Market Overview: Circular Economy Efficiency and Advanced Lead Batteries Drive the Global Lead Market Outlook

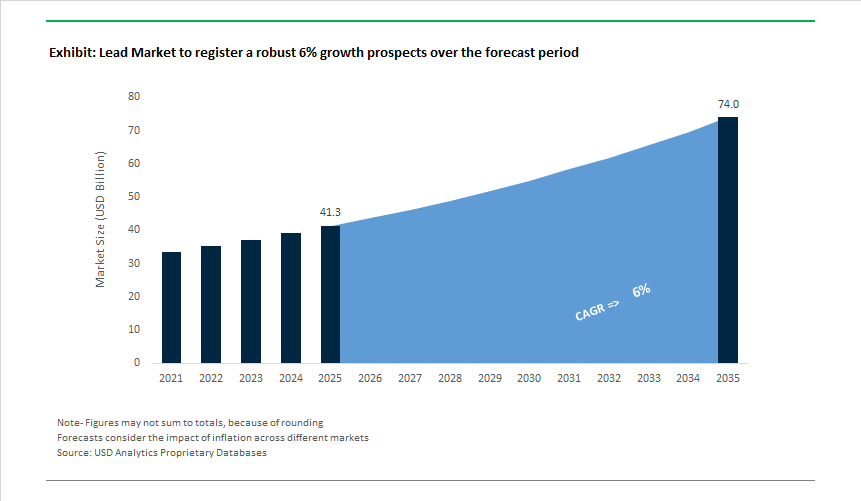

The Global Lead Market stands at USD 41.3 billion in 2025 and is projected to reach USD 74.0 billion by 2035, expanding at a 6.0% CAGR as lead consolidates its role as one of the most industrially resilient and circular metals in the global materials system. Today, lead is not competing on novelty; it is winning on supply certainty, recyclability, cost-per-kWh, and regulatory maturity, particularly in battery-centric applications where reliability outweighs chemistry experimentation.

The market’s structural strength is anchored in unmatched circular economy efficiency. In developed markets, lead recycling rates exceed 99%, and secondary lead now supplies 60-70% of global refined output, insulating battery manufacturers from upstream mining volatility. This recycling dominance transforms lead into a closed-loop industrial metal, where availability is driven by collection efficiency and smelting capacity rather than ore discovery. For producers and OEMs, competitive advantage today is being built around vertically integrated recycling networks, high-purity alloy control, and regional smelting scale, rather than access to primary mines.

Demand growth is being driven by the evolution of lead-acid battery technology, not by legacy usage alone. Advanced Lead Batteries-particularly AGM (Absorbent Glass Mat), EFB (Enhanced Flooded Battery), and TPPL (Thin Plate Pure Lead) formats-are becoming standard requirements for start-stop vehicles, micro-hybrids, telecom infrastructure, motive power, and data center UPS systems. These applications require higher lead purity, thicker grids, and superior dynamic charge acceptance, structurally increasing lead intensity per battery even as vehicle electrification progresses.

In automotive markets, start-stop and micro-hybrid systems are crossing critical adoption thresholds, with penetration expected to exceed 60% by 2027. These vehicles typically require 10-15% more lead per battery compared with conventional SLI systems due to partial-state-of-charge operation and durability demands. Rather than declining, automotive lead demand is therefore shifting toward higher-value battery formats, reinforcing volume stability and margin potential for advanced lead producers.

Non-automotive demand provides an additional layer of resilience. Hyperscale data centers, cloud infrastructure, and 5G telecom networks continue to specify VRLA and AGM batteries for uninterruptible power supply (UPS) and backup systems because of their instant response, proven safety, predictable degradation, and recycling simplicity. These segments already account for 15-20% of non-automotive lead demand, and their expansion ties lead consumption directly to digital infrastructure growth rather than internal combustion vehicle cycles.

In addition, lead’s competitive position is reinforced by its regulatory clarity and low system risk. Unlike newer battery chemistries, lead-acid systems benefit from decades of standardized handling, transport, recycling, and environmental compliance frameworks. This reduces permitting friction, accelerates deployment, and lowers lifecycle uncertainty for utilities, telecom operators, and fleet managers-factors that are increasingly valued as infrastructure scales.

Market Analysis: Recycling Expansion, Technology Upgrades and Strategic Battery Investments Reshape the Global Lead Industry

Strategic developments underscore the Lead Industry's transition toward capacity expansion, circularity leadership, and advanced battery innovation. In October 2025, Recyclus Group announced a major expansion of its Tipton, UK plant from 16,000 t/year to 80,000 t/year by 2027, reinforcing Europe’s shift toward secure, closed-loop battery recycling ecosystems. On the other hand, the United States strengthened domestic supply chain resilience when the U.S. DoD issued a new contract in September 2025 prioritizing domestic suppliers of AGM batteries for military vehicles, reaffirming Lead’s role in auxiliary and mission-critical energy systems. This followed January 2025, when Clarios expanded its North American footprint via acquisition of select battery manufacturing assets, consolidating its leadership in start-stop AGM battery supply.

Innovation-led market activity also accelerated. In July 2025, EnerSys introduced a new generation of TPPL (Thin Plate Pure Lead) batteries offering higher cycle life and improved power density for motive power and material-handling applications, reinforcing demand for ultra-high purity lead alloys. China continued to demonstrate strong utilization of recycled lead, with the China Nonferrous Metals Industry Association reporting a 5% QoQ rise in secondary smelter utilization in June 2025, driven by EV auxiliary battery and e-bike demand. Earlier, in February 2025, Exide Industries entered a joint venture to supply large-scale lead-acid ESS solutions for solar farm integration-evidence of lead-acid’s continued cost advantage for grid-balancing and short-duration ESS.

Primary supply also saw selective investments: Grupo México’s April 2025 commitment to expand Peruvian Pb-Zn mining capacity provided modest relief to primary concentrate availability. On the other hand, technological advances continue to elevate battery performance; November 2024 academic studies confirmed that carbon additive technologies can improve dynamic charge acceptance in VRLA batteries by up to 40%, enhancing competitiveness for grid services and renewable-firming applications. These combined developments reflect a market experiencing consistent innovation, responsible recycling expansion, and sustained demand across automotive, telecom, industrial, and ESS sectors.

Lead Market Trends and Opportunities

Trend 1: Strategic Investment in Advanced Lead-Carbon Batteries for Grid-Scale Storage

Advanced lead-carbon batteries are increasingly being positioned as a value-tier, safety-first solution for long-duration stationary energy storage, particularly in grids with high renewable penetration. Unlike lithium-based systems that face thermal runaway risks and complex end-of-life challenges, lead-carbon systems leverage a mature recycling ecosystem with circularity rates exceeding 99%, making them attractive for utilities and policymakers prioritizing lifecycle sustainability. This positioning has moved from theory to large-scale execution. Between 2024 and 2025, China commissioned the world’s largest lead-carbon long-duration energy storage (LDES) installation in Huzhou, deploying roughly 3 million 2V lead-carbon AGM batteries to deliver 1 GWh of storage with a 10-hour discharge profile. The project demonstrates that lead-based chemistries can operate at grid-relevant scale while maintaining predictable degradation behavior and high safety margins. Performance improvements are equally critical. Recent 2025 evaluations show that lead-carbon batteries exhibit around 32% lower capacity fade after 1,500 cycles compared to conventional lead-acid, primarily due to carbon additives that suppress sulfation under partial-state-of-charge (PSoC) operation. This allows utilities to cycle systems more aggressively for renewable smoothing without premature failure. On the policy side, the U.S. Department of Energy’s Energy Storage Grand Challenge has set a $35/kWh cost target for advanced lead technologies, with national laboratories actively working to push cycle life toward the 3,000-cycle threshold. Collectively, these developments signal a structural re-rating of lead from a “legacy battery metal” to a strategic enabler of cost-effective, recyclable grid storage.

Trend 2: Tightening Export Controls and Formalization of Secondary Lead Supply Chains

The global lead market is undergoing a regulatory reset as governments tighten controls on the export and processing of used lead-acid batteries (ULAB) and lead-bearing scrap, fundamentally reshaping secondary supply dynamics. Historically, a significant share of lead recycling relied on cross-border flows to loosely regulated smelters, particularly in parts of Southeast Asia and Africa. That model is rapidly being dismantled. Effective January 1, 2025, amendments under the Basel Convention brought all lead-containing scrap under strict Prior Informed Consent (PIC) requirements, sharply restricting unregulated exports and favoring regions with integrated, compliant recycling infrastructure. This shift disproportionately benefits North America and Europe, where secondary lead already satisfies roughly 90% of domestic demand and environmental controls are deeply embedded. In Europe, the December 2025 launch of the REsourceEU plan reinforced this trajectory by allocating €3.2 billion to accelerate domestic battery recycling and by moving toward classifying lead-containing “black mass” as hazardous waste by early 2026—a change that effectively closes export pathways to informal smelters. China is pursuing a parallel consolidation strategy. Under proposals tied to the 16th Five-Year Plan, secondary lead producers are now required to reinvest at least 3% of annual revenue into emissions control R&D, with non-compliant operators facing forced relocation into designated industrial parks. The combined effect of these policies is a structural tightening of compliant secondary lead supply, increased pricing power for Tier-1 recyclers, and a higher barrier to entry for informal producers—strengthening lead’s ESG profile while reinforcing supply security.

Opportunity 1: High-Purity Lead for Small Modular Reactors and Advanced Nuclear Systems

The accelerating deployment of small modular reactors (SMRs) and Generation IV nuclear designs is opening a high-margin, technology-driven opportunity for lead as both a shielding material and a primary coolant. Unlike water-cooled reactors, lead-cooled fast reactors operate at atmospheric pressure and leverage lead’s exceptionally high boiling point of 1,749 °C to deliver inherent safety advantages. In April 2025, Sweden’s SEALER reactor program advanced its commercialization roadmap using liquid lead coolant, underscoring growing confidence in lead-based thermal hydraulics for compact reactor cores. As SMRs are increasingly targeted for deployment near industrial clusters and urban load centers, radiation shielding requirements are becoming more stringent. Lead remains the material of choice for modular gamma-ray shielding due to its unmatched density, attenuation efficiency, and ease of prefabrication into standardized blocks suitable for serial reactor manufacturing. Beyond shielding, more than half of advanced reactor concepts currently in licensing rely on lead or lead-bismuth eutectic alloys for core cooling and neutron management. This creates a specialized demand for nuclear-grade, ultra-low-impurity lead ingots, a segment largely insulated from battery-driven price volatility and increasingly attractive to producers capable of meeting stringent nuclear certification standards.

Opportunity 2: Corrosion-Resistant Lead Linings for Chemical and Metallurgical Infrastructure

Despite advances in polymers and composite materials, lead’s unparalleled resistance to sulfuric acid and other aggressive chemicals continues to secure its role in critical chemical-processing infrastructure. This demand is structurally linked to the global sulfuric acid value chain, which underpins fertilizer production, base-metal refining, and uranium processing. In 2025, sulfuric acid production remained a core driver of lead sheet demand, particularly in China and India, where governments are expanding phosphate fertilizer capacity to reinforce food security. At the same time, a large share of chemical plants and metallurgical facilities in North America and Europe are entering a maintenance super-cycle, as assets built 30–40 years ago require relining to comply with modern environmental and safety standards. Lead sheets and antimonial lead alloys are being re-specified for storage tanks, electrowinning cells, and acid handling systems due to their long service life and predictable corrosion behavior. This resilience extends into uranium leaching and copper electrowinning operations, where lead anodes and linings remain irreplaceable for electrochemical stability. As new mining and processing projects come online in jurisdictions such as Canada and Australia to secure critical mineral supply, lead’s role as a quiet but indispensable infrastructure material is set to remain a stable, high-reliability revenue stream within the broader metals landscape.

Market Share Analysis: Lead Market

Market Share by Type: Recycled (Secondary) Lead Anchors Cost, Carbon, and Supply Stability

Recycled (secondary) lead accounts for approximately 62% of the global lead market, reflecting a structural advantage that no other base metal currently matches: true closed-loop recyclability at industrial scale. Lead-acid batteries remain the most successfully recycled consumer product worldwide, with 99% recovery rates validated by Battery Council International and global producers. For buyers, this translates into an unusually resilient supply chain insulated from mining disruptions, permitting risks, and geopolitical volatility that increasingly affect primary lead output. The economics are equally compelling—technical disclosures from Boliden and Ecobat confirm that secondary lead production delivers a 65% lower carbon footprint and requires 35% less energy than primary smelting, making recycled lead one of the few industrial metals that simultaneously reduces cost and Scope 3 emissions. Critically, lead’s metallurgy enables infinite recycling without purity loss, a point reinforced by Boliden’s 2025 desulfurization upgrades that pushed recycled lead emissions below 1 kg CO₂ per kg of lead—a benchmark now shaping procurement policies across automotive, industrial, and energy-storage OEMs. As carbon pricing tightens and ESG-linked financing becomes standard, these attributes explain why secondary lead is structurally irreplaceable in the current materials landscape.

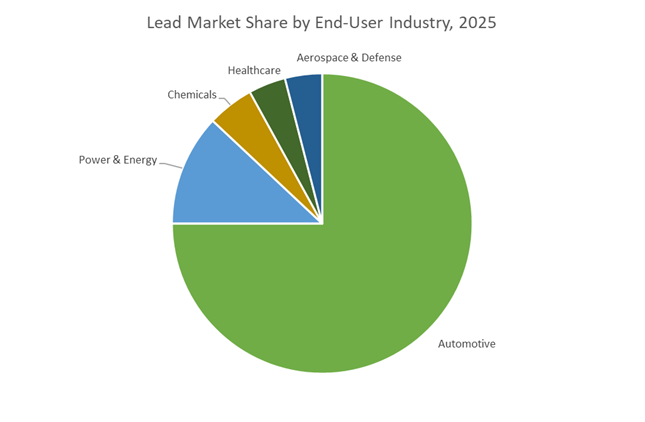

Market Share by Application: Automotive Demand Locks in Volume Through Circular Battery Economics

Automotive applications command roughly 75% of global lead demand, underscoring the enduring relevance of lead-acid batteries even as lithium-ion adoption accelerates. The market reality is operational rather than technological: every internal combustion vehicle and virtually every electric vehicle still requires a 12V lead-acid battery to power safety-critical systems, sensors, and control units. Clarios alone reports that its batteries are installed in one out of every three vehicles globally, supported by an industrial-scale recycling network capable of processing 8,000 batteries per hour—a throughput unmatched by any competing battery chemistry. This circular infrastructure underpins cost leadership, enabling lead-acid systems to remain the lowest-risk, lowest-cost solution for automotive auxiliary power in 2025. Strategic investment is reinforcing this dominance: Clarios’ USD 6 billion American Energy Manufacturing Strategy aims to add 400,000 metric tons of domestic recycling capacity, directly addressing supply security concerns for North American OEMs. At the product level, manufacturers such as Exide Industries and EnerSys have standardized 100% recyclable battery designs, recovering lead, plastic, and electrolyte with zero residual waste. This “zero-waste automotive battery” model aligns perfectly with 2025 circular-economy regulations, locking automotive manufacturing into lead’s ecosystem and sustaining its overwhelming application share.

Competitive Landscape: Vertically Integrated Recyclers and Mining Majors Shape the Global Lead Industry

The global Lead Industry is defined by the interplay of large miners, vertically integrated battery manufacturers, and advanced stored energy solution providers. Competitive differentiation increasingly depends on circularity leadership, low-cost primary lead production, innovation in AGM/EFB/TPPL technologies, and regional supply chain resilience. Companies that successfully integrate mining, recycling, and advanced grid or automotive storage solutions are poised to lead the next decade of growth.

Glencore Plc - Global Primary Lead Supply Backbone With Integrated Mining and Smelting

Glencore is one of the world’s largest producers of zinc-lead ore through operations such as Mount Isa and McArthur River. Its integrated model-including smelting and refining assets across Australia and Europe-ensures stable flows of high-purity primary lead metal to global markets. With ongoing decommissioning of older, high-emission assets and reinvestment in efficient operations, Glencore strengthens its role as a cost leader. Its global marketing division provides hedging and price-risk management services to major battery OEMs, reinforcing its strategic importance in the Lead value chain.

Clarios LLC - Dominant Lead-Acid Battery Manufacturer With Closed-Loop Recycling Leadership

Clarios controls roughly one-third of the North American lead-acid battery market and operates a highly advanced closed-loop recycling system, sourcing 99% of its lead from recycled inputs. Its strategic emphasis on AGM/EFB batteries for start-stop vehicles and micro-hybrid systems keeps it at the forefront of automotive decarbonization trends. With over 35 facilities worldwide, Clarios offers unmatched supply reliability to global OEMs, while its investments in thin-plate technology continue to improve battery efficiency and charge acceptance.

Enersys - TPPL Technology Pioneer For Motive Power, Telecom, and Industrial Applications

EnerSys is a global leader in Thin Plate Pure Lead (TPPL) technology, leveraging ultra-pure 99.99% lead grids to deliver superior cycle life and deep-discharge performance. Following a multi-year expansion program that increased TPPL production capacity by 15%, the company now serves critical UPS, telecom, motive power, and defense sectors. EnerSys’ ruggedized lead batteries remain widely adopted across military and industrial environments that require high reliability under variable load and temperature conditions.

Hindustan Zinc Ltd. - India’s Integrated Lead Producer Supporting Rapid Automotive and Inverter Demand

Hindustan Zinc remains India’s sole primary lead producer and operates one of the world’s largest integrated zinc-lead mining complexes. The company recorded strong refined lead production in FY2025, supplying rapidly expanding domestic markets such as automotive SLI and inverter batteries. Its expansion of lead concentrate capacity at the Rampura Agucha Mine-targeting a 20% output increase by mid-2026-strengthens India’s strategic supply base. Strong by-product recovery of silver and cadmium further lowers net production costs, improving the competitiveness of its primary lead output.

GS Yuasa Corporation - Advanced Lead Battery Supplier For Global Automotive and Industrial Systems

GS Yuasa serves as a key supplier of SLI and AGM battery systems to Japanese and European automotive OEMs, meeting stringent quality, cold-cranking, and durability requirements. Its research programs in lead-carbon hybrid batteries highlight efforts to improve charge acceptance and cycle life for renewable ESS applications. With production and recycling operations across Asia, Europe, and North America, GS Yuasa maintains broad integration capabilities. The company also holds a strong position in motorcycle and powersports batteries, a segment that demands high-performance, compact designs.

The United States lead market in 2025 is defined by an aggressive reshoring and industrial revitalization strategy, aimed at reducing long-standing dependence on Asian refined lead while strengthening national security supply chains. The most transformative development is Korea Zinc’s USD 7.4 billion “U.S. Smelter” investment in Clarksville, Tennessee, announced in December 2025. Designed as a multi-metal critical minerals complex, the facility will process 1.1 million tons of raw material annually, producing refined lead alongside zinc and copper using next-generation, low-emission smelting technologies. This project marks the largest U.S. investment in lead processing infrastructure in decades and directly aligns with federal objectives to localize battery and defense material supply.

Parallel to smelting investments, the revival of the Bunker Hill Mine in Idaho signals a renewed commitment to primary lead mining under modern environmental standards. Unlike legacy operations, the project incorporates advanced containment and effluent control systems, addressing ESG concerns that historically constrained U.S. lead output. Reinforcing this momentum, the USGS 2025 Critical Minerals update reaffirmed lead’s role in backup power systems, defense electronics, and grid resilience, enabling accelerated federal approvals for secondary lead recycling plants, which now account for the majority of domestic supply growth.

Australia – Autonomous Mining and High-Grade Lead-Zinc Optimization

Australia’s lead market strategy in 2025 emphasizes technological efficiency over volume expansion, allowing the country to remain a top-tier exporter despite selective mine closures. The Abra Base Metals Mine in Western Australia, which reached nameplate capacity in late 2025, has become a global reference point for autonomous and 5G-enabled mining operations. Private 5G networks, tele-remote dozing, and automated haulage systems have significantly lowered operating costs per ton of lead-zinc concentrate, improving Australia’s competitiveness even amid volatile global prices.

While mature assets such as the Potosi/Silver Peak mines approach closure due to reserve depletion, output stability has been preserved through life extensions at high-grade operations like South32’s Cannington mine, which reported stronger-than-expected grades in H2 2025. Strategically, Australia has repositioned its lead-zinc-silver deposits as “low-ESG-risk” supply sources through a 2025 critical minerals diversification agreement, making Australian lead increasingly attractive to European and North American refiners seeking transparent, regulation-aligned inputs.

China – Regulatory Tightening and Secondary Lead Consolidation

China remains the world’s largest producer and consumer of lead, but its 2025 market profile reflects a shift from scale-driven expansion to regulated, quality-focused growth. Nationwide environmental inspections during FY 2024–25 temporarily disrupted production in major smelting hubs such as Henan and Yunnan, pushing China into net refined lead imports during peak demand periods. This reversal exerted upward pressure on global LME prices and highlighted the tightening regulatory environment facing domestic producers.

Following the Two Sessions policy announcements, Beijing introduced targeted industrial stimulus measures that boosted demand for e-bikes, telecom backup systems, and renewable energy storage, all heavily reliant on lead-acid batteries. At the same time, the MIIT increased mandatory recycled content thresholds for new batteries, accelerating consolidation among secondary lead smelters. Smaller, inefficient recyclers are being phased out, while large, compliant operators gain scale—cementing recycled lead as the structural backbone of China’s long-term supply model.

India – Solar Grid Storage and Recycling-Led Growth

India’s lead market in 2025 is being reshaped by explosive growth in solar energy storage and advanced recycling infrastructure. Lead recycling has become a strategic priority, with companies like Gravita India Ltd. reporting record throughput at its Mundra Port facility and expanding turnkey smelting solutions across 70+ countries. India’s stringent Battery Waste Management Rules (BWMR) have created one of the world’s most structured secondary lead ecosystems, positioning the country as a global hub for compliant recycling technologies.

Logistics reforms are playing a pivotal role. The National Logistics Policy (NLP) 2025, highlighted in the LEADS 2024–25 report, has significantly reduced the cost of transporting scrap batteries to recycling centers—critical as India scales toward its 284 GW solar capacity target. On the primary supply side, Hindustan Zinc’s ramp-up at the Sindesar Khurd and Zawar mines ensures steady domestic lead availability, supporting India’s rapidly expanding data center and telecom backup power infrastructure under the Digital India initiative.

European Union – Circular Economy Enforcement and Green Lead Premiums

The European Union lead market in 2025 is defined by regulatory enforcement rather than production growth, driven by the EU Battery Regulation. From mid-2025, the mandate requiring minimum 80% lead recovery from waste batteries has fundamentally altered sourcing strategies across the region. OEMs and recyclers are now required to implement digital Battery Passports, enabling full traceability of recycled lead content and lifecycle emissions.

Supply dynamics tightened during 2025 due to planned maintenance outages at major smelters in Germany and Poland, coinciding with the rollout of “Green Lead” certification frameworks. These certified materials—produced with low-carbon smelting and high recycled content—are commanding premiums over standard LME grades. While initiatives such as the Prysmian–Versalis partnership focus on broader cable and materials recycling, they reflect a systemic shift toward circular raw material flows, reinforcing recycled lead as a compliance-driven necessity rather than a cost-driven option.

Mexico – High-Grade Lead Recovery and USMCA Integration

Mexico has strengthened its role in the North American lead supply chain in 2025 through operational recovery and improved ore grades. Following the resolution of prior labor disputes, Newmont’s Peñasquito mine delivered higher lead and zinc grades, reaffirming its status as a cornerstone supplier for automotive and industrial customers under USMCA trade rules. The mine’s scale and polymetallic output provide critical feedstock stability for U.S.-based battery and manufacturing industries.

Looking ahead, the La Colorada Skarn project, advanced by Pan American Silver, represents one of the world’s largest undeveloped silver-lead-zinc resources. Ongoing feasibility work in 2025 points to long-term supply security for the region, positioning Mexico as a strategic bridge between primary mining and North American downstream consumption, particularly in automotive and backup power applications.

2025 Strategic Matrix: Lead Market National Comparison

Lead Market Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Technology / Policy Focus

|

|

United States

|

Infrastructure reshoring

|

USD 7.4B Korea Zinc smelter project

|

Critical minerals & secondary lead

|

|

Australia

|

Autonomous mining

|

Abra Mine reaches full capacity

|

5G-enabled remote operations

|

|

China

|

Regulatory ESG tightening

|

Net refined lead imports during inspections

|

Recycled lead mandates

|

|

India

|

Solar & grid storage

|

Mundra recycling expansion (BWMR)

|

Secondary lead & logistics reform

|

|

European Union

|

Circular economy

|

Mandatory 80% lead recovery

|

Battery Passports & Green Lead

|

|

Mexico

|

North American auto supply

|

Peñasquito grade recovery

|

USMCA-integrated mining

|

Lead Market Report Scope

Lead Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$41.3 Billion

|

|

Market Size (2035)

|

$74 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Type (Refined Lead, Recycled Lead, Antimonial Lead, Lead Alloys), By Product Form (Lead Ingots, Lead Sheets & Plates, Lead Pipes & Extruded Products, Lead Powder & Pellets), By Application (Batteries, Lead-Based Pigments & Compounds, Ammunition, Radiation Shielding, Construction, Solder & Cable Sheathing), By End-User Industry (Automotive, Power & Energy, Healthcare, Chemicals, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Glencore plc, Korea Zinc Co. Ltd., The Doe Run Company, Henan Yuguang Gold and Lead Co. Ltd., EcoBat Technologies, Nyrstar (Trafigura Group), Boliden Group, Gravita India Limited, Teck Resources Limited, Aqua Metals Inc., South32 Limited, Nippon Mining & Metals (JX), Recyclex S.A., Mittal Pigments, Clarios

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lead Market Segmentation

By Type

- Refined Lead

- Recycled Lead

- Antimonial Lead

- Lead Alloys

By Product Form

- Lead Ingots

- Lead Sheets & Plates

- Lead Pipes & Extruded Products

- Lead Powder & Pellets

By Application

- Batteries

- Lead-Based Pigments & Compounds

- Ammunition

- Radiation Shielding

- Construction (Roofing, Flashings, Soundproofing)

- Solder & Cable Sheathing

By End-User Industry

- Automotive

- Power & Energy

- Healthcare

- Chemicals

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Lead Market

- Glencore plc

- Korea Zinc Co., Ltd.

- The Doe Run Company

- Henan Yuguang Gold and Lead Co., Ltd.

- EcoBat Technologies

- Nyrstar (Trafigura Group)

- Boliden Group

- Gravita India Limited

- Teck Resources Limited

- Aqua Metals, Inc.

- South32 Limited

- Nippon Mining & Metals (JX)

- Recyclex S.A.

- Mittal Pigments

- Clarios

*- List not Exhaustive