Advanced Lead-Acid Battery Market Overview: Performance Reliability, Circularity Economics & Strategic Procurement Insights

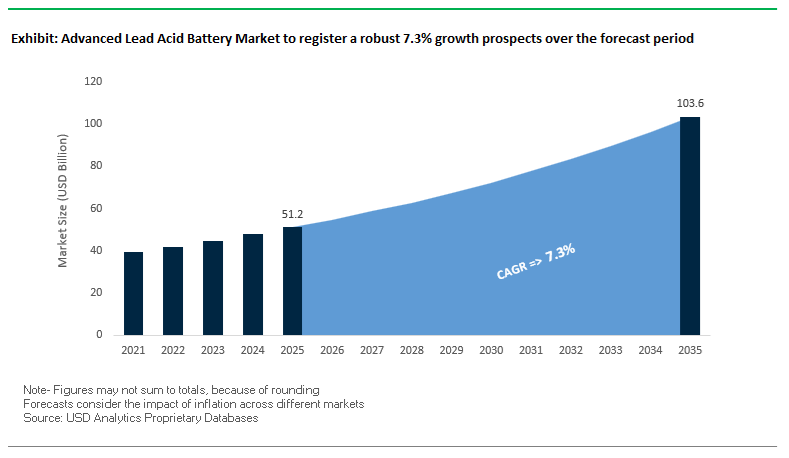

The Advanced Lead-Acid Battery Market, valued at USD 51.2 billion in 2025 and projected to reach USD 103.6 billion by 2035 at a healthy 7.3% CAGR, remains a foundational energy-storage segment supported by unmatched recycling rates, robust manufacturing maturity, and continuous improvements in energy efficiency and cycling durability. Across automotive, telecom, industrial backup, grid support, and cost-sensitive storage systems, advanced chemistries—including AGM (Absorbed Glass Mat), EFB (Enhanced Flooded Batteries), and Lead-Carbon technologies—are strategically positioned to meet rising performance, reliability, and sustainability expectations.

For industry leaders and procurement teams, decision-making increasingly revolves around Total Cost of Ownership (TCO) versus alternatives like LFP, the strength of closed-loop recycling economics, and the ability of advanced lead-acid systems to meet demanding technical KPIs such as Dynamic Charge Acceptance (DCA), partial-state-of-charge (PSoC) resilience, deep-cycle life, and long-duration float stability. AGM and EFB batteries remain indispensable for automotive start-stop systems, engineered specifically for higher DCA and improved PSoC durability, while lead-carbon variants demonstrate >4,000 cycles at 70% DoD—a compelling lifecycle-cost advantage for stationary telecom, microgrid, and industrial backup applications.

Supply chain reliability is a key differentiator, reinforced by >95% recycling rates in mature markets, delivering superior material security, ESG compliance, and stable raw-material availability compared to emerging chemistries. As OEMs and utilities modernize storage infrastructures, strategic buyers must balance performance metrics (DCA, cycle life, charge recovery, float longevity) with supplier capabilities in automation maturity, low-antimony grid technology, carbon-enhanced negative plates, and Industry 4.0 quality systems.

Key insights for Business Development Managers

- Recycling leadership: Advanced lead-acid batteries remain the world’s most recycled consumer product, with recovery rates consistently >95% in mature markets - a major ESG and supply-security advantage.

- Dynamic Charge Acceptance (DCA): New AGM designs deliver up to 5× higher DCA versus conventional flooded cells, enabling reliable start-stop and micro-hybrid automotive functions.

- Stationary storage competitiveness: Lead-Carbon variants report >4,000 cycles at 70% DoD in lab conditions - a metric that narrows TCO gaps with some LFP offerings for long-duration stationary use.

- Long standby life for critical systems: VRLA technologies are expected to provide 10–15 years of floating-charge standby life in telecom and UPS deployments.

- Manufacturing quality uplift: Automation and AI/vision adoption target up to 80% defect reduction in plate formation and assembly, improving AGM/EFB consistency and yield.

Market Analysis: Capacity Expansions, Regulatory Recycling Mandates & Product Breakthroughs

The Advanced Lead-Acid Battery industry entered a phase of both capacity investment and regulatory tightening that materially affects near-term supply dynamics and long-term product economics. In November 2025, Clarios announced a major manufacturing expansion - allocating roughly US$1 billion to next-generation technologies and raising component capacity by 30 million parts at its U.S. Oconee facility - strengthening the global supply of low-antimony AGM units required by modern vehicles. This capex wave is driven by persistent automotive demand for high-DCA, start-stop capable batteries and by OEMs’ preference for suppliers who can guarantee scale, quality and local content.

Regulatory and recycling policy also accelerated adoption and circularity metrics. In July 2025, the European Union implemented new rules to calculate and verify battery recycling efficiency, mandating 75% recycling efficiency for lead-acid batteries by December 2025 (rising to 80% by 2030). These rules reinforce the industry’s circular advantage but also raise compliance costs for recyclers and producers who must demonstrate documented recovery rates. Parallel capacity growth and policy signals can be seen geographically: February 2025 marked the commissioning of Luminous Power Technologies’ 2 GWh lead-acid plant in Haridwar, India - a strategic expansion to serve industrial and backup markets in growing regional demand centers.

Product and technology rollouts during 2024–2025 also re-shaped market options. A December 2024 gel lead-acid energy storage product targeted residential solar integration with improved deep-cycle safety; in November 2024 a Pure Lead Max (PLM) VRLA was launched in North America for high-reliability data-center UPS applications (backed by an eight-year warranty). Earlier moves such as September 2024 Exide’s SLI-AGM launch and October 2024 Amara Raja’s export push signal supplier efforts to diversify portfolios and geographies. Finally, India’s Battery Waste Management rules (amendments from 2022) that take effect in 2026–2027 (setting a 90% lead recovery target) underline how national regulation is strengthening the global recycling and supply ecosystem for lead-acid technologies.

Key Trends Redefining the Advanced Lead Acid Battery Market

Trend 1: Regulatory-Driven Standardization of AGM and EFB Batteries for Start-Stop and Micro-Hybrid Vehicle Platforms

Fuel economy laws such as CAFE regulations in the United States and Euro emission norms in Europe have fundamentally reshaped the demand landscape for automotive lead-acid batteries. Start-stop vehicles now impose highly dynamic power loads—requiring batteries to sustain frequent cycling, rapid charge acceptance, and ongoing partial-state-of-charge (PSoC) operation. This shift is accelerating the replacement of traditional SLI batteries with AGM (Absorbent Glass Mat) and EFB (Enhanced Flooded Battery) technologies that meet OEM warranty life and HRPSoC performance requirements.

In Europe, start-stop penetration reached approximately 78% of new vehicles by 2025, creating a guaranteed, high-volume demand base for advanced lead-acid batteries engineered for repetitive engine-off cycles. Within this market, AGM batteries have emerged as the dominant technology, accounting for around 82.7% of the European start-stop segment in 2024, underscoring the material and design advantages of AGM chemistry—particularly in urban driving conditions where constant cycling stresses conventional batteries. AGM and EFB solutions deliver up to three times the cycle life and twice the charge acceptance of traditional SLI batteries, which is essential to prevent premature failure under start-stop duty cycles.

As automakers increase adoption of mild hybrids and micro-hybrid systems that rely on HRPSoC operation, standardized performance thresholds are accelerating across global markets. This regulatory push is cementing AGM and EFB batteries as baseline technologies rather than premium options, reshaping the competitive dynamics within the advanced lead acid battery market.

Trend 2: Increasing Deployment in Grid Stabilization and Renewable Integration Through High-Recycling, Non-Flammable Storage Systems

A second major trend is the renewed strategic relevance of advanced lead acid batteries in grid reliability, data center backup, telecom infrastructure, and short-duration renewable smoothing applications. Lead-acid battery chemistries—particularly VRLA and AGM—offer a combination of non-flammability, low cost, and nearly closed-loop recyclability unmatched by other battery technologies. The recycling efficiency rate in the European Union consistently exceeds 80–90%, with all countries surpassing the mandated 65% minimum target in 2023. In the United States, recovery rates approach 99%, demonstrating a mature and high-integrity circular infrastructure.

Thin Plate Pure Lead (TPPL) technology is further strengthening the role of advanced lead-acid systems in mission-critical power. TPPL batteries provide 8–10 years of service life, approximately 25% longer than standard VRLA systems, making them particularly suited for data centers that require predictable long-term backup. Their non-flammable nature, unlike lithium-ion systems which carry inherent thermal runaway risk, positions advanced lead-acid batteries as the preferred chemistry for nuclear plants, hospitals, emergency systems, and telecom environments with stringent safety requirements.

As renewable energy penetration increases and utilities seek reliable short-duration storage buffers, the combination of circularity, cost efficiency, and inherent safety ensures that lead-acid batteries continue to retain a durable strategic role in global energy storage ecosystems.

High-Value Opportunities Emerging in the Advanced Lead Acid Battery Market

Opportunity 1: Carbon-Enhanced Lead Acid Systems for Extended Cycle Life and High PSoC Energy Storage

The integration of advanced carbon materials into the negative active mass (NAM) is creating one of the most attractive performance-enhancing opportunities in the advanced lead acid battery market. Lead-carbon batteries, incorporating engineered carbon black, carbon fibers, graphite, or nanotubes, substantially improve cycle life and charge acceptance in high-cycling and PSoC applications.

Testing shows that batteries incorporating optimal carbon fiber compositions can deliver 3,642 cycles, representing a 2.87× improvement compared to baseline lead-acid batteries. This cycle-life expansion is essential for applications such as renewable energy storage (RES), micro-hybrids, industrial backup, and HRPSoC automotive systems. Carbon additives suppress sulfation—a key failure mode in partially charged batteries—by forming conductive networks that prevent the growth of large, resistive lead sulfate crystals. The result is improved energy efficiency, longer operational life, and significantly higher reliability under demanding cycling conditions.

As utilities, telecom systems, and automotive OEMs seek lower-cost alternatives to lithium-ion for cycling-intensive applications, carbon-enhanced lead acid batteries present a compelling pathway to modernize legacy chemistries without sacrificing recyclability or safety.

Opportunity 2: Expansion in De-Risked, Shallow-Cycle Applications Where Safety, Cost, and Recycling Outperform Lithium-Ion

Despite the dominance of lithium-ion in high-energy-density markets, there is a growing movement toward lead-acid technology in sectors where safety compliance, low total cost of ownership, and recyclability guarantees are primary decision criteria. Many mission-critical environments prohibit lithium-ion systems due to thermal runaway risks, making VRLA and AGM batteries the only acceptable solution.

Advanced lead acid batteries offer a non-flammable chemistry profile, making them indispensable for nuclear energy facilities, regulated telecom nodes, medical centers, fire-sensitive industrial environments, and emergency infrastructure. They also provide significant economic advantages: for applications requiring short-duration discharge (<4 hours)—such as UPS ride-through support, backup switching, and auxiliary grid stabilization—the initial system cost of lead acid remains substantially lower than comparable lithium-ion solutions.

As global safety standards tighten and ESG compliance becomes a procurement priority, advanced lead acid batteries are positioned to expand in strategically de-risked market segments where predictability, recyclability, and regulatory compatibility outweigh the higher energy density of lithium-based systems.

Advanced Lead Acid Battery Market Share Analysis

Market Share by Technology Type: AGM Batteries Lead with 49.2% Share

Absorbent Glass Mat (AGM) batteries dominate the Advanced Lead Acid Battery Market with a 49.2% share in 2025, reflecting their position as the next-generation standard for automotive, transportation, and premium stationary storage systems. Their leadership stems from superior cyclic performance, vibration resistance, maintenance-free operation, and enhanced power delivery, making AGM technology the preferred solution for modern start-stop vehicles, micro-hybrids, and backup power systems. The segment’s strong penetration is directly tied to tightening automotive efficiency regulations, rapid adoption of start-stop systems across global OEM platforms, and the need for robust auxiliary power handling in increasingly electronics-heavy vehicles. Meanwhile, the broader technology landscape reinforces a stratified market structure: Enhanced Flooded Batteries (EFB) remain critical for mid-tier automotive applications; advanced flooded industrial batteries continue to anchor motive power and heavy-duty backup systems; Gel VRLA and Lead-Carbon (Pb-C) technologies push the boundaries of cycle life and partial-state-of-charge performance required for renewable-energy storage; and supercapacitor hybrids, while technologically promising, remain commercially niche due to cost barriers. This segmentation highlights AGM’s central role as the market’s high-volume, high-value workhorse while emerging chemistries drive specialized innovation in grid and industrial applications.

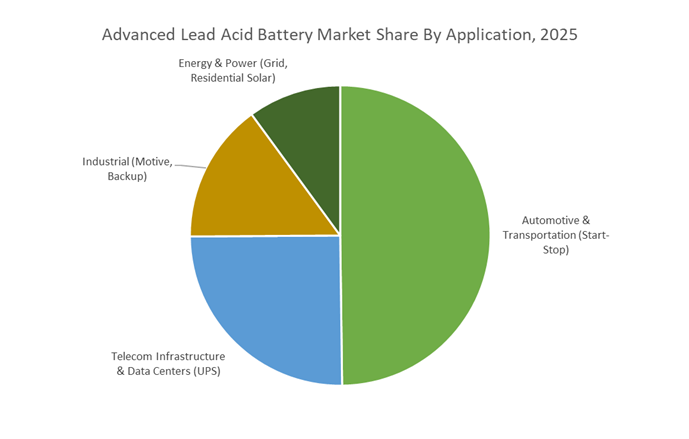

Market Share by Application: Automotive & Transportation Lead with 49.6% Share

Automotive & Transportation, particularly the start-stop vehicle segment, leads the Advanced Lead Acid Battery Market with a 49.6% share in 2025, serving as the industry’s revenue anchor despite long-term electrification pressures. Start-stop systems require high-power, durable, and cost-efficient batteries capable of frequent cycling, rapid recharge acceptance, and stable performance under partial state-of-charge—attributes that advanced lead-acid chemistries such as AGM and EFB deliver exceptionally well. This strong market share reflects the global OEM push toward fuel-efficiency compliance, CO₂ reduction mandates, and hybridization of internal combustion platforms, which collectively ensure sustained medium-term demand for lead-acid technologies. Beyond automotive, other end-use segments reinforce the technology’s strategic positioning: telecom infrastructure and data centers rely on VRLA solutions as a proven, safe, and cost-stable alternative to lithium-ion for UPS systems; industrial motive power and backup applications maintain steady consumption due to durability and predictable lifecycle economics; and energy & power storage, including residential solar and off-grid systems, represent the most innovation-active domain where Lead-Carbon batteries attempt to carve a value-tier niche below lithium-ion. Collectively, these dynamics show a market maximizing returns from a massive automotive installed base while defending industrial strongholds and selectively expanding into cost-sensitive stationary storage applications.

Country Analysis: Global Advanced Lead Acid Battery Market Innovation Hubs

India: Scaling Renewable Energy Storage and Domestic Lead-Acid Battery Manufacturing Under Aatmanirbhar Bharat

India has become one of the fastest-growing hubs for advanced lead-acid battery adoption as the country intensifies its renewable energy transition, rural telecom expansion, and domestic manufacturing ecosystem. The government’s move to introduce ₹5,400 crore ($650 million) in Viability Gap Funding (VGF) for building 30 GWh of battery storage systems significantly strengthens national demand for cost-efficient energy storage. This benefits advanced lead-acid chemistries—particularly VRLA, AGM, and lead-carbon batteries—which play a vital role in utility-scale and distributed BESS configurations due to their affordability and fast deployment capability.

India’s manufacturing capacity is also expanding rapidly. The inauguration of a new BESS manufacturing facility in Bengaluru in June 2025 marks a major milestone in strengthening the indigenous energy storage supply chain under Aatmanirbhar Bharat. Parallel industry growth drivers include the country’s massive telecom expansion into rural markets, which requires reliable backup power batteries for telecom towers, sustaining strong VRLA and AGM demand. Additionally, India’s automotive sector continues accelerating micro-hybrid and start-stop vehicle adoption, leading to increased use of Enhanced Flooded Batteries (EFB) and AGM batteries in conventional and mild-hybrid vehicles to meet stringent fuel efficiency and emissions norms. Together, these developments position India as a central market for renewable-aligned, cost-effective, and mass-manufacturable advanced lead-acid battery technologies.

United States: Strengthening Grid Reliability and Circular Battery Materials Through High-Value Lead-Acid Recycling

The United States remains a critical innovation hub for advanced lead-acid energy storage, driven by grid modernization initiatives and the country’s globally leading recycling infrastructure. With a recycling rate exceeding 98%, lead-acid batteries are the most recycled consumer product in the United States—an advantage aligned with federal circular economy goals and sustainable materials policies. This closed-loop ecosystem provides a secure supply of refined lead and battery components, reinforcing U.S. energy independence and manufacturing resilience.

Advanced lead-acid batteries continue to play a central role in utility-scale stationary storage, particularly for short-duration applications such as peak shaving, spinning reserve, and grid frequency regulation. Utility operators and OEMs are increasingly deploying advanced VRLA technologies for their quick response time, low upfront cost, and proven operational stability. Lead-acid chemistries also dominate backup power in data centers, hospitals, telecom networks, military installations, and Department of Defense sites, where reliability and robust performance remain paramount. The U.S. research ecosystem further strengthens competitiveness through extensive R&D in lead-carbon hybrid technologies, improving dynamic charge acceptance (DCA), cycle life, and performance under partial state-of-charge conditions—all critical for renewable energy integration and deep-cycling applications.

China: Global Leader in VRLA Manufacturing and E-Mobility Adoption for Two- and Three-Wheelers

China is the largest global producer and consumer of lead-acid batteries, driven by unparalleled demand from electric two-wheelers, three-wheelers, and industrial logistics fleets. The country’s massive e-bike and e-rickshaw market creates continuous, high-volume consumption of motive lead-acid batteries, pushing manufacturers to further reduce cost per cycle while enhancing durability for daily deep-discharge operations. This scale advantage helps China maintain its global dominance in VRLA, gel VRLA, and flooded lead-acid battery production.

China’s expanding industrial and warehousing sectors are intensifying demand for electric forklifts and material-handling equipment, where motive lead-acid batteries remain the preferred choice due to their long-standing reliability and economic advantage over lithium alternatives. At the same time, Chinese automotive OEMs are increasing integration of AGM batteries into mild-hybrid and conventional vehicles to comply with stronger emissions regulations. This shift enhances start-stop efficiency and supports auxiliary loads in modern vehicles. With massive installed production capacity and strong local demand, China remains the world’s largest market for industrial, motive, and e-mobility-based lead-acid batteries.

Germany (Europe): Premium Automotive AGM Systems and Circular Economy-Driven Battery Regulation

Germany and the broader European Union serve as advanced innovation centers for premium AGM and EFB lead-acid batteries, driven by the region’s luxury automotive manufacturers and strict environmental regulations. German OEMs require high-performance AGM batteries capable of supporting advanced start-stop systems, regenerative braking, and extensive onboard electronics, making AGM technology indispensable in Europe’s premium vehicle platforms.

The EU’s strong circular economy policies reinforce the relevance of lead-acid technology. With mandated collection and recycling targets exceeding 75%, lead-acid batteries are far easier to recycle and reuse compared to many lithium-ion chemistries. This regulatory alignment strengthens the market for industrial, automotive, and telecom-grade lead-acid solutions. Furthermore, European innovators are integrating advanced Battery Management Systems (BMS) and sensor-driven predictive maintenance tools to extend operational life in industrial fleets, telecom networks, and renewable energy installations. Germany’s combination of automotive excellence, sustainability frameworks, and industrial engineering precision positions Europe as a critical region for high-performance, regulation-aligned advanced lead-acid battery technologies.

Japan: Prioritizing Safety, Grid Stability, and High-Reliability VRLA Technologies for Critical Infrastructure

Japan maintains a strong leadership position in high-reliability VRLA and advanced lead-acid batteries, driven by its emphasis on safety, disaster resilience, and stable grid operations. Japanese utilities, telecom operators, and transportation networks rely heavily on VRLA UPS systems to support critical infrastructures such as nuclear power facilities, metro rail systems, data centers, and emergency operations centers. The country’s unique seismic risks necessitate robust, vibration-resistant, and thermally stable battery solutions designed for extreme reliability during adverse conditions.

Japan also invests heavily in advanced materials research to enhance lead-acid performance. Academic institutions and industry developers are exploring electrolyte additives such as manganese sulfate to improve electrode reversibility, reduce sulfation, and extend cycle life—particularly for long-duration and high-temperature applications. These innovations ensure lead-acid batteries remain a cornerstone of Japan’s grid stabilization, emergency backup, and mission-critical industrial systems.

Competitive Landscape: Supplier Capabilities, Strategic Investments & Differentiation in Advanced Lead-Acid

The Advanced Lead-Acid competitive field is shaped by vertically integrated manufacturers, aftermarket service leaders, and regionally dominant producers. Differentiation stems from manufacturing scale (smelting to cell assembly), proprietary low-antimony and pure-lead grid technologies, TPPL/Thin Plate Pure Lead capabilities, aftermarket and service networks, and investments in Industry 4.0 to reduce defects and accelerate throughput. The paragraphs below profile leading firms and their strategic value propositions.

Clarios - scaling low-antimony AGM production with a US$1 billion investment

Clarios is the global leader in automotive SLI batteries, specializing in AGM and EFB platforms. Its November 2025 commitment of approximately US$1 billion to U.S. manufacturing (Oconee) - increasing component capacity by 30 million parts - aims to secure supply for low-antimony batteries demanded by modern vehicle electrical architectures. Clarios’ scale, combined with focused investments in automation and quality analytics, positions it as the primary supplier for OEMs prioritizing high DCA performance, local capacity, and robust recycling partnerships.

EnerSys - industrial energy storage leader with aftermarket service expansion

EnerSys is a dominant supplier of industrial and stationary power batteries (Hawker®, Odyssey®) with strong traction in motive power and telecom UPS markets. The company is expanding its geographic aftermarket footprint through acquisitions (e.g., service firms in the U.K.), strengthening lifecycle service and swap-out capabilities. EnerSys’ competency in TPPL technology and high-rate discharge solutions makes it a preferred vendor for data centers and critical infrastructure where rapid discharge, deep-cycle tolerance and long standby life are required.

Exide Industries Ltd. - South Asian scale player diversifying into advanced chemistries

Exide is a leading manufacturer across automotive, industrial and solar backup segments in South Asia. Product innovations such as the SLI-AGM introduction (September 2024) respond to intensive electronic loads and start-stop vehicle configurations. Exide’s announced investments in advanced chemistry cell manufacturing (Exide Energy Solutions Ltd.) and export expansion signal a strategic pivot to broaden regional influence and compete on both price and advanced lead-acid performance.

GS Yuasa Corporation - precision manufacturing for high-reliability and hybrid applications

GS Yuasa brings Japanese manufacturing precision to VRLA and specialized industrial batteries, including ruggedized solutions for submarine, aerospace and grid support applications. The company is prioritizing integration of advanced lead-acid technologies into renewable energy hybrid systems and grid resilience projects, leveraging decades of safety and performance experience to capture high-reliability niches where certification and lifecycle assessments are critical.

East Penn Manufacturing - vertically integrated domestic producer emphasizing pure-lead advances

East Penn (Deka®) is notable for full vertical integration - from lead smelting to finished battery - ensuring exceptional quality control and supply-chain resilience. Its investments in pure lead and low-resistance grid technologies aim to extend cycle life and reduce corrosion, enhancing battery life for stationary and motive applications. East Penn’s domestic footprint and vertical control make it a preferred partner for buyers valuing traceability, localized supply and rapid response.

Amara Raja Energy & Mobility Ltd. - Indian OEM partner expanding exports and technology scope

Amara Raja is a significant Indian manufacturer with strong OEM partnerships (e.g., Hyundai, Maruti Suzuki) and a growing export orientation. Its strategic push to increase overseas shipments and investments in new energy technologies reflects a dual strategy: defend domestic market share while scaling internationally. Amara Raja’s position in the Indian ecosystem - combined with its product portfolio across VRLA and EFB segments - makes it an important supplier for regional automotive and industrial backup demand.

Advanced Lead Acid Battery Market Report Scope

Advanced Lead Acid Battery Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$51.2 Billion

|

|

Market Size (2035)

|

$103.6 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Technology Type (AGM Batteries, Enhanced Flooded Batteries, Gel VRLA Batteries, Lead-Carbon Batteries, Supercapacitor Hybrid Lead-Acid Batteries, Flooded Lead-Acid), By Product Type (Motive Power, Reserve Power/Stationary, Starting Lighting & Ignition), By Application (Automotive & Transportation, Energy & Power, Telecom Infrastructure, Data Centers, Industrial), By Construction Method (Valve Regulated Lead Acid, Vented/Flooded)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Clarios International Inc., EnerSys, GS Yuasa Corporation, Exide Industries Ltd., East Penn Manufacturing Co., Amara Raja Batteries Ltd., Leoch International Technology Ltd., The Furukawa Battery Co. Ltd., Narada Power Source Co. Ltd., Crown Battery Manufacturing Company, HOPPECKE Batterien GmbH & Co. KG, Trojan Battery Company, Coslight Technology International Group Co. Ltd., NorthStar Battery Company, HBL Power Systems Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Lead Acid Battery Market Segmentation

By Technology Type

- Absorbent Glass Mat (AGM) Batteries

- Enhanced Flooded Batteries (EFB)

- Gel VRLA Batteries

- Lead-Carbon (Pb-C) Batteries

- Supercapacitor Hybrid Lead-Acid Batteries

- Flooded Lead-Acid

By Product Type

- Motive Power

- Reserve Power / Stationary

- Starting, Lighting & Ignition

By Application

- Automotive & Transportation

- Energy & Power

- Telecom Infrastructure

- Data Centers

- Industrial

By Construction Method

- Valve Regulated Lead Acid

- Vented / Flooded

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Advanced Lead Acid Battery Market

- Clarios International Inc.

- EnerSys

- GS Yuasa Corporation

- Exide Industries Ltd.

- East Penn Manufacturing Co.

- Amara Raja Batteries Ltd.

- Leoch International Technology Ltd.

- The Furukawa Battery Co., Ltd.

- Narada Power Source Co., Ltd.

- Crown Battery Manufacturing Company

- HOPPECKE Batterien GmbH & Co. KG

- Trojan Battery Company

- Coslight Technology International Group Co., Ltd.

- NorthStar Battery Company

- HBL Power Systems Ltd.

*- List not Exhaustive