Gamma Butyrolactone Market to Reach $5.9 Billion by 2034 at 4.1% CAGR Driven by Semiconductor Purity Standards and EV Battery Electrolytes

The Gamma Butyrolactone (GBL) Market is projected to expand from $4.1 billion in 2025 to $5.9 billion by 2034, registering a CAGR of 4.1% over the forecast period. Market growth is supported by rising consumption of high-purity GBL in semiconductor fabrication, lithium-ion battery electrolytes, pharmaceutical intermediates, specialty solvents, and performance coatings. Structural demand is increasingly tied to electronics miniaturization, expansion of electric vehicle manufacturing, and advanced pharmaceutical synthesis where ultra-low impurity levels and controlled solvent properties are critical.

In 2024, Mitsubishi Chemical Group completed a major capacity expansion at its GBL facilities to serve high-purity semiconductor and EV battery applications. The expansion builds on initiatives launched in late 2023 and strengthens supply for battery-grade electrolyte solvents. In 2025, BASF SE confirmed its commitment to maintaining ultra-high purity GBL output with APHA color values below 20, aligning with zero-defect electronics manufacturing standards and pharmaceutical-grade solvent requirements. In early 2026, several Tier-1 battery manufacturers integrated advanced GBL-based electrolyte formulations designed to improve the thermal stability and lifecycle performance of Lithium Iron Phosphate batteries, reinforcing GBL’s role in next-generation energy storage chemistry.

Feedstock economics and pricing volatility shaped 2025 market conditions. In March 2025, Ashland Inc. announced a global price increase for 1,4-Butanediol and derivative solvent products including GBL, citing rising feedstock costs and macroeconomic pressures impacting pharmaceutical and coatings customers. By September 2025, North American GBL price indices rose due to elevated energy and production expenses, while APAC prices softened amid oversupply of 1,4-Butanediol and high Chinese inventories despite sustained lithium battery demand. In November 2025, Mitsubishi Gas Chemical Company signed a long-term agreement for 1 million tons of ultra-low carbon methanol, securing a lower-carbon precursor supply chain for downstream derivatives such as GBL. These developments illustrate increasing integration between methanol sourcing strategies and solvent-grade chemical production.

Regulatory compliance and portfolio restructuring influenced competitive positioning. In June 2025, Thailand implemented stricter hazardous substance regulations covering GBL manufacture and handling, compelling regional producers to upgrade safety protocols and waste treatment systems to maintain operating licenses. In January 2026, LyondellBasell Industries confirmed divestment plans for four European chemical assets under its cash improvement strategy, streamlining exposure to traditional chemical streams while redirecting capital toward circular and lower-carbon technologies. Concurrently, a 2025 breakthrough in polymer science advanced commercial-scale trials of high-molecular-weight poly(γ-butyrolactone), a chemically recyclable polymer that can depolymerize back into pure GBL monomers, strengthening the solvent’s relevance in the circular plastics economy.

Pharmaceutical and specialty derivative expansion added further demand momentum. In August 2025, leading producers ramped up output of α-Acetyl-γ-Butyrolactone, a key intermediate in Vitamin B1 and antipsychotic drug manufacturing. In January 2025, Mitsui Chemicals and Mitsubishi Chemical initiated a joint study to stabilize phenol-related supply chains, reflecting a broader economic security strategy across Asian solvent and resin production networks.

The Gamma Butyrolactone Market outlook reflects high-purity solvent demand in semiconductor fabrication, integration into EV battery electrolytes, feedstock cost sensitivity linked to methanol and BDO supply, regulatory tightening in Southeast Asia, and the emergence of recyclable poly(γ-butyrolactone) materials. Competitive differentiation is increasingly anchored in purity benchmarks, low-carbon precursor sourcing, and downstream integration into electronics, pharmaceuticals, and energy storage applications.

Market Size Outlook, 2021-2034.png)

Gamma Butyrolactone (GBL) Market Trends and Strategic Growth Opportunities

Regulatory Tightening Is Structurally Reshaping the GBL Supply Chain

The global Gamma Butyrolactone market is undergoing a structural transformation as regulatory scrutiny intensifies across major consuming regions. In the United States, Drug Enforcement Administration reaffirmed Gamma Butyrolactone as a List I chemical under the Controlled Substances Act in August 2025, significantly raising compliance thresholds. Mandatory federal registration, enhanced storage security, and transaction-level reporting requirements are steadily excluding small traders and distributors, resulting in market consolidation around Tier-1 chemical manufacturers with integrated compliance frameworks. This shift is effectively de-commoditizing GBL and repositioning it as a controlled specialty chemical rather than a freely traded industrial solvent.

In Europe, the July 2025 amendment to Germany’s New Psychoactive Substances Act further tightened oversight on GBL and 1,4-Butanediol, accelerating the transition toward captive and audited industrial use models. At a global level, the International Narcotics Control Board has expanded mandatory pre-export notification requirements across more than 60 countries, adding administrative complexity and increasing lead times for cross-border trade. Collectively, these measures are reducing spot-market liquidity while favoring long-term contracts, vertically integrated production, and traceable end-use supply chains. For established producers, regulatory consolidation is acting as a competitive moat that improves pricing discipline and margin stability.

Shift Toward Electronic-Grade and Battery-Grade High-Purity GBL

Producers are increasingly pivoting toward high-purity Gamma Butyrolactone grades, particularly those exceeding 99.9% purity, to offset regulatory risk and capture structurally resilient demand. Approximately 35% to 40% of global GBL output is now internally consumed for N-Methyl-2-pyrrolidone synthesis, positioning GBL as a strategic intermediate rather than a standalone commodity. By 2024, combined global GBL and NMP production capacity exceeded 1.2 million metric tons, with capacity additions concentrated in closed-loop systems designed for battery and electronics manufacturing.

In the semiconductor and electronic components sector, GBL has strengthened its position as a high-performance solvent due to its superior solvency and impurity control. European industrial data indicates that electrical capacitance and related electronic applications accounted for more than 77% of regional GBL revenue in 2024, driven by the requirement for ultra-low metallic contamination levels below 10 parts per billion. This trend aligns with rising complexity in integrated circuit manufacturing, where solvent purity directly impacts yield, reliability, and device miniaturization.

Battery Gigafactory Expansion Driving Structural Demand for GBL-Derived Solvents

The electrification of transport is emerging as the single most powerful demand catalyst for Gamma Butyrolactone. GBL remains indispensable in lithium-ion battery manufacturing as the upstream feedstock for NMP, which is used to dissolve polyvinylidene fluoride binders in electrode coating processes. With global electric vehicle sales exceeding 17 million units during 2024 and 2025, NMP now represents nearly 60% of all solvent consumption in battery electrode fabrication, directly anchoring GBL demand to EV production volumes.

In the United States alone, more than 850 battery-related facilities were recorded by late 2024, reflecting a dense and rapidly expanding gigafactory pipeline. This creates a significant opportunity for GBL producers to embed themselves into long-term supply agreements that include on-site solvent recovery and purification systems. Such integration not only lowers operating costs for battery manufacturers but also strengthens supplier lock-in, regulatory compliance, and sustainability performance, making GBL a strategic enabler rather than a transactional input.

Pharmaceutical Synthesis and Sustainable Solvent Innovation Creating High-Margin Niches

Beyond energy storage, Gamma Butyrolactone continues to play a critical role in pharmaceutical synthesis, particularly as a core precursor for racetam-class nootropics and advanced antiviral formulations. Pharmaceutical-grade GBL typically requires 99.9% purity along with USP and Ph. Eur. compliance, creating a high-margin niche supported by aging demographics and rising neurological disorder prevalence. Demand growth in this segment is less cyclical and more regulation-driven, favoring producers with GMP-certified facilities and traceable production systems.

Sustainability is unlocking an additional layer of opportunity. In mid-2025, research breakthroughs demonstrated commercially viable pathways for producing bio-based Gamma Butyrolactone from biomass-derived succinic acid, achieving selectivity levels above 55%. This innovation offers producers a credible route to decouple from petroleum-based 1,4-Butanediol while meeting increasingly stringent sustainability mandates from electronics, pharmaceutical, and consumer goods customers. Parallel to this, GBL adoption as a biodegradable alternative to chlorinated solvents is accelerating within industrial cleaning and specialty formulation markets. Industry adoption of eco-friendly solvent systems rose by approximately 35% in 2025, positioning Gamma Butyrolactone as a compliance-aligned solution with strong solvency performance and low environmental persistence.

Gamma Butyrolactone Market Share and Segmentation Insights

Industrial Grade Gamma Butyrolactone Dominates Large-Volume Chemical Manufacturing Applications

Industrial Grade Gamma Butyrolactone accounted for 72.80% of the Gamma Butyrolactone Market share in 2025, making it the most widely consumed purity category across global chemical manufacturing sectors. Industrial grade GBL is extensively used in agrochemical synthesis, specialty chemical intermediates, industrial solvent formulations, and polymer processing, where standard purity material delivers the required performance at competitive cost. The dominance of industrial grade material reflects the scale of bulk chemical production processes that require reliable solvent systems but do not demand the extreme purity levels associated with electronics manufacturing. These applications include pesticide intermediates, pharmaceutical precursors, and industrial cleaning formulations, all of which rely on GBL’s strong solvency, high boiling point, and chemical stability. In 2025, the market is experiencing growing grade migration pressure driven by high-performance battery manufacturing. Ultra-high purity GBL is increasingly required for lithium-ion battery electrolyte production, where even trace contaminants can impact electrochemical stability and battery safety. This shift has created a two-tier supply structure within the gamma butyrolactone market, with ultra-high purity grades commanding premium pricing and requiring dedicated purification and production lines.

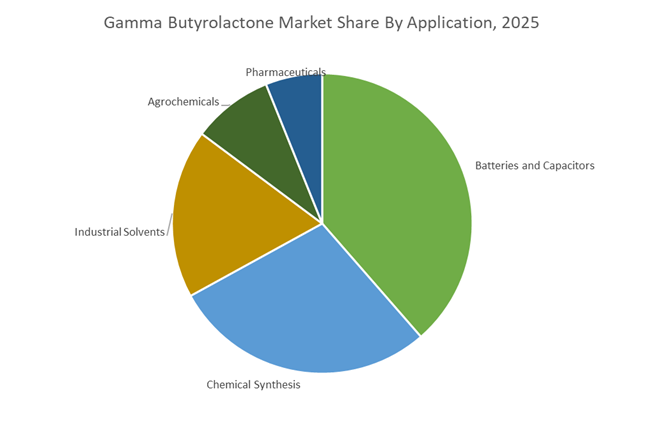

Lithium-Ion Batteries and Capacitors Drive the Largest Consumption of Gamma Butyrolactone Solvents

Batteries and Capacitors represented 38.60% of the Gamma Butyrolactone Market share in 2025, establishing this segment as the leading application for GBL-based solvents. Gamma butyrolactone plays a critical role in lithium-ion battery electrolyte systems, where it functions as a high-performance solvent capable of dissolving lithium salts and enabling efficient ion transport between electrodes. The rapid expansion of electric vehicle battery manufacturing, grid-scale energy storage systems, and consumer electronics batteries has significantly increased global demand for high-quality GBL solvents used in electrolyte formulations. Battery manufacturers rely on GBL because it provides excellent electrochemical stability, high dielectric constant, and compatibility with advanced lithium salt chemistries used in modern battery designs. In 2025, demand growth is increasingly linked to the development of high-voltage lithium-ion batteries designed for higher energy density and longer driving ranges in electric vehicles. These next-generation batteries utilize high-nickel cathode materials and silicon-enhanced anodes, which require electrolytes capable of maintaining stability at elevated voltages and across wide temperature ranges. Specialized GBL-based electrolyte formulations are therefore becoming essential components in advanced battery systems.

Competitive Landscape in Gamma Butyrolactone Market

BASF SE Leads Global Electronic Grade GBL and Integrated Production

BASF SE remains the global leader in the gamma butyrolactone and NMP segments. For fiscal 2026, BASF forecasts EBITDA before special items between €6.2 billion and €7.0 billion, with its Chemicals segment expected to deliver earnings growth supported by solvent and precursor demand. The ramp-up of the Zhanjiang Verbund site in China during late 2025 and early 2026 strengthens BASF’s position in high-growth Asian electronics and lithium-ion battery markets. The company offers a comprehensive portfolio of GBL grades, including ultra-high purity electronic grade material for semiconductor manufacturing and precision cleaning. BASF is targeting 2026 CO2 emissions between 17.2 and 18.2 million metric tons, balancing capacity expansion with process optimization and renewable energy integration across its global GBL production network.

Mitsubishi Chemical Expands Capacity for EV Battery Electrolyte Solvents

Mitsubishi Chemical Group Corporation is the second-largest global gamma butyrolactone producer. In July 2024, the company expanded GBL production capacity at its Okayama Plant from 18,000 to 20,000 tons per year, reinforcing supply to electronics and battery customers. For the fiscal year ending March 2026, the group targets consolidated net sales of approximately ¥4,400 billion, emphasizing specialty materials and advanced chemical intermediates. Under its Growth and Sustainability strategy, Mitsubishi positions GBL as a key electrolyte solvent precursor supporting lithium-ion battery manufacturing for electric vehicles. The company’s strong integration into Asian EV supply chains provides structural advantage as battery-grade solvent demand accelerates across Japan, South Korea, and China.

Ashland Focuses on High-Margin Pharmaceutical and Life Sciences Applications

Ashland Inc. has repositioned itself as a specialty ingredients company. Following divestitures of lower-margin product lines in late 2025, Ashland improved its adjusted EBITDA margin to 25% heading into 2026. The company leverages gamma butyrolactone as a precursor for pyrrolidones used in pharmaceutical excipients, injectables, and advanced tablet coatings. Its go-to-market strategy prioritizes high-purity solvent systems aligned with life sciences and nutrition growth segments. For 2026, Ashland has issued guidance reflecting renewed revenue growth supported by new pharmaceutical contracts and demand for specialty-grade intermediates within regulated healthcare markets.

LyondellBasell Aligns GBL Portfolio with Circular and Low-Carbon Strategy

LyondellBasell Industries holds approximately 14.1% of the global gamma butyrolactone and NMP market. In February 2026, the company updated its 2030 climate targets, aiming for a 32% reduction in Scope 1 and Scope 2 emissions relative to 2020 and production of 800,000 metric tons of recycled or renewable polymers. Construction of the MoReTec-1 facility in Germany strengthens its circular chemical feedstock capabilities, enhancing long-term flexibility in precursor production. LyondellBasell is optimizing its Performance Olefins and Derivatives segment through capacity rationalization in Europe and the United States to improve profitability. Its integrated olefins and derivatives platform supports efficient upstream feedstock access for GBL manufacturing within a decarbonizing petrochemical framework.

Xinjiang Tianye Strengthens Cost Leadership in the BDO to GBL Chain

Xinjiang Tianye Group Co., Ltd. is a major Chinese producer operating at scale within the BDO to GBL conversion chain using the Reppe process. The company primarily supplies the domestic Chinese market, the world’s largest GBL consumption base driven by EV battery gigafactories and electronics manufacturing clusters. Its Northwest China production complex benefits from low-cost raw materials and regional integration across acetylene and BDO feedstocks. In 2025, Tianye implemented advanced closed-loop waste management systems to comply with stricter environmental regulations governing solvent and intermediate production. The company’s agriculture-chemical integration model supports high-volume, cost-competitive gamma butyrolactone supply for agrochemical synthesis and industrial solvent applications, reinforcing its position as a key domestic supplier in China’s expanding specialty solvent market.

China: Semiconductor Self-Sufficiency and Low-Carbon Process Intensification

China’s gamma butyrolactone market is being structurally reshaped by industrial policy that couples electronic-grade purity with carbon efficiency. In September 2025, the Ministry of Industry and Information Technology issued its 2025–2026 work plan to stabilize chemical sector growth, explicitly prioritizing high-end electronic chemicals. Semiconductor-grade GBL was elevated as a strategic input for domestic self-sufficiency, accelerating investment in purification, analytics, and contamination control ahead of the 2026 technology cycle.

Capacity and process upgrades followed. In June 2025, Zhejiang Realsun Chemical commissioned an ultra-high-purity GBL line at 99.9% minimum, targeting lithium-ion battery electrolytes and pharmaceutical intermediates aligned with tighter 2026 safety and quality mandates. Parallel advances under the National Green Initiative scaled green hydrogenation routes for maleic anhydride, cutting the carbon footprint of GBL production by an estimated 18% to meet European Green Deal expectations. Provincial governments in Jiangsu and Shandong reinforced this trajectory with roughly USD 1.2 billion in 2025 grants for fine-chemical parks that integrate 1,4-butanediol and GBL loops, improving yields and logistics for export-ready supply.

United States: Yield Modernization and Green-Solvent Substitution

The United States GBL market is pivoting toward yield stability, healthcare compliance, and solvent substitution. In September 2025, Ashland initiated a strategic shutdown at its Calvert City unit to install next-generation reactors. The modernization, scheduled to restore full output in fiscal Q1 2026, is designed to tighten yield consistency for high-value GBL-based intermediates used across coatings and specialty formulations.

Healthcare and sustainability signals are broadening demand. In October 2025, LyondellBasell expanded its Purell portfolio in North America, leveraging GBL derivatives as solvents in medical-grade polymer manufacturing compliant with USP and EU Pharmacopeia requirements for 2026 deliveries. Regulatory momentum also favors GBL. Following a March 2025 review by the U.S. Environmental Protection Agency, registrations for furan-based green solvents accelerated a shift away from chlorinated chemistries toward GBL in industrial paint stripping and degreasing. In parallel, late-2025 innovation by Afton Chemical applied specialized GBL-derived compounds in the first commercial additive for hydrogen combustion engines, addressing lubrication challenges in carbon-free heavy-duty transport.

Germany: Mass-Balanced Chemistry and Pharma Supply Assurance

Germany’s GBL market is advancing through mass-balance sustainability and pharmaceutical supply chain reform. In March 2025, Evonik introduced mass-balanced GBL-based derivatives within its eCO series using ISCC PLUS bio-attributed feedstocks. These inputs enable automotive coatings manufacturers to reduce Scope 3 emissions by up to 50% for 2026 programs, aligning solvent selection with OEM carbon accounting.

Energy transition and regulation are reinforcing the shift. In November 2025, BASF confirmed that its Ludwigshafen site transitioned to 100% renewable electricity across the BDO-GBL-NMP value chain, positioning the portfolio for Europe’s premium green-solvent market as carbon-border mechanisms tighten. Concurrently, Germany is leading implementation of EU Pharma Package updates. GBL producers are aligning with the 2026 Critical Medicines Act, which requires end-to-end supply chain mapping for solvents used in antibiotics and anesthetics, elevating documentation and traceability standards.

South Korea: Battery Electrolytes and Semiconductor Localization

South Korea’s GBL demand is being propelled by batteries and chipmaking localization. In 2025, the electrical and electronics segment posted outsized growth on the back of domestic lithium-ion battery investments, where GBL is favored for high-voltage electrolyte formulations due to solvency and stability. Recognition of intellectual property leadership followed in December 2025 when MU Ionic Solutions, a joint venture involving Mitsubishi Chemical, received the Asia IP Elite award for electrolyte licensing centered on GBL-based systems for next-generation EV batteries.

Public funding is accelerating domestic supply. Mid-2025, the South Korean government announced a USD 300 million grant to localize photoresist strippers and cleaning agents, with GBL-based formulations prioritized for the 2026 pilot phase in the Yongin semiconductor cluster. This program anchors GBL within Korea’s materials sovereignty agenda for advanced manufacturing.

Thailand: Regional Distribution and Bio-Circular Feedstocks

Thailand is positioning itself as a Southeast Asian distribution and bio-circular node for GBL. In November 2025, BASF inaugurated expanded APG capacity in Bangpakong. While the core focus is surfactants, the integrated logistics hub supports efficient distribution of GBL-based co-solvents into the regional industrial cleaning market, improving service levels across ASEAN.

Policy incentives are catalyzing feedstock innovation. Under Thailand’s Bio-Circular-Green economy roadmap for 2025–2026, producers are incentivized to develop bio-based GBL from sugarcane and cassava waste. The objective is to reduce regional chemical imports by 20% by end-2026, embedding GBL within a circular bioeconomy framework and strengthening local resilience.

Summary of Country-Level Strategic Drivers in the Gamma Butyrolactone Market

Gamma Butyrolactone (GBL) Market County Level Snapshot

|

Country / Region

|

Primary Strategic Driver

|

Implications for GBL

|

|

China

|

Semiconductor self-sufficiency and green processing

|

Ultra-high-purity output, lower-carbon exports

|

|

United States

|

Yield modernization and green solvents

|

Stable domestic supply and chlorinated solvent substitution

|

|

Germany

|

Mass-balance sustainability and pharma reform

|

Scope 3 reduction and traceable solvent supply

|

|

South Korea

|

Battery and semiconductor localization

|

Growth in electrolyte and photoresist applications

|

|

Thailand

|

Bio-circular economy and logistics hubs

|

Bio-based GBL and ASEAN distribution strength

|

Gamma Butyrolactone (GBL) Market Report Scope

Gamma Butyrolactone (GBL) Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.1 Billion

|

|

Market Size (2034)

|

$5.9 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Purity Grade (Ultra-High Purity, Industrial Grade), By Application (Batteries and Capacitors, Agrochemicals, Pharmaceuticals, Industrial Solvents, Chemical Synthesis), By End-Use Industry (Electrical and Electronics, Agrochemical Industry, Pharmaceuticals and Healthcare, Chemical and Petrochemical, Automotive and Transportation)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Ashland Inc., Mitsubishi Chemical Group Corporation, LyondellBasell Industries N.V., Zhejiang Realsun Chemical Co., Ltd., Chang Chun Group, Saudi International Petrochemical Company, Huntsman Corporation, Dairen Chemical Corporation, Binzhou Yuneng Chemical Co., Ltd., Anhui LIGU New Material Co., Ltd., Balaji Amines Limited, Nippon Shokubai Co., Ltd., Dow Inc., Hefei TNJ Chemical Industry Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Gamma Butyrolactone Market Segmentation

By Purity Grade

- Ultra-High Purity

- Industrial Grade

By Application

By End-Use Industry

- Electrical and Electronics

- Agrochemical Industry

- Pharmaceuticals and Healthcare

- Chemical and Petrochemical

- Automotive and Transportation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Gamma Butyrolactone Industry

- BASF SE

- Ashland Inc.

- Mitsubishi Chemical Group Corporation

- LyondellBasell Industries N.V.

- Zhejiang Realsun Chemical Co., Ltd.

- Chang Chun Group

- Saudi International Petrochemical Company

- Huntsman Corporation

- Dairen Chemical Corporation

- Binzhou Yuneng Chemical Co., Ltd.

- Anhui LIGU New Material Co., Ltd.

- Balaji Amines Limited

- Nippon Shokubai Co., Ltd.

- Dow Inc.

- Hefei TNJ Chemical Industry Co., Ltd.

*- List not Exhaustive