones, it offers a far superior experience compared to early polymer-based solutions. Its thinness (often 30–100 μm) enables the necessary bend radius for foldable form factors while maintaining the premium feel expected in flagship devices.

Trend 2 - Flexible Glass Gains Qualification as the Gold-Standard Encapsulation Barrier for High-Efficiency Flexible Photovoltaics

Flexible photovoltaics-particularly perovskite solar cells (PSCs)-require hermetic encapsulation to ensure long-term operational stability. Polymer barrier films have struggled to meet the stringent moisture and oxygen protection required, driving the qualification of flexible glass as the industry’s highest-performance encapsulation layer.

Flexible glass delivers a near-zero Water Vapor Transmission Rate (WVTR), typically below 1 × 10⁻⁶ g·m⁻²·day⁻¹, a level that plastic films cannot reliably achieve. This impermeability is essential for protecting perovskite absorbers, which degrade rapidly in the presence of moisture and oxygen.

Studies linking barrier performance with device degradation show exponential benefits: as WVTR decreases from 10¹ to 10⁻⁴ g·m⁻²·day⁻¹, perovskite cell degradation rates drop sharply. With flexible glass encapsulation, PSCs have demonstrated 77% efficiency retention after 840 hours, highlighting its role in enabling long-lifespan flexible PV products.

Flexible glass also unlocks significant weight reductions in Building-Integrated Photovoltaics (BIPV) and Vehicle-Integrated Photovoltaics (VIPV) by replacing heavy rear glass while retaining a durable protective front layer. This weight advantage substantially improves structural design flexibility, installation efficiency, and system performance in next-generation PV applications.

Opportunity 1 - Flexible Glass as a Biocompatible, Hermetic Substrate for Implantable & Wearable Bioelectronics

The medical device industry is emerging as a major future growth frontier for flexible glass, driven by its unique ability to combine biocompatibility, hermeticity, and flexibility-attributes essential for chronic implantable systems.

Implantable bioelectronics such as neurostimulators, electrophysiology sensors, pacemakers, and organ-monitoring platforms require encapsulation materials that can withstand long-term exposure to corrosive biofluids without leaching toxins or compromising device integrity. Flexible glass provides superior hermetic sealing compared to polymer substrates like PI or PDMS, making it a leading candidate for next-generation biomedical electronics.

Glass also provides excellent biocompatibility, eliciting minimal immune response-an essential requirement for chronic implants. As researchers develop ultra-thin formats (<100 μm), flexible glass increasingly matches the conformance needs of soft tissues and curved anatomical structures.

Applications include:

- Neural interfaces requiring stable electrical insulation

- Wearable skin electronics needing moisture-resistant substrates

- Cardiac and organ-integrated sensors demanding long-term operational durability

Flexible glass’s mechanical stability, chemical inertness, and optical transparency (for optogenetic and imaging-based tools) create strong commercial potential for the emerging implantable electronics market.

Opportunity 2 - Flexible Glass as a Hermetic Barrier for Thin-Film Solid-State Batteries & Roll-to-Roll Energy Storage Manufacturing

Flexible glass is positioned to become a key enabler of high-performance thin-film solid-state batteries (SSBs) that rely on sensitive lithium metal anodes and oxygen-intolerant solid electrolytes. These systems require encapsulation barriers with ultra-low permeability and high thermal stability, making flexible glass uniquely suited to next-generation battery production.

The industry’s shift to roll-to-roll manufacturing for electrodes, separators, and full battery stacks demands flexible substrates that can withstand continuous processing. Flexible glass meets this requirement, enabling scalable, cost-efficient fabrication while maintaining hermeticity and mechanical durability.

Lithium metal anodes-the foundation of high-energy SSBs-must be protected from trace moisture and oxygen exposure, conditions that easily destabilize polymer-based barriers. Flexible glass provides a stable, inert, and impermeable environment necessary to achieve long cycle life and prevent dendritic reactions.

A major differentiator is flexible glass’s compatibility with high-temperature deposition processes. Manufacturing of thin-film solid-state components such as LiPON often requires temperatures approaching 1200°C, which polymer substrates cannot tolerate. Flexible glass substrates under qualification can withstand these extreme conditions, enabling next-generation battery chemistries that demand high-temperature processing.

This capability positions flexible glass as a foundational material for advanced SSB architectures supporting mobile devices, electric vehicles, aerospace systems, and grid-scale microbatteries.

Flexible Glass Market Share Analysis

Market Share by Product Type: Ultra-Thin Glass Dominates Through Superior Flexibility, Optical Performance, and Mechanical Reliability

Ultra-Thin Glass (UTG) holds the leading 52% share in the Flexible Glass Market, driven by its unmatched ability to deliver mechanical flexibility, high optical clarity, and exceptional surface durability—performance attributes that are indispensable for next-generation foldable and rollable electronic devices. The extreme thinness of UTG—typically 30 to 100 μm, even thinner than a human hair—enables bending radii as tight as 1.4 to 3 mm, a level of flexibility unattainable with thicker strengthened glass or polymer substitutes. This mechanical behavior is critical for enabling smooth folding actions without inducing surface cracking or optical distortion in devices like foldable smartphones, ultra-portable tablets, and advanced wearable displays. UTG’s dominance is further reinforced by its chemical strengthening via ion exchange and lamination processes, which allow it to endure 200,000 to over 1.5 million folding cycles, meeting the durability standards demanded by global consumer electronics OEMs. This combination of resilience, transparency, and scratch resistance positions UTG as the only commercially viable material that satisfies both the aesthetic and functional requirements of premium foldable device architectures. As major device manufacturers continue investing heavily in flexible OLED/AMOLED display roadmaps, UTG’s unique performance advantages secure its position as the market’s fastest-growing and highest-share product category.

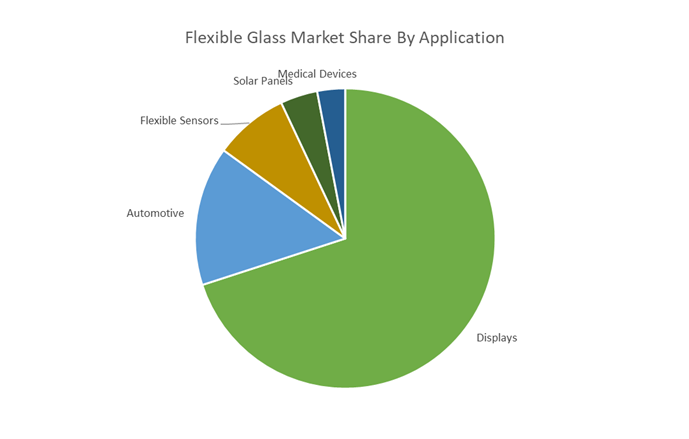

Market Share by Application: Displays Lead the Market Through High-Volume Device Production and Premium Material Requirements

Displays dominate the Flexible Glass Market with a commanding 70% share, reflecting the explosive demand for high-performance OLED, AMOLED, and next-generation flexible display technologies in consumer electronics. Flexible glass plays a mission-critical role in this segment due to its superior barrier properties, offering far better moisture and oxygen protection than polymer films—an essential requirement for maintaining the longevity and efficiency of oxygen-sensitive OLED materials. Its high surface hardness, often reaching up to 9H, delivers the scratch resistance expected in premium smartphones and tablets, where daily handling, abrasion exposure, and long-term durability are central purchasing criteria. The optical clarity of flexible glass, exceeding 90% light transmittance, ensures brightness accuracy, color fidelity, and low visual distortion, making it the preferred choice for high-end display stacks where user experience is tightly linked to visual performance.

Because smartphones, tablets, wearables, and emerging foldable/rollable devices constitute billions of units in annual production, the sheer scale of this industry amplifies demand for flexible glass solutions far beyond that of niche applications like sensors, solar modules, or automotive interiors. As global OEMs accelerate innovation in flexible displays—targeting slimmer device profiles, larger foldable screens, and improved cover window durability—the strategic importance of flexible glass continues to rise. These factors collectively solidify the Displays segment as the dominant application area driving sustained long-term growth in the Flexible Glass Market.

Country Analysis: Global Flexible Glass Development Hubs

South Korea: First-Mover Leadership in Foldable OLED Devices and Ultra-Thin Glass (UTG) Commercialization

South Korea continues to dominate the global Ultra-Thin Glass (UTG) ecosystem, supported by its unparalleled leadership in OLED display manufacturing and commercial-scale deployment of foldable smartphones. Flagship device makers—most notably Samsung—shape worldwide UTG demand by specifying chemically strengthened ultra-thin cover glass for premium foldable product lines such as the Galaxy Z Fold and Galaxy Z Flip series. This first-mover advantage has positioned South Korea as the epicenter of UTG integration, influencing global performance benchmarks for flexibility, scratch resistance, fold durability, and long-term optical clarity.

Collaborative manufacturing partnerships further reinforce this dominance. South Korean display companies maintain tight supply-chain alignment with global UTG innovators like SCHOTT and Corning, ensuring a consistent supply of high-purity, strengthenable UTG sheets capable of supporting mass-production folding mechanics. R&D priorities currently focus on reducing fold-crease visibility, improving mechanical resilience, increasing surface hardness, and expanding rollable OLED applications, including concept-stage rollable televisions that require flexible glass substrates and foldable cover layers. With ongoing supplier advances in crease optimization and durability enhancement, South Korea will remain the global anchor market for next-generation foldable, rollable, and hybrid display architectures.

United States: Material Science Breakthroughs and Fusion Draw Dominance in Ultra-Thin Flexible Glass

The United States leads the global flexible glass market from the materials science side, driven by pioneering research and manufacturing depth in fusion draw ultra-thin glass technologies. Corning Incorporated, one of the industry’s most influential innovators, continues to set global standards through its proprietary fusion draw process, which produces virtually defect-free flexible glass—including Corning® Willow® Glass—in thicknesses as low as 100–200 micrometers. This ultra-smooth, pristine surface profile is essential for advanced electronics applications such as foldable displays, wearable devices, and emerging sensor architectures.

Corning’s long-range investment strategy further elevates U.S. leadership. The company’s Springboard 2025 expansion plan aims to generate an additional $4 billion in annualized sales by 2026, a substantial portion tied to innovations in specialty materials, including flexible glass substrates and cover sheets. Beyond consumer electronics, the U.S. is actively opening new markets for flexible glass through its 2025 Solar Market-Access Platform, expected to reach $2.5 billion by 2028. This initiative accelerates the adoption of flexible glass in thin-film solar cells, providing high durability, chemical resistance, and superior thermal stability for next-generation photovoltaic systems. In parallel, automotive manufacturers in the U.S. are scaling the integration of flexible glass for curved cockpit displays, panoramic interfaces, and lightweight interior digital dashboards, reflecting a broader industry shift toward seamless, glass-centric vehicle UX design.

Germany / European Union: UTG Production Excellence and Precision Down-Draw Technology for High-Reliability Applications

Germany and the broader EU remain critical contributors to the global flexible glass market through their mastery of precision ultra-thin glass production, particularly for high-reliability applications in consumer electronics, medical devices, and wearables. SCHOTT AG, a world-renowned specialty glass manufacturer, solidified its leadership with the 2025 launch of Xensation® Flex, a UTG product capable of achieving bending radii below 2 mm once processed—making it one of the most flexible and durable UTG materials available today. This advancement places SCHOTT at the center of next-generation foldable and rollable device design, directly supplying premium UTG for several top-tier smartphone manufacturers.

SCHOTT’s competitive advantage is further reinforced by its down-draw production technology, which allows ultra-thin glass to be pulled directly from the melt without the need for acid etching, resulting in a more sustainable and environmentally efficient manufacturing process. The company’s UTG has already been integrated into commercial products such as vivo’s X Flip and X Fold 2, with TÜV Rheinland certifying over 500,000 folds, demonstrating real-world durability and market readiness. Europe’s technical focus extends beyond consumer electronics: manufacturers are heavily targeting flexible medical devices, advanced wearables, and high-performance sensor systems, where flexible glass requires superior chemical resistance, optical stability, and precise electrical compatibility. The EU thus remains a technological stronghold for ultra-thin glass engineered for long-term reliability.

China: High-Volume Display Manufacturing and Rapid Expansion of Domestic Ultra-Flexible Glass (UFG) Ecosystems

China has evolved into one of the largest and fastest-growing markets for flexible and ultra-thin glass, driven by its massive consumer electronics manufacturing ecosystem and state-backed industrial incentives. Major display giants such as BOE Technology Group are leading global consumption of flexible substrates for foldable smartphones, OLED laptops, automotive displays, and emerging large-format foldable devices. China’s push into Ultra-Flexible Glass (UFG) is reinforced by an expanding portfolio of foldable devices—such as the Honor Magic V Flip and several 17.3-inch foldable notebook prototypes—demonstrating rapid application diversification and rising demand for robust UTG and hybrid-glass materials.

Manufacturing scale is one of China’s greatest advantages. As the Asia-Pacific region represents the world’s largest glass production base, China benefits from a deeply integrated supply chain capable of supporting complex roll-to-roll flexible glass production, lowering costs and accelerating commercialization cycles. Government-backed industrial policies continue to encourage domestic sourcing and technology localization, reducing dependence on imported UTG while strengthening China’s competitiveness in global display supply chains. With expansive production capacity and fast-paced innovation across smartphones, IT devices, and automotive displays, China is emerging as a powerful growth engine in the flexible glass market.

Competitive Landscape: Global UTG and Flexible Glass Suppliers Expand Thin Glass Portfolios, Semiconductor-Grade Precision, and 3D Forming Capabilities

The competitive environment in the Flexible Glass Market is shaped by material science leaders specializing in ultra-thin glass, glass-ceramics, structured substrates, high-strength cover glass, semiconductor packaging glass, and flexible display laminates. Companies are competing on thickness reduction, bend strength, purity, surface smoothness, coating integration, and large-area flexibility, while also scaling production for mass-market electronics and automotive applications.

Corning leads the market in ultra-thin glass (UTG) with its flagship Gorilla® Glass and Willow® Glass platforms, engineered for foldable displays, sensors, and cover windows. Its proprietary Fusion-forming process produces pristine, highly uniform glass substrates under 100 μm, essential for TFT backplanes and AMOLED technologies. In March 2025, Corning expanded its portfolio with Gorilla® Glass Ceramic, delivering exceptional drop durability for mobile devices. The company’s Q3 2025 earnings confirmed accelerating adoption of UTG for mass-produced foldable smartphones, solidifying Corning as the preferred supplier for next-gen flexible electronics.

SCHOTT AG provides advanced UTG and thin glass-ceramic solutions through its AS 87 eco and FLEXINITY® series targeted at display, semiconductor, and industrial sectors. Its September 2025 FLEXINITY® launch, featuring structured wafers with TTV <1 μm, positions SCHOTT as a critical supplier to 3D IC and FO-WLP manufacturing. SCHOTT’s expertise in hermetic, thermally stable compositions makes its glass substrates ideal for OLED encapsulation, optical sensors, and microdevices requiring high-temperature processing and perfect barrier properties.

AGC is a major innovator in chemically strengthened flexible glass, offering UTG solutions for both electronics and automotive interiors. In December 2025, AGC achieved a milestone by introducing 3D curved UTG for cockpit displays, enabling lightweight, seamless integrated dashboards. Its investment in FINEO vacuum insulating glass (January 2025) further demonstrates AGC’s strategic push into ultra-thin, lightweight architectural glazing. AGC’s capabilities in low-carbon glass manufacturing and complex forming processes position it strongly in automotive, IT hardware, and energy-efficient building applications.

NEG specializes in thin glass substrates, including its high-precision G-Leaf UTG, engineered for flexible AMOLED and high-resolution display backplanes. With extensive investments in continuous thin glass production lines to serve Asia-Pacific panel makers, NEG delivers UTG with minimal defects, excellent surface smoothness, and precise dimensional accuracy. These attributes are essential for lithography alignment and uniform deposition of display layers in foldable and rollable consumer devices.

Sumitomo Chemical plays a key role in the flexible display supply chain by providing polarizers, flexible cover windows, touch sensor stacks, and UTG lamination solutions. Its portfolio focuses on the integration of functional films and circuitry directly onto UTG surfaces prior to chemical strengthening, ensuring high optical clarity, durability, and foldability. Sumitomo supports leading OEMs in developing complete cover window assemblies for foldable smartphones and larger rollable displays.

Flexible Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.2 Billion

|

|

Market Size (2035)

|

$4.1 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Product Type/Composition (Ultra-Thin Glass, Flexible Glass-Ceramics, Aluminosilicate Glass, Borosilicate Glass, Phosphate Glass), By Film Thickness (<50 µm, 50–100 µm, ≥100 µm), By Manufacturing Process (Fusion Draw Process, Down-Draw Process, Roll-to-Roll Process), By Application (Displays, Automotive, Flexible Sensors, Solar Panels, Medical Devices)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Corning Incorporated, SCHOTT AG, AGC Inc., Nippon Electric Glass Co. Ltd., Saint-Gobain S.A., LG Display Co. Ltd., Samsung Display Co. Ltd., BOE Technology Group Co. Ltd., Universal Display Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Glass Market Segmentation

By Product Type / Composition

- Ultra-Thin Glass (UTG)

- Flexible Glass-Ceramics

- Aluminosilicate Glass

- Borosilicate Glass

- Phosphate Glass

By Film Thickness

- < 50 Micrometers

- 50–100 Micrometers

- 100 Micrometers

By Manufacturing Process

- Fusion Draw Process

- Down-Draw Process

- Roll-to-Roll Process

By Application

- Displays (foldable OLEDs, rollable TVs, wearable displays)

- Automotive (curved infotainment displays, HUD windshields)

- Flexible Sensors

- Solar Panels

- Medical Devices

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Flexible Glass Market

- Corning Incorporated

- SCHOTT AG

- AGC Inc.

- Nippon Electric Glass Co. Ltd. (NEG)

- Saint-Gobain S.A.

- LG Display Co., Ltd.

- Samsung Display Co. Ltd.

- BOE Technology Group Co. Ltd.

- Universal Display Corporation

*- List not Exhaustive