Furan Resins Market to Reach $37.6 Billion by 2034 at 6.7% CAGR Driven by Foundry Innovation and Bio-Based Feedstocks

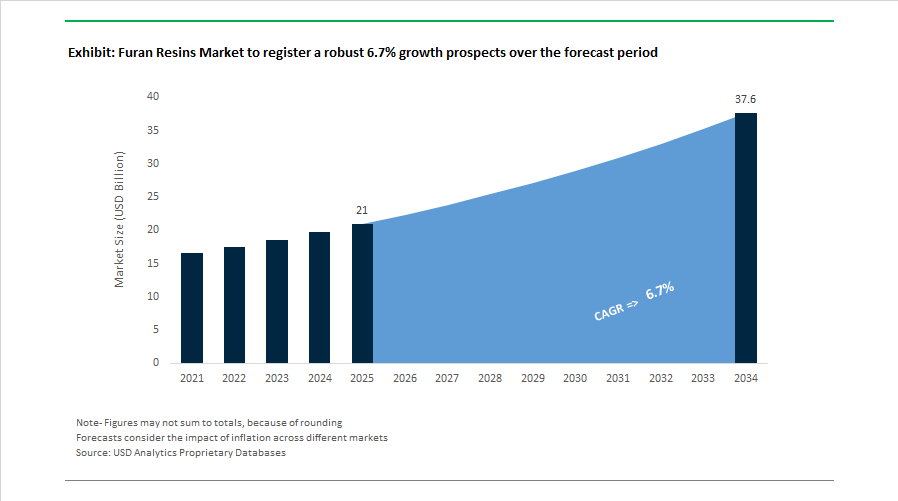

The Furan Resins Market is projected to expand from $21 billion in 2025 to $37.6 billion by 2034, registering a CAGR of 6.7% over the forecast period. Market growth is strongly anchored in steel and iron foundry applications, large-scale sand casting for automotive lightweighting, corrosion-resistant mortars, oilfield sand consolidation, and high-performance adhesives. Structural demand is accelerating as automotive OEMs adopt mega casting architectures for electric vehicles, while aerospace and energy sectors require low-defect casting materials compatible with nickel-based superalloys and high-chrome iron components.

In January 2026, Hüttenes-Albertus Group was formally recognized as a global market leader in specialty chemicals for the foundry industry following its 2025 recertification and strategic emphasis on Mega Sand Casting for automotive engineering. In July 2025, Hüttenes-Albertus partnered with Laempe Mössner Sinto to demonstrate large-format aluminum structural components for EV platforms using advanced furan resin binders. This shift toward single-piece castings reduces assembly complexity and improves structural rigidity, directly reinforcing high-performance binder consumption. In June 2025, HA Korea broke ground on a new Miryang production facility to localize output in Asia-Pacific, the largest consumption hub for furan resin systems in automotive and industrial machinery manufacturing.

Environmental compliance and emission reduction are reshaping binder chemistry. In a joint initiative concluded in early 2026, SI Group South Africa and Hüttenes-Albertus introduced a nitrogen-free hybrid furan resin system designed to reduce sulfur emissions and casting fumes in steel and iron foundries. Throughout 2025, ASK Chemicals and Chang Chun Group launched low-nitrogen resin grades engineered to minimize gas-related casting defects in aerospace and wind energy components. In January 2025, multiple patents including WO2025000788A1 and WO2025020679A1 were filed for novel furfural production methods using covalent organic frameworks and double-acid catalysts, aiming to improve biomass conversion efficiency and reduce process energy intensity. These innovations signal a transition toward low-emission foundry binders and energy-efficient furfuryl alcohol synthesis pathways.

Bio-based feedstock integration is becoming a structural theme across the value chain. In January 2024, the Hüttenes-Albertus Group released its Sustainability Insights progress report outlining its transition toward 100% bio-based feedstocks derived from non-food agricultural waste, aligning with the EU Together for Sustainability framework. In March 2025, BASF SE expanded fermentation-based molecule production through its Isobionics unit, reinforcing a broader industry pivot toward biotech-derived intermediates. This development has influenced furan resin producers to evaluate microbial fermentation routes for furfuryl alcohol to reduce reliance on conventional thermal extraction from biomass. In April 2024, Perfex Chemical Solution LLC acquired DynaChem Solutions, integrating the FURALLOY® brand into its industrial resin portfolio and strengthening its presence in down-well sand consolidation and chemical-resistant construction materials.

Additive manufacturing and digitalization are introducing new performance benchmarks. In April 2025, Vesuvius plc partnered with voxeljet AG to optimize furan-based binders for high-speed 3D sand printing, enhancing mold complexity, curing efficiency, and takeout properties. By mid-2025, leading manufacturers implemented AI-driven digital monitoring systems to control curing kinetics and formulation consistency in real time, reducing material waste in construction-grade adhesives and industrial sealants. These process optimization strategies are elevating production precision and reinforcing quality assurance in high-value casting applications.

The Furan Resins Market outlook reflects convergence of mega casting adoption in EV manufacturing, low-nitrogen emission standards, biomass-based furfural innovation, digital process control, and additive manufacturing integration. Competitive advantage is increasingly defined by environmental compliance, feedstock security, regional capacity expansion in Asia-Pacific, and application-specific binder engineering for high-integrity cast components.

Trends and Opportunities in the Global Furan Resins Market

Consolidation and Strategic Focus on High-Performance Industrial Binders

Furan resins are being deliberately ring-fenced for applications where their thermal stability, low ash content, and resistance to aggressive chemical environments deliver a non-substitutable advantage over phenolic, epoxy, and vinyl ester systems. This trend is driving consolidation around specialized grades rather than volume expansion into low-margin uses.

A key catalyst has been the foundry sector’s shift toward low-emission, high-strength binder systems. Through deployments continuing into 2024–2025, ASK Chemicals advanced its MAGNASET 2.0 technology, which reduces free furfuryl alcohol content to below 25% by weight. This directly addresses toxicological classification challenges while improving core performance. Foundries adopting these systems have reported approximately 15% higher core strength and materially lower gas-related casting defects, supporting higher casting yields and reduced scrap rates in iron and steel production.

Beyond foundries, furan resins are gaining specification preference in chemically aggressive industrial environments. By early 2025, furan-based mortars and linings were increasingly selected for phosphoric acid, fertilizer, and chemical processing plants. Their ability to withstand pH extremes from 0 to 12 and sustained operating temperatures approaching 190°C positions them as a superior alternative to epoxy and vinyl ester systems, which often suffer premature failure under combined thermal and acidic stress. This durability directly reduces maintenance downtime and lifecycle costs, reinforcing the strategic value of furan binders in heavy industry.

Strategic Substitution of Phenolic Resins in Eco-Conscious Composites

Global regulatory pressure to eliminate formaldehyde emissions is accelerating the substitution of phenol-formaldehyde resins with bio-sourced furan systems, particularly in wood products and friction materials. Compliance with EU 2025/351 and TSCA Title VI standards is no longer optional, making formaldehyde-free chemistry a structural requirement rather than a sustainability premium.

Research published in December 2025 demonstrated that replacing phenolic binders with 30 to 45% bio-based furan resins derived from agricultural residues such as corncobs and bagasse preserves plywood dimensional stability while reducing formaldehyde emissions by up to 40%. This finding is driving renewed interest from engineered wood manufacturers seeking to maintain mechanical performance while aligning with green building certification frameworks.

In automotive friction materials, Tier-1 suppliers began piloting furan-modified binders in heavy-duty brake pads during late 2025. These systems exhibited improved fade resistance and a more stable coefficient of friction at elevated temperatures compared with traditional phenolics. Importantly, they also align with OEM sustainability roadmaps and REACH compliance targets, positioning furan resins as a viable long-term binder solution in safety-critical automotive components.

Critical Role in Carbon–Carbon and Aerospace Composites

One of the highest-margin growth avenues for furan resins lies in carbon–carbon and carbon–ceramic composite manufacturing, where furan chemistry serves as an optimal carbon precursor. As defense and aerospace programs accelerate, demand for ultra-high-temperature materials is expanding rapidly.

With U.S. and European defense sales exceeding $950 billion in 2024 and continuing to rise through 2025, production of rocket nozzles, hypersonic leading edges, and missile components has intensified. Furan resins are favored in these applications due to their high char yield of approximately 50 to 55%, enabling the formation of dense, high-purity carbon matrices that outperform many petroleum-based polymers during carbonization.

Semiconductor manufacturing represents an adjacent opportunity. As fabrication nodes advance toward 3 nm and below in 2025–2026, demand is rising for ultra-clean carbon–silicon carbide wafer carriers capable of operating in high-temperature vacuum environments. Furan resins engineered with metallic impurity levels below 5 ppm are being developed as binders for these carriers, ensuring zero contamination risk during advanced deposition processes.

Development of Fully Bio-Based Thermosets and Furan–Epoxy Hybrids

The furan resins market is also benefiting from a shift beyond basic bio-content toward molecularly engineered, fully renewable thermoset platforms. This evolution is creating new opportunities in electronics, additive manufacturing, and advanced coatings.

A landmark study published in December 2025 reported the successful development of a phosphorus-free, bio-based epoxy resin built on furan chemistry. The material achieved tensile strength of approximately 74 MPa and a tensile modulus nearing 5.9 GPa, matching or exceeding conventional bisphenol-A epoxies while delivering inherent flame retardancy. This positions furan–epoxy hybrids as credible BPA-free alternatives in applications facing tightening chemical scrutiny.

In parallel, the expansion of the bio-based epoxy market, approaching $4 billion by 2025, is opening a niche for furan-derived reactive diluents. These components are increasingly used to control viscosity in high-speed SLA and DLP 3D printing resins, ensuring processability without sacrificing the thermal rigidity required for under-the-hood automotive electronics and power modules. For furan resin producers, this represents a strategic entry point into digitally enabled manufacturing and advanced electronics supply chains.

Furan Resins Market Share and Segmentation Insights

Furfuryl Alcohol Resin Leads Bio-Based Foundry Binder Technologies

Furfuryl Alcohol Resin accounted for 68.40% of the Furan Resins Market share in 2025, making it the dominant resin type used in industrial casting and specialty resin applications. This resin is primarily used as a binder in foundry sand mold and core production, where it provides critical performance characteristics including high thermal stability, excellent dimensional accuracy, strong bonding strength, and controlled collapsibility after metal casting. These properties allow foundries to produce complex metal components with precise shapes and minimal casting defects. A significant advantage of furfuryl alcohol resin is its bio-based origin, as the primary raw material—furfuryl alcohol is derived from agricultural residues such as corncobs, rice hulls, and sugarcane bagasse, making it an important renewable material within the industrial resin sector. In 2025, the supply chain for furfuryl alcohol has become a strategic focus for resin manufacturers due to rising demand for sustainable bio-based chemicals. Producers have invested in diversified biomass feedstock sourcing and improved catalytic conversion technologies to maintain stable furfuryl alcohol production despite seasonal variability in agricultural residue availability. These innovations strengthen the reliability and scalability of bio-based resin supply within the global furan resins market.

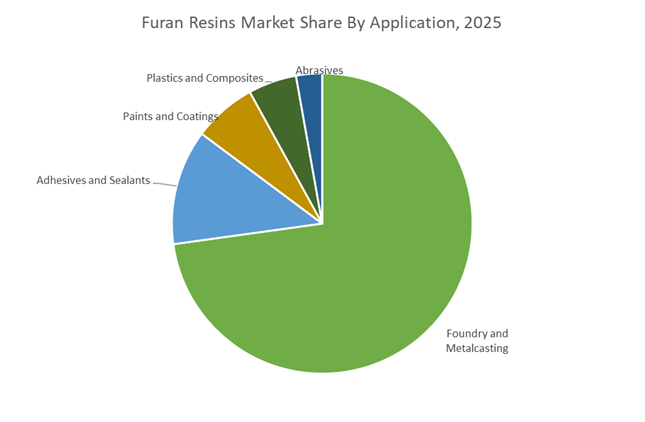

Foundry and Metalcasting Industry Drives the Majority of Global Furan Resin Consumption

Foundry and Metalcasting represented 72.80% of the Furan Resins Market share in 2025, making it the largest application segment for furan-based resin systems. Furan resins are widely used as sand binders in metal casting operations, where they enable the production of strong and precise molds used to manufacture metal components across industries such as automotive, industrial machinery, construction equipment, and heavy engineering. The chemical structure of furan binders allows them to withstand extreme temperatures encountered during molten metal pouring, while still providing sufficient mold collapsibility for efficient casting removal and finishing. Automotive manufacturing is a particularly important demand driver, as foundries use furan resin binders to produce engine blocks, cylinder heads, transmission housings, and other complex cast components. In 2025, the foundry sector is increasingly influenced by the automotive industry’s push toward vehicle lightweighting and improved fuel efficiency. To meet these requirements, manufacturers are designing thinner-walled and more geometrically complex metal castings, which require binder systems capable of delivering higher mold strength, lower gas generation during casting, and faster curing cycles.

Competitive Landscape in Furan Resins Market

ASK Chemicals Advances Low-Emission and Low-FA Furan Binder Systems

ASK Chemicals GmbH remains a global leader in high-performance foundry binder systems, focusing on environmental health and safety optimization in furan resin technology. In 2025 and 2026, the company scaled its MAGNASET 2.0 platform, a second-generation furan resin engineered to maintain high reactivity while reducing free furfuryl alcohol content below 40%, addressing tightening workplace exposure regulations. Its BLUE platform, including ECOCURE BLUE, is designed to cut BTX and VOC emissions by up to 50% during casting, improving air quality in foundries. ASK Chemicals is prioritizing label-free or milder classification binders to eliminate severe hazard labeling and enhance occupational safety. The ASKURAN portfolio, including furan-resol hybrid systems, delivers extreme thermal stability for steel and iron casting applications requiring structural integrity under high thermal loads.

Hüttenes-Albertus Expands Low-Sulfur and Inorganic Binder Development

Hüttenes-Albertus continues to hold a strong position in the European and North American foundry binder markets, particularly through its HA-International joint venture operations. Throughout 2025, the company expanded R&D facilities in Germany and India to advance inorganic binder systems while leveraging deep expertise in furan resin chemistry. In early 2026, HA introduced low-sulfur furan resins designed to prevent spherical graphite defects in ductile iron castings, a critical quality parameter for automotive engine blocks and drivetrain components. The company is transitioning toward biomass-to-chemical pathways, sourcing agricultural residues to reduce fossil dependency in resin production. HA’s furan binder systems are engineered for high-temperature resistance exceeding 1,400°C, reinforcing its relevance in heavy-duty iron and steel foundries.

Hongye Chemical Strengthens Vertical Integration in Furfuryl Alcohol Supply

Hongye Chemical is one of the largest vertically integrated producers of furan-based chemicals, controlling significant global furfuryl alcohol capacity. As of 2025 and 2026, the company holds approximately 17% of global furan resin market volume, supported by large-scale domestic production in China. Under the China Green 2030 initiative, Hongye invested in automated closed-loop distillation systems to lower carbon intensity and improve energy efficiency in resin synthesis. Its product portfolio includes furfuryl alcohol resins and furfural resins widely used in paints, plastics, adhesives, and foundry applications across Asia. Hongye is expanding exports into Southeast Asia and the Middle East, regions experiencing rapid growth in metal casting and infrastructure development.

Pennakem Focuses on Bio-Based Furan Building Blocks and Composites

Pennakem, part of the Minasolve and Biolandes Group, is a leading North American supplier of bio-based furanic building blocks and specialty resins. In 2025, the company sales are driven by renewable feedstock utilization such as corn cobs and oat hulls. Its Renewable Specialization strategy aligns with Safe and Sustainable by Design principles, positioning Pennakem as a key supplier of bio-based furfuryl alcohol resins. In early 2026, the company increased production of high-purity furfuryl alcohol resins for advanced composite materials used in aerospace and automotive lightweighting applications. Its eco-friendly binder portfolio offers sustainable alternatives to petroleum-derived phenolic resins while maintaining corrosion resistance and high mechanical performance.

Kao Enhances Precision Casting Performance Through AI and Molecular Engineering

Kao Corporation’s Chemical Division applies advanced materials science to high-precision furan binder systems used in precision casting. In January 2026, Kao integrated AI-driven logistics and supply chain optimization across its chemical operations, improving global delivery speed and reducing fixed costs. Under its K27 Mid-term Plan, the company prioritizes Global Sharp Top products, including fast-curing furan resins with enhanced mold dimensional stability and improved sand adhesion. Kao has significantly expanded its European distribution network to accelerate international growth, targeting 50% of brand sales outside Japan by 2027. Its molecular engineering capabilities enable ultra-low-odor furan resins with superior bonding strength, supporting high-quality castings in automotive, industrial machinery, and precision component manufacturing.

China: Biomass Integration and High-Heat Specialty Pivot

China continues to anchor the global furan resins market through vertically integrated biomass processing and rapid diversification into specialty applications. In its 2025 mid-year disclosure, Jinan Shengquan Group reaffirmed its leadership in global furan resin capacity, underpinned by a fully integrated biomass-to-chemical chain that converts agricultural residues into furfuryl alcohol at scale. This integration supports a substantial share of global foundry resin demand and insulates domestic producers from feedstock volatility.

Product evolution is accelerating alongside regulatory pressure. Under the 2025–2026 green chemical work plan issued by the Ministry of Industry and Information Technology, foundries are required to reduce VOC emissions by 15%, prompting a shift from phenolic systems toward low free furfuryl alcohol furan resins. At the same time, Shengquan’s move into electronic-grade materials reflects China’s AI infrastructure buildout. Its proprietary polyphenylene ether resin, often paired with furan chemistries for thermal stability, achieved certification with domestic telecom OEMs ahead of 2026. Downstream diversification is also evident with the February 2025 commissioning of a 1,000-ton-per-year porous carbon line derived from furan precursors, targeting sodium-ion battery anodes.

United States: Trade Realignment and Bio-Based Modernization

The U.S. furan resins market is undergoing structural adjustment driven by tariffs, emissions policy, and operational upgrades. Tariff measures implemented in early 2025 on Chinese chemical intermediates, including furfural, raised input costs and accelerated a domestic-first sourcing strategy among North American foundries. This shift has increased demand for regional suppliers such as Ashland and Hexion, particularly for corrosion-resistant furan coatings used in oil and gas and heavy industrial castings.

Operational resilience is improving. Ashland initiated a USD 60 million network optimization program in mid-2025, upgrading specialty resin and additive lines to improve margin stability. Following a September 2025 outage, its Calvert City unit completed equipment replacement to enable processing of advanced bio-based intermediates. Regulatory signals are also shaping formulation choice. New EPA metalcasting emission guidelines introduced in late 2025 favor high-thermal-stability furan binders that minimize gas evolution and dimensional defects during high-temperature pours, reinforcing furan systems as compliant alternatives.

Germany: Green Deal Compliance and Safer Foundry Chemistries

Germany’s furan resins market is aligned tightly with European decarbonization and worker safety mandates. As automotive supply chains serving OEMs such as Volkswagen and BMW adapt to the European Green Deal, foundries are modernizing with bio-based furan resins that deliver lower lifecycle emissions than petroleum-derived binders. These materials are increasingly specified in high-precision castings where sustainability credentials are audited at supplier level.

Technology upgrades are reinforcing adoption. ASK Chemicals rolled out its MAGNASET 2.0 furan resin platform through 2024–2025, featuring free furfuryl alcohol content below 40%. This materially improves environmental classification and workplace exposure profiles. In parallel, BASF integrated bio-based furan-derived additives into its 2025–2026 automotive coatings initiatives, enhancing chemical resistance and surface durability in premium finishes.

India: Lightweight Casting Demand and Feedstock Localization

India’s furan resins market is expanding on the back of tighter emission standards and bio-economy policy support. As Bharat Stage VI enforcement deepens through 2026, demand for lightweight aluminum and magnesium castings has intensified. Indian foundries are increasingly selecting furan resins for high-precision sand casting of complex engine and transmission components, where dimensional accuracy and surface finish are critical.

Supply-side localization is gaining traction. The government’s 2025 bio-economy roadmap incentivized small-scale furfural extraction units using corncobs and sugarcane bagasse, reducing dependence on imported Chinese feedstocks. Downstream innovation is also emerging. Following Sudarshan Chemical’s acquisition of Heubach Group in March 2025, R&D has expanded into functional colorants for furan-based plastics, targeting construction and automotive aesthetics with enhanced durability.

Japan: Digital Process Control and High-Performance Polymers

Japan’s furan resins market is increasingly defined by electronics precision and high-value structural materials. In June 2025, Tokuyama Corporation launched a digital monitoring platform for advanced materials, including resins used in semiconductor CMP slurries. Real-time viscosity and curing data are enabling electronics manufacturers to target yield improvements approaching 10% by 2026.

Portfolio realignment is reinforcing this focus. Mitsubishi Chemical initiated a strategic review in early 2025, redirecting capital toward high-performance furan-based polymers for aerospace and medical devices. These applications prioritize chemical resistance, thermal stability, and long service life, positioning furan chemistries as specialty enablers rather than bulk binders.

Summary: Furan Resins Market Country Drivers

Furan Resins Market County Level Snapshot

|

Country

|

Strategic Focus

|

Market Implication

|

|

China

|

Biomass integration and electronics

|

Scale leadership and specialty diversification

|

|

United States

|

Tariff-driven localization

|

Increased demand for domestic furan binders

|

|

Germany

|

Green Deal and safety compliance

|

Shift to low-FA, bio-based resins

|

|

India

|

Lightweight casting and agri-waste

|

Feedstock localization and foundry growth

|

|

Japan

|

Digital control and high-performance

|

Expansion into electronics and aerospace

|

Furan Resins Market Report Scope

Furan Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21 Billion

|

|

Market Size (2034)

|

$37.6 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Type (Furfuryl Alcohol Resin, Furfural Resin, Bran Ketone Resin, Branone Formaldehyde Resin), By Curing Process (No-Bake, Cold Box Process, Hot Box Process), By Application (Foundry and Metalcasting, Adhesives and Sealants, Paints and Coatings, Plastics and Composites, Abrasives), By End-Use Industry (Automotive and Transportation, Construction and Infrastructure, Aerospace and Defense, Chemicals and Oil and Gas, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Jinan Shengquan Group Shareholding Co., Ltd., Ashland Inc., ASK Chemicals GmbH, Hexion Inc., BASF SE, Huntsman Corporation, Mitsubishi Chemical Group Corporation, DIC Corporation, DynaChem Inc., Illovo Sugar Africa (Pty) Ltd., TransFurans Chemicals bvba, Pennakem, LLC, Hongye Chemical Co., Ltd., Kao Corporation, Sumitomo Bakelite Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Furan Resins Market Segmentation

By Type

- Furfuryl Alcohol Resin

- Furfural Resin

- Bran Ketone Resin

- Branone Formaldehyde Resin

By Curing Process

- No-Bake

- Cold Box Process

- Hot Box Process

By Application

- Foundry and Metalcasting

- Adhesives and Sealants

- Paints and Coatings

- Plastics and Composites

- Abrasives

By End-Use Industry

- Automotive and Transportation

- Construction and Infrastructure

- Aerospace and Defense

- Chemicals and Oil and Gas

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Furan Resins Industry

- Jinan Shengquan Group Shareholding Co., Ltd.

- Ashland Inc.

- ASK Chemicals GmbH

- Hexion Inc.

- BASF SE

- Huntsman Corporation

- Mitsubishi Chemical Group Corporation

- DIC Corporation

- DynaChem Inc.

- Illovo Sugar Africa (Pty) Ltd.

- TransFurans Chemicals bvba

- Pennakem, LLC

- Hongye Chemical Co., Ltd.

- Kao Corporation

- Sumitomo Bakelite Co., Ltd.

*- List not Exhaustive