Glauber’s Salt Market to Reach $1.9 Billion by 2034 at 3.2% CAGR Driven by Low-Carbon Sodium Sulfate Recovery and Circular Byproduct Integration

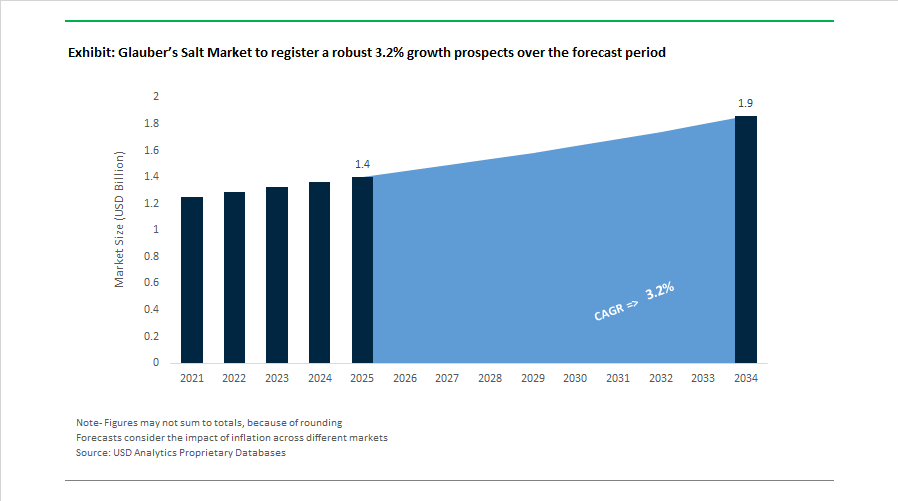

The Glauber’s Salt Market is projected to expand from $1.4 billion in 2025 to $1.9 billion by 2034, registering a CAGR of 3.2% over the forecast period. Growth is supported by steady demand for sodium sulfate in detergents, glass manufacturing, textiles, pulp and paper, pharmaceuticals, and emerging thermal energy storage systems. Market dynamics are increasingly shaped by low-carbon recovery technologies, byproduct stream integration from viscose and lithium processing, and tightening purity standards in specialty chemical applications. The transition from bulk filler usage toward high-purity functional grades is redefining value creation across the sodium sulfate supply chain.

In 2024, Grasim Industries Limited launched EcoSodium, a sustainably recovered sodium sulfate derived from viscose staple fiber production. Positioned as a low-carbon alternative to mined Glauber’s salt, the product targets environmentally conscious textile and detergent manufacturers across Asia and Europe. In early 2024, Tata Chemicals Limited completed integration of a U.S.-based sodium sulfate facility following its late-2023 acquisition, reinforcing its footprint in high-purity anhydrous sodium sulfate for specialty chemicals and glass applications. In August 2024, Ciner Resources LP implemented a closed-loop evaporation system in California, improving recovery efficiency by 15% while reducing freshwater consumption in compliance with Western U.S. environmental standards. During 2024, Alkim Alkali Kimya A.S. completed solar-assisted evaporation modernization at its lake operations, lowering extraction-related carbon intensity and strengthening its appeal to European glass manufacturers.

Industrial energy efficiency and pricing volatility influenced 2025 market conditions. In May 2025, a major Shandong producer commissioned a Mechanical Vapor Recompression plant for sodium sulfate crystallization, reducing energy consumption compared to conventional multi-effect evaporation systems and aligning with China’s 2025 industrial energy-saving mandates. In June 2025, sodium sulfate prices in China reached a 12-month high amid tightening supply from reduced byproduct output in rayon and lithium processing sectors, coupled with restocking by detergent and packaging manufacturers. In June 2025, global consumer goods companies such as Unilever PLC and Procter & Gamble highlighted a shift in detergent formulation, with concentrated powder tablets in emerging markets utilizing high-purity Glauber’s salt as a solubility enhancer rather than a bulk filler.

Application diversification expanded in late 2025 and 2026. In October 2025, Sigma-Aldrich and Intersac introduced ultra-high-purity anhydrous sodium sulfate grades with impurity levels below 0.05%, meeting stringent pharmaceutical requirements for pH buffering and moisture control in injectable formulations. In late 2025, European industrial partners demonstrated stabilized Glauber’s salt-palmitic acid dispersions for residential thermal energy storage systems, addressing long-standing phase segregation challenges and enabling commercial viability in 2026. In July 2025, Saskatchewan Mining and Minerals Inc. broke ground on a $220 million facility transformation to leverage its reserves for Sulphate of Potash fertilizer production while maintaining sodium sulfate output. In January 2026, battery recycling firms in North America and Europe reported commercial-grade sodium sulfate recovery from lithium-ion black mass streams, creating a secondary circular supply channel for glass and textile industries.

The Glauber’s Salt Market outlook reflects low-carbon extraction modernization, byproduct recovery from viscose and lithium sectors, high-purity pharmaceutical grade expansion, energy-efficient crystallization systems, and emerging applications in thermal energy storage. Competitive positioning increasingly depends on carbon intensity reduction, feedstock diversification, circular economy integration, and compliance with evolving purity and environmental standards across detergents, glass, and specialty chemicals.

Competitive Landscape in Glauber’s Salt Market

Alkim Alkali Kimya Strengthens Natural Sodium Sulfate Leadership Through Reserve Security

Alkim Alkali Kimya A.S. is one of the largest global producers of natural sodium sulfate, supported by patented underground solution mining operations in Ankara with proven reserves exceeding 500 million tons. Its physical moisture-removal processing method avoids chemical transformation steps, allowing refined sodium sulfate to remain exempt from certain REACH-style regulatory classifications. In early 2026, Alkim accelerated capacity expansion to capture growing EMEA demand in detergent, glass manufacturing, and textile dyeing applications. The company produces ultra-high purity anhydrous sodium sulfate tailored for powdered detergent formulations, the largest end-use segment globally. Diversification into potassium sulfate fertilizers in 2025 and 2026 enhances margin resilience while leveraging its established sodium sulfate infrastructure.

Nafine Chemical Industry Anchors China’s Dominance in Sodium Sulfate Supply

Nafine Chemical Industry Group Co., Ltd. operates at the center of China’s sodium sulfate production hub, benefiting from localized mirabilite deposits and cost-efficient large-scale extraction. China accounts for approximately 70% of global sodium sulfate output, and Nafine remains a leading volume supplier within this ecosystem. The company markets high-volume anhydrous sodium sulfate and Glauber’s salt primarily for the powdered detergent sector, which represents roughly 44% of global revenue demand. In 2026, Nafine intensified environmental compliance investments, deploying closed-loop waste management systems aligned with China’s updated green industrial standards. Asia-Pacific sodium sulfate consumption is projected to approach 9,000 thousand tonnes by 2032, reinforcing Nafine’s regional supply chain dominance.

Searles Valley Minerals Advances Domestic Mineral Security in North America

Searles Valley Minerals, a subsidiary of Nirma Limited, is the primary North American producer of natural sodium sulfate extracted from Searles Lake brines in California. The company operates an integrated mineral portfolio including borax, soda ash, and sodium sulfate, and contributes substantial royalties for mineral rights on public lands. In 2026, SVM became an active participant in the Climate VISION initiative, supporting greenhouse gas reduction through optimized brine processing technologies. Its Resource Longevity strategy incorporates haloalkaliphilic bacterial monitoring to preserve brine ecosystem stability while maintaining extraction efficiency. Domestic localization strategies align with US industrial policy favoring regionally sourced raw materials for glass manufacturing and textile processing sectors.

Lenzing AG Expands Bio-Based Sodium Sulfate Through Circular Biorefinery Model

Lenzing AG produces high-purity sodium sulfate as a byproduct of its viscose and lyocell fiber manufacturing operations, positioning it as a bio-based and traceable alternative in the specialty sodium sulfate market. In early 2026, the company emphasized its Circular Biorefinery model, recovering sulfur compounds during fiber production and converting them into sodium sulfate, thereby closing the chemical loop. This byproduct stream supports pharmaceutical and detergent manufacturers seeking low carbon footprint and traceable supply chains. Fiber capacity expansions in Thailand and Brazil during 2024 and 2025 increased regional sodium sulfate availability in Asia-Pacific and Latin America. By monetizing chemical recovery, Lenzing strengthens its pathway toward net-zero greenhouse gas emissions by 2050.

Cordenka Targets Specialty Pharmaceutical Sodium Sulfate Applications

Cordenka GmbH, a producer of industrial rayon, supplies high-purity sodium sulfate derived from wood-based chemical recovery processes. In February 2026, the company highlighted its Advancing Circularity initiative, integrating biochemical wood feedstocks with advanced chemical recovery technologies. Cordenka has shifted marketing focus toward pharmaceutical-grade sodium sulfate used in colon-cleansing preparations and analytical laboratory applications requiring strict GMP compliance. Its positioning in the European specialty-grade sodium sulfate segment is supported by adherence to pharmacopeia standards and rigorous quality control. Bio-circular applications in agriculture and industry further diversify its revenue streams beyond traditional detergent markets.

Industrias Peñoles Maintains Latin American Leadership Through Scale and Digital Optimization

Industrias Peñoles S.A. de C.V., through its Química del Rey facility, operates the largest sodium sulfate plant in the Western Hemisphere. The company produces high-purity anhydrous sodium sulfate primarily serving textile dyeing and detergent manufacturing across the Americas. In early 2026, Peñoles reported stable output from its chemical division, supported by modernization initiatives and regional industrial growth. Deployment of physical AI systems and automated sensor arrays is improving magnesium and sodium salt extraction efficiency, enhancing cost competitiveness. Latin America is currently expanding at a rate above the global average due to industrial upgrades in Brazil and Mexico, reinforcing Peñoles’ regional supply leadership in the natural sodium sulfate market.

Glauber’s Salt Market Share and Segmentation Insights

Anhydrous Sodium Sulfate Leads the Glauber’s Salt Market Due to High-Purity Industrial Processing Demand

Anhydrous Sodium Sulfate accounted for 52.80% of the Glauber’s Salt Market share in 2025, establishing it as the dominant product form across global sodium sulfate consumption. This form is widely preferred in detergent formulation, glass manufacturing, and industrial chemical processing, where low moisture content and consistent chemical composition are essential for maintaining production efficiency and product quality. Anhydrous sodium sulfate functions as a processing aid, filler, and flow control agent, particularly in powder detergent manufacturing and industrial glass melting processes where excess water content can interfere with processing stability. In 2025, producers are increasingly focusing on energy-efficient drying technologies to improve production economics and sustainability. The removal of water from Glauber’s salt to produce anhydrous sodium sulfate is energy intensive, prompting manufacturers to adopt mechanical vapor recompression systems and advanced waste heat recovery technologies. These improvements significantly reduce energy consumption and carbon emissions during dehydration, enabling producers to maintain competitive pricing while meeting rising sustainability expectations within the global Glauber’s salt market.

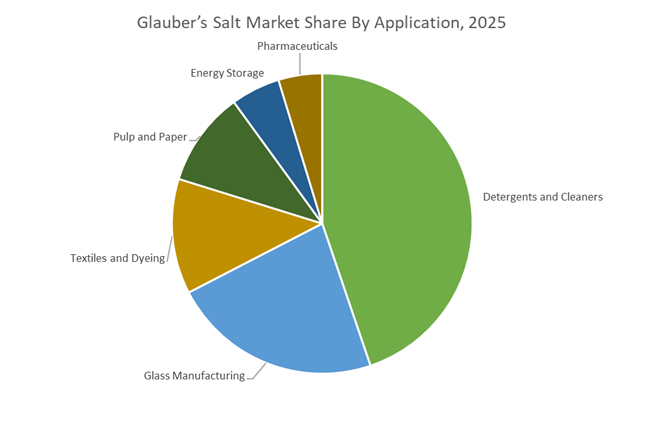

Detergents and Cleaners Drive the Largest Demand for Glauber’s Salt in Powder Detergent Manufacturing

Detergents and Cleaners represented 44.80% of the Glauber’s Salt Market share in 2025, making this segment the largest application for sodium sulfate-based materials. In powdered laundry detergents, sodium sulfate serves as an inert filler and processing aid, providing bulk to detergent formulations while improving powder flow properties and manufacturing efficiency during blending and granulation. The compound is chemically stable and compatible with surfactants, bleaching agents, and other detergent ingredients, making it a widely used additive in large-scale detergent production. Despite the increasing popularity of liquid detergents and unit-dose detergent pods, powdered detergent products continue to maintain strong demand in developing markets and cost-sensitive consumer segments. In 2025, powdered detergent formulations remain particularly important for color-safe laundry products, oxygen bleach detergents, and industrial cleaning powders, supporting steady sodium sulfate consumption. Manufacturers are simultaneously working to optimize detergent formulations to reduce environmental impact and improve biodegradability, ensuring continued relevance of sodium sulfate within the global detergent and cleaning products industry.

China: Sodium-Ion Batteries and Energy-Efficient Crystallization as Demand Anchors

China’s Glauber’s salt industry is being structurally reshaped by its rapid pivot toward next-generation energy storage and stricter industrial efficiency mandates. At its December 2025 supplier conference, CATL outlined a dual-track battery roadmap that places sodium-ion batteries alongside lithium-ion systems for early 2026 commercialization in electric vehicles and grid-scale storage. This shift is directly expanding the downstream relevance of sodium sulfate and Glauber’s salt derivatives as precursors in cathode material synthesis, particularly where cost stability and raw material security are prioritized over lithium intensity. Parallel to battery demand, China’s dominance in solar glass manufacturing continues to absorb large volumes of sodium sulfate sourced from mirabilite reserves.

Regulatory pressure is accelerating process modernization. Under the MIIT 2025 Chemical Industry Work Plan, sodium sulfate producers are required to deploy Mechanical Vapor Recompression technology in crystallization units, targeting a 15% reduction in energy consumption by 2026. Major extraction regions in Sichuan and Shanxi are also investing in smart mining systems and digital twins to optimize mirabilite recovery and logistics efficiency. These initiatives collectively reinforce China’s role as both the largest producer and the most technologically advanced processor of Glauber’s salt globally, with competitiveness increasingly defined by energy intensity and downstream integration rather than reserve scale alone.

India: Textile Parks, Pharmaceutical Grade Expansion, and Circular Recovery

India’s Glauber’s salt demand profile is closely tied to textile processing, pharmaceuticals, and circular chemical recovery. The rollout of PM MITRA textile parks during 2025–2026 has embedded centralized chemical recovery infrastructure into large-scale dyeing clusters. Within these parks, Glauber’s salt is used as a leveling agent in high-volume dyeing to ensure shade consistency for export-oriented apparel manufacturing, directly linking sodium sulfate consumption to India’s textile export corridors.

Industrial investments are reinforcing higher-value applications. Vishnu Chemicals’ 2025 expansion in Telangana is upgrading capacity for pharmaceutical-grade sodium sulfate, responding to rising demand for bulk laxative formulations across Southeast Asia. At the same time, Grasim Industries under the Aditya Birla Group has implemented closed-loop recovery systems in viscose fiber plants, capturing sodium sulfate from waste streams and redirecting it into detergent manufacturing. This circularity model is reducing dependence on synthetic sulfate production and positioning Glauber’s salt as a recovered, low-cost input across multiple Indian chemical value chains.

Spain: Low-Carbon Natural Extraction and Specialty Grades for European Manufacturing

Spain has consolidated its position as Europe’s benchmark for natural sodium sulfate extraction, with Glauber’s salt increasingly marketed on sustainability credentials. In 2025, Minera de Santa Marta completed major upgrades at its Toledo and Burgos sites, optimizing solar evaporation processes to deliver low-carbon sodium sulfate tailored for eco-detergent formulations. These investments align with growing demand from European consumer goods companies seeking lower Scope 3 emissions in basic inorganic inputs.

Regulatory leadership is shaping product differentiation. Spanish producers have been early movers in updating EU REACH safety dossiers, with specific emphasis on sulfate ion discharge impacts on wastewater systems. Innovation is also extending into precision manufacturing. Sulquisa’s October 2025 launch of fine-grain anhydrous sulfate derived from Glauber’s salt is designed for high-speed automated glass lines in Germany and France, highlighting Spain’s role as a supplier of engineered sodium sulfate grades rather than bulk commodities alone.

United States: Natural Brine Supply, Pharma Demand, and Energy Storage Pilots

In the United States, Glauber’s salt demand is anchored in natural brine extraction, pharmaceuticals, and emerging energy storage applications. Searles Valley Minerals completed a USD 40 million infrastructure overhaul in California during 2025, strengthening the reliability of natural sodium sulfate supply for North American architectural and solar glass producers. This investment responds to sustained growth in domestic glass demand tied to construction and renewable energy deployment.

Pharmaceutical consumption is rising in parallel. FDA tentative approvals issued in May 2025 for generic sulfate-based colonoscopy preparations have driven a measurable increase in demand for ultra-high purity Glauber’s salt among U.S. contract manufacturers. Beyond traditional uses, the Department of Energy has identified Glauber’s salt as a viable phase change material for thermal energy storage. Pilot projects launching in early 2026 are evaluating its application in sustainable building insulation, expanding the material’s relevance beyond chemical and glass markets.

Germany: Circular By-Product Recovery and Emissions-Driven Preferences

Germany’s Glauber’s salt market is increasingly shaped by circular economy principles and tightening environmental standards. Lenzing Group’s intensified by-product valorization program in 2025 is refining sodium sulfate generated during Lyocell fiber production and supplying it to domestic textile dyeing hubs. This approach reduces waste disposal while providing a consistent source of high-purity Glauber’s salt under a closed-loop industrial model.

Regulatory dynamics favor recovery over synthesis. Late-2025 guidelines from Germany’s Federal Environment Agency prioritize natural extraction and high-efficiency recovery of sodium sulfate compared to synthetic production routes based on sulfuric acid neutralization. As a result, German end users are increasingly specifying recovered or naturally sourced Glauber’s salt in procurement contracts, reinforcing demand for traceable, low-emission supply streams across textiles and detergents.

Comparative Overview: Glauber’s Salt Industry by Country

Glauber’s Salt Market County Level Snapshot

|

Country

|

Primary Demand Drivers

|

Strategic Industry Direction

|

|

China

|

Sodium-ion batteries, solar glass

|

Energy-efficient crystallization and smart mining

|

|

India

|

Textiles, pharmaceuticals, detergents

|

Integrated textile parks and circular recovery

|

|

Spain

|

Eco-detergents, glass manufacturing

|

Low-carbon natural extraction and specialty grades

|

|

United States

|

Glass, pharmaceuticals, energy storage

|

Natural brine reliability and PCM innovation

|

|

Germany

|

Textiles, detergents

|

By-product valorization and emission-led sourcing

|

Glauber’s Salt Market Report Scope

Glauber’s Salt Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$1.9 Billion

|

|

Market Growth Rate

|

3.2%

|

|

Segments

|

By Form (Glauber’s Salt, Anhydrous Sodium Sulfate, Salt Cake), By Source (Natural Extraction, Synthetic Production, By-product Recovery), By Grade (Technical Grade, Pharmaceutical Grade, Food and Feed Grade), By Application (Detergents and Cleaners, Glass Manufacturing, Textiles and Dyeing, Pulp and Paper, Pharmaceuticals, Energy Storage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nafine Chemical Industry Group Co., Ltd., Alkim Alkali Kimya A.Ş., Minera de Santa Marta, S.A., Saskatchewan Mining and Minerals Inc., Searles Valley Minerals Inc., Lenzing AG, Vishnu Chemicals Ltd., Grasim Industries Ltd., Cooper Natural Resources, Inc., Sulquisa S.A., Nippon Chemical Industrial Co., Ltd., Jiangsu Jingshen Salt and Chemical Industry Co., Godavari Biorefineries Ltd., Elementis PLC, Sichuan Xinxing Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glauber’s Salt Market Segmentation

By Form

- Glauber’s Salt

- Anhydrous Sodium Sulfate

- Salt Cake

By Source

- Natural Extraction

- Synthetic Production

- By-product Recovery

By Grade

- Technical Grade

- Pharmaceutical Grade

- Food and Feed Grade

By Application

- Detergents and Cleaners

- Glass Manufacturing

- Textiles and Dyeing

- Pulp and Paper

- Pharmaceuticals

- Energy Storage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Glauber’s Salt Industry

- Nafine Chemical Industry Group Co., Ltd.

- Alkim Alkali Kimya A.Ş.

- Minera de Santa Marta, S.A.

- Saskatchewan Mining and Minerals Inc.

- Searles Valley Minerals Inc.

- Lenzing AG

- Vishnu Chemicals Ltd.

- Grasim Industries Ltd.

- Cooper Natural Resources, Inc.

- Sulquisa S.A.

- Nippon Chemical Industrial Co., Ltd.

- Jiangsu Jingshen Salt and Chemical Industry Co.

- Godavari Biorefineries Ltd.

- Elementis PLC

- Sichuan Xinxing Chemical Co., Ltd.

*- List not Exhaustive