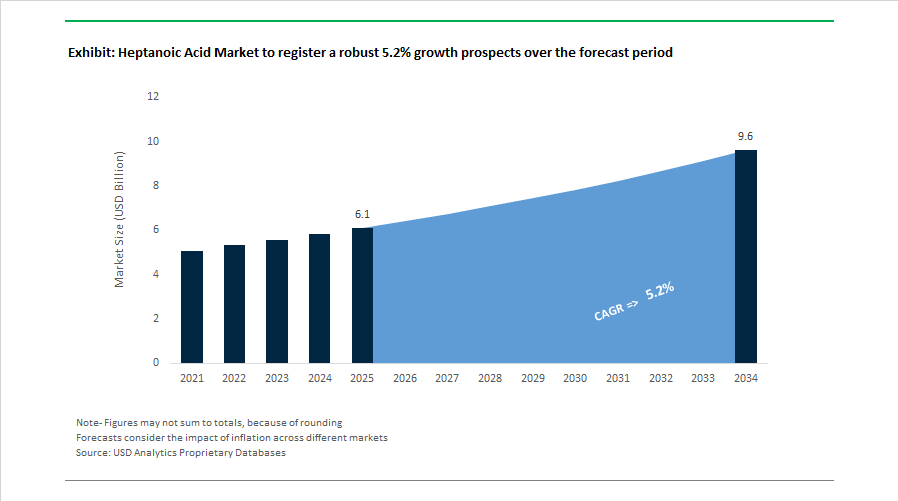

The Heptanoic Acid Market is projected to expand from $6.1 billion in 2025 to $9.6 billion by 2034, registering a CAGR of 5.2%. Growth is supported by rising demand for synthetic esters in aviation lubricants, hybrid-electric vehicle transmission fluids, cosmetic intermediates, and dielectric cooling fluids for high-density data centers. Increasing regional supply localization in Europe, sustainability-led fatty acid synthesis, and the development of renewable C7 carboxylic acids are reshaping procurement strategies for lubricant formulators, specialty ester producers, and personal care manufacturers.

In early 2024, Arkema announced an R&D collaboration targeting renewable synthesis pathways for odd-chain fatty acids, specifically C7 to C10 acids. The initiative strengthens the push toward bio-based heptanoic acid for high-purity cosmetic and specialty applications. In 2024, a German regional consortium launched a pilot plant for fermentation-based C7 production from agricultural sugars, demonstrating a 28% reduction in carbon intensity compared to conventional petrochemical oxidation routes. In July 2024, India enforced new Bureau of Indian Standards requirements for specialty esters, prompting domestic producers to upgrade quality control systems for pharmaceutical- and food-grade heptanoic acid derivatives. In October 2024, Oleon completed its acquisition of A. Azevedo in Brazil, strengthening raw material integration and expanding global fatty acid derivative supply capacity.

Supply chain realignment accelerated in 2025. In March 2025, OQ Chemicals announced the launch of dedicated heptanoic acid production at its Oberhausen facility, commencing commercial output in June 2025. The multi-purpose Oxo configuration allows flexible switching between C5, C7, and C9 acids, improving feedstock resilience during periods of propylene and syngas volatility. By mid-2025, European customers gained access to locally produced commercial volumes, reducing reliance on imports and enabling just-in-time delivery for aviation ester and advanced cooling fluid applications. In 2025, a major Japanese lubricant OEM introduced hybrid-electric transmission fluids formulated with heptanoic acid esters to deliver low-viscosity performance, thermal stability, and oxidation resistance for integrated motor systems.

Sustainability and advanced thermal management are shaping 2026 demand patterns. In December 2025, Oleon secured a Gold Medal in the EcoVadis Sustainability Assessment, reinforcing its credentials in renewable fatty acid chemistry for cosmetic and lubricant brands. In January 2026, Oleon partnered with Iceotope to advance precision liquid cooling technologies for AI-driven data centers, utilizing heptanoate-based dielectric fluids for efficient heat dissipation in high-density computing infrastructure. In December 2025, Clean Science and Technology commenced catechol production, enhancing backward integration in aromatic intermediates that compete with heptanoic-based stabilizer systems in polymer applications.

The Heptanoic Acid Market is increasingly characterized by European production localization, bio-fermentation pilots for low-carbon C7 acids, lubricant innovation for electrified mobility, and expansion into high-performance dielectric cooling fluids. Competitive positioning is determined by Oxo-technology flexibility, carbon intensity reduction, pharmaceutical-grade purity compliance, and integration across global fatty acid derivative value chains serving aerospace, automotive, personal care, and data infrastructure sectors.

The heptanoic acid market is increasingly aligned with the rapid evolution of high-performance lubricants required for electric vehicles, hybrid drivetrains, aviation systems, and advanced industrial machinery. As power densities rise and operating temperatures increase, lubricant formulators are shifting toward synthetic esters such as heptyl heptanoate that offer superior oxidative stability, low volatility, and extended drain intervals. This transition is driving targeted capacity investments focused on consistent quality and regional supply security rather than commodity-scale volumes.

In Europe, OQ Chemicals commissioned a dedicated heptanoic acid production unit in Oberhausen, Germany, with operations scheduled to begin in mid-2025. The facility is designed to serve aviation lubricants and next-generation energy applications where trace impurity control and batch-to-batch consistency are critical. This investment reflects a broader trend in which lubricant OEM approvals increasingly require localized production and transparent supply chains.

From a formulation standpoint, development programs in 2024 and 2025 demonstrated that incorporating heptanoic acid-derived esters into hybrid electric vehicle transmission fluids can reduce evaporative loss by approximately 14%. This performance gain supports compliance with stringent environmental discharge norms, including Vessel General Permit requirements, while improving lubricant longevity. At the strategic level, Arkema has reinforced its commitment to C7 chemistry in its 2024 to 2028 roadmap, positioning heptanoic acid as a core building block for green energy, electric mobility, and specialty materials platforms expected to scale strongly through the end of the decade.

The cost structure and regional competitiveness of heptanoic acid are being reshaped by structural changes in the 1-hexene feedstock landscape. Producers are gradually moving away from traditional ethylene oligomerization routes toward more selective ethylene trimerization and metathesis-based technologies. These routes improve feedstock efficiency and reduce exposure to cyclic ethylene price volatility, which has historically constrained margin stability for oxo-acid producers.

Process optimization studies published in 2025 identified metathesis conditions that deliver selectivity levels of around 70% toward higher-weight olefins, enabling more predictable downstream conversion into heptanoic acid. As a result, producers are increasingly able to decouple heptanoic acid economics from short-term olefin market swings. At the same time, demand is shifting decisively toward high-purity grades. Between 2023 and 2024, global demand for heptanoic acid with purity levels above 98.5% increased by roughly 27%, driven by food, fragrance, and pharmaceutical applications that require tight odor and impurity specifications.

Asia-Pacific remains central to this transformation. With the region accounting for nearly 36% of global chemical intermediate consumption, new integrated production hubs are redefining supply dynamics. The ramp-up of large-scale Verbund complexes such as BASF’s Zhanjiang site by late 2025 is expected to lower logistics costs and improve availability of oxo-intermediates across the region. This shift is encouraging downstream customers to regionalize sourcing strategies while maintaining access to globally competitive pricing.

One of the most attractive growth opportunities for heptanoic acid lies in the fine fragrance and personal care sector, where demand for biodegradable and clean-label aroma chemicals continues to intensify. Heptanoic acid derivatives such as methyl heptanoate and other C7 esters play a critical role in delivering fruity, fatty, and wine-like notes that are essential for modern fragrance compositions. While this segment represents a smaller share of total volume compared to lubricants, it commands significantly higher margins due to stringent quality requirements and branding-driven pricing.

The commercial backdrop is compelling. In 2024, the global beauty industry generated approximately USD 720 billion in revenue, with the U.S. fragrance market alone valued at around USD 8 billion. Within this context, heptanoic acid esters are increasingly specified as natural-identical alternatives that align with sustainability narratives without compromising olfactory performance. Bio-based production routes are reinforcing this appeal. Pilot-scale projects in Germany demonstrated in 2024 that odd-chain fermentation of agricultural sugars can produce bio-based C7 acids with an estimated 28% lower carbon intensity than petroleum-derived enanthic acid. This positions heptanoic acid as a strategic input for fragrance houses pursuing ecolabel certifications and science-based emissions targets.

Beyond scent creation, heptanoic acid is gaining traction as a functional masking agent capable of suppressing rancid or off-notes associated with natural oils. This expands its relevance in the fast-growing natural skincare and haircare segments, where formulators seek to balance botanical authenticity with consumer-acceptable sensory profiles.

Regulatory pressure on traditional biocides, nitrites, and secondary amines is driving a fundamental reformulation of metalworking fluids across Europe, North America, and parts of Asia. Within this context, heptanoic acid derivatives such as sodium heptanoate are emerging as high-potential, non-toxic corrosion inhibitors that align with occupational safety and environmental compliance objectives.

Electrochemical studies published in late 2024 confirmed that low concentrations of sodium heptanoate, around 0.3%, can form stable hydrophobic passive films on carbon steel surfaces. These films provide effective corrosion protection in aqueous systems without the health and disposal risks associated with conventional inhibitors. The multifunctional nature of heptanoic-based additives further enhances their value proposition. Specialty suppliers including Evonik are promoting formulations that combine corrosion inhibition, emulsification, and low-foaming behavior, allowing metalworking fluid producers to simplify additive packages and extend sump life.

Supply resilience is a critical enabler of this opportunity. European producers such as OQ Chemicals are leveraging proprietary oxo-production capabilities to ensure consistent regional supply of heptanoic acid, reducing exposure to volatile bio-based feedstocks like castor oil, which experienced price fluctuations of around 18% in 2023. As industrial customers increasingly prioritize stable pricing, regulatory compliance, and worker safety, heptanoic acid-based corrosion inhibitors are positioned to become a cornerstone of next-generation metalworking fluid formulations.

Industrial Grade accounted for 58.60% of the Heptanoic Acid Market share in 2025, making it the most widely used grade across global heptanoic acid consumption. Industrial grade heptanoic acid is primarily utilized in lubricant production, synthetic ester manufacturing, corrosion inhibitor formulations, and chemical intermediate synthesis, where standard purity levels provide adequate performance while maintaining cost efficiency for large-scale industrial processes. The compound serves as an important precursor in the production of specialty esters used in high-performance lubricants and industrial fluids, enabling improved thermal stability and oxidation resistance in demanding operating environments. In 2025, demand for industrial grade heptanoic acid is increasing alongside the expansion of synthetic lubricant markets, particularly within automotive and heavy industrial sectors. Synthetic lubricants formulated using heptanoic acid derivatives exhibit excellent low-temperature fluidity, high thermal stability, and superior oxidation resistance, making them well suited for modern machinery operating under high loads and extreme temperature conditions. These performance characteristics are driving stronger consumption of industrial-grade heptanoic acid within global lubricant manufacturing supply chains.

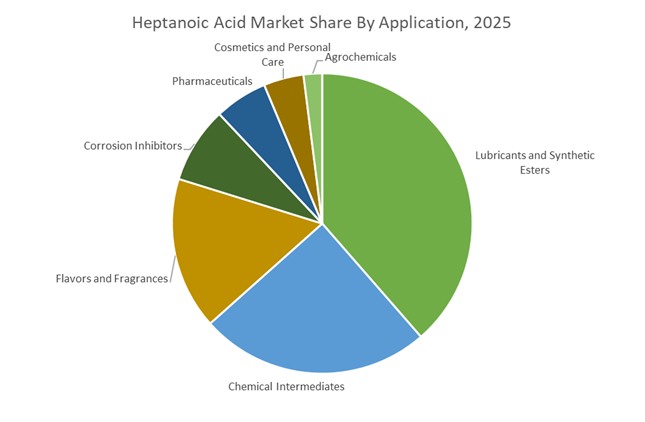

Lubricants and Synthetic Esters represented 38.60% of the Heptanoic Acid Market share in 2025, making this the largest application segment for heptanoic acid derivatives. The compound is widely used as a key raw material in the synthesis of polyol esters and diester-based lubricants, which are valued for their excellent lubricity, thermal stability, and performance under extreme operating conditions. These synthetic ester lubricants are commonly applied in aviation turbine engines, industrial compressors, refrigeration systems, and high-performance automotive lubrication systems, where traditional mineral oil lubricants cannot deliver sufficient performance. In 2025, the lubricant sector is experiencing notable demand growth driven by the global transition toward environmentally friendly refrigeration technologies. As industries phase down high-global-warming-potential HFC refrigerants, new refrigeration systems increasingly rely on natural refrigerants such as carbon dioxide, ammonia, and hydrocarbons. These next-generation cooling systems require synthetic ester lubricants that offer strong miscibility with alternative refrigerants and maintain lubrication performance under high-pressure operating conditions, creating sustained demand for heptanoic acid-derived lubricant esters.

Arkema S.A. is the global benchmark for bio-based heptanoic acid, leveraging its fully integrated castor oil value chain to support Rilsan® Polyamide 11 and specialty lubricant production. In 2026, Arkema advanced its transformation into a Specialty Materials pure-player by revising business segmentation to increase transparency in high-margin bio-based intermediates. The company emphasizes that castor-derived materials are key contributors to EBITDA resilience despite weaker demand in legacy European industrial sectors. Its heptanoic acid portfolio highlights 100% renewable origin, high stability, and pharmaceutical-grade purity suitable for dermatological and personal care formulations. Arkema continues promoting purity and sustainability credentials at global industry events such as In-Cosmetics 2026 to capture premium cosmetic ingredient demand.

Oxea, formerly OQ Chemicals, is the dominant European producer of oxo-based heptanoic acid, utilizing proprietary hydroformylation and oxidation processes. In June 2025 and 2026, the company launched dedicated C7 acid production at its Oberhausen facility to reduce European reliance on imports and stabilize regional supply chains. Oxea is positioning itself as a strategic supplier to aviation lubricant and industrial ester markets requiring consistent quality and scale. Its OxBalance® Neopentyl Glycol Diheptanoate, introduced as a biomass-balanced cosmetic ester, addresses sustainability-driven substitution of cyclic silicones. Following a leadership realignment in February 2026, Oxea entered a Strategic Relaunch phase centered on high-growth carboxylic acids and value-added derivatives.

Oleon N.V., part of the Avril Group, is strengthening its oleochemical footprint in vegetable-derived C7 derivatives following its 2024 merger with Kerfoot Group Ltd. The expanded distribution network enhances access to natural and organic oils across Europe and North America. In 2026, Oleon markets 98% pure triglyceride of heptanoic acid as a high-performance base for environmentally friendly lubricants and specialty esters. The company targets the Clean Label personal care sector by offering traceable, vegetable-based heptanoic acid compliant with ECOCERT and COSMOS standards. Backed by Avril Group integration, Oleon is scaling its bio-based carboxylic acid portfolio across Southeast Asia and North America.

Acme Synthetic Chemicals is a key Indian manufacturer specializing in castor oil-derived heptanoic acid with minimum purity of 97% by GC. The company maintains strong domestic distribution while exporting pharmaceutical-grade C7 acid to Middle Eastern and European fragrance manufacturers. In early 2026, Acme expanded its contract manufacturing capabilities for customized heptanoate esters tailored to automotive motor oil viscosity requirements. Investment in advanced distillation technologies enables production of colorless to pale-yellow grades with minimal odor, critical for fragrance and cosmetic applications. Its customer-centric purity approach positions Acme as a competitive supplier in Asia-Pacific’s growing bio-based fatty acid market.

Tokyo Chemical Industry Co., Ltd. operates at the high-precision end of the heptanoic acid market, supplying analytical and reagent-grade material exceeding 99% purity. Through its catalog-based distribution model, TCI provides rapid delivery to pharmaceutical synthesis, steroid esterification, and specialty research applications across Japan, South Korea, and the United States. In 2025 and 2026, the company enhanced its digital procurement infrastructure to provide real-time batch-specific Certificates of Analysis for biotech and fragrance laboratories. Unlike volume-driven producers, TCI competes through precision, traceability, and just-in-time supply for pilot-scale and laboratory research. This positioning secures its dominance in specialized chemical synthesis and pharmaceutical R&D segments.

Germany is emerging as a strategic anchor for the European heptanoic acid industry, driven by supply security priorities, high-performance lubricant demand, and tightening chemical compliance frameworks. In June 2025, OQ Chemicals operationalized a dedicated heptanoic acid production unit at its Oberhausen site, leveraging proprietary Oxo synthesis technology. This investment materially strengthens Europe’s internal supply of C7 carboxylic acids for aviation lubricants, energy-sector fluids, and transformer dielectric applications. The move aligns with a broader German industrial strategy to reduce reliance on Asian imports of synthetic fatty acids that are critical for refrigerant oils and electrical insulation fluids.

Downstream demand fundamentals remain robust. Germany’s chemical clusters continue to dominate global exports of high-performance synthetic lubricants, with 2025 data indicating a 20.4% share of global exports. Heptanoic acid plays a central role as an intermediate in the production of low-viscosity, high-thermal-stability polyol ester lubricants used in aerospace and advanced energy systems. On the regulatory front, the European Chemicals Agency transitioned all heptanoic acid safety data into the ECHA CHEM database effective September 2025. German manufacturers have moved early to update Safety Data Sheets in line with revised occupational exposure limits, reinforcing compliance leadership. Process efficiency is also improving. Production facilities across the Ruhr region have implemented Mechanical Vapor Recompression distillation, targeting 12 to 15% reductions in steam energy intensity by early 2026. Looking ahead, German R&D institutes have announced a 2026 pilot for biodegradable aviation lubricants derived from heptanoic acid, supporting stricter environmental requirements in civil aviation.

France occupies a distinct position in the heptanoic acid value chain through its leadership in bio-based oleochemicals and premium downstream applications. In late 2025, Arkema completed a 50% capacity expansion of its Oleris bio-based oleochemicals platform. The expansion is centered on Arkema’s castor oil to heptanoic acid process, positioning France as a leading supplier of fully bio-sourced C7 intermediates for lubricants, cleaners, and specialty esters. This capacity surge directly addresses rising demand from customers seeking traceable, renewable alternatives to petrochemical-derived acids.

Market access advantages have also expanded. Arkema’s Oleris C7 heptanoic acid secured USDA BioPreferred certification in 2025, enabling French exports to compete more effectively in North American government procurement programs for sustainable products. In parallel, France’s cosmetics and personal care sector is integrating high-purity heptanoic acid esters such as neopentyl glycol diheptanoate into premium formulations, citing improved sensory performance, enhanced spreadability, and clean beauty positioning. Upstream resilience is being addressed through supply chain collaboration. Arkema expanded its Pragati sustainable castor farming initiative with Indian partners in 2025, securing raw material continuity for 2026–2027 production cycles and reinforcing France’s leadership in circular, bio-based heptanoic acid production.

China’s heptanoic acid industry is transitioning from volume-driven production toward higher-purity, application-specific grades supported by industrial policy. In 2025, the Ministry of Industry and Information Technology released a directive under the draft 15th Five-Year Plan prioritizing specialty fatty acids. This includes targeted subsidies for ≥99% purity heptanoic acid production in Shandong and Jiangsu, accelerating investments in pharmaceutical, food, and aroma-grade capacities.

Commercial execution is already visible. Handan Kezheng Chemical commissioned a new USP-grade heptanoic acid line in late 2025 to supply global pharmaceutical markets, particularly valproic acid synthesis and related therapeutic intermediates. China also maintains a dominant position in aroma chemicals. Domestic producers of ethyl heptanoate account for nearly 28% of global supply in 2025, serving food flavoring applications that require consistent fruity and pineapple notes. Process modernization is supporting export compliance. Chinese manufacturers have transitioned to antimony-free catalytic oxidation routes for heptanal conversion, significantly lowering heavy metal residues in food-grade batches ahead of 2026 export requirements. Additionally, several firms announced the scaling of heptanoyl chloride infrastructure in Q4 2025 to support next-generation biodegradable agrochemical formulations, broadening heptanoic acid’s role in sustainable agriculture inputs.

India’s heptanoic acid industry is gaining momentum through policy-backed bio-based prioritization and expanding downstream demand from automotive and pharmaceutical sectors. Under the national BioE3 policy framework for 2025–2026, bio-based heptanoic acid derived from castor oil has been formally designated a high-priority green growth chemical. This designation is unlocking R&D incentives and accelerating domestic capacity planning focused on renewable feedstocks.

Demand growth is closely linked to lubricants and mobility. With India’s automotive industry on track to become the world’s third largest by 2026, domestic producers such as Kalpsutra Chemicals expanded heptanoic acid ester lines in 2025 to serve hybrid-electric vehicle lubricant formulations requiring thermal stability and oxidative resistance. Regulatory alignment is also advancing. Indian manufacturers are upgrading purification and analytical units in early 2026 to comply with Revised Schedule M pharmaceutical standards, ensuring domestically produced heptanoic acid qualifies for high-value active pharmaceutical ingredient synthesis. Innovation in production economics is emerging as well. A Gujarat-based chemical cluster launched a 2025 pilot using enzymatic synthesis routes for heptanoic acid, aiming to reduce capital expenditure by approximately 15% compared to conventional oxidation processes.

The United States heptanoic acid market is characterized by stringent performance standards, specialty corrosion applications, and pharmaceutical-grade demand. Aviation remains a core end use. In 2025, U.S. lubricant blenders continued to prioritize heptanoic acid sources compliant with MIL-PRF-23699, reflecting sustained demand for high-thermal-stability jet engine lubricants. Supply chain qualification and traceability are therefore critical competitive factors.

Beyond aviation, new application segments are emerging. In early 2025, Gulf Coast specialty chemical firms introduced sodium heptanoate formulations for corrosion inhibition in water-based cooling systems used by hyperscale data centers. These formulations are replacing phosphate-based inhibitors due to environmental discharge concerns and system compatibility advantages. Pharmaceutical demand is tightening quality thresholds. The U.S. Food and Drug Administration issued updated 2025 guidance on Inactive Ingredient Database limits for heptanoic acid derivatives in topical drugs, driving demand for higher-purity analytical grades. Supporting this trend, Thermo Fisher Scientific announced a USD 22 million investment in North American oral solid dose manufacturing infrastructure in late 2024 and early 2025, indirectly boosting consumption of heptanoic-acid-based carriers and prodrug intermediates.

|

Country |

Strategic Driver |

Key End-Use Focus |

Strategic Implication |

|

Germany |

Supply localization, REACH updates |

Aviation lubricants, energy fluids |

European supply security and efficiency |

|

France |

Bio-based capacity expansion |

Cosmetics, sustainable lubricants |

Renewable differentiation |

|

China |

Industrial policy, purity upgrades |

Pharma, aroma chemicals, agrochemicals |

Multi-grade scale and export readiness |

|

India |

BioE3 incentives, auto growth |

HEV lubricants, APIs |

Bio-based expansion and compliance |

|

United States |

Aviation standards, FDA guidance |

Jet lubricants, pharma carriers |

High-purity, application-specific demand |

|

Parameter |

Details |

|

Market Size (2025) |

$6.1 Billion |

|

Market Size (2034) |

$9.6 Billion |

|

Market Growth Rate |

5.2% |

|

Segments |

By Grade (Pharmaceutical Grade, Industrial Grade, Food and Fragrance Grade), By Source Type (Synthetic Heptanoic Acid, Bio-Based Heptanoic Acid), By Application (Lubricants and Synthetic Esters, Flavors and Fragrances, Pharmaceuticals, Cosmetics and Personal Care, Corrosion Inhibitors, Agrochemicals, Chemical Intermediates) |

|

Study Period |

2019- 2025 and 2026-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Arkema S.A., OQ Chemicals GmbH, Handan Kezheng Chemical Co., Ltd., Jinan Chenghui Shuangda Chemical Co., Ltd., Kalpsutra Chemicals Pvt. Ltd., Merck KGaA, Tokyo Chemical Industry Co., Ltd., Acme Synthetic Chemicals, Parchem Fine & Specialty Chemicals, Inc., Spectrum Laboratory Products, Inc., Yancheng Huade Biological Engineering Co., Ltd., National Analytical Corporation, Vantage Specialty Chemicals, Santa Cruz Biotechnology, Inc., Thermo Fisher Scientific Inc. |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

*- List not Exhaustive

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Heptanoic Acid Market Landscape & Outlook (2026–2034)

2.1. Introduction to Heptanoic Acid Market

2.2. Market Valuation and Growth Projections (2026–2034)

2.3. Growth Drivers: Synthetic Lubricants, EV Transmission Fluids, and Aviation Ester Demand

2.4. Supply Chain Transformation: European Capacity Expansion and Regional Localization

2.5. Sustainability and Bio-Based C7 Acid Development in Specialty Chemicals

3. Innovations Reshaping the Heptanoic Acid Market

3.1. Trend: Strategic Capacity Expansion for High-Performance Synthetic Lubricants

3.2. Trend: Feedstock Realignment and High-Purity Heptanoic Acid Production

3.3. Opportunity: Bio-Based Aroma Chemicals for Fine Fragrance and Personal Care

3.4. Opportunity: Heptanoic Acid-Based Corrosion Inhibitors for Advanced Metalworking Fluids

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Bio-Based Fatty Acid Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Supply Chain Localization

5. Market Share and Segmentation Insights: Heptanoic Acid Market

5.1. By Grade

5.1.1. Pharmaceutical Grade

5.1.2. Industrial Grade

5.1.3. Food and Fragrance Grade

5.2. By Source Type

5.2.1. Synthetic Heptanoic Acid

5.2.2. Bio-Based Heptanoic Acid

5.3. By Application

5.3.1. Lubricants and Synthetic Esters

5.3.2. Flavors and Fragrances

5.3.3. Pharmaceuticals

5.3.4. Cosmetics and Personal Care

5.3.5. Corrosion Inhibitors

5.3.6. Agrochemicals

5.3.7. Chemical Intermediates

5.4. By Region

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. South and Central America

5.4.5. Middle East and Africa

6. Country Analysis and Outlook of Heptanoic Acid Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Heptanoic Acid Market Size Outlook by Region (2026–2034)

7.1. North America Heptanoic Acid Market Size Outlook to 2034

7.1.1. By Grade

7.1.2. By Source Type

7.1.3. By Application

7.1.4. By Region

7.2. Europe Heptanoic Acid Market Size Outlook to 2034

7.2.1. By Grade

7.2.2. By Source Type

7.2.3. By Application

7.2.4. By Region

7.3. Asia Pacific Heptanoic Acid Market Size Outlook to 2034

7.3.1. By Grade

7.3.2. By Source Type

7.3.3. By Application

7.3.4. By Region

7.4. South America Heptanoic Acid Market Size Outlook to 2034

7.4.1. By Grade

7.4.2. By Source Type

7.4.3. By Application

7.4.4. By Region

7.5. Middle East and Africa Heptanoic Acid Market Size Outlook to 2034

7.5.1. By Grade

7.5.2. By Source Type

7.5.3. By Application

7.5.4. By Region

8. Company Profiles: Leading Players in the Heptanoic Acid Market

8.1. Arkema S.A.

8.2. OQ Chemicals GmbH

8.3. Handan Kezheng Chemical Co., Ltd.

8.4. Jinan Chenghui Shuangda Chemical Co., Ltd.

8.5. Kalpsutra Chemicals Pvt. Ltd.

8.6. Merck KGaA

8.7. Tokyo Chemical Industry Co., Ltd.

8.8. Acme Synthetic Chemicals

8.9. Parchem Fine & Specialty Chemicals, Inc.

8.10. Spectrum Laboratory Products, Inc.

8.11. Yancheng Huade Biological Engineering Co., Ltd.

8.12. National Analytical Corporation

8.13. Vantage Specialty Chemicals

8.14. Santa Cruz Biotechnology, Inc.

8.15. Thermo Fisher Scientific Inc.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

The Heptanoic Acid Market is expected to grow from $6.1 billion in 2025 to $9.6 billion by 2034, registering a CAGR of 5.2%. Growth is supported by increasing demand for synthetic ester lubricants used in aviation turbines, hybrid-electric vehicle transmission fluids, and advanced industrial machinery. Expanding applications in cosmetics, pharmaceutical intermediates, and dielectric cooling fluids for high-density data centers are also contributing to market expansion. European capacity additions and bio-based C7 acid innovation are further strengthening supply security and sustainability positioning.

Synthetic ester lubricants represent the largest application segment, accounting for 38.60% of global heptanoic acid consumption in 2025. Heptanoic acid serves as a key intermediate in producing polyol esters and diesters used in aviation engines, refrigeration compressors, and advanced automotive lubrication systems. These lubricants provide superior thermal stability, oxidation resistance, and low-temperature fluidity compared with mineral oils. As electrified mobility systems and high-performance machinery require more durable lubrication solutions, demand for heptanoic acid-based ester formulations continues to increase.

Bio-based production of heptanoic acid is gaining traction as chemical producers seek lower-carbon synthesis routes and renewable feedstocks. Fermentation-based production technologies using agricultural sugars have demonstrated approximately 28% lower carbon intensity compared with conventional petrochemical oxidation pathways. Bio-based heptanoic acid derived from castor oil or fermentation processes is increasingly preferred in cosmetics, personal care, and specialty chemical applications that require sustainability certification. This shift supports the broader transition toward renewable fatty acid chemistry within the specialty chemicals sector.

New application areas are emerging in data center cooling fluids, corrosion inhibitors, and fragrance chemicals. Heptanoate-based dielectric fluids are being explored for immersion cooling technologies used in high-density AI data centers due to their thermal stability and low volatility. In industrial applications, sodium heptanoate is gaining traction as a corrosion inhibitor for metalworking fluids, offering a safer alternative to traditional biocides and nitrites. Additionally, heptanoic acid esters are used in fragrance formulations to create fruity and wine-like aroma profiles.

Key companies operating in the Heptanoic Acid Market include Arkema S.A., OQ Chemicals GmbH, Oleon N.V., Tokyo Chemical Industry Co., Ltd., Acme Synthetic Chemicals, Kalpsutra Chemicals Pvt. Ltd., Merck KGaA, Thermo Fisher Scientific Inc., Parchem Fine & Specialty Chemicals, Inc., and Handan Kezheng Chemical Co., Ltd. These companies focus on bio-based fatty acid production, high-purity pharmaceutical-grade intermediates, and advanced oxo-technology manufacturing. Strategic initiatives include European capacity expansion, renewable feedstock integration, and development of specialty ester derivatives for aviation, automotive, and personal care applications.