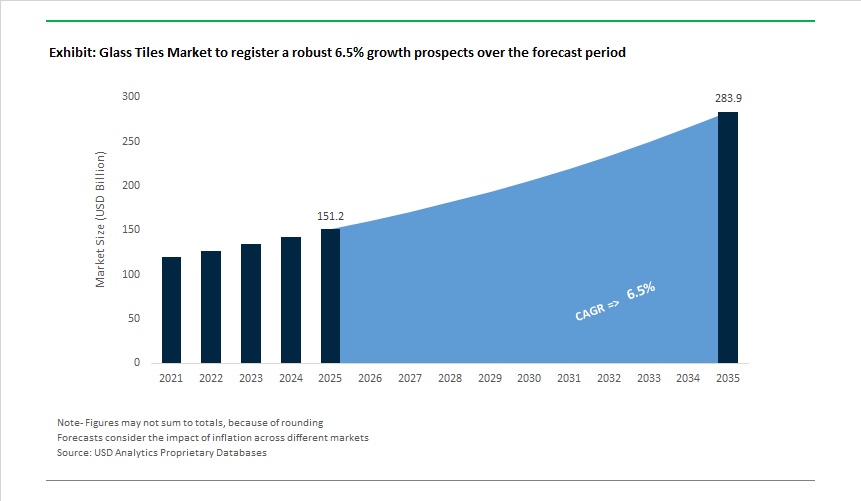

The Global Glass Tiles Market is valued at USD 151.2 billion in 2025 and is projected to reach USD 283.8 billion by 2035, expanding at a 6.5% CAGR as glass tiles evolve from decorative surface finishes into performance-driven building materials. Today, market growth is being shaped less by cyclical construction activity and more by regulatory sustainability pressure, structural engineering constraints, and design-led value creation across residential, commercial, and institutional projects.

Sustainability is no longer a marketing attribute; it is a procurement filter. Architects, developers, and public infrastructure buyers are increasingly specifying glass tiles with high recycled cullet content-often in the 70-99% range-to meet green building certifications such as LEED, IGBC, and equivalent national frameworks. At the manufacturing level, this shift is being reinforced by lower-temperature sintering processes, with firing temperatures dropping below 900°C, materially reducing energy intensity and CO₂ emissions per square meter. Producers that can document recycled content, energy reduction, and lifecycle performance are gaining preferential access to large-scale commercial and government-backed projects.

Structural considerations are becoming equally influential. As urban buildings grow taller and façade systems become more complex, dead-load reduction has emerged as a decisive design constraint. Ultra-thin and lightweight glass tiles are increasingly specified for curtain walls, ventilated façades, and retrofit applications because they reduce structural load, simplify anchoring systems, and improve seismic performance. In high-rise and earthquake-prone regions, these attributes directly affect engineering approvals and installation costs, positioning glass tiles as a functional lightweighting solution, not merely an aesthetic choice.

Performance in demanding environments further reinforces adoption. With near-zero water absorption levels below 0.5%, glass tiles outperform ceramics and natural stone in high-moisture and chemically exposed settings, including swimming pools, spas, showers, wellness facilities, and hospitality interiors. This durability translates into longer service life, lower maintenance, and reduced replacement cycles-key drivers for premium residential developments and luxury commercial spaces where lifecycle cost outweighs upfront material pricing.

Design innovation is the final growth lever reshaping competitive dynamics. Matte and textured finishes, enabled by nano-etching and surface engineering, are now the fastest-growing aesthetic segment, often commanding 10-15% price premiums over conventional glossy tiles. These finishes address demand for glare reduction, tactile surfaces, and contemporary visual language in high-end interiors. As customization becomes central to architectural differentiation, manufacturers with flexible production lines, digital patterning capabilities, and rapid colorway development are capturing higher-margin business.

The Glass Tiles industry is undergoing rapid transformation driven by design preferences, sustainability regulations, performance requirements, and advanced manufacturing technologies. In December 2025, global architectural reports confirmed a strong shift toward Oversized Glass Tiles (24 inches and above), primarily for wall cladding and luxury bathrooms where seamless aesthetics and reduced grout lines are prioritized. This evolution aligns with the market’s growing preference for minimalist design and surface continuity. Earlier in September 2025, advances in nano-etching enabled durable anti-fingerprint matte surfaces, expanding the use of matte Glass Tiles into commercial environments where high foot traffic and easy-clean properties are essential. On the other hand, supply chain shifts in August 2025 caused a 5% price increase due to feedstock shortages and higher logistics costs, affecting low-carbon Glass Tile producers who rely heavily on consistent cullet availability.

Sustainability milestones remain central to industry development. In June 2025, a UK research breakthrough demonstrated the feasibility of creating tiles with 95% recycled industrial waste, accelerating progress toward near-100% recycled glass tile compositions. Complementing this movement, AGC Glass Europe’s March 2025 announcement of recycling 700,000 tonnes of cullet in 2024 and targeting a 50% cullet ratio by 2030 underscored the shift toward low-carbon glass inputs. This trend further gained traction in January 2025, when Dal-Tile unveiled a new product line emphasizing recycled content, signaling heightened awareness among U.S. manufacturers toward sustainable building materials. Additionally, design trends continue to evolve, as demonstrated by the September 2024 resurgence of iridescent and opalescent finishes, leveraging glass translucency to create color-shifting, luxury aesthetics increasingly favored in high-end residential and hospitality spaces.

Digitalization and production modernization are also reshaping market dynamics. In May 2025, demand for digitally printed Glass Tiles surged as architects and designers gravitated toward hyper-customized patterns for backsplashes, countertops, and feature walls. These innovations allow manufacturers to expand product portfolios without increasing inventory complexity.

The global push toward net-zero embodied carbon in construction is accelerating the adoption of high-recycled-content glass tiles across commercial interiors, institutional buildings, and premium facades. Developers are increasingly prioritizing materials that contribute measurable sustainability credits without compromising aesthetics or durability, positioning recycled glass tiles as a strategic specification rather than a niche eco-option. During 2024–2025, leading manufacturers standardized production lines incorporating 25% to 65% recycled content, combining post-consumer bottles with pre-consumer industrial scrap. This composition directly supports LEED v4.1 Materials & Resources credits, particularly under the “Sourcing of Raw Materials” and “Environmental Product Declarations” pathways, which are now baseline requirements for Tier-1 corporate offices, airports, and mixed-use developments. Beyond certification optics, lifecycle performance is becoming a decisive factor. A 2025 life-cycle assessment conducted by RMIT University demonstrated that substituting virgin raw materials with unwashed recycled glass can reduce tile-level embodied carbon by 13%–18%, a meaningful reduction for developers subject to the EU CSRD and emerging U.S. climate disclosure rules. Importantly, durability concerns around recycled materials are being structurally resolved. Peer-reviewed research published in Glass Structures and Engineering (mid-2025) confirms that fused recycled glass tiles now match Grade-5 porcelain in impact resistance and wear performance, enabling their use in high-traffic public spaces such as transit concourses and civic buildings. This convergence of sustainability credentials and long-term performance is shifting recycled glass tiles from symbolic ESG features into core architectural finishes.

Architectural design language in commercial and hospitality spaces is evolving rapidly, favoring seamless, grout-minimal surfaces over traditional small-format mosaics. This shift is driving strong demand for large-format glass tile panels, enabled by advances in tempering, lamination, and digital ceramic printing. By 2025, fabrication facilities have successfully scaled production of monolithic glass panels in 10–12 mm thickness as well as ultra-thin 1.6 mm formats, allowing designers to specify uninterrupted wall expanses while reducing joint density by more than 90%. The visual impact is matched by technological sophistication. High-definition digital ceramic ink printing now achieves resolutions of up to 1440 dpi, allowing permanent replication of rare stone patterns, abstract art, or branded motifs directly onto glass surfaces with full UV stability. Early-2025 disclosures from Hartung Glass Industries highlighted a sharp rise in demand for customized digitally printed glass, driven by luxury retail renovations and corporate identity-focused interiors. The trend is also intersecting with smart-infrastructure design. In transit hubs and flagship public buildings, large-format glass tile assemblies are being integrated with embedded LEDs, sensors, and control systems, transforming static feature walls into interactive information and wayfinding surfaces. This convergence of architectural glass, digital printing, and IoT functionality is expanding the role of glass tiles from decorative finishes to experiential design infrastructure within smart city projects.

Post-pandemic regulatory tightening and heightened awareness of indoor hygiene are creating a strong retrofit opportunity for non-porous glass tile systems in public and semi-public buildings. Hospitals, schools, airports, and transport terminals are actively replacing porous stone and ceramic finishes with glass surfaces that inherently resist microbial growth. Glass tiles offer 0% water absorption, eliminating conditions that support mold and mildew, a critical advantage for facilities targeting WELL Building Standard and equivalent health-focused certifications. Market momentum is reinforced by surface technology advancements. By 2025, antibacterial glass materials—using silver ion (Ag⁺) and titanium dioxide (TiO₂) coatings—have demonstrated the ability to neutralize 99.9% of bacteria within 24 hours, making them a preferred solution for high-contact zones such as operating rooms, food service areas, and restrooms. From an operational standpoint, facility managers are recognizing cost benefits alongside hygiene gains. Technical data from recent public-sector retrofit projects indicate that glass tile installations can reduce cleaning chemical consumption by approximately 30%, supporting low-VOC indoor air quality goals while lowering maintenance intensity. As building codes in emerging markets increasingly emphasize material durability, hygiene, and lifecycle efficiency—such as recent updates to national public-infrastructure standards in Africa and Southeast Asia—glass tiles are becoming a default retrofit choice rather than a premium upgrade.

The maturation of Building-Integrated Photovoltaics (BIPV) is transforming glass tiles from passive envelope elements into active energy-generating components, unlocking new value streams for façades, roofs, and atriums. In 2025, next-generation BIPV glass tiles using crystalline silicon technology achieved 18%–22.5% conversion efficiency, narrowing the performance gap with conventional rooftop solar while offering superior architectural integration. Semi-transparent configurations—allowing roughly 20% visible light transmission—are gaining traction in atriums, transit stations, and industrial halls where daylighting and power generation must coexist. Structural feasibility has also improved markedly. Manufacturers have introduced ultra-lightweight glass tiles weighing as little as 6 kg/m², utilizing 1.6 mm tempered glass to deliver high impact resistance against wind and hail while remaining suitable for retrofitting older buildings with limited load capacity. Policy momentum is accelerating adoption. In early 2025, China mandated BIPV integration in all new public infrastructure projects, a move increasingly mirrored by EU green-building directives and financial incentives under the U.S. Inflation Reduction Act. These mandates are expanding the addressable market for solar glass tiles beyond showcase projects into mainstream schools, metro stations, and government facilities, positioning BIPV-enabled glass tiles as a cornerstone material for the next generation of net-zero and energy-positive buildings.

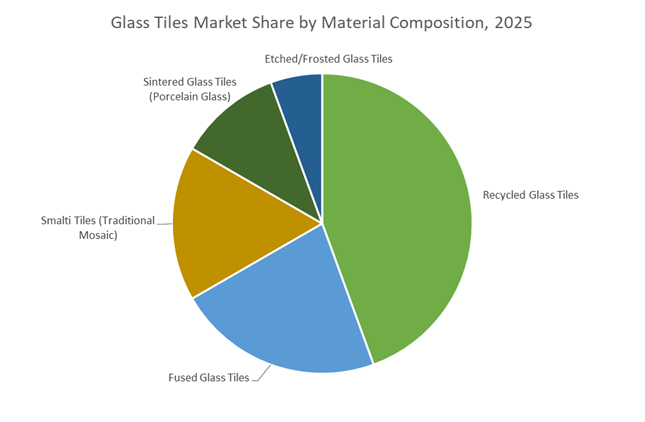

Recycled glass tiles account for approximately 40% of the global glass tiles market because they uniquely align verified sustainability credentials with aggressive cost rationalization, a combination that has reshaped specification decisions in 2025. The segment’s leadership is no longer driven by environmental positioning alone; it is anchored in measurable manufacturing and procurement advantages. The shift toward 100% post-consumer feedstock, exemplified by early-2025 launches using recycled automotive windshields, has resolved long-standing transparency gaps around recycled content—an issue that previously limited adoption among commercial architects and ESG-driven residential developers. On the cost side, cullet-based production reduces furnace temperatures, enabling up to 30% lower energy consumption versus virgin glass or ceramic tile manufacturing, directly improving embodied-carbon metrics tied to net-zero construction frameworks. This efficiency has unlocked structural pricing power: strategic 40% price reductions on sintered recycled glass tiles in 2025 repositioned the category from premium niche to mid-market default, accelerating volume penetration. Performance characteristics reinforce dominance—recycled glass tiles are non-porous, antimicrobial, and sealant-free, eliminating lifecycle maintenance costs that plague natural stone alternatives. These combined factors—verifiable circularity, lower production energy, competitive pricing, and reduced total cost of ownership—explain why recycled glass tiles now anchor material demand across both residential and light-commercial specifications.

The residential segment represents roughly 55% of total glass tile demand, driven by a 2025 convergence of renovation intensity, wellness-focused interiors, and sustainability-linked property value uplift. Unlike new-build cycles, residential demand is being pulled by renovation economics: industry order-flow analysis shows that over 45% of glass tile volumes are tied to kitchen and bathroom remodels, where reflective surfaces are specified to enhance daylight penetration and visually expand compact urban living spaces. Sustainability credentials increasingly influence homeowner decisions—manufacturers report 84% wastewater recovery rates in tile production, enabling glass tiles to be marketed as genuinely circular products rather than surface-level eco options. This resonates with buyers targeting certification-linked resale premiums, as residential projects seeking LEED v4.1 or Green Squared credentials rose by 15% year-over-year, with glass tiles contributing directly to point accumulation. Health considerations further reinforce adoption: zero-VOC emissions position recycled glass tiles as preferred finishes for nurseries, indoor spas, and allergy-sensitive households, a differentiator that ceramics and composites struggle to match. Collectively, renovation-driven demand, certification economics, and indoor-air-quality priorities have structurally anchored residential applications as the dominant consumption base for glass tiles in 2025.

The competitive landscape of the Glass Tiles Market is defined by companies that excel in sustainable manufacturing, advanced coating technologies, large-format designs, and recycled glass utilization. Market leaders are accelerating adoption of low-carbon glass production, expanding product lines with recycled content, and investing in digital printing and nano-etching capabilities. Strong regional supply chains, global distribution networks, and deep material science expertise also distinguish the top players. Collectively, these companies shape market direction through innovations in recycled materials, aesthetic versatility, and eco-efficient production.

Saint-Gobain maintains a leading role by supplying high-quality float glass that forms the foundation for a significant share of global Glass Tile production. Its Low-Carbon Glass product line-produced using high cullet content and renewable energy-reduces embodied carbon, making it a preferred choice for sustainable construction. Saint-Gobain’s R&D focus on multifunctional Low-E coatings further enhances thermal and solar control performance for façade applications. Its circularity pact with IKEA (2024-2025) reinforces commitment to recycled content and strengthens its alignment with global green building initiatives.

AGC Inc. serves as a major supplier of advanced flat glass products that support high-performance Glass Tiles, including laminated and tempered variants. Its 2024-2025 creation of a dedicated XR materials unit and partnership with Meta Reality Labs highlights deep R&D capabilities applicable to specialty glass coatings and ceramic-glass composites. AGC’s growing expertise in precision glass-ceramics and waveguide materials demonstrates transferable scientific strengths that elevate the performance of sintered and fused Glass Tiles. With a strong presence across Asia, Europe, and the Americas, AGC delivers supply chain stability for global tile manufacturers.

Daltile commands one of the most diverse tile portfolios in North America, with a strong presence in both commercial and residential segments. Its 2024 launch of Recycled Glass Tiles aligns with rising consumer demand for circular materials and reinforces its sustainability credentials. With over 99% of its tile collections using recycled or reclaimed materials, Daltile remains at the forefront of eco-friendly tile manufacturing. Its design-driven strategy, enhanced by digital printing and specialty finishes, enables strong positioning in premium backsplashes, countertops, and designer wall applications.

Marazzi is recognized for its leadership in aesthetic innovation, particularly through the use of advanced digital printing technologies that deliver ultra-high-resolution Glass Tile designs. As part of the Oversized Tile trend, Marazzi has led in expanding large-format and matte product offerings that appeal to contemporary architectural styles. Its extensive global distribution network accelerates the adoption of new design innovations across major construction markets. The company also prioritizes production efficiency, integrating energy-saving processes and waste reduction in both ceramic and glass surfacing lines.

Interstyle excels in niche, premium tile markets where customization, artisanal finishes, and architectural detailing take priority. Its proprietary fusing techniques produce deep, saturated colors and iridescent surfaces ideal for luxury pools, spas, boutique hotels, and designer commercial projects. The company’s strength lies in delivering tailored Glass Tile and mosaic combinations in unique shapes, blends, and visual effects. With products featuring verified recycled content, Interstyle appeals to clients seeking both sustainability and high-end aesthetic performance in demanding environments.

Spain continues to set the global design agenda for the glass tiles market, with 2025 marking a decisive pivot toward digitally enabled aesthetics and modular architectural systems. Insights unveiled at Cevisama 2025 highlight a move toward multi-dimensional realism, where advanced digital printing on glass substrates recreates natural erosion, mineral oxidation, and tactile depth. These “sensory textures” are redefining premium interior applications, particularly in bathrooms, spas, and high-moisture environments where glass tiles outperform traditional ceramics in durability and hygiene.

From a sustainability perspective, Spanish manufacturers—supported by national and regional policy frameworks—are scaling thin-gauged glass-ceramic composites as slim as 6 mm. These products materially reduce raw material intensity and logistics-related emissions, aligning with EU decarbonization objectives. A parallel trend is modular integration, enabling seamless transitions between interior wall cladding and exterior ventilated façades. This systemized approach is gaining traction in premium residential and mixed-use developments across Western Europe, positioning Spain as the benchmark supplier for design-led, low-carbon glass tile solutions.

Italy’s glass tiles industry in 2025 is consolidating its dominance in the high-value, sustainability-driven segment, leveraging deep expertise in surface chemistry and kiln engineering. Production volumes have rebounded strongly, with a marked shift toward ultra-high-purity glass mosaics aimed at export markets that demand stringent environmental credentials. The defining transformation, however, is technological: Italian producers are commercializing water-based digital adhesives and molds, eliminating solvent-based glazes that historically contributed to VOC emissions.

This manufacturing shift directly supports global demand for LEED- and BREEAM-certified building materials, making Italian glass tiles the preferred option for green luxury developments. Compliance with the EU Emissions Trading System (ETS) has further accelerated investment into AI-driven, energy-efficient kilns optimized specifically for glass-tile sintering. By 2025, these upgrades have become less a regulatory burden and more a competitive moat, allowing Italy to price its products at a premium while maintaining export resilience amid tightening carbon regulations.

The U.S. glass tiles market in 2025 is being reshaped by trade policy and domestic manufacturing modernization. Newly implemented federal tariffs on imported glass tiles have prompted developers and distributors to reassess sourcing strategies, accelerating a shift toward domestic, high-recycled-content glass tile production. This localization trend is particularly pronounced in commercial and hospitality construction, where supply chain predictability and compliance with sustainability reporting requirements are increasingly critical.

On the manufacturing side, leading U.S. producers are integrating AI-based visual inspection systems to detect micro-defects in glass tiles, improving yield and reducing scrap rates by double-digit percentages. Demand growth is most visible in high-end hospitality corridors—especially Florida and Nevada—where backlit glass tiles and photoluminescent safety tiles are being specified for both aesthetic impact and functional wayfinding during power outages. These use cases underscore how U.S. demand is shifting from commodity tiling toward technology-enabled, safety-oriented glass tile applications.

India’s glass tiles market is scaling rapidly in 2025, driven by digital manufacturing adoption and national industrial policy alignment. Innovations showcased at Glasspro INDIA 2025 reflect the integration of AI and advanced analytics into furnace operations, enabling optimized heat cycles for specialty glass tiles. This digitalization improves energy efficiency and product consistency—critical factors as India expands capacity to serve both domestic and export markets.

Government-backed Production Linked Incentive (PLI) programs are indirectly catalyzing growth in specialized glass tiles, particularly those featuring anti-microbial coatings for hospitals, laboratories, and cleanroom environments. At the same time, Indian manufacturers are strengthening their export footprint across the Middle East and Africa, offering competitively priced alternatives to European glass mosaics. This combination of digital efficiency, healthcare-driven demand, and export competitiveness positions India as one of the fastest-scaling supply bases in the global glass tiles landscape.

The UAE represents a high-margin demand center for the global glass tiles market, underpinned by an unprecedented surge in luxury real estate and hospitality construction. In 2025 alone, tens of thousands of new building permits—concentrated in Dubai and Abu Dhabi—are translating directly into demand for premium mosaic glass tiles, particularly those produced from recycled bottle glass to support Net-Zero 2050 objectives.

Luxury developers are increasingly specifying bespoke, digitally printed glass tiles that deliver photorealistic patterns for spas, pools, and experiential interiors. With international tourism rebounding strongly, hospitality operators are using glass tiles not only as surface finishes but as branding elements that differentiate high-end properties. The UAE’s market is therefore less volume-driven and more defined by customization, sustainability credentials, and design exclusivity, making it a strategic destination for premium global suppliers.

Turkey’s glass tiles market is structurally supported by its massive urban renewal mandate, one of the largest reconstruction efforts globally. The renewal of millions of residential units is generating sustained domestic demand for high-durability glass tiles, particularly in kitchens and bathrooms where renovation projects consume substantially more tile per square meter than new builds. This creates a stable, multi-year demand base largely insulated from short-term export volatility.

In response to energy price fluctuations and EU carbon regulations, Turkish manufacturers are accelerating investments in solar-powered tile production facilities. Large-scale rooftop solar installations are reducing exposure to natural gas costs while ensuring compliance with the EU’s Carbon Border Adjustment Mechanism (CBAM). As a result, Turkey is emerging as a cost-competitive, low-carbon manufacturing hub for glass tiles serving both domestic reconstruction and export markets across Europe.

|

Country |

Strategic Driver |

2025 Key Milestone |

Primary Material / Technology Focus |

|

Spain |

Design leadership |

Cevisama 2025 innovation roadmap |

Glass-ceramic composites & modular systems |

|

Italy |

Sustainable manufacturing |

Water-based digital adhesive adoption |

Ultra-high-purity glass mosaics |

|

United States |

Trade protection & localization |

Impact of 2025 import tariffs |

Recycled, domestically produced glass tiles |

|

India |

Digital manufacturing scale-up |

AI-optimized furnace operations |

Anti-microbial & specialty glass tiles |

|

UAE |

Luxury real estate boom |

30,000+ H1 2025 building permits |

Bespoke, digitally printed mosaics |

|

Turkey |

Urban reconstruction |

6.7 million building renewal mandate |

High-durability, solar-manufactured tiles |

|

Parameter |

Details |

|

Market Size (2025) |

$151.2 Billion |

|

Market Size (2035) |

$283.8 Billion |

|

Market Growth Rate |

6.5% |

|

Segments |

By Material Composition (Recycled Glass, Smalti, Fused Glass, Sintered Glass, Etched/Frosted Glass), By Product Format (Mosaic Tiles, Large-Format Slabs, Subway Tiles, Listello Tiles, Back-Painted Panels), By Surface Finish (Glossy/Polished, Matte/Iridescent, Textured/3D Inkjet, Anti-Slip), By Application (Residential, Commercial, Industrial) |

|

Study Period |

2019- 2024 and 2025-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Daltile (Mohawk Industries Inc.), RAK Ceramics, Iris Ceramica Group, Emser Tile, Sicis S.p.A., Artistic Tile, Kajaria Ceramics Limited, Crossville Inc., Interstyle Ceramic & Glass, Vidrepur S.A., Oceanside Glass & Tile, Bisazza S.p.A., Trend Group S.p.A., Ann Sacks Tile & Stone Inc., Hakatai Enterprises Inc. |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

*- List not Exhaustive

Table of Contents: Glass Tiles Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Glass Tiles Market Landscape & Outlook (2025–2035)

2.1. Introduction to Glass Tiles Market

2.2. Market Valuation and Growth Projections (2025–2035)

2.3. Sustainability Mandates and Recycled Content Adoption

2.4. Structural Lightweighting and Performance Advantages

2.5. Design-Led Differentiation and Manufacturing Innovation

3. Innovations Reshaping the Glass Tiles Market

3.1. Trend: High-Recycled-Content Glass Tiles for LEED, ESG, and Net-Zero Compliance

3.2. Trend: Large-Format and Digitally Printed Glass Panels for Architectural Feature Walls

3.3. Opportunity: Hygiene-Focused Retrofits in Healthy Building Infrastructure

3.4. Opportunity: Building-Integrated Photovoltaic (BIPV) Glass Tiles for Net-Zero Architecture

4. Competitive Landscape and Strategic Initiatives

4.1. Sustainability-Driven Product Development and Low-Carbon Manufacturing

4.2. Digital Printing, Nano-Etching, and Surface Engineering Advances

4.3. Capacity Expansion, Localization, and Supply Chain Optimization

4.4. Design Partnerships with Architects, Developers, and Infrastructure Agencies

5. Market Share and Segmentation Insights: Glass Tiles Market

5.1. By Material Composition

5.1.1. Recycled Glass Tiles

5.1.2. Smalti Tiles

5.1.3. Fused Glass Tiles

5.1.4. Sintered Glass Tiles

5.1.5. Etched and Frosted Glass Tiles

5.2. By Product Format

5.2.1. Mosaic Tiles

5.2.2. Large Format Glass Slabs

5.2.3. Subway Tiles

5.2.4. Listello Tiles

5.2.5. Back-Painted Glass Panels

5.3. By Surface Finish

5.3.1. Glossy and Polished

5.3.2. Matte and Iridescent

5.3.3. Textured and 3D Inkjet Printed

5.3.4. Anti-Slip and Grit-Treated

5.4. By Application

5.4.1. Residential

5.4.2. Commercial

5.4.3. Industrial

6. Country Analysis and Outlook of Glass Tiles Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. United Kingdom

6.7. Italy

6.8. Spain

6.9. Turkey

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Glass Tiles Market Size Outlook by Region (2025–2035)

7.1. North America Glass Tiles Market Size Outlook to 2035

7.1.1. By Material Composition

7.1.2. By Product Format

7.1.3. By Surface Finish

7.1.4. By Application

7.2. Europe Glass Tiles Market Size Outlook to 2035

7.2.1. By Material Composition

7.2.2. By Product Format

7.2.3. By Surface Finish

7.2.4. By Application

7.3. Asia Pacific Glass Tiles Market Size Outlook to 2035

7.3.1. By Material Composition

7.3.2. By Product Format

7.3.3. By Surface Finish

7.3.4. By Application

7.4. South and Central America Glass Tiles Market Size Outlook to 2035

7.4.1. By Material Composition

7.4.2. By Product Format

7.4.3. By Surface Finish

7.4.4. By Application

7.5. Middle East and Africa Glass Tiles Market Size Outlook to 2035

7.5.1. By Material Composition

7.5.2. By Product Format

7.5.3. By Surface Finish

7.5.4. By Application

8. Company Profiles: Leading Players in the Glass Tiles Market

8.1. Daltile (Mohawk Industries, Inc.)

8.2. RAK Ceramics

8.3. Iris Ceramica Group

8.4. Emser Tile

8.5. Sicis S.p.A.

8.6. Artistic Tile

8.7. Kajaria Ceramics Limited

8.8. Crossville Inc.

8.9. Interstyle Ceramic & Glass

8.10. Vidrepur S.A.

8.11. Oceanside Glass & Tile

8.12. Bisazza S.p.A.

8.13. Trend Group S.p.A.

8.14. Ann Sacks Tile & Stone, Inc.

8.15. Hakatai Enterprises, Inc.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Methodology

9.4. Data Sources and Assumptions

9.5. Research Coverage

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

The global Glass Tiles Market was valued at USD 151.2 billion in 2025 and is expected to reach USD 283.8 billion by 2035, expanding at a CAGR of 6.5%. Growth is being driven by sustainability mandates, structural lightweighting requirements in urban construction, and increasing demand for design-led, high-performance architectural materials.

Recycled glass tiles are increasingly specified because they combine verified sustainability credentials with strong lifecycle performance. Tiles with 70–99% recycled cullet content contribute directly to LEED, IGBC, and equivalent green-building credits, while lower sintering temperatures reduce embodied carbon. Their non-porous nature also delivers superior durability, hygiene, and reduced maintenance compared with ceramic or natural stone alternatives.

Ultra-thin and lightweight glass tiles reduce dead load on façades and interior wall systems, simplifying anchoring requirements and improving seismic performance. These attributes are critical in high-rise buildings, retrofit projects, and earthquake-prone regions, positioning glass tiles as functional lightweighting solutions rather than purely decorative finishes.

Key trends include oversized and large-format glass tiles for seamless surfaces, digitally printed and customized patterns, and matte or textured finishes enabled by nano-etching. Performance-driven demand is also rising in high-moisture and hygiene-sensitive environments due to glass tiles’ near-zero water absorption, chemical resistance, and compatibility with antibacterial surface treatments.

The glass tiles market is led by manufacturers with strong capabilities in recycled glass utilization, digital printing, and sustainable production. Key players include Saint-Gobain S.A., AGC Inc., Daltile, Marazzi Group, Interstyle Ceramic & Glass, RAK Ceramics, and Bisazza S.p.A.. Competitive differentiation increasingly depends on recycled content documentation, design flexibility, large-format capability, and low-carbon manufacturing processes.