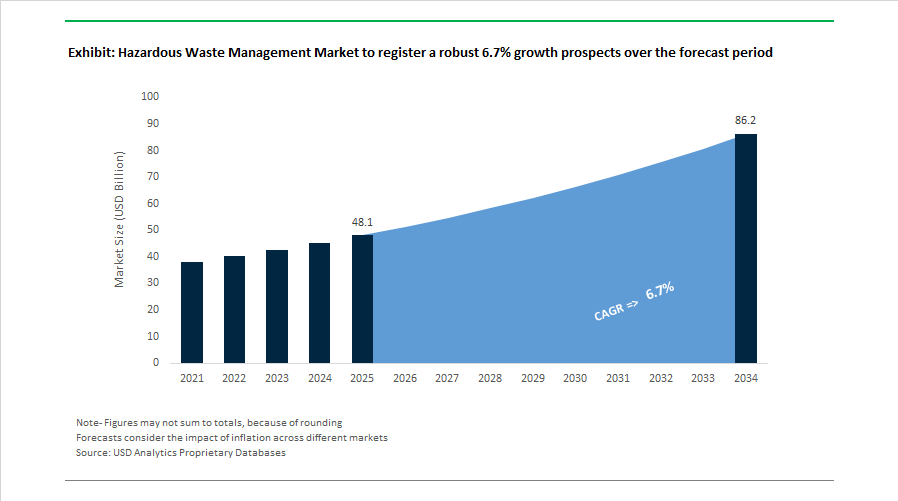

Hazardous Waste Management Market to Reach $86.2 Billion by 2034 at 6.7% CAGR Driven by PFAS Regulation, Healthcare Waste Consolidation, and Circular Infrastructure Investment

The Hazardous Waste Management Market is projected to grow from $48.1 billion in 2025 to $86.2 billion by 2034, registering a CAGR of 6.7%. Market expansion is supported by tightening PFAS regulations, rising medical and industrial waste volumes, stricter Extended Producer Responsibility frameworks, and accelerated investment in recycling and advanced thermal treatment infrastructure. Consolidation among major environmental services providers and increasing deployment of high-efficiency treatment, storage, and disposal facilities are reshaping competitive positioning across North America, Europe, and emerging Asian markets.

In March 2024, Clean Harbors, Inc. completed the $400 million acquisition of HEPACO, expanding its environmental and emergency response footprint across more than 40 regional service locations in the Eastern United States. In April 2024, Clean Harbors launched its Total PFAS Solution platform, offering integrated sampling, transportation, and thermal destruction services to meet evolving EPA regulatory standards on per- and polyfluoroalkyl substances. In November 2024, Waste Management, Inc. finalized its $7.2 billion acquisition of Stericycle, Inc., significantly strengthening its presence in medical and hazardous healthcare waste incineration and compliance services. In October 2024, the Global Framework on Chemicals issued its first project call to fund hazardous waste infrastructure in developing economies, expanding opportunities for multinational waste contractors.

Regulatory modernization and technology deployment intensified in 2025. In March 2024, India revised its Hazardous and Other Wastes Rules to enhance digital manifest tracking and impose stricter Extended Producer Responsibility obligations on industrial waste generators. In June 2025, Veolia Environnement S.A. inaugurated a major PFAS treatment plant in Delaware, providing advanced resin filtration and carbon regeneration services to over 100,000 residents. The same month, Veolia introduced its Drop® PFAS destruction technology in Europe, claiming a 99.9999% elimination rate for targeted contaminants, positioning the company at the forefront of hazardous chemical remediation. In 2025, Veolia also confirmed near-completion of its advanced rotary kiln incinerator in Gum Springs, Arkansas, with industrial capacity largely pre-contracted.

Market consolidation and circular economy investments accelerated into 2026. In September 2025, Clean Harbors reported achieving its 2030 recycling target five years early, recycling 1.9 million metric tons of materials in 2024 through expanded used oil, solvent, and e-scrap recovery operations. In November 2025, Veolia North America signed a definitive agreement to acquire Clean Earth from Enviri Corporation for $3.04 billion, a transaction expected to close in mid-2026 and add 19 TSDF facilities, elevating Veolia to the second-largest hazardous waste operator in the United States. Republic Services, Inc. continued scaling its Polymer Centers network through 2026 following its acquisition of US Ecology, shifting revenue toward specialty recycling and recovered resin markets. Waste Management confirmed in its 2025 Sustainability Report that it remains on track to complete $3 billion in sustainability growth investments by 2026, including renewable natural gas facilities and advanced recycling systems supporting specialty and industrial material recovery.

The Hazardous Waste Management Market landscape reflects heightened PFAS liability enforcement, healthcare waste consolidation, EPR-driven compliance frameworks, digital tracking mandates, rotary kiln and advanced incineration investments, and rapid growth in specialty recycling infrastructure. Competitive differentiation increasingly depends on integrated PFAS treatment capabilities, TSDF network density, advanced thermal destruction efficiency, circular economy platform expansion, regulatory compliance expertise, and capital deployment into renewable and specialty material recovery assets across global markets.

Hazardous Waste Management Market Trends and Strategic Opportunities

Strategic Regionalization of High-Temperature Thermal Treatment Capacity

The hazardous waste management market is undergoing a structural shift toward regionalized treatment infrastructure as governments tighten oversight on transboundary waste movement and progressively restrict hazardous landfilling. Regulatory pressure across North America, Europe, and parts of Asia is accelerating investment in localized high-temperature thermal treatment assets, including advanced incineration and cement kiln co-processing facilities. These technologies are increasingly viewed as indispensable for the safe destruction of complex chemical residues, infectious medical waste, and persistent organic pollutants.

Capital intensity reflects the strategic importance of this trend. Modern hazardous waste incinerators equipped with integrated air pollution control systems require capital investments ranging from 15 million to 100 million dollars per facility. According to United Nations Industrial Development Organization, industrial zones in developing economies alone will require close to 850 million dollars in dedicated hazardous waste infrastructure investment over the next decade to meet international compliance benchmarks. Capacity is also consolidating geographically. In November 2025, Veolia completed a 3 billion dollar acquisition of Clean Earth, doubling its U.S. footprint to 82 specialized treatment sites. This acquisition establishes a nationwide network designed to deliver localized, high-purity waste destruction services to advanced manufacturing sectors such as semiconductors and pharmaceuticals.

Thermal treatment technologies currently account for roughly 40% of the hazardous waste treatment mix, driven by their ability to achieve 99.99% destruction efficiency for persistent organic pollutants and regulated healthcare waste streams. Post-pandemic growth in infectious medical waste, expanding at an estimated 8.7% compound annual rate, is further reinforcing the strategic value of regional thermal destruction capacity.

Mandatory Digitalization and Real-Time Compliance Ecosystems

The second major trend reshaping the hazardous waste management market is the regulatory-driven transition from paper-based documentation to fully digital, real-time compliance systems. Governments are mandating end-to-end digital tracking of hazardous waste to improve transparency, prevent illegal dumping, and strengthen enforcement across the waste lifecycle.

A key inflection point occurred in April 2025 with the implementation of the United Kingdom’s mandatory digital waste tracking regime, which replaced physical transfer notes with centralized electronic records. All entities handling controlled waste are now required to log waste movements digitally, with non-compliance subject to uncapped financial penalties in certain jurisdictions. Similar digitalization initiatives are being rolled out across the European Union and select U.S. states, creating a de facto global standard for traceability.

Service providers are responding by embedding advanced software into their operations. Companies such as Clean Harbors are integrating AI-enabled compliance platforms built on cloud infrastructure to automate manifesting, reporting, and regulatory audits. These systems leverage GIS mapping, blockchain-based record immutability, and real-time sensor data, delivering operational efficiency improvements of up to 25% at treatment and incineration facilities. The digital hazardous waste solutions market, valued at 2.92 billion dollars in 2024, is also enhancing logistics efficiency through IoT-enabled container monitoring and predictive route optimization, reducing fuel consumption and lowering total collection costs for hazardous waste operators.

On-Site Destructive Treatment for PFAS-Contaminated Media

The regulatory crackdown on per- and polyfluoroalkyl substances is creating one of the most significant growth opportunities in the hazardous waste management market. The April 2024 finalization of national drinking water standards by the Environmental Protection Agency, setting maximum contaminant levels of 4.0 parts per trillion for PFOA and PFOS, has triggered widespread deployment of PFAS capture systems. This, in turn, is generating concentrated secondary waste streams such as spent carbon, resins, and brines that require permanent destruction rather than disposal.

Updated federal guidance during 2024 and 2025 prioritizes high-temperature thermal treatment above 1,100 degrees Celsius and Subtitle C hazardous waste landfills to minimize PFAS release risks. Emerging destructive technologies such as supercritical water oxidation and advanced pyrolysis are gaining regulatory recognition as promising solutions. In mid-2025, Veolia introduced its patented Drop technology in Europe, capable of achieving destruction efficiencies approaching 99.9999% for targeted PFAS compounds. This level of performance is increasingly critical as thousands of municipal water systems begin remediation to comply with new standards.

The addressable market is substantial. The municipal drinking water PFAS treatment segment alone is projected to reach 2.26 billion dollars by 2035, expanding at a compound annual rate above 20% from 2025. This demand is amplified by the designation of PFOA and PFOS as hazardous substances under CERCLA, which shifts long-term remediation liability to polluters and ensures sustained demand for certified destructive treatment services.

Integrated Hazardous Waste Solutions for EV Battery Gigafactories

The rapid global expansion of lithium-ion battery gigafactories is creating a parallel opportunity for hazardous waste management providers capable of delivering integrated, on-site chemical and materials handling solutions. Battery manufacturing generates hazardous solvent streams, particularly N-methyl-2-pyrrolidone, as well as large volumes of production scrap containing valuable metals.

In 2024, production scrap accounted for more than 54% of total EV battery recycling activity, underscoring the scale of recoverable material generated before batteries ever reach end-of-life. Hazardous waste operators are increasingly embedding on-site recovery systems to reclaim lithium, cobalt, and nickel at purities exceeding 99.6%, enabling immediate reintegration into new cell production. This closed-loop model improves supply security while reducing the environmental footprint of battery manufacturing.

Operational complexity favors established players. Damaged or defective high-voltage battery packs, classified as Class 9 hazardous goods, carry collection and handling costs 40 to 60% higher than conventional scrap. This has concentrated market share among providers that own permitted treatment, storage, and disposal facilities and maintain specialized fire-resistant logistics fleets. Solvent recovery services are emerging as a critical differentiator. In its February 2025 regulatory filing, Clean Harbors highlighted growing demand from EV battery and semiconductor manufacturers for customized solvent recycling and emergency response capabilities. As gigafactory capacity scales globally, integrated hazardous waste management is becoming a strategic enabler of safe, compliant, and cost-efficient electrification supply chains.

Hazardous Waste Management Market Share and Segmentation Insights

Liquid Hazardous Waste Leads the Hazardous Waste Management Market Due to Industrial Wastewater and Chemical Streams

Liquid Hazardous Waste accounted for 42.80% of the Hazardous Waste Management Market share in 2025, making it the largest waste type managed within the global hazardous waste treatment industry. Industrial operations generate substantial volumes of contaminated aqueous streams, spent solvents, oily wastewater, chemical processing liquids, and acid or alkaline effluents, all of which require specialized treatment before discharge or disposal. Conventional municipal wastewater treatment facilities typically lack the capability to handle these hazardous liquids safely, necessitating dedicated hazardous waste treatment infrastructure. As a result, specialized treatment technologies such as chemical neutralization, advanced oxidation processes, membrane filtration, solvent recovery, and thermal treatment systems are widely deployed to process liquid hazardous waste streams. In 2025, the sector is increasingly integrating water reclamation and resource recovery technologies within hazardous liquid waste treatment facilities. Advanced treatment plants are capable of recovering valuable chemicals including solvents, acids, and industrial reagents, while also producing reclaimed water suitable for industrial reuse, enabling companies to reduce disposal volumes while improving environmental sustainability and operational economics.

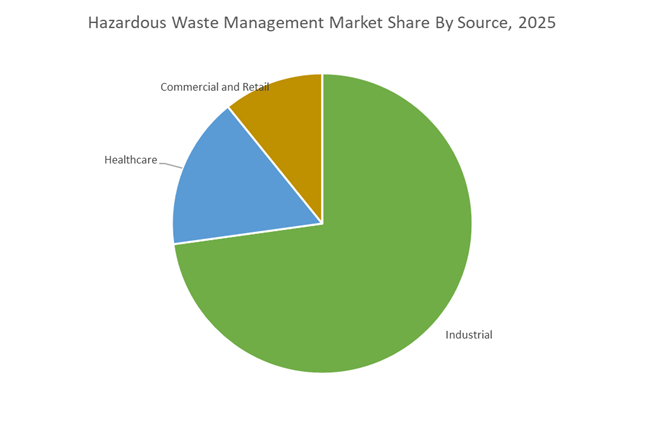

Industrial Sector Drives the Largest Generation of Hazardous Waste in Global Waste Management Systems

Industrial sources represented 72.80% of the Hazardous Waste Management Market share in 2025, establishing manufacturing and heavy industry as the primary generators of hazardous waste globally. Industrial sectors such as chemical manufacturing, petroleum refining, pharmaceuticals, metal finishing, electronics production, and industrial coatings produce a diverse range of hazardous waste streams including spent solvents, heavy metal-containing sludge, corrosive acids and bases, toxic chemical residues, and contaminated process water. The scale and complexity of these waste streams require specialized treatment, storage, transportation, and disposal systems managed by licensed hazardous waste service providers. In 2025, the industrial sector is increasingly adopting circular economy strategies in hazardous waste management, shifting focus from disposal toward resource recovery and waste valorization. Industrial companies are partnering with waste management firms to recover solvents for reuse, extract valuable metals from sludge, and convert hazardous waste into energy through waste-to-energy technologies. Additionally, many manufacturers are implementing on-site treatment systems and closed-loop recycling processes, enabling them to reduce hazardous waste generation at the source while improving sustainability performance metrics and regulatory compliance.

Competitive Landscape in the Hazardous Waste Management Market

The Hazardous Waste Management Market is highly consolidated, with leading environmental services companies expanding through strategic acquisitions, advanced treatment technologies, PFAS remediation capabilities, and circular economy infrastructure. Major players such as Veolia, Clean Harbors, Waste Management, Republic Services, and SUEZ are strengthening their market positions through TSDF capacity expansion, AI-driven logistics, resource recovery technologies, and large-scale hazardous waste treatment networks.

Veolia Expands Hazardous Waste Leadership Through Clean Earth Acquisition and PFAS Treatment Infrastructure

Veolia Environnement S.A. continues to strengthen its global leadership in the hazardous waste management market through its GreenUp strategic plan (2024–2027), positioning itself as a key provider of ecological transformation services. In a major strategic move scheduled for 2026, Veolia will complete the $3 billion acquisition of Clean Earth from Enviri Corporation, effectively doubling its hazardous waste footprint in the United States by adding 19 EPA-permitted Treatment, Storage, and Disposal Facilities (TSDFs) and more than 700 operating permits. The company also inaugurated a state-of-the-art hazardous waste incinerator in Gum Springs, Arkansas, capable of high-temperature destruction of complex waste streams including PFAS compounds under its “BeyondPFAS” service line. With over 350 proprietary environmental technologies, Veolia reported a 3.3% revenue increase in its European hazardous waste division in 2025, while advancing circular economy initiatives that recovered 6.5 million tons of recyclable materials and targeting 8.7 million metric tons of pollutants treated annually.

Clean Harbors Strengthens North American Hazardous Waste Disposal Network with PFAS and Logistics Innovation

Clean Harbors, Inc. remains the largest hazardous waste disposal company in North America, maintaining a significant competitive moat through its extensive network of incinerators, secure landfills, and technical services infrastructure. The company has established strong leadership in the rapidly expanding PFAS remediation market, reporting 20% revenue growth from PFAS-related services in 2025, with a project pipeline expanding 15% to 20% each quarter. To support operational expansion, Clean Harbors announced a $50 million strategic investment between 2025 and 2026 to expand the Safety-Kleen Environmental vacuum truck fleet, projected to generate $12 million to $14 million in incremental EBITDA. In January 2026, the company also agreed to acquire environmental businesses from Depot Connect International (DCI) for approximately $130 million, adding wastewater treatment and railcar cleaning capabilities. Additionally, Clean Harbors is deploying AI-driven route optimization and IoT sensor networks across its fleet of more than 15,000 vehicles, improving hazardous materials tracking and operational efficiency.

Waste Management Accelerates Special Waste and Circular Resource Recovery Capabilities

Waste Management, Inc. (WM) is strategically expanding its presence in the industrial and hazardous waste services segment, leveraging its vast North American waste management infrastructure and landfill network. In early 2026, WM reported record operating leverage in its collection and disposal operations due to the adoption of automated waste profiling systems and advanced data analytics, enabling the company to prioritize high-value hazardous waste streams over lower-margin residential volumes. WM has also invested $40 million in an organics recycling facility in Texas, launched between late 2024 and early 2025, with the capacity to process 100,000 tons of organic waste annually, converting landfill byproducts into Renewable Natural Gas (RNG). As part of its sustainability strategy, the company deployed electric vehicle infrastructure across more than 20 facilities by 2025, supporting a transition toward zero-emission heavy-duty waste fleets by 2030. WM’s Special Waste division is also experiencing increased demand for coal ash disposal and soil remediation projects, utilizing its Subtitle C and Subtitle D landfill assets.

Republic Services Strengthens Environmental Solutions Platform with Circular Plastics and Emergency Response

Republic Services, Inc. has emerged as a key player in the hazardous waste management and environmental services market, expanding through its integrated Environmental Solutions platform. The company is advancing its climate leadership strategy, targeting a 40% increase in circular material recovery by 2030, while maintaining strong operational performance with a Total Recordable Incident Rate (TRIR) below 2.0 during 2024–2025, a critical benchmark for industrial hazardous waste contracts. Republic Services also operates as a U.S. Coast Guard-certified Oil Spill Response Organization (OSRO), providing 24/7 emergency response for environmental incidents across North American waterways, integrated with its hazardous chemical stabilization and storage facilities. The company is investing heavily in its Polymer Center–Blue Polymers recycling network, enabling the recovery of complex plastic waste streams that previously lacked recycling pathways. Additionally, Republic manages a broad portfolio of liquid waste stabilization systems and leachate treatment facilities, protecting groundwater while enabling industrial water reuse and environmental remediation.

SUEZ Expands Global Hazardous Waste Treatment with Heavy Metal Remediation and Solvent Recycling Projects

SUEZ continues to maintain a strong position in the global hazardous waste management market, particularly across Europe and Asia, where it focuses on industrial waste remediation, solvent recovery, and high-temperature treatment technologies. In January 2026, a SUEZ-led consortium secured a RMB 110 million contract for a hexavalent chromium contamination risk-mitigation project in Chongqing, China, targeting polluted industrial sites along the Yangtze River basin. The company further strengthened its circular solvent recycling capabilities through a RMB 170 million investment in Chongqing, enabling industries to recover and reuse high-purity organic solvent precursors. In partnership with PYREG, SUEZ is deploying the Pyrolis® S2B pyrocarbonisation technology, which converts hazardous sewage sludge into biochar, simultaneously enabling carbon sequestration and pathogen neutralization. Supporting these initiatives is SUEZ’s Global Technical Centre of Excellence, which oversees more than 350 proprietary technologies for hazardous waste incineration, chemical-physical treatment, and advanced industrial waste processing.

China: Digital Enforcement and Structural Shift Away from Landfilling

China’s hazardous waste management industry is entering a decisive enforcement and infrastructure transformation phase, anchored in digital governance and long-term treatment realignment. In February 2025, the Ministry of Ecology and Environment announced a mandatory digital-first management framework requiring all key hazardous waste facilities to implement full-process digital monitoring by late 2026. This includes real-time GPS tracking of waste movement, automated manifest reconciliation, and centralized data reporting. The policy directly targets illegal dumping and misrouting, long-standing risks in industrial waste handling across chemical, metallurgical, and manufacturing clusters.

Infrastructure strategy is being reshaped through the draft 15th Five-Year Plan released in late 2025, which sets an explicit target to restrict hazardous waste landfilling to under 10% of total treatment by 2030. This is accelerating capital deployment into plasma gasification, rotary kiln incineration, and other high-temperature destruction technologies capable of handling persistent organic pollutants and complex residues. Regulatory consolidation is reinforcing this direction. A draft Ecology and Environment Law Code issued in April 2025 introduces a phaseout pathway for obsolete industrial processes that generate high volumes of POPs, effectively tightening upstream waste generation controls alongside downstream treatment.

Operational resilience is another policy priority. By 2026, municipal governments are required to establish integrated medical waste disposal systems combining centralized treatment with on-site solutions for remote regions. At the same time, China is selectively enabling circular pathways. The 2025 “Exemption List” allows certain hazardous streams, including HW08 waste mineral oils and HW34 waste acids, to be reclassified as general solid waste if utilization criteria are met. This regulatory flexibility is incentivizing investment in regeneration, recovery, and resource transformation technologies within the hazardous waste management value chain.

United States: Data Modernization, Compliance Accessibility, and Market Consolidation

The United States hazardous waste management landscape is being reshaped by regulatory digitalization, compliance simplification, and accelerated industry consolidation. In September 2025, the U.S. Environmental Protection Agency officially launched the Hazardous Waste Information Platform, replacing the legacy RCRAInfo system. HWIP introduces advanced geospatial search, integrated data visualization, and streamlined reporting workflows, materially improving traceability across more than 35 million tons of hazardous waste generated annually. This platform enhances enforcement efficiency while reducing administrative friction for generators and treatment operators.

To support compliance at the mid-market level, the EPA relaunched its Guidance Portal in August 2025 as a centralized access point for active Resource Conservation and Recovery Act documentation. This initiative is particularly relevant for small and medium enterprises navigating evolving hazardous waste classifications, accumulation rules, and disposal requirements. Regulatory attention is also intensifying around emerging contaminants. In 2025, the EPA introduced a consolidated “one-stop” resource hub for hazardous waste cleanups, with new guidance addressing PFAS disposal pathways and waste streams such as discarded e-cigarette components.

Commercial dynamics are evolving in parallel. The first half of 2025 marked a rebound in mergers and acquisitions, highlighted by Radius Recycling’s USD 1.3 billion acquisition and continued expansion by players such as GFL Environmental and Waste Connections. Strategic focus is shifting toward specialized remediation services and IT Asset Disposition capabilities, reflecting rising demand for secure handling of complex, high-liability waste streams. Collectively, these developments position the U.S. market around digital transparency, compliance scalability, and portfolio-driven growth.

India: Fiscal Accountability and Real-Time Emissions Oversight

India’s hazardous waste management industry is transitioning toward outcome-based governance, real-time monitoring, and innovation-led remediation. The Union Government’s Outcome Budget for 2025–26 introduced measurable performance indicators for the Hazardous Substances Management Division, with targeted allocations for expanding Common Bio-Medical Waste Treatment Facilities in urban and semi-urban hubs such as Kochi. This approach ties public spending directly to treatment capacity expansion and operational effectiveness.

Regulatory oversight is tightening at the facility level. As of early 2025, the Central Pollution Control Board mandated Online Continuous Emission Monitoring Systems for all waste-to-energy plants. These systems track toxic metal concentrations in incineration ash and flue gases in real time, strengthening enforcement against secondary pollution risks associated with hazardous waste combustion. Innovation is being actively encouraged. The HSM Division is funding private startups through challenge-based initiatives to develop solutions for hazardous micro-plastics and complex chemical waste, with organizations such as the Climate Collective Foundation involved in early-stage deployment.

Fiscal instruments are also being introduced to support remediation. The Health Security and National Security Cess Act, 2026 establishes new levies on industrial waste generators, with proceeds earmarked for national environmental cleanup and hazardous waste infrastructure projects. Together, these measures signal a shift toward accountability-driven growth, where regulatory compliance, fiscal responsibility, and private-sector innovation converge.

European Union: Substance Transparency and Circular Control Enforcement

At a regional level, the European Union is redefining hazardous waste management through stricter substance controls, digital traceability, and reinforced circular economy safeguards. Regulation (EU) 2025/40 on Packaging and Packaging Waste, published in early 2025 and effective from August 12, 2026, introduces a 100 ppm limit on heavy metals including lead, cadmium, and mercury, alongside comprehensive bans on PFAS in food-contact packaging. These thresholds significantly elevate compliance requirements for packaging producers and downstream waste handlers.

Further structural tightening came with the revised Waste Framework Directive entering into force in October 2025. The directive mandates official sorting of separately collected textiles prior to shipment, preventing hazardous or contaminated materials from being misclassified as reusable exports. This has direct implications for hazardous waste identification, cross-border shipment controls, and enforcement consistency across member states. Looking ahead, the European Commission is authorized to adopt digital marking technologies by August 2026 to identify substances of concern in packaging waste. This digital traceability layer is expected to materially enhance sorting accuracy, regulatory audits, and chemical risk management across the EU hazardous waste ecosystem.

Summary Table: Country and Regional Policy Signals in Hazardous Waste Management

Hazardous Waste Management Market County Level Snapshot

|

Geography

|

Primary Policy Lever

|

Strategic Focus Area

|

Market Signal

|

|

China

|

Digital monitoring mandate, Five-Year Plan targets

|

High-temperature treatment, circular utilization

|

Enforcement-led infrastructure investment

|

|

United States

|

HWIP platform, EPA guidance consolidation

|

Data transparency, M&A-driven scale

|

Compliance efficiency and portfolio expansion

|

|

India

|

Outcome budgeting, OCEMS mandate

|

Biomedical waste, WTE oversight

|

Accountability and innovation funding

|

|

European Union

|

PPWR, Waste Framework Directive

|

Substance traceability, textile control

|

Circular economy enforcement

|

Hazardous Waste Management Market Report Scope

Hazardous Waste Management Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$48.1 Billion

|

|

Market Size (2034)

|

$86.2 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Waste Type (Solid Hazardous Waste, Liquid Hazardous Waste, Sludge, Specialized Hazardous Waste), By Treatment Method (Thermal Treatment, Chemical Treatment, Physical and Physicochemical Treatment, Biological Treatment), By Disposal Method (Land Burial, Deep Well Injection, Engineered Storage, Energy Recovery), By Source (Industrial, Healthcare, Commercial and Retail)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Clean Harbors, Inc., Veolia Environnement S.A., Waste Management, Inc., Suez S.A., Republic Services, Inc., Remondis SE & Co. KG, Bealson & Co., Biffa plc, Enviri Corporation, Tradebe Environmental Services, Seche Environnement, Cleanaway Waste Management Ltd., Triumvirate Environmental, US Ecology, Inc., Halenke & Co.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hazardous Waste Management Market Segmentation

By Waste Type

- Solid Hazardous Waste

- Liquid Hazardous Waste

- Sludge

- Specialized Hazardous Waste

By Treatment Method

- Thermal Treatment

- Chemical Treatment

- Physical and Physicochemical Treatment

- Biological Treatment

By Disposal Method

- Land Burial

- Deep Well Injection

- Engineered Storage

- Energy Recovery

By Source

- Industrial

- Healthcare

- Commercial and Retail

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hazardous Waste Management Market

- Clean Harbors, Inc.

- Veolia Environnement S.A.

- Waste Management, Inc.

- Suez S.A.

- Republic Services, Inc.

- Remondis SE & Co. KG

- Bealson & Co.

- Biffa plc

- Enviri Corporation

- Tradebe Environmental Services

- Seche Environnement

- Cleanaway Waste Management Ltd.

- Triumvirate Environmental

- US Ecology, Inc.

- Halenke & Co.

*- List not Exhaustive