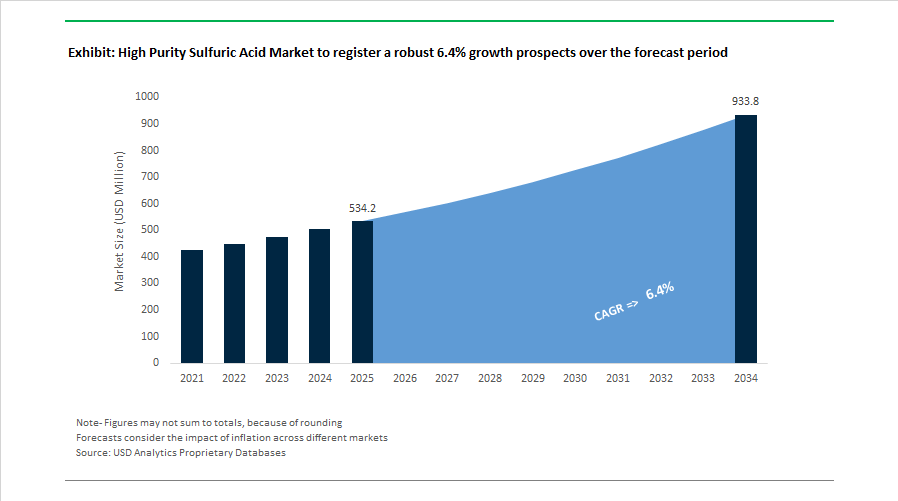

High Purity Sulfuric Acid Market to Reach $933.6 Million by 2034 at 6.4% CAGR Driven by Semiconductor-Grade Expansion and Ultra-High-Purity Standards

The High Purity Sulfuric Acid Market is projected to grow from $534.2 Million in 2025 to $933.6 Million by 2034, registering a CAGR of 6.4%. Growth is primarily fueled by the rapid expansion of semiconductor fabrication plants, tightening electronic-grade purity standards, regional self-sufficiency initiatives in sulfur-based chemicals, and increasing demand for ultra-high-purity (UHP) reagents in advanced chip manufacturing below 5nm process nodes. High purity sulfuric acid plays a critical role in wafer cleaning, semiconductor etching, advanced display panel production, and photovoltaic cell processing, where contamination thresholds are measured in parts per trillion. The market is increasingly shaped by investments in nano-scale impurity detection, closed-loop acid recycling systems, and low-carbon sulfuric acid production aligned with ESG-driven procurement policies in electronics manufacturing.

Capacity expansion accelerated across major producing regions beginning in early 2024. In January 2024, Dow Inc. announced the expansion of its Terneuzen facility in the Netherlands, adding 300,000 metric tons of sulfuric acid capacity to strengthen European supply for refining and high-precision chemical applications. In March 2024, CF Industries finalized the acquisition of INEOS Fertilizers' European assets, integrating large-scale sulfuric acid production units in the UK and Belgium to enhance regional distribution networks for purified industrial-grade acid. In May 2024, ChemChina and Qatar Chemical Company signed a strategic agreement to build a 1.5 million metric ton sulfuric acid plant in Qatar, targeting Middle East supply independence by 2026. In the first half of 2024, Sumitomo Chemical doubled its high-purity sulfuric acid capacity at Ehime Works using advanced nano-scale impurity analytics to meet the stringent quality stability requirements of next-generation logic chips. In July 2024, PVS Chemicals completed a $14.2 million Waste Heat to Power facility in Chicago, generating 95% of site electricity internally and reducing the carbon intensity of electronic-grade sulfuric acid production. In December 2024, ExxonMobil Chemical Company launched a new semiconductor-grade sulfuric acid line, formally entering the ultra-high-purity electronics chemicals segment.

Investment momentum intensified through 2025 with a clear focus on semiconductor hubs and regulatory tightening. In April 2025, BASF SE announced a high double-digit million-euro investment to construct a semiconductor-grade sulfuric acid plant at its Ludwigshafen Verbund site, with operations scheduled for 2027 to support European chipmakers. In April 2025, SABIC and Ma'aden commissioned a 1.2 million metric ton sulfuric acid joint venture facility in Saudi Arabia, reinforcing regional petrochemical and high-purity chemical supply chains. In 2025, KPCT Advanced Chemicals, a joint venture between Kanto Group and Chemtrade Logistics, confirmed operational status of its $200 million Casa Grande, Arizona greenfield facility, the first electronic-grade sulfuric acid plant of its kind in North America with 100,000 metric tons annual capacity serving the expanding Arizona semiconductor corridor. Following this opening, the partners began studying sulfuric acid recycling systems to recover and re-purify spent acid from semiconductor waste streams, advancing a circular supply model for U.S. fabrication plants. Effective July 1, 2025, China implemented the GB/T 534-2024 national standard, introducing stricter heavy metal thresholds for chromium and iron, compelling producers to upgrade to electronic-grade filtration and purification systems. In mid-2025, Merck KGaA expanded purity-control laboratories capable of detecting contaminants at single-digit parts-per-trillion levels, a prerequisite for future 2nm semiconductor node manufacturing.

The High Purity Sulfuric Acid Market is increasingly defined by semiconductor-grade H2SO4 capacity additions, ultra-high-purity analytical technologies, heavy metal contamination controls, sulfuric acid recycling systems, and low-carbon production infrastructure. Strategic investments are concentrated in Europe, North America, Japan, China, and the Middle East, reflecting regional chip manufacturing expansion and regulatory alignment with advanced electronics fabrication standards.

High-Purity Sulfuric Acid Market Trends and Opportunities Influencing Semiconductor Chemical Supply Chains

Semiconductor Fab Expansion Driving Structural Demand for PPT-Grade High Purity Sulfuric Acid

The high purity sulfuric acid market is increasingly shifting toward Parts Per Trillion (PPT) grade sulfuric acid as semiconductor manufacturing advances toward sub-2nm and Angstrom-level process nodes. At these geometries, even trace metallic contamination can disrupt wafer yield, making ultra-high purity sulfuric acid essential for wafer cleaning, photoresist stripping, and precision wet etching. Consequently, semiconductor manufacturers are prioritizing Grade 5 electronic-grade sulfuric acid to maintain process integrity in advanced logic and AI chip fabrication.

Major fab expansions are reinforcing this demand trajectory. In March 2025, TSMC expanded its U.S. investment to $165 billion to construct three new fabrication facilities, each requiring localized supplies of PPT-grade sulfuric acid. Intel plans to begin commercial production of its 18A (1.8-nm equivalent) process at Fab 52 in Arizona in 2026, further intensifying the need for ultra-pure wet chemicals. Samsung Electronics also reported a 130% projected increase in AI semiconductor orders for its 2nm process in early 2026. Supporting this ecosystem, BASF announced in April 2025 a high double-digit million-euro investment in a semiconductor-grade sulfuric acid facility in Ludwigshafen, expected to start operations in 2027 to serve Europe’s emerging mega-fab infrastructure.

Regionalized Semiconductor Supply Chains Accelerating Local Production of Electronic-Grade Sulfuric Acid

Geopolitical dynamics and semiconductor industrial policies are accelerating the regionalization of high purity sulfuric acid supply chains. Governments are encouraging localized chemical manufacturing ecosystems to minimize logistics risks and ensure contamination-controlled delivery of electronic-grade sulfuric acid to fabrication plants. This shift is particularly evident across North America and Europe as semiconductor manufacturing capacity expands rapidly.

The U.S. CHIPS and Science Act, which allocated $52.7 billion for semiconductor manufacturing incentives, has triggered more than $200 billion in private investments by 2026, creating a strong localized demand pull for semiconductor-grade wet chemicals. One example is the KPCT Advanced Chemicals joint venture between Kanto Group and Chemtrade, which is constructing a $175–$250 million facility in Casa Grande, Arizona, capable of producing 100,000 metric tons of electronic-grade sulfuric acid annually. In Europe, the EU Chips Act has mobilized over €100 billion in commitments, including the €10 billion ESMC joint venture in Dresden involving TSMC, Bosch, Infineon, and NXP, significantly reshaping regional sourcing strategies for high purity sulfuric acid used in semiconductor fabrication.

Long-Term Supply Partnerships with Semiconductor Foundries Creating Stable Demand Channels

Strategic partnerships between high purity sulfuric acid manufacturers and semiconductor foundries are emerging as a key market opportunity. Due to the strict logistics requirements associated with ultra-pure sulfuric acid transport and storage, semiconductor companies increasingly prefer on-site or nearby chemical supply arrangements. These long-term “over-the-fence” supply agreements ensure consistent quality, reduce contamination risks, and provide chemical producers with stable demand visibility.

This partnership model is already gaining traction across major semiconductor hubs. In Texas, Samsung C&T America partnered with Dongjin Semichem and Martin Resource Management to construct a dedicated electronic-grade sulfuric acid facility supplying Samsung’s Taylor semiconductor fab, scheduled for mass production in the second half of 2026. Similarly, the $5 billion collaboration between NVIDIA and Intel to manufacture Feynman AI accelerators is expected to strengthen long-term demand for PPT-grade sulfuric acid tailored to Intel’s 14A and 18A process nodes. In Europe, industry groups such as CLEPA are advocating deeper semiconductor value-chain integration to secure chip supply for software-defined vehicles, creating additional opportunities for sulfuric acid producers to integrate with regional semiconductor ecosystems.

Spent Acid Regeneration and Circular Chemical Systems Creating Sustainability-Driven Market Opportunities

The growing emphasis on sustainability and cost optimization is driving innovation in spent acid regeneration (SAR) technologies within the high purity sulfuric acid market. Semiconductor fabs generate significant volumes of used sulfuric acid during wafer cleaning processes, creating opportunities to implement closed-loop recycling systems that convert waste acid back into electronics-grade sulfuric acid. These systems reduce environmental impact, lower raw material costs, and align with stricter global environmental regulations.

Several companies are actively investing in this circular model. MECS Inc., part of Elessent Clean Technologies, recently partnered with Taiwan’s SAR Technology Inc. to deploy advanced equipment for a spent acid regeneration facility designed to recycle semiconductor process acid into high-purity sulfuric acid. Meanwhile, Mitsubishi Gas Chemical expanded its electronic materials operations in 2025 as part of a green chemicals strategy focused on closed-loop sulfuric acid recycling, with systems capable of reducing hazardous waste by 30–40%. Complementing these initiatives, Mitsubishi Chemical Group’s ¥280 billion growth investment strategy includes research into purification technologies that can upgrade industrial-grade sulfuric acid into semiconductor-grade material, supporting the long-term sustainability of the global high purity sulfuric acid supply chain.

High Purity Sulfuric Acid Market Share and Segmentation Insights

Electronic Grade Sulfuric Acid Leads the High Purity Sulfuric Acid Market for Semiconductor Processing

Electronic Grade accounted for 52.80% of the High Purity Sulfuric Acid Market share in 2025, making it the dominant grade used in advanced electronic manufacturing processes. Electronic grade sulfuric acid is produced with extremely high purity levels, typically at concentrations of 96–98%, with metal contaminants reduced to parts-per-trillion concentrations, ensuring compatibility with sensitive semiconductor fabrication processes. This ultra-pure chemical is widely used in wafer cleaning, photoresist stripping, and surface preparation steps in semiconductor fabrication plants. Semiconductor manufacturing requires highly controlled chemical environments where even trace contaminants can compromise microchip performance and yield, making electronic grade sulfuric acid an essential process chemical. In 2025, increasing semiconductor manufacturing complexity has driven the adoption of advanced purification technologies including multi-stage distillation, membrane filtration systems, and getter-based impurity removal techniques. Additionally, specialized packaging solutions such as fluorinated polymer containers and quartz-lined transport vessels are being used to maintain ultra-high purity from production facilities to semiconductor fabrication plants.

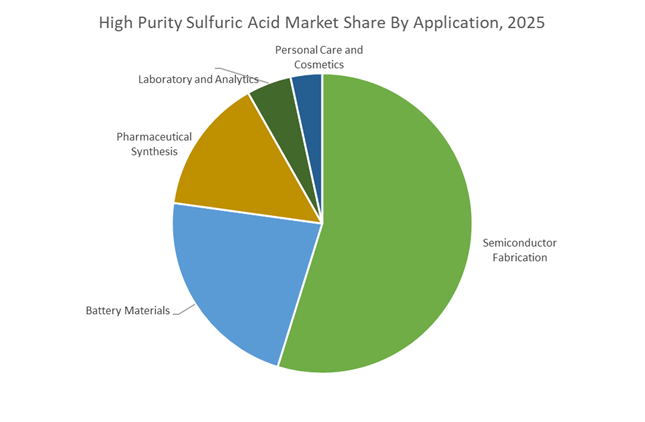

Semiconductor Fabrication Drives the Largest Demand for High Purity Sulfuric Acid

Semiconductor Fabrication represented 54.80% of the High Purity Sulfuric Acid Market share in 2025, establishing it as the primary application sector for ultra-pure sulfuric acid chemicals. In semiconductor manufacturing, sulfuric acid plays a central role in wet chemical processing steps used during wafer fabrication, including photoresist removal, wafer cleaning, oxide etching, and organic contaminant removal. Each semiconductor wafer undergoes multiple chemical cleaning cycles throughout production, resulting in substantial consumption of high purity sulfuric acid across fabrication facilities. As semiconductor devices become more advanced, particularly with the development of sub-5 nanometer process nodes and advanced transistor architectures, the demand for ultra-pure process chemicals has intensified. In 2025, semiconductor manufacturers are increasingly implementing closed-loop sulfuric acid recycling systems within fabrication plants. These systems recover and purify spent sulfuric acid through advanced filtration and reconcentration processes, enabling 80–90% reuse of process chemicals while maintaining the strict purity requirements needed for advanced semiconductor production.

Competitive Landscape in High Purity Sulfuric Acid Market

BASF SE Expands Semiconductor-Grade Capacity for Sub-5nm Fabrication

BASF SE leverages its Verbund integration model to supply ultra-high-purity sulfuric acid tailored for semiconductor manufacturing. In April 2025, BASF announced a strategic investment to expand semiconductor-grade sulfuric acid production at Ludwigshafen, reinforcing Europe’s position in advanced electronic chemicals. The company is targeting next-generation chip fabrication, specifically sub-5nm nodes where defect minimization and metal contamination control are mission-critical. BASF’s ultra-pure grades achieve impurity concentrations in the parts-per-trillion range, meeting stringent wafer cleaning and etching requirements. Its global supply network ensures consistent electronic-grade sulfuric acid delivery across Europe, Asia, and North America, positioning BASF as a primary supplier to leading semiconductor foundries.

Mitsubishi Chemical Group Drives Ultra-Low Metal Impurity Standards

Mitsubishi Chemical Group remains a core technology leader in high purity process chemicals through its Star Series sulfuric acid portfolio. These electronic-grade acids reduce metal impurities to below 10 ppt, enabling advanced silicon wafer cleaning for miniaturized integrated circuits. In 2026, Mitsubishi Chemical is collaborating directly with semiconductor manufacturers to co-develop chemical solutions that adapt to rapid device scaling and advanced lithography processes. The company holds a significant share among the top global producers of semiconductor-grade sulfuric acid. Its advanced quality control systems ensure high-efficiency removal of metallic contaminants, critical for maintaining yield in extreme ultraviolet lithography environments.

Kanto Chemical Strengthens U.S. Semiconductor Localization Strategy

Kanto Chemical Co., Inc. is a specialized leader in electronic-grade reagents, recognized for its Ultrapur technology platform. Through its joint venture KPCT Advanced Chemicals LLC with Chemtrade Logistics, the company established a 100,000 metric ton electronic-grade sulfuric acid facility in Casa Grande, Arizona. The plant reached full operational status in late 2024 and early 2025, supporting the rapidly expanding U.S. semiconductor manufacturing base. Kanto’s Ultrapur-100 series guarantees metal impurity levels as low as 100 ppt and utilizes Teflon-coated packaging systems to eliminate contamination risks from container materials. Its localized production strategy aligns with domestic sourcing requirements under U.S. semiconductor incentive programs, reducing logistical vulnerabilities in high purity chemical supply chains.

Chemtrade Logistics Ramps Up North American Ultra-Pure Acid Capacity

Chemtrade Logistics Income Fund is the primary North American manufacturer of ultra-pure sulfuric acid for semiconductor applications. In February 2026, the company reported record Adjusted EBITDA of $507.4 million for 2025, with electronic-grade acid identified as a major growth driver. Chemtrade is executing the commercial ramp-up of its new ultrapure sulfuric acid facility in Cairo, Ohio, with customer qualification processes extending through 2026. The company also completed quality upgrades at its Tulsa, Oklahoma plant to enhance impurity control and reliability. With 2026 EBITDA guidance between $485 million and $525 million, Chemtrade emphasizes a step-change in earnings potential driven by high purity and regenerated acid portfolios serving the domestic electronics sector.

PVS Chemicals Advances Sustainable Domestic Electronic-Grade Production

PVS Chemicals, Inc. has transitioned from industrial sulfuric acid dominance into a competitive position in the electronic-grade segment. The company upgraded its purification infrastructure to target semiconductor foundries across the North American Silicon Heartland. In partnership with Energy Systems Group, PVS installed a Waste Heat to Power facility at its Chicago plant, generating 2.6 MW of renewable electricity and powering approximately 95% of site operations. Its sterile, high-purity sulfuric acid grades support semiconductor production, pharmaceutical synthesis, and solar cell manufacturing. Advanced filtration and polishing technologies allow PVS to meet stringent purity specifications required for cleanroom and advanced wafer processing environments.

Avantor Integrates Digital Purity Assurance for Cleanroom Supply Chains

Avantor, Inc., under the J.T. Baker brand, supplies electronic-grade sulfuric acid that meets and exceeds SEMI Tier 5 standards. The company is integrating digital purity assurance systems into its logistics framework, utilizing QR-verified packaging and real-time digital certificates of analysis to support cleanroom traceability. In 2026, Avantor is capitalizing on semiconductor expansion in Taiwan, South Korea, and the United States by offering integrated chemical management services alongside high purity acid supply. The company maintains a strong footprint in pharmaceutical manufacturing, where its sulfuric acid products comply with cGMP and ICH Q7 guidelines. This dual exposure to semiconductor fabrication and life sciences strengthens Avantor’s positioning in mission-critical ultra-high-purity chemical markets.

Germany: Semiconductor-Grade Localization and Decarbonized Acid Manufacturing

Germany is rapidly positioning itself as the anchor market for high purity sulfuric acid in Europe, driven by semiconductor sovereignty goals and stringent contamination thresholds for advanced wafer fabrication. In April 2025, BASF announced a major investment in a new semiconductor-grade sulfuric acid unit at its Ludwigshafen Verbund site. The facility is engineered with next-generation purification and distillation systems to address a high double-digit million-euro demand surge from European chip manufacturers. This expansion directly supports rising consumption from logic and memory fabs that require ultra-clean wet processing chemicals.

Policy alignment is a central driver. Under the European Chips Act, Germany is prioritizing localized chemical supply chains to reduce dependence on Asian imports. BASF’s new unit is scheduled to come online by 2027, synchronized with the ramp-up of multiple European semiconductor fabrication lines. R&D intensity is also increasing. German research teams are advancing parts-per-trillion grade sulfuric acid suitable for sub-5nm process nodes, where metal ion contamination must remain below 10 ppt to avoid yield loss. Parallel to purity upgrades, Germany is piloting decarbonized production pathways. Chemical clusters are testing green-hydrogen-derived sulfur inputs and electrified heat recovery systems to comply with the 2026 EU Industrial Emissions Directive, embedding sustainability into high purity acid manufacturing.

China: Feedstock Volatility and Rapid Transition to PPT-Grade Production

China’s high purity sulfuric acid industry is undergoing accelerated transformation, shaped by feedstock price pressure and aggressive electronic chemical localization. Domestic sulfur prices peaked above 3,800 RMB per ton in late 2025, reflecting sharp demand growth from solid-state battery manufacturing, where sulfuric acid is a key reagent for lithium sulfide synthesis. This price dynamic has reinforced the strategic importance of sulfur integration and recovery across China’s chemical value chain.

Industrial policy is reinforcing capacity expansion. Under the 15th Five-Year Plan directives issued by the Ministry of Industry and Information Technology, localization of electronic special chemicals has been prioritized, particularly for 12-inch wafer fabrication. State-owned leaders Sinopec and PetroChina expanded high-purity refining capacity by approximately 18% in 2025 to supply semiconductor and lithium iron phosphate battery hubs in East China. Technological capability has also advanced. By late 2025, Chinese producers successfully transitioned from G3 parts-per-billion grades to G5 parts-per-trillion mass production, enabling domestic support for 7nm process technology and reducing reliance on imported electronic-grade acids.

United States: Semiconductor Corridors and Battery Mineral Processing

The United States high purity sulfuric acid market is expanding at the intersection of semiconductor reshoring and domestic battery mineral processing. Federal CHIPS Act grants distributed in 2025 accelerated over-the-fence supply models, prompting U.S. producers to expand ultra-high purity sulfuric acid lines in the Arizona and Texas semiconductor corridors. These facilities are designed to deliver continuous, contamination-controlled supply directly to fabs, minimizing logistics risk and process variability.

Industry consolidation has reinforced domestic capacity. In March 2025, Ecovyst completed the acquisition of sulfuric acid assets from Cornerstone Chemical in Louisiana, significantly expanding access to both virgin and regenerated high-purity acid across the Gulf Coast. Demand is also rising from energy transition sectors. Late 2025 policy shifts under the Inflation Reduction Act increased domestic processing of nickel and cobalt for EV batteries, driving higher consumption of high purity leaching acids. In pharmaceuticals, updated 2026 purity expectations under FDA and USP frameworks have pushed manufacturers to upgrade analytical labs with ICP-MS systems for real-time trace metal detection, raising the bar for pharmaceutical-grade sulfuric acid qualification.

Japan: Export-Led Growth and Traceability-Driven Quality Control

Japan continues to play a critical role as a high purity sulfuric acid exporter and technology leader. In October 2025, Japanese exporters recorded a 135% year-on-year increase in sulfuric acid shipments, primarily serving high-tech manufacturing clusters in the Philippines and India. This export growth reflects Japan’s strength in producing consistently clean acid grades trusted by electronics and specialty materials customers.

Strategic focus is shifting toward advanced materials and licensing. Following the 2026 sale of Ecovyst’s advanced materials segment to Technip Energies, Japanese firms such as Mitsubishi Chemical intensified efforts around electrolyte licensing and high purity intermediates for AI server thermal management and advanced electronics. Circular economy leadership is also emerging. At Expo 2025 Osaka, Japanese chemical producers showcased digital traceability platforms that track high purity acids from sulfur sourcing through electronics manufacturing and eventual recycling, reinforcing Japan’s reputation for quality assurance and lifecycle accountability.

India: Quality Mandates and Semiconductor-Linked Logistics Expansion

India’s high purity sulfuric acid industry is transitioning from fragmented supply toward regulated, application-specific consumption driven by semiconductors and pharmaceuticals. In May 2026, the Ministry of Chemicals and Fertilizers enforced the H Acid Quality Control Second Amendment Order, making Bureau of Indian Standards certification mandatory for high-purity derivatives. This regulation is raising baseline quality expectations and favoring suppliers capable of consistent electronic and pharmaceutical-grade output.

Infrastructure investments are reinforcing demand. Under the Sagarmala Project, India expanded port-side chemical storage and handling hubs during 2025–2026 to support the India Semiconductor Mission, facilitating import and domestic movement of electronic-grade acids. Pharmaceutical demand is also scaling. In late 2025, government approval of 12 new Bulk Drug Parks increased localized consumption of high purity sulfuric acid for active pharmaceutical ingredient synthesis, positioning India as a growing downstream consumer of regulated, high-specification acids.

Summary Table: Country-Level Strategic Signals in the High Purity Sulfuric Acid Industry

High Purity Sulfuric Acid Market County Level Snapshot

|

Country

|

Strategic Driver

|

Primary Application Focus

|

Structural Implication

|

|

Germany

|

Chips Act alignment, decarbonization

|

Semiconductor wet processing

|

Localized, low-carbon PPT-grade supply

|

|

China

|

ESC localization, sulfur integration

|

Semiconductors, solid-state batteries

|

Rapid scale-up to G5-grade self-sufficiency

|

|

United States

|

CHIPS Act, IRA battery policy

|

Fabs, EV mineral refining, pharma

|

Corridor-based UHP capacity expansion

|

|

Japan

|

Export growth, traceability platforms

|

Electronics, advanced materials

|

Quality-led export dominance

|

|

India

|

BIS mandates, logistics investment

|

APIs, semiconductor chemicals

|

Regulated demand and infrastructure-led growth

|

High Purity Sulfuric Acid Market Report Scope

High Purity Sulfuric Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$534.2 Million

|

|

Market Size (2034)

|

$933.6 Million

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Grade (Electronic Grade, Pharmaceutical Grade, Reagent Grade, Industrial High-Purity Grade), By Application (Semiconductor Fabrication, Pharmaceutical Synthesis, Battery Materials, Laboratory and Analytics, Personal Care and Cosmetics), By End-Use Industry (Electronics and Semiconductors, Healthcare and Pharmaceuticals, Energy and Energy Storage, Chemical and Petrochemical Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Mitsubishi Chemical Group, Sumitomo Chemical Co., Ltd., Kanto Chemical Co., Inc., PVS Chemicals, Inc., Ecovyst Inc., FUJIFILM Wako Pure Chemical Corporation, Avantor, Inc., Asia Union Electronic Chemical Corp., Chemtrade Logistics, LS MNM, INEOS Group, Jianghua Microelectronics Materials, UBE Corporation, Sinopec Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Purity Sulfuric Acid Market Segmentation

By Grade

- Electronic Grade

- Pharmaceutical Grade

- Reagent Grade

- Industrial High-Purity Grade

By Application

- Semiconductor Fabrication

- Pharmaceutical Synthesis

- Battery Materials

- Laboratory and Analytics

- Personal Care and Cosmetics

By End-Use Industry

- Electronics and Semiconductors

- Healthcare and Pharmaceuticals

- Energy and Energy Storage

- Chemical and Petrochemical Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the High Purity Sulfuric Acid Industry

- BASF SE

- Mitsubishi Chemical Group

- Sumitomo Chemical Co., Ltd.

- Kanto Chemical Co., Inc.

- PVS Chemicals, Inc.

- Ecovyst Inc.

- FUJIFILM Wako Pure Chemical Corporation

- Avantor, Inc.

- Asia Union Electronic Chemical Corp.

- Chemtrade Logistics

- LS MNM

- INEOS Group

- Jianghua Microelectronics Materials

- UBE Corporation

- Sinopec Group

*- List not Exhaustive