Market Overview: Bleaching Agents Market Growth Driven by Hydrogen Peroxide Megaplants, Semiconductor-Grade Expansions, and Low-Carbon Processes (2025–2034)

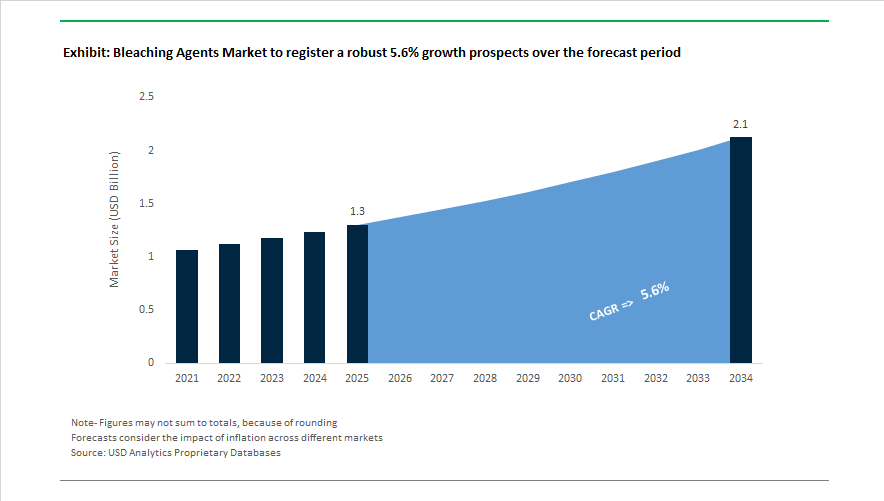

The bleaching agents market is projected to expand from USD 1.3 billion in 2025 to USD 2.1 billion by 2034, registering a CAGR of 5.6% supported by rising demand for hydrogen peroxide in pulp and paper bleaching, textile processing, water treatment, semiconductor cleaning, and sustainable polymer synthesis. Technology-driven capacity growth accelerated in 2024 when Solvay doubled electronic-grade hydrogen peroxide output at its Zhenjiang facility, strengthening supply for semiconductor cleaning and etching applications. In January 2024, Solvay partnered with INEOS Styrolution to develop hydrogen peroxide-based bleaching pathways for sustainable styrene monomer production, replacing chlorine-dependent processes. In February 2024, Kemira divested its oil and gas portfolio to focus on water solutions and fiber processing sectors where bleaching chemistry plays a central role. Carbon footprint reduction initiatives gained traction in April 2024 when Evonik introduced the carbon-neutral Way to GO2 hydrogen peroxide product line for textile and paper applications.

Industrial integration and specialty-grade production expanded through 2025. In January 2025, Evonik formed a joint venture with Fuhua Tongda Chemicals in Leshan to produce specialty hydrogen peroxide for electronics, solar panels, and aseptic packaging, with operations targeted for early 2026. In March 2025, Evonik licensed its hydrogen peroxide megaplant technology to Pingmei Shenma Group for a 200-kiloton facility supporting textile and pulp bleaching demand. Solvay also licensed high-yield hydrogen peroxide process technology in 2025 to North Huajin Chemical Industries for a 300,000-tonne propylene oxide complex, integrating bleaching intermediates into large-scale petrochemical synthesis. Regional supply strengthening occurred in Q3 2025 when Aditya Birla Chemicals secured a multi-year European export contract for bleaching agents, reinforcing India’s role in global supply.

Corporate restructuring and consolidation are shaping competitive dynamics entering 2026. In November 2025, AkzoNobel and Axalta announced a proposed merger, consolidating portfolios across coatings and chemical additives linked to bleaching and surface treatment processes. In December 2025, AkzoNobel divested its Indian subsidiary to JSW Group, sharpening its focus on higher-margin specialty chemicals. That same month, Arkema divested its plastic additives business to Praana to prioritize specialty materials and sustainable chemical solutions. Capacity expansion continued earlier in 2024 when Kemira commissioned additional bleaching production in Brazil to support Latin American pulp markets.

Regulatory and Technology-Led Trends and Opportunities in the Bleaching Agents Market

Transition Toward TCF and ECF Bleaching in Pulping Driven by AOX Regulations

Pulp and paper producers are under increasing compliance pressure to eliminate Adsorbable Organic Halides (AOX), dioxins, and organochlorine residues from effluents. The introduction of tighter AOX discharge ceilings, such as the November 2025 CPCB update setting limits at 1.0 kg per tonne, is accelerating the replacement of chlorine dioxide with Totally Chlorine-Free (TCF) and Enhanced Elemental Chlorine-Free (ECF) bleaching systems. Market conversion is being enabled by oxygen-based oxidizers, ozone sequences, and hydrogen peroxide chemistries that are compatible with low-emission pulping. A strategic inflection point occurred in January 2025, when Nouryon introduced a low-carbon hydrogen peroxide portfolio targeted to Nordic mills. The innovation was engineered for Scope 3 emission reductions, enabling high brightness pulp output with nearly 90% reduction in lifecycle carbon footprint. This development signals a maturing procurement preference for bleaching agents aligned with carbon-neutral packaging.

Stabilization of Liquid Peroxide Systems for Cold-Wash Laundry Formulations

In consumer and institutional laundry markets, low-temperature wash cycles have become mainstream due to energy efficiency targets and textile damage considerations. The bleaching agents market is experiencing demand migration away from heat-activated sodium percarbonate toward liquid hydrogen peroxide systems formulated for stability in 30–40°C wash conditions. Emerging polymer-based stabilizers and phosphonate additives are preventing peroxide decomposition caused by metal-ion interference in hard water. The expansion of detergent-grade peroxide supply, including Evonik’s mid-2025 joint venture ramp-up in Leshan, China, reflects scale-up momentum. Cold-wash compatible bleaching agents are now mission-critical in hotels, hospitals, and food-service providers seeking hygienic outcomes without thermal degradation of synthetic textiles.

Peracetic Acid Positioned as the Preferred Green Disinfectant in Water and Food Safety

Peracetic Acid (PAA) is gaining traction as a chlorine-free, fully biodegradable disinfectant and is emerging as a core growth engine in the bleaching agents market. Municipal wastewater utilities in North America and Europe began adopting PAA at scale through 2024 and 2025 for tertiary disinfection because it generates no trihalomethanes or haloacetic acids, both of which are under strict enforcement in water safety frameworks. In parallel, food-processing facilities are increasing PAA adoption following FDA approval for direct no-rinse use on meat, poultry, and fresh produce up to 500 ppm. Technical bodies like NAPSO have endorsed PAA for post-harvest treatment of crops prone to fungal decay. The alignment of PAA with organic certification frameworks strengthens its commercial relevance, giving suppliers access to high-margin food-grade chemical segments.

Sodium Hydrosulfite Demand Supported by E-Commerce Packaging and High-Yield Pulping

Sodium hydrosulfite (dithionite) remains indispensable for reductive bleaching of lignin-rich mechanical pulps used in paperboard, containerboard, and newsprint. As e-commerce packaging volumes expand, demand for high-yield pulps continues to grow, especially in Asia-Pacific economies where the transition from plastics to paper packaging is advancing at rapid scale. Sodium hydrosulfite protects mechanical fiber quality by eliminating chromophores without oxidative fiber damage, making it strategically relevant to packaging producers balancing cost, brightness, and strength specifications. Its global valuation surpassed approximately 280 million USD in 2024, underscoring its resilience compared to oxidative bleaching classes in high-volume packaging applications.

Bleaching Agents Market Share and Segmentation Insights

Market Share by Product Type: Hydrogen Peroxide Accelerates as Chlorine Alternatives Advance

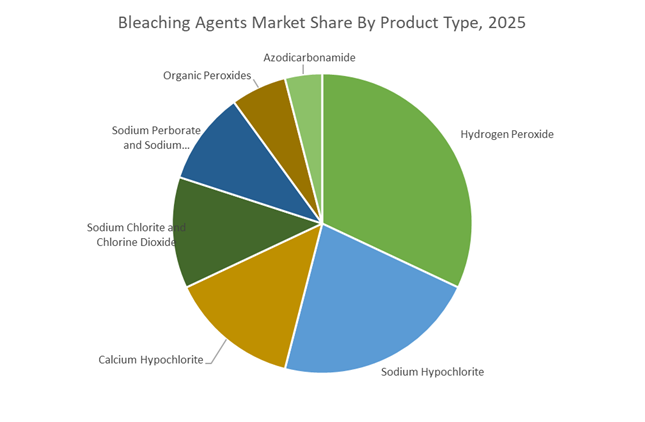

Hydrogen peroxide leads the Bleaching Agents Market with a 32% share in 2025 and is also the fastest-growing product type, favored for its environmentally benign decomposition into water and oxygen. High-strength grades dominate pulp and paper, textile bleaching, and wastewater treatment as elemental chlorine-free and total chlorine-free processes expand. Sodium hypochlorite holds the second-largest share, sustaining demand across household cleaning, industrial sanitation, and water treatment due to low cost and broad antimicrobial activity, although gradual substitution by peroxide and chlorine dioxide continues. Calcium hypochlorite remains standard in pool sanitation and municipal disinfection. Sodium chlorite and chlorine dioxide serve specialized ECF pulp bleaching and advanced water treatment. Sodium perborate and sodium percarbonate support detergent formulations, while organic peroxides such as benzoyl peroxide retain niche roles in food and pharmaceuticals. Azodicarbonamide represents the smallest segment, with regulatory pressure accelerating replacement by enzyme-based alternatives.

Market Share by End Use Industry: Pulp Leadership Balanced by Textile and Water Infrastructure Growth

Pulp and paper account for 28% of bleaching agent demand in 2025, driven by requirements for high-brightness packaging and tissue grades as graphic paper declines. Textile follows as the second-largest segment, with hydrogen peroxide dominating cotton and blended fabric processing, increasingly concentrated in Asia-Pacific amid stricter effluent regulations. Water treatment is expanding steadily, utilizing sodium and calcium hypochlorite for disinfection and chlorine dioxide for taste and odor control, supported by wastewater reuse initiatives. Household and personal care remains high-volume through bleach and oxygen-based detergents, reshaped by e-commerce and private labels. Food and beverage applications span flour, oil, and sugar refining, while healthcare relies on hydrogen peroxide and peracetic acid for sterilization. Electronics is a niche but high-growth outlet, where ultra-pure hydrogen peroxide is essential for semiconductor wafer cleaning and PCB fabrication.

Competitive Landscape Analysis of the Bleaching Agents Market

The global bleaching agents market in 2026 is defined by decarbonization mandates, semiconductor-grade purity requirements, and the transformation of pulp and water treatment chemistry toward digitalized, closed-loop systems. Competitive differentiation increasingly hinges on renewable hydrogen integration, low-carbon hydrogen peroxide production, peracetic acid sterilization systems, and AI-driven dosage optimization. Major players are investing in satellite peroxide plants, fossil-free sodium chlorate, mass balance carbon tracking, and chemicals-as-a-service models to meet ESG requirements across pulp & paper, electronics, textile, food processing, and wastewater treatment sectors. High-growth applications include sub-7nm semiconductor fabrication, cold sterilization packaging, recycled fiber brightening, and low-temperature household bleaching formulations.

Solvay leads net-zero hydrogen peroxide innovation for pulp and semiconductor markets

Solvay remains the global benchmark in high-purity hydrogen peroxide production, operating the world’s largest active oxygen network. Its INTEROX portfolio dominates pulp bleaching and electronics-grade peroxide supply, while EURECO low-temperature PAP serves concentrated detergents and personal care. In early 2026, Solvay scaled its myH2O2 satellite plant concept, installing automated peroxide units directly at pulp mills and mining sites to eliminate transport risk and carbon emissions. Under its decarbonized essential chemicals roadmap, the company is transitioning mega-plants to renewable hydrogen, targeting net-zero certified bleaching agents. Ultra-high-grade peroxide supports sub-7nm semiconductor etching required for AI chip manufacturing.

Evonik Industries expands specialty active oxygen and cold sterilization solutions in Asia

Evonik repositioned its Active Oxygens business toward high-margin specialty markets and Asian industrial growth. Through the Evonik Fuhua New Materials joint venture established in 2025, the company began supplying semiconductor- and solar-grade hydrogen peroxide in 2026. Integration of Thai Peroxide strengthened its presence in Southeast Asia’s pulp and textile sectors. Evonik also introduced advanced peracetic acid formulations engineered for cold sterilization of aseptic food packaging, enabling longer shelf life without nutrient degradation. Its pathway diversification strategy moves beyond bleaching into complex oxidation systems for wastewater treatment and chemical synthesis, reinforcing leadership in specialty active oxygen chemistry.

Nouryon pioneers low-carbon chlorine dioxide and AI-optimized pulp bleaching

Nouryon sets the industry standard for chlorine dioxide technology, supporting elemental chlorine free pulp bleaching globally. Eka HP Puroxide, scaled in 2026, represents the first low-carbon hydrogen peroxide manufactured using fossil-free hydrogen and renewable electricity. Nouryon’s integrated manufacturing model embeds bleaching plants within pulp mills, delivering chemicals as a service. Its SVP-Pure chlorine dioxide generators now incorporate AI-driven real-time brightness sensors, optimizing dosage and reducing bleach waste significantly. In 2026, the company focuses on sustainable pulping solutions, providing stabilizers that maintain high brightness in recycled fibers while preventing yellowing during post-consumer paper processing.

Kemira strengthens functional bleaching and green sodium chlorate production

Kemira specializes in water-intensive industries, bridging pulp bleaching and municipal water treatment. In February 2026, the acquisition of SIDRA Wasserchemie enhanced its European portfolio of coagulants and bleaching stabilizers. Kemira’s functional bleaching strategy enhances not only fiber brightness but also tissue strength and absorbency. The company developed a wind-powered sodium chlorate production method in Finland, marketed as the greenest bleach option for Nordic pulp producers. Through its KemConnect digital platform, Kemira uses predictive analytics to manage closed-loop water systems, delivering application-specific bleaching optimization for tissue and board manufacturers.

Arkema advances bio-based peroxides and specialty textile bleaching intermediates

Arkema refocused its portfolio in early 2026 toward specialty materials, strengthening its hydrogen peroxide and sodium chlorate operations. The company emphasizes bio-based innovation, developing organic peroxides derived from renewable oils for plant-based household cleaning products. Its Singapore platform integrates peroxide technology into bio-based transparent polyamides such as Rilsan, highlighting cross-division synergy. Arkema produces high-stability hydrogen peroxide grades tailored for textile bleaching, minimizing fiber damage during high-speed processing. By divesting legacy plastic additives, Arkema is reallocating capital toward high-purity bleaching intermediates serving medical, textile, and specialty materials markets.

BASF integrates mass balance carbon tracking into industrial bleaching powders

BASF leverages its Verbund infrastructure to manufacture inorganic bleaching agents critical to textile, food, and water treatment industries. The Blankit range includes sodium hydrosulfite and sodium metabisulfite used in industrial and home care applications. In 2026, BASF expanded mass balance carbon tracking across bleaching lines, enabling customers to procure sodium sulfite with significantly reduced product carbon footprint. The company is also developing enzyme-stabilized bleach boosters optimized for cold-water performance at 20 degrees Celsius, supporting energy-efficient laundering. With global port logistics and bulk shipping capabilities, BASF maintains cost leadership in industrial-scale bleaching powders and water treatment chemicals.

China Bleaching Agents Market: Semiconductor Purity Scaling and Regulatory-Driven Substitution

China is at the epicenter of demand bifurcation in the bleaching agents industry, balancing ultra-high purity requirements from electronics manufacturing with tightening environmental mandates in traditional industries. In September 2025, Solvay inaugurated a major expansion at its Zhenjiang site, doubling output of electronic-grade hydrogen peroxide to support advanced semiconductor cleaning and etching processes. This expansion aligns with China’s aggressive wafer fabrication and advanced node ambitions, where even trace metallic impurities in H2O2 can compromise yield. The photovoltaic sector is reinforcing this trajectory. In February 2025, the Shandong Huatai Interox Chemical facility, a Solvay joint venture, outlined plans to scale photovoltaic-grade hydrogen peroxide capacity to 48 kilotons per year, directly linked to mono- and multi-crystalline solar cell manufacturing.

Innovation infrastructure is being localized to sustain this growth. In November 2025, Nouryon opened a new innovation center in Shanghai with dedicated laboratories for cleaning and natural resources, enabling co-development of tailored bleaching solutions for Asia-Pacific customers. This is complemented by Nouryon’s announcement of an Organic Peroxides Innovation Center in Tianjin, scheduled for 2026, to accelerate polymer and bleaching formulation development. Regulatory pressure is simultaneously reshaping downstream demand. The Ministry of Ecology and Environment implemented stricter 2025–2026 effluent standards for textile dyeing, mandating a shift away from sodium hypochlorite toward hydrogen peroxide and ozone-based bleaching sequences. This regulatory substitution is structurally increasing demand for peroxide-based systems across China’s textile hubs.

United States Bleaching Agents Market: Pulp Capacity, Water Safety, and PFAS-Free Transition

The United States bleaching agents market is being driven by sustainable packaging demand, drinking water safety upgrades, and regulatory anticipation around fluorinated chemistries. In the pulp and paper sector, Kemira expanded sodium chlorate capacity at its Eastover, South Carolina facility to support long-term global demand for sustainably bleached pulp used in packaging and tissue applications. This expansion reflects a broader shift toward elemental chlorine-free and totally chlorine-free bleaching sequences.

Municipal water treatment is another structural growth vector. Under updated guidelines from the U.S. Environmental Protection Agency effective in 2025, utilities are increasingly replacing bulk chlorine gas with on-site chlorine dioxide generators to reduce trihalomethane formation and improve dosing control. At the same time, U.S. manufacturers are proactively transitioning to fluoro-free polymer processing aids as carriers for bleaching masterbatches, anticipating federal restrictions on PFAS in food-contact materials by late 2026. Hydrogen peroxide remains central to this transition. By early 2026, the U.S. hydrogen peroxide market value is projected to exceed USD 889 million, supported by its growing role as an eco-friendly disinfectant in healthcare, food processing, and clean-in-place systems.

India Bleaching Agents Market: Import Substitution and Textile-Centric Demand

India’s bleaching agents industry is characterized by rapid capacity localization and structurally strong textile demand. In August 2024, DCM Shriram commissioned a new hydrogen peroxide plant in Jhagadia, Gujarat, with 52,500 tonnes per year capacity. This investment materially reduces reliance on imports for paper and textile bleaching and improves supply security for domestic processors.

Textiles remain the dominant demand driver. As a core node in the Asia-Pacific textile value chain, India accounts for a substantial share of the region’s roughly 65% contribution to global textile bleaching chemical consumption. The industry is steadily shifting toward peroxide-based whitening agents due to lower effluent toxicity and compatibility with zero-liquid-discharge norms. Policy support reinforces this shift. Under the Production Linked Incentive scheme, the government has prioritized chlor-alkali derivatives, providing a strategic tailwind for domestic sodium hypochlorite producers while encouraging modernization and environmental compliance across bleaching operations.

Thailand and Southeast Asia Bleaching Agents Market: Capacity Consolidation and Regional Supply Build-Out

Southeast Asia is emerging as a strategically important bleaching agents production and consumption zone, supported by acquisitions and greenfield infrastructure. In March 2025, Evonik Industries completed the acquisition of Thai Peroxide Co. Ltd., significantly strengthening its position in specialty bleaching chemicals and peracetic acid across the region. This move enhances supply reliability for food processing, healthcare, and water treatment applications in Thailand and neighboring markets.

Capacity expansion is extending beyond Thailand. In June 2024, Nuberg EPC secured a contract to build a 40,000 MTPA hydrogen peroxide plant for PT Sulfindo Adiusaha in Indonesia. This facility addresses growing regional demand from industrial bleaching, mining, and municipal water treatment, reducing dependence on imports and improving responsiveness to local regulatory requirements.

Germany and the European Union Bleaching Agents Market: Logistics Optimization and Green Hydrogen Integration

In Germany and across the European Union, the bleaching agents industry is increasingly shaped by decarbonization and transport regulation. During 2025, producers such as Kemira and Evonik Industries increased the share of powdered bleaching formulations in their portfolios. These products lower freight-related emissions, reduce water transport, and simplify compliance with ADR hazardous materials regulations, offering both environmental and logistical advantages.

Process decarbonization is advancing in parallel. Major German chemical clusters are integrating green hydrogen into the anthraquinone process used for hydrogen peroxide synthesis, targeting a 25% reduction in Scope 1 and 2 emissions by late 2026. This transition positions European suppliers to meet tightening carbon disclosure and procurement standards from pulp, paper, and textile customers seeking lower embedded emissions in bleaching chemicals.

Country-Level Strategic Snapshot: Bleaching Agents Industry

Bleaching Agents Market County Level Snapshot

|

Country / Region

|

Strategic Orientation

|

Key 2024–2026 Developments

|

|

China

|

Electronic-grade purity and effluent compliance

|

Semiconductor and PV-grade H2O2 expansions, textile shift to peroxide and ozone

|

|

United States

|

Sustainable pulp and water safety

|

Sodium chlorate expansion, ClO2 adoption, PFAS-free processing transition

|

|

India

|

Import substitution and textile dominance

|

New H2O2 capacity, peroxide-based whitening, PLI support

|

|

Thailand / Southeast Asia

|

Regional consolidation and capacity build

|

Evonik acquisition, Indonesian H2O2 greenfield plant

|

|

Germany / EU

|

Decarbonization and logistics efficiency

|

Powdered formulations, green hydrogen integration

|

Bleaching Agents Market Report Scope

Bleaching Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2034)

|

$2.1 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Type (Azodicarbonamide, Hydrogen Peroxide, Sodium Hypochlorite, Sodium Chlorite and Chlorine Dioxide, Calcium Hypochlorite, Sodium Perborate and Sodium Percarbonate, Organic Peroxides), By Form (Liquid, Powder), By Grade (Industrial Grade, Food Grade, Electronic Grade, Pharmaceutical Grade), By End Use Industry (Pulp and Paper, Textile, Water Treatment, Healthcare, Electronics, Food and Beverage, Household and Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Solvay, Evonik Industries, Nouryon, Arkema, Kemira, Dow, BASF, Mitsubishi Gas Chemical, Hansol Chemical, Aditya Birla Chemicals, DCM Shriram, Olin Corporation, ERCO Worldwide, PeroxyChem, Guangdong HEC Technology

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bleaching Agents Market Segmentation

By Product Type

- Azodicarbonamide

- Hydrogen Peroxide

- Sodium Hypochlorite

- Sodium Chlorite and Chlorine Dioxide

- Calcium Hypochlorite

- Sodium Perborate and Sodium Percarbonate

- Organic Peroxides

By Form

By Grade

- Industrial Grade

- Food Grade

- Electronic Grade

- Pharmaceutical Grade

By End Use Industry

- Pulp and Paper

- Textile

- Water Treatment

- Healthcare

- Electronics

- Food and Beverage

- Household and Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bleaching Agents Industry

- Solvay

- Evonik Industries

- Nouryon

- Arkema

- Kemira

- Dow

- BASF

- Mitsubishi Gas Chemical

- Hansol Chemical

- Aditya Birla Chemicals

- DCM Shriram

- Olin Corporation

- ERCO Worldwide

- PeroxyChem

- Guangdong HEC Technology

*- List not Exhaustive