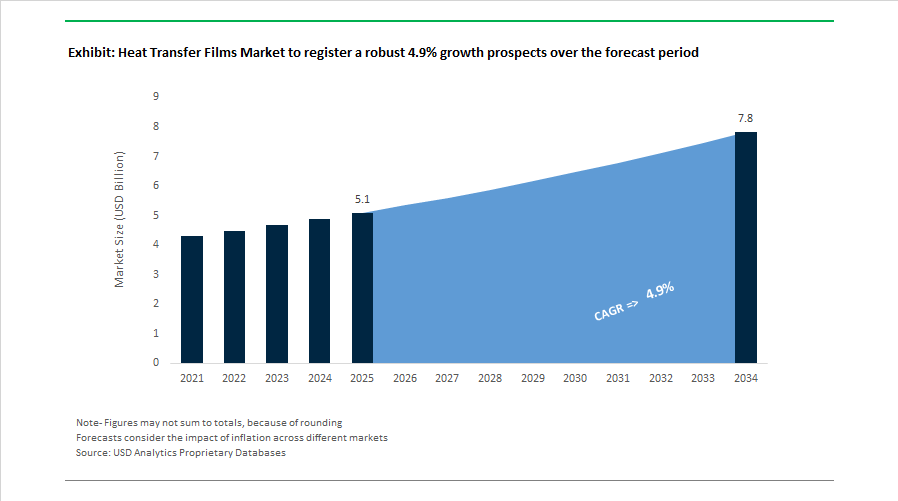

Heat Transfer Films Market to Reach $7.8 Billion by 2034 at 4.9% CAGR Fueled by DTF Printing, Sustainable Film Innovation, and Advanced Protective Coatings

The Heat Transfer Films Market is projected to grow from $5.1 billion in 2025 to $7.8 billion by 2034, registering a CAGR of 4.9%. Expansion is driven by rapid adoption of Direct-to-Film (DTF) technology, rising demand for premium textile branding solutions, growth in automotive paint protection films (PPF), and the transition toward PVC-free and recyclable film substrates. Heat transfer vinyl (HTV), dye-sublimation media, overlaminates, and specialty polyurethane films are increasingly engineered for superior wash durability, color vibrancy, stretch resistance, and sustainability compliance across apparel, signage, packaging, and transportation applications.

In October 2024, Chemica introduced Sublok Revolution, a specialized flex film designed to block dye migration on sublimated polyester sportswear, addressing ink bleeding issues common in high-performance textiles. In late 2024 and through 2025, 3M rolled out its upgraded Scotchgard™ Paint Protection Film Pro Series featuring enhanced self-healing capability and integrated UV resistance for automotive applications. In January 2025, Chemica expanded its portfolio with the Tex’Touch premium range, delivering a textured twill finish for sports logos and high-end branding. The same month, STAHLS' launched its 2025 Heat Printing Heroes catalog, upgrading UltraColor MAX™ DTF transfers with EasyRip™ functionality to streamline high-detail, full-color applications.

Technology migration toward DTF accelerated through 2025 and 2026. In April 2025, Avery Dennison showcased a PVC-free overlaminate at the ISA International Sign Expo, reinforcing the industry’s shift toward eco-friendly graphics films. In April 2025, TransTech Group completed the acquisition of Koch Heat Transfer assets, consolidating TWISTED TUBE® and BROWN FINTUBE® brands and strengthening thermal engineering capabilities supporting film and heat exchange technologies. In July 2025, Dai Nippon Printing developed a mono-material polypropylene film lid for pharmaceutical PTP packaging, replacing aluminum foil with a recyclable heat-resistant alternative. In September 2025, Insta Graphic Systems debuted a comprehensive DTF transfer system, enabling decorators to produce fine-detail transfers with improved wash durability and soft hand-feel.

Sustainability and geographic expansion remained central themes. In late 2024 into 2025, Siser launched PureHT™, marketed as the first compostable heat transfer vinyl aligned with circular fashion objectives. In December 2025, Dai Nippon Printing established DNP Corporation India and DNP Imagingcomm India in New Delhi, commencing operations in March 2026 to expand dye-sublimation thermal transfer media across South Asia. In February 2026, M&R Printing Equipment introduced the Stinger series and expanded into DTF equipment, establishing dedicated film consumable supply chains in the U.S. and Poland. In November 2025, 3M announced its 2025–2027 innovation strategy targeting 1,000 product launches, with a significant focus on Transportation & Electronics film technologies.

The Heat Transfer Films Market trajectory reflects premium textile customization, hybrid digital-print workflows, recyclable mono-material packaging films, self-healing automotive protection layers, compostable HTV materials, and regional manufacturing expansion in Asia. Competitive positioning increasingly depends on high-definition DTF capabilities, PVC-free formulations, UV and abrasion resistance performance, supply chain localization, and sustainability-driven material science innovation across apparel, signage, pharma packaging, and mobility segments.

Heat Transfer Films Market Trends and Strategic Opportunities

Migration to Mono-Material Packaging and Design for Recycling Compliance

The heat transfer films market is increasingly shaped by the packaging industry’s transition toward mono-material structures that support recyclability and regulatory compliance. Brand owners in e-commerce and retail are moving away from multi-layer laminates that combine incompatible polymers, inks, and adhesives. Heat transfer films enable graphics, branding, and functional coatings to be applied directly onto polyethylene or polypropylene substrates, eliminating separate pressure-sensitive labels and simplifying recycling at end of life. This design-for-recycling approach aligns with mechanical recycling infrastructure already established across Europe and North America.

Life-cycle assessments released in 2024 by the European Commission indicate that replacing mixed-material laminates with mono-material PP film structures can reduce lifecycle carbon emissions by 16 to 20%, largely due to lower material complexity and reduced sorting losses. This environmental benefit has accelerated adoption among fast-moving consumer goods brands seeking to meet extended producer responsibility targets.

Material innovation is reinforcing this shift. In June 2024, Avery Dennison launched its Sustainable Print portfolio featuring chlorine-free, halogen-free heat transfer films that deliver a reported 53% reduction in greenhouse gas emissions compared with conventional PVC decorative films. At the same time, circularity initiatives are maturing. Leonhard Kurz expanded its RECOSYS 2.0 program in 2024 to establish an industrial take-back system for PET carrier films, converting post-use transfer media into high-quality recycled PET suitable for injection molding. These developments position heat transfer films as a core enabler of circular packaging strategies rather than a secondary decorative component.

Lightweighting and Component Consolidation in Automotive Interiors

Automotive interiors are emerging as a second major growth engine for heat transfer films, driven by vehicle lightweighting and process simplification. OEMs are replacing multi-part, painted interior components with molded plastic substrates decorated in a single heat transfer step. This approach eliminates paint shops, reduces volatile organic compound emissions, and cuts component weight, which is especially critical for electric vehicles where mass reduction directly supports extended driving range.

The technical requirements of connected and autonomous vehicles are influencing material choices. The industry is shifting away from metalized decorative layers toward nano-ceramic heat transfer films that provide infrared rejection without interfering with 5G signals, advanced driver assistance systems, or satellite communications. These signal-transparent films have become essential for 2025-era cabin architectures that integrate displays, antennas, and sensors directly into interior trim.

Sustainability is further enhanced through material substitution. Demonstrations at the 2025 Folien + Fahrzeug exhibition highlighted collaboration between Kurz and FRIMO to laminate decorative heat transfer films directly onto natural fiber composites such as kenaf and flax. These solutions reduce synthetic polymer content by roughly 50% while maintaining premium tactile and visual quality. For OEMs under pressure to document cradle-to-gate emissions reductions, this integration of heat transfer films with bio-based substrates is becoming a strategic differentiator.

High-Performance Durability for Seamless Appliance Interfaces

Household appliances are transitioning toward seamless, glass-like control panels that integrate aesthetics and functionality. This evolution creates a high-margin opportunity for advanced heat transfer films capable of delivering long-term durability under aggressive use conditions. Appliance manufacturers are increasingly specifying multi-layer transfer films, often ranging from five to eleven layers, that combine decorative effects with hard, chemical-resistant topcoats.

These films are engineered to withstand more than 10,000 cycles of abrasive cleaning and prolonged exposure to detergents, solvents, and heat, aligning with the ten-year durability expectations of the major appliance segment. The ability to apply metallic finishes, textures, and protective layers in a single transfer step reduces assembly complexity while ensuring consistent surface quality across large production volumes.

Smart appliance interfaces further expand this opportunity. In 2025, control panel suppliers reported rising adoption of heat transfer film-decorated modules that comply with IEC 61439 electrical safety standards. These films provide dielectric insulation while delivering the high-gloss black and deep-contrast aesthetics favored in premium smart-home products, supporting both functional safety and design differentiation.

Integrated Functional Inks for Smart Surface Electronics

The most transformative opportunity for the heat transfer films market lies in the convergence of decoration and electronics. Manufacturers are increasingly integrating conductive and functional inks directly into the heat transfer process, enabling decorative graphics and electronic functionality to be applied simultaneously. This approach reduces production steps and supports thinner, lighter electronic assemblies.

At technology showcases in 2024, Henkel and Linxens demonstrated heat transfer foils incorporating Positive Temperature Coefficient inks that function as self-regulating heaters. These systems rapidly reach target temperatures without overheating, making them attractive for automotive seat heating, medical wearables, and personal care devices where safety and energy efficiency are paramount.

Within printed electronics, silver-based inks continue to dominate due to conductivity, accounting for roughly 80% of current usage. However, copper-based inks are recording the fastest growth in 2025 as advances in anti-oxidation coatings make them viable for high-volume RFID tags and smart packaging at lower cost. Parallel investments in rotary screen and high-speed printing lines are enabling antennas and sensors to be produced directly on flexible foils, supporting 5G connectivity in space-constrained environments where rigid printed circuit boards are impractical.

Heat Transfer Films Market Share and Segmentation Insights

Polyurethane Heat Transfer Films Lead the Heat Transfer Films Market Through Superior Apparel Performance

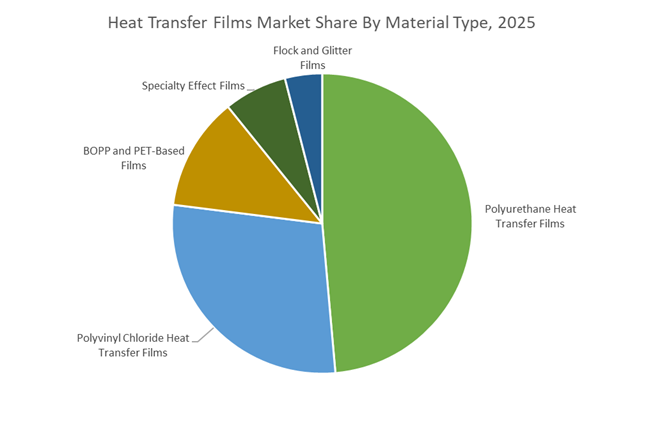

Polyurethane Heat Transfer Films accounted for 48.60% of the Heat Transfer Films Market share in 2025, establishing them as the most widely used material type in textile decoration technologies. Polyurethane (PU) heat transfer films are preferred due to their soft texture, excellent elasticity, and superior durability, characteristics that are critical for modern apparel applications such as sportswear, fashion garments, and stretchable fabrics. Compared with traditional PVC heat transfer films, polyurethane films provide enhanced comfort, improved breathability, and long-lasting wash resistance, making them particularly suitable for high-performance clothing. PU heat transfer films are widely applied through heat press transfer technology, allowing manufacturers to produce detailed graphics, logos, and decorative elements on garments without compromising fabric flexibility. In 2025, the polyurethane segment is evolving through the development of solvent-free production technologies, including water-based polyurethane coatings and hot-melt polyurethane film systems. These innovations eliminate solvent emissions during film production and application processes while maintaining the soft hand feel and stretch performance required for premium textile decoration.

Apparel and Textiles Industry Drives the Largest Demand for Heat Transfer Films

Apparel and Textiles represented 68.40% of the Heat Transfer Films Market share in 2025, making it the dominant end-use sector for heat transfer film technologies. Heat transfer films are widely used in T-shirt printing, sportswear branding, team uniforms, fashion garment decoration, and custom apparel production, where they enable high-quality graphics and durable textile embellishment. The technology allows manufacturers and customization businesses to apply logos, numbers, graphic designs, and branding elements onto garments using heat press equipment, supporting both large-scale production and small-batch personalization. The rapid expansion of custom apparel businesses, e-commerce merchandise printing, and print-on-demand clothing services has further strengthened demand for heat transfer films globally. In 2025, market growth within the textile sector is strongly influenced by the continued expansion of athleisure and performance apparel markets. Sportswear and activewear manufacturers increasingly require high-stretch polyurethane heat transfer films that maintain adhesion and visual quality during repeated washing, stretching, and intense physical activity. Advanced film formulations also incorporate moisture management compatibility and antimicrobial textile properties, enabling manufacturers to create functional decorative elements for premium activewear garments.

Competitive Landscape in Heat Transfer Films market

Avery Dennison Expands Sustainable and Performance Heat Transfer Portfolio

Avery Dennison Graphics Solutions is strengthening its position across automotive wraps, window films, and DIY heat transfer vinyl through innovation and portfolio expansion. In February 2026, the company introduced MPI 1903, a mid-tier cast wrapping film engineered for enhanced durability and performance graphics at competitive pricing. The integration of Siser by Avery Dennison has expanded its reach in the custom apparel segment with the EasyPSV Starling line, offering 55 colored vinyl films targeting the fast-growing professional crafter and DIY markets. Its DOL 7460 digital overlaminate featuring ADReva technology represents a solvent-free and PVC-free protective solution aligned with sustainability mandates. The Encore Series window films, utilizing nanotechnology to block up to 93% of infrared heat, reinforce Avery Dennison’s leadership in thermal management and automotive glazing.

STAHLS’ Drives Digital Heat Printing and Dimensional Decoration Growth

STAHLS’ Inc. remains a dominant player in the North American heat transfer vinyl and team sports decoration market, controlling a substantial share of commercial distribution. In February 2026, the company launched its updated product catalog highlighting UltraColor MAX Direct to Film transfers that eliminate weeding and screen burning, improving production efficiency for short-run apparel. STAHLS’ is transitioning toward dimensional decoration with FlexStyle emblems and 3D puff transfers that enable decorators to achieve higher-margin customization. The Fulfill Engine ProPlace IQ projection system enhances placement precision and digital workflow integration in high-volume production environments. Through its CAD-CUT brand and distribution of Siser HTV, STAHLS’ maintains largest commercial network share across key distribution channels.

Siser Strengthens Compostable and High-Texture Heat Transfer Innovation

Siser S.r.l. continues to define the global benchmark for easy-weeding heat transfer vinyl with its flagship EasyWeed product family. In 2025 and 2026, the company introduced PureHT, recognized as the first compostable heat transfer material designed for eco-conscious apparel brands complying with European sustainability standards. Its Easy Puff Metallic line merges three-dimensional expansion with metallic finishes, aligning with 2026 retail-driven demand for textured and premium apparel graphics. Siser is expanding beyond materials into a full-system ecosystem with the Baby Press and Romeo and Juliet cutters, enabling precision cutting and application. Specialized variants such as Aurora iridescent and Sublithin anti-dye migration films address technical challenges in sublimated polyester and performance sportswear markets.

3M Advances Industrial and EV Thermal Management Film Applications

3M Company focuses on high-performance industrial heat transfer films for safety, reflective apparel, and electric vehicle thermal management. Its Scotchlite Reflective Materials remain essential for compliance with EN ISO 20471 and global high-visibility standards in workwear. In 2026, 3M is deepening its presence in the EV sector by integrating thermal management films that protect battery modules and enhance energy efficiency in high-voltage systems. The company is also innovating low-temperature adhesive films designed for delicate technical fabrics, reducing scorching risk during branding processes. With operations in more than 70 countries, 3M leverages global distribution strength to maintain leadership in automotive glazing and safety textile segments.

Chemica Focuses on Low-Temperature and Water-Based PU Film Technologies

Chemica has established itself as a European specialist in ultra-thin, soft-touch polyurethane heat transfer films. Its Hotmark Revolution series allows application at temperatures as low as 120°C or within five seconds in Quick Mode, improving throughput in fast-fashion production lines. The company has transitioned its core manufacturing lines to water-based PU formulations, significantly reducing solvent usage and supporting eco-design objectives. Expansion of the Sublok Revolution range addresses anti-dye migration challenges in sublimated polyester sportswear by preventing color bleed and ghosting. Chemica maintains an extensive catalog exceeding 1,000 SKUs, including outdoor Sunmark films and velvet-texture Upperflok products tailored for premium apparel decoration.

Hexis Graphics Expands Asia-Pacific Production and PVC-Free Innovation

Hexis Graphics is accelerating global growth through the establishment of HEXSO, a new production facility in China announced in late 2025 and 2026. The plant supports long-term Asia-Pacific expansion while reducing transportation-related carbon emissions through localized manufacturing. Hexis allocates approximately 2.5% of annual turnover to research and development, focusing on PVC-free printable cast films and Take Heat Easy technology that simplifies installation. Its Holeshot Hextreme customized decoration kits target extreme sports branding, while the Bodyfence range provides advanced paint protection and surface films. The HEXSO facility is built to modern environmental standards and is structured to supply entry-level product ranges demanded in emerging markets without compromising quality or durability.

United States: Performance Differentiation and Industrial-Scale Customization

The United States heat transfer films industry is evolving through a convergence of DIY market expansion, advanced material science, and industrial automation. In late 2025, Avery Dennison Graphics Solutions deepened its strategic partnership with Siser North America, launching the EasyPSV Starling collection. This product line targets the fast-growing DIY and crafting segment with 57 new color variants engineered for dishwasher resistance and precise weeding. The move reflects rising consumer demand for durable, home-applied decorative films and positions heat transfer vinyl as a core material in the personalized apparel and home décor ecosystem.

At the higher end of performance applications, Avery Dennison’s debut of the Encore Series automotive films in February 2025 introduced dye-free nanotechnology capable of repelling up to 93% of infrared heat. This sets a new benchmark for solar heat rejection in vehicle wraps and supports the transition toward energy-efficient automotive surface solutions for the 2026 model cycle. Manufacturing workflows are also being redefined. STAHLS’ Hotronix entered a global manufacturing agreement with Stampinator, integrating Hotronix IQ heat press systems into automated screen-printing lines. This enables high-speed application of Direct-to-Film and specialty transfers at industrial throughput. Sustainability remains an additional lever. Avery Dennison’s ADReva Technology, launched in June 2025, introduced the DOL 7460 Digital Overlaminate, a PVC-free and solvent-free solution aligned with anticipated 2026 eco-labeling criteria, reinforcing the U.S. market’s shift toward compliant and long-life graphic films.

Germany: Circularity-Driven Textile Decoration and Automation Leadership

Germany’s heat transfer films industry is distinguished by its strong alignment with circular economy principles and high-precision automation. At the K 2025 trade fair in Düsseldorf, Leonhard Kurz showcased functional prototypes of sports jerseys produced entirely from recycled PET. The innovation leverages near-series heat transfer processes to apply decorative elements without compromising recyclability, addressing a key challenge in sustainable textile manufacturing. This development underscores Germany’s role in advancing recyclable garment decoration technologies for performance and sportswear markets.

Automation and waste reduction further define the German landscape. DekorTech GmbH, through its DIGITRAN brand, introduced the FlexLine DTF600 MK-II system in late 2025. By combining five-head digital printing with the TURBOTRAN 6.1 transfer unit, the platform achieves industrial throughput of up to 600 textiles per hour, supporting Europe’s promotional products and on-demand apparel sectors. Leonhard Kurz also received the German Innovation Award 2025 for its RECOSYS textile decoration technology, which enables large-scale recovery and reuse of PET carrier films. This capability significantly reduces waste in automotive interior and technical textile supply chains, reinforcing Germany’s leadership in closed-loop heat transfer film systems.

China: Domestic Material Substitution and Smart Manufacturing Scale-Up

China’s heat transfer films industry is being reshaped by national industrial policy, biodegradable material adoption, and rapid digitization of manufacturing. As the Made in China 2025 program enters its final phase, the Ministry of Industry and Information Technology finalized subsidy frameworks in late 2025 for 40 national and 48 provincial innovation centers. These centers are mandated to achieve a 70% domestic content rate for core polymer materials used in high-heat transfer films, accelerating substitution of imported specialty polymers with locally developed alternatives.

Environmental regulation is reinforcing this shift. Government disclosures indicate a rapid transition within the Shandong chemical cluster toward PLA and PBAT-based heat transfer carriers, driven by stricter provincial controls on non-recyclable plastics in packaging and consumer goods. Manufacturing efficiency is also advancing. Leading producers such as Guangdong Guanhao High-Tech implemented AI-driven thickness monitoring across multilayer polyurethane film lines in 2025, reducing raw material variance by 15% ahead of the 2026 export cycle. These developments collectively position China as a scale-driven market increasingly focused on material localization, compliance, and process consistency.

India: Policy-Led Modernization and Green Textile Infrastructure

India’s heat transfer films industry is entering a modernization phase underpinned by fiscal support, regulatory flexibility, and integrated textile infrastructure development. The Union Budget 2025–26 increased allocations to the Ministry of Textiles by 19%, with a significant share of funding under the Amended Technology Upgradation Fund Scheme directed toward digital printing and heat transfer machinery. This investment is accelerating modernization across major textile clusters such as Surat and Ludhiana, where garment decoration and value-added printing are central to export competitiveness.

Regulatory reforms are providing additional momentum. In June 2025, the Ministry of Heavy Industries extended the implementation deadline for mandatory Quality Control Orders on textile machinery to September 1, 2026. This extension offers processors a critical window to upgrade to BIS-compliant, high-speed heat transfer equipment without disrupting operations. Structural demand is also emerging from the PM MITRA initiative, under which seven integrated textile parks are being developed with plug-and-play facilities. These parks mandate the use of eco-certified, halogen-free heat transfer vinyls, embedding sustainability requirements directly into India’s next-generation textile manufacturing base.

South Korea: Premium PU Films and Global DIY Innovation Hub

South Korea has consolidated its position as a high-value producer in the heat transfer films industry, particularly in polyurethane-based and specialty decorative films. In 2025, Hansol Corporation expanded capacity for ultra-thin PU transfer films engineered for performance apparel. These films offer approximately 40% higher stretchability than conventional PVC alternatives, supporting the functional requirements of 2026 activewear and sportswear collections.

Beyond industrial apparel, South Korean manufacturers have emerged as global leaders in premium DIY heat transfer vinyl. Producers have captured a dominant share of the high-end customization segment through innovations such as 3D puff effects and glow-in-the-dark films. These products comply with OEKO-TEX Standard 100 requirements for infant safety, strengthening acceptance in European and North American consumer markets. South Korea’s focus on design-led differentiation and compliance-grade materials positions it as a strategic innovation hub within the global heat transfer films value chain.

Summary Table: Country-Level Strategic Signals in the Heat Transfer Films Industry

Heat Transfer Films Market County Level Snapshot

|

Country

|

Strategic Driver

|

Industrial Focus

|

Strategic Implication

|

|

United States

|

DIY expansion, nanotechnology

|

Automotive, DTF automation

|

Performance and customization leadership

|

|

Germany

|

Circular economy, automation

|

rPET textiles, waste recovery

|

Closed-loop decoration systems

|

|

China

|

Industrial policy, localization

|

Biodegradable polymers, smart factories

|

Scale with domestic materials

|

|

India

|

Budget support, cluster upgrades

|

Digital printing, eco-certified HTV

|

Modernization and compliance

|

|

South Korea

|

PU innovation, premium DIY

|

Performance apparel, specialty HTV

|

High-value differentiation

|

Heat Transfer Films Market Report Scope

Heat Transfer Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2034)

|

$7.8 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Material Type (Polyurethane Heat Transfer Films, Polyvinyl Chloride Heat Transfer Films, BOPP and PET-Based Films, Flock and Glitter Films, Specialty Effect Films), By Printing Technology (Digital Print Transfers, Screen Printed Transfers, Direct-to-Film Transfers, Offset and Lithographic Transfers), By Application Method (Heat Press Transfer, Plotter-Based Cutting, Industrial Roll-to-Roll Transfer), By End-Use Industry (Apparel and Textiles, Automotive, Consumer Goods, Packaging and Labeling, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, Siser Srl, STAHLS’, Leonhard Kurz Stiftung & Co. KG, Chemica, Poli-Tape Group, Hexis S.A.S., Dae Ha Co., Ltd., Hansol Paper Co., Ltd., Guangdong Guanhao High-Tech Co., Ltd., Alwan, Biser, Unimark Heat Transfer Co., 3M Company, Nitto Denko Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Heat Transfer Films Market Segmentation

By Material Type

- Polyurethane Heat Transfer Films

- Polyvinyl Chloride Heat Transfer Films

- BOPP and PET-Based Films

- Flock and Glitter Films

- Specialty Effect Films

By Printing Technology

- Digital Print Transfers

- Screen Printed Transfers

- Direct-to-Film Transfers

- Offset and Lithographic Transfers

By Application Method

- Heat Press Transfer

- Plotter-Based Cutting

- Industrial Roll-to-Roll Transfer

By End-Use Industry

- Apparel and Textiles

- Automotive

- Consumer Goods

- Packaging and Labeling

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Heat Transfer Films Industry

- Avery Dennison Corporation

- Siser Srl

- STAHLS’

- Leonhard Kurz Stiftung & Co. KG

- Chemica

- Poli-Tape Group

- Hexis S.A.S.

- Dae Ha Co., Ltd.

- Hansol Paper Co., Ltd.

- Guangdong Guanhao High-Tech Co., Ltd.

- Alwan

- Biser

- Unimark Heat Transfer Co.

- 3M Company

- Nitto Denko Corporation

*- List not Exhaustive