Leather Chemicals Market Growth Trajectory 2025–2034: Sustainable Tanning, Performance Coatings, and Automotive Leather Driving $34.1 Billion Outlook at 7.3% CAGR

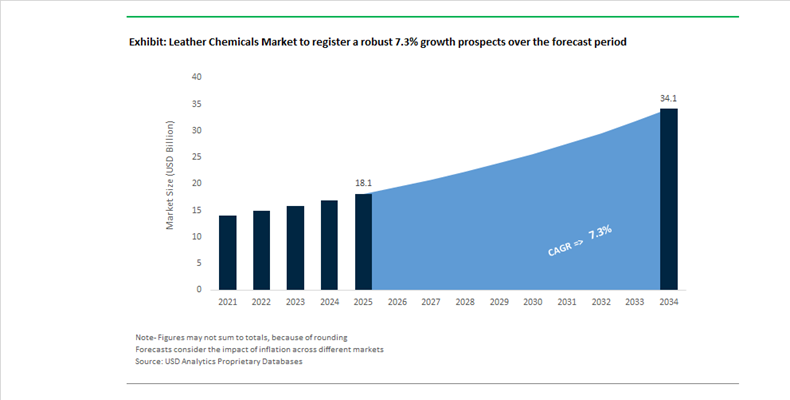

The Leather Chemicals Market is projected to expand from $18.1 billion in 2025 to $34.1 billion by 2034, registering a robust CAGR of 7.3%. Growth is being propelled by accelerating demand for sustainable tanning chemicals, water-based polyurethane dispersions, bio-based fatliquors, chrome-free systems, and high-performance leather finishing coatings across automotive interiors, luxury fashion, footwear, and technical leather goods. Increasing regulatory scrutiny around hazardous substances, wastewater discharge, and VOC emissions is reshaping procurement strategies within tanneries, pushing the adoption of eco-certified wet-end chemicals, retanning agents, syntans, preservatives, and finishing formulations.

In early 2024, industry collaboration led to the commercial scaling of the AVICUERO System, a water-efficient tanning platform often paired with bio-based fatliquors from Trumpler, significantly reducing salt usage and tannery effluent loads. In 2024, TFL Ledertechnik introduced its PURE TEC range, a portfolio of high bio-based beamhouse and wet-end chemicals engineered to lower carbon intensity while maintaining mechanical strength and heat resistance required for automotive upholstery leather. In December 2024, Codyeco achieved ZDHC Level 3 Certification for over 800 leather chemical products, reinforcing market migration toward verified hazardous substance-free formulations. These developments mark a structural shift toward low-impact leather processing chemicals aligned with global sustainability compliance frameworks.

Strategic expansion in chrome-free and automotive-compliant tanning systems intensified in 2025 and 2026. In 2025, Royal Smit & Zoon advanced Zeology tanning into the automotive sector, demonstrating heat and light-fastness performance suitable for premium vehicle interiors while ensuring improved biodegradability of leather waste. In late 2025, BASF accelerated restructuring to prioritize green transformation in leather chemicals, expanding its Valure and Astacin finishing lines based on water-based polyurethane dispersions to reduce VOC emissions. In August 2025, TFL implemented leadership changes to advance its sustainability-focused “TFL Effect” strategy and launched an Autumn-Winter 2026/27 trend collection emphasizing low-Bisphenol syntans compliant with ZDHC standards.

Consolidation and portfolio realignment are redefining competitive dynamics. In February 2026, Henkel signed a definitive agreement to acquire Stahl Group for €2.1 billion, integrating market-leading leather finishing and performance coatings into Henkel’s Adhesive Technologies platform, strengthening its position in automotive and luxury fashion coatings. On January 5, 2026, Muno launched as an independent wet-end specialist following the divestment of Stahl’s wet-end division, focusing exclusively on sustainable tanning and retanning innovation with R&D hubs in Italy and India. In February 2026, Lanxess introduced Preventol CT 40 at the India International Leather Fair, a next-generation preservative combining electrophilic and membrane-active protection for wet-blue and wet-white leather storage stability. This sequence of acquisitions, spin-offs, and product launches highlights intensifying specialization in wet-end chemistry, preservative systems, and high-performance finishing technologies within the global leather chemicals value chain.

Strategic Trends and High-Growth Opportunities Shaping the Leather Chemicals Market

Trend: Rapid Transition to Chrome-Free and Advanced Tanning Chemistries

The leather chemicals market is undergoing a fundamental shift as regulatory pressure and brand-led sustainability commitments accelerate the move away from conventional chrome-tanning systems. Anticipated revisions to EU REACH in 2026, combined with the expanding enforcement of ZDHC MRSL protocols, are forcing tanneries to adopt mineral-free and bio-polymeric tanning agents that deliver environmental compliance without compromising performance. Luxury footwear, automotive upholstery, and children’s products are leading this transition, as buyers in these segments require both regulatory safety and premium material properties.

Chemical innovation has reached a critical inflection point. LANXESS has scaled its Levotan X-Biomer technology, which uses biodegradable polymers derived from renewable raw materials. Industrial deployments demonstrate around a 30% reduction in Chemical Oxygen Demand in tannery effluents compared to traditional synthetic retanning agents, while preserving wet-white leather quality. Regulatory momentum is reinforcing this shift. By November 2025, the European Commission advanced its Omnibus VI and REACH updates, signaling phased reductions in bisphenols and selected metal salts. This is pushing adoption of high-exhaustion leather chemicals that minimize unfixed residues in wastewater. Importantly, technical barriers are falling. Glutaraldehyde-free and mineral-free tanning systems introduced during 2024 and 2025 now achieve shrinkage temperatures above 85°C, meeting the stringent heat resistance thresholds required for automotive interiors and eliminating a historic disadvantage of chrome-free leather.

Trend: Vertical Integration and Chemicals-as-a-Service Models Redefine Value Creation

Leading suppliers in the leather chemicals market are increasingly differentiating through vertical integration and branded processing systems that combine proprietary formulations with digital dosing, application expertise, and wastewater management. This chemicals-as-a-service approach is designed to lock in long-term customer relationships while delivering measurable reductions in water, energy, and chemical consumption at the tannery level.

A benchmark example is the integrated hub model deployed by Stahl. In October 2025, Stahl reopened its advanced coatings and processing facility in Ranipet, India, featuring centralized R&D, application laboratories, and a zero liquid discharge wastewater system. This configuration enables rapid co-development of market-ready solutions tailored to local raw materials while meeting global OEM specifications. Resource efficiency gains are becoming a decisive purchasing criterion. The Stahlite processing system replaces traditional heavy fatliquors with lightweight polymeric softening agents, reducing hide weight by up to one third in luxury automotive interiors. For electric vehicles, this translates into measurable reductions in vehicle mass and approximately 0.5 g per kilometer lower CO2 emissions. At the same time, chemical-process integration has shortened retanning cycle times by as much as 40% since late 2024, lowering per-unit energy costs amid volatile utility pricing and strengthening the economic case for premium chemical systems.

Opportunity: Advanced Coating Technologies for Premium Automotive Vegan Interiors

The rapid expansion of electric vehicle production is creating a high-margin opportunity for leather chemical suppliers in synthetic and bio-based coating systems used for next-generation interiors. Automakers are increasingly replacing animal leather with polyurethane and hybrid bio-based materials to meet Scope 3 emissions targets while maintaining luxury aesthetics and durability.

BASF has commercially scaled its Haptex technology, a fully solvent-free synthetic leather solution. Lifecycle assessments published in 2025 indicate greenhouse gas emission reductions of approximately 52% and water savings of 30% compared to conventional synthetic leather processes. Performance innovation continues to accelerate. In October 2025, Stahl introduced the PermaQure EPU embossable polyurethane system, a 100% solids resin that enables post-embossing on flat substrates. This reduces production complexity while delivering abrasion resistance exceeding 100,000 cycles, aligning with automotive durability standards. Parallel R&D is focused on coatings for plant-based substrates such as mushroom, pineapple, and cactus fibers. These bio-synthetic hybrids are gaining traction in Asia-Pacific markets, which already account for more than 40% of global automotive vegan leather consumption, positioning advanced coatings as a key growth lever in the regional value chain.

Opportunity: Chemical Enablers of a Circular and Regulated Leather Economy

The emergence of circular economy frameworks is opening a structurally significant opportunity for leather chemical suppliers that can enable recycling, traceability, and compliance. The rollout of the EU Digital Product Passport and expanding Extended Producer Responsibility schemes in 2025 are forcing brands to document chemical content, recyclability, and environmental impact across the leather lifecycle.

Advanced chemical recycling is increasingly viewed as the most viable route to circularity. Unlike mechanical recycling, which degrades fiber integrity, chemical processes based on glycolysis and enzymatic depolymerization can remove dyes, finishes, and hazardous residues, allowing leather waste to re-enter production streams with near-virgin performance characteristics. Industry assessments published in November 2025 estimate the advanced recycling market could represent a 50 to 75 billion dollar opportunity by 2035, with leather chemicals playing a critical enabling role. Regulatory pull is intensifying outside Europe as well. California’s SB 707 textile recovery law mandates extended producer responsibility by 2030, compelling brands to partner with chemical suppliers capable of validating recycled feedstocks against REACH and ZDHC standards. As compliance, traceability, and circularity converge, specialized leather chemicals are set to become central to sustainable value creation across the global leather industry.

Leather Chemical Market Share and Segmentation Insights

Finishing Chemicals Lead Leather Chemical Consumption Through Performance, Appearance, and Surface Protection Functions

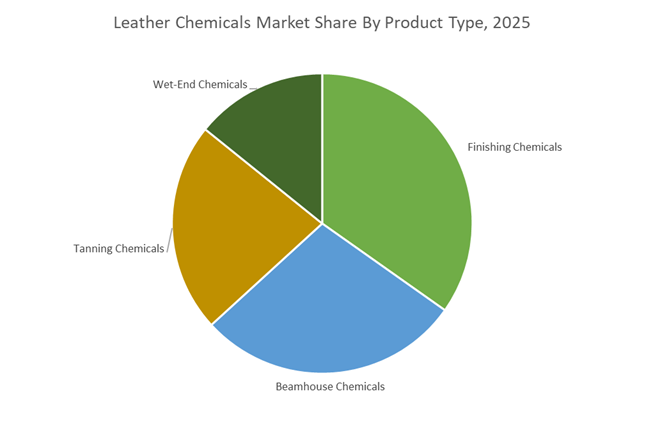

Finishing chemicals accounted for 34.80% of the Leather Chemicals Market share in 2025, making them the largest product category within the leather processing value chain. These chemicals include coatings, pigments, lacquers, waxes, binders, and protective topcoats that determine the final surface characteristics of leather products. Finishing formulations directly influence color uniformity, gloss level, softness, water resistance, abrasion resistance, and durability, which are critical attributes in footwear, upholstery, automotive interiors, and fashion leather goods. Because finishing chemicals are applied to nearly all processed leather products, they represent one of the highest-value segments of the leather chemicals industry. In 2025, the market has been significantly influenced by the shift toward environmentally compliant leather finishing technologies, particularly the growing adoption of water-based finishing systems. Environmental regulations limiting solvent emissions have accelerated the development of low-VOC coatings, advanced polymer binders, and water-dispersible pigment systems that deliver comparable performance to solvent-based finishes while supporting sustainability targets within global leather manufacturing supply chains.

Footwear Manufacturing Drives the Largest Demand for Leather Chemicals

Footwear represented 42.80% of the Leather Chemicals Market share in 2025, establishing it as the dominant application sector for leather processing chemicals. The global footwear industry produces billions of pairs of shoes annually, creating substantial demand for leather chemicals used throughout the tanning and finishing process. Footwear leather requires specialized chemical treatments to achieve durability, flexibility, abrasion resistance, color stability, and water repellency, properties necessary for both performance and aesthetic appeal in consumer footwear products. Leather used in footwear manufacturing typically undergoes multiple chemical processing stages including beamhouse treatments, tanning, wet-end processing, and finishing, each requiring specific chemical formulations. In 2025, sustainability commitments from major global footwear brands have significantly influenced leather chemical selection across supply chains. Manufacturers increasingly demand chrome-free tanning agents, bio-based auxiliaries, and ZDHC-compliant finishing chemicals, enabling footwear producers to meet environmental and regulatory standards while maintaining the material performance required for modern athletic, casual, and luxury footwear production.

Leather Chemicals Market Competitive Landscape

The leather chemicals market competitive landscape in 2026 is defined by portfolio specialization, bio-based tanning chemistries, and ZDHC-compliant innovations. Leading players are executing divestitures, acquisitions, and regional capacity expansions to align with low-VOC formulations, chrome-free processing, and high-performance leather finishing demands across automotive and luxury segments.

Stahl transitions into a pure-play leader in water-borne leather coatings

Stahl Holdings B.V. is consolidating its leadership in specialty leather coatings through a decisive portfolio restructuring and high-value acquisition pipeline. The 2026 carve-out of its wet-end leather chemicals unit (Muno) positions Stahl as a pure-play coatings specialist, while Henkel’s €2.1 billion acquisition integrates its high-performance leather finishing technologies into advanced adhesive platforms. Its dominance in water-based polyurethane dispersions and water-borne leather finishing systems ensures compliance with ZDHC standards and automotive OEM specifications. Strategic acquisitions such as Weilburger Graphics and ISG expand its capabilities into hybrid flexible substrates, reinforcing its premium positioning across luxury leather goods and performance materials.

LANXESS accelerates chrome-free tanning adoption with advanced biocide systems

LANXESS AG is strengthening its foothold in sustainable leather chemicals by advancing chrome-free and low-VOC tanning technologies tailored for Asia-Pacific manufacturing hubs. The launch of Preventol® CT 40 at IILF 2026 highlights its innovation in high-performance leather preservatives, offering dual-action antifungal protection and extended shelf life for Wet Blue and Wet White intermediates. Its glutaraldehyde-based tanning portfolio delivers zero wastewater impact while reducing environmental compliance risks under REACH regulations. With high-concentration biocides and integrated Sustainable Leather Management systems, LANXESS is optimizing dosage efficiency, logistics, and regulatory alignment for large-scale leather processing operations.

BASF restructures global operations to scale bio-based leather auxiliaries

BASF SE is reinforcing its position in high-volume leather auxiliaries through cost optimization and regional production realignment under its “Winning Ways” strategy. The expansion of the Zhanjiang Verbund site enhances supply chain integration for the Asia-Pacific leather chemicals market, while operational restructuring targeting €2.3 billion in annual savings improves margin recovery. Its Bionas® and Relugan® product lines are increasingly shifting toward bio-based raw materials, reducing beamhouse carbon emissions and supporting sustainable leather processing. The strategic focus on Industrial Solutions following portfolio divestitures ensures continued investment in leather tanning agents, retanning chemicals, and performance auxiliaries.

TFL strengthens ZDHC-compliant specialty leather chemicals with digital integration

TFL Ledertechnik GmbH is reinforcing its position as a pure-play leather chemicals specialist by aligning product innovation with stringent environmental compliance and design-driven demand. Achieving ZDHC MRSL V3.1 Level 3 certification across its portfolio ensures full compliance with global clean leather production standards. Under new leadership, TFL is integrating AI-enabled Safety Data Sheet systems to streamline formulation compliance and enhance tannery efficiency. Its recovery of global production capacity post-disruption and continued focus on footwear leather chemicals and upholstery applications position the company strongly for the 2026–2027 demand rebound.

Royal Smit & Zoon advances circular leather chemistry with zeolite-based tanning

Royal Smit & Zoon is setting industry benchmarks in circular leather chemicals through its proprietary Zeology platform, enabling fully chrome-free, aldehyde-free, and biodegradable tanning processes. This innovation supports compostable leather waste streams and aligns with rising demand for sustainable leather manufacturing. Its EcoVadis Platinum ESG rating and collaboration with the Leather Working Group reinforce its leadership in lifecycle assessment-driven production. By leveraging renewable feedstocks for fatliquors and syntans, the company is enabling measurable carbon reduction across the leather value chain while supporting next-generation tannery models.

Elementis expands high-margin additives portfolio for premium leather finishing

Elementis PLC is evolving into a high-margin specialty additives provider by exiting legacy chromium operations and expanding into bio-based rheology modifiers. The acquisition of Alchemy Ingredients strengthens its presence in natural-derived additives for water-borne leather coatings, while ongoing divestment of its pharmaceutical unit sharpens focus on coatings and personal care segments. With innovation-driven revenue reaching 16.4%, Elementis is capitalizing on its hectorite clay technology to deliver superior rheology control, enhanced leather “hand-feel,” and durability in advanced leather finishing systems, particularly in premium and automotive applications.

India Leather Chemicals Market: Policy-Led Sustainability and Export-Driven Chemical Upgrading

India’s leather chemicals market is undergoing a structural upgrade anchored in public funding, sustainability mandates, and export competitiveness. Under the Indian Footwear and Leather Development Programme, cumulative allocations of approximately USD 220 million through 2026 have shifted decisively toward environmental infrastructure. During the 2025–2026 cycle, the STEP sub-scheme is providing 70 to 80% capital subsidies for Common Effluent Treatment Plants, directly addressing chromium-heavy wastewater challenges that historically constrained chemical-intensive tanning clusters. Parallel support under the Integrated Development of Leather Sector scheme is accelerating MSME modernization, with 30% financial assistance enabling automated chemical dosing systems that are already reducing chemical wastage by up to 15% across organized tanneries.

Cluster-led growth and export momentum are reinforcing demand for higher-value leather chemicals. Newly designated mega hubs in Agra, Kanpur, and Chennai are prioritizing REACH-compliant finishing agents to align with European buyer requirements, while strategic collaborations such as the January 2024 partnership between Pidilite Industries and Syn-Bios are introducing polymer-based, heavy-metal-free tanning auxiliaries. A 25% surge in leather and footwear exports in FY 2024–25 has intensified the use of high-exhaustion dyes, specialty fatliquors, and consistency-enhancing retanning agents to meet the quality benchmarks of global brands. At the workforce level, projected demand for 135,000 skilled workers in the South Indian footwear belt through FY 2025–27 is driving specialized chemical application training via institutions such as CLRI and FDDI, further professionalizing chemical usage at the factory floor.

China Leather Chemicals Market: Regulatory Tightening and Digitalized Chemical Efficiency

China’s leather chemicals market is being reshaped by national green standards and technology-driven efficiency gains. The implementation of GB/T 44838-2024 from June 1, 2025 introduces stringent Green Product Evaluation criteria for leather apparel, mandating advanced chromium waste handling and low-carbon chemical attributes. This regulatory baseline is complemented by the MIIT 2025 work plan, which targets a 5% annual increase in chemical sector added value and explicitly supports bio-based auxiliaries and high-performance finishing resins, particularly for automotive upholstery and premium leather goods.

Capacity expansion and digital transformation are reinforcing this transition. Stahl confirmed the doubling of its China manufacturing capacity in 2025 to serve domestic luxury fashion and automotive interiors. Simultaneously, under the 14th Five-Year Plan, higher environmental taxes on high-VOC tanning processes are accelerating adoption of low-emission formulations. By late 2025, leading Chinese tanneries are integrating AI-driven chemical monitoring systems to optimize pH control and reaction efficiency, delivering up to a 10% reduction in chemical consumption per hide while improving batch consistency.

Netherlands Leather Chemicals Market: Portfolio Realignment and Bisphenol-Free Innovation

The Netherlands continues to play a strategic role as a technology and sustainability anchor for the global leather chemicals industry. In November 2025, Stahl completed the carve-out of its wet-end leather business into an independent entity, Muno, enabling sharper focus on high-growth specialty performance coatings. This structural realignment reflects a broader industry shift toward value-added finishing systems with lower regulatory risk and higher margins.

Product innovation and transparency are reinforcing competitive positioning. Royal Smit & Zoon launched BioTan XP 01L in 2025, a retanning agent with no detectable bisphenol, anticipating stricter 2026 EU consumer safety thresholds. At the same time, Dutch leaders including TFL and Smit & Zoon have transitioned to 100% renewable electricity across core European operations, reporting localized reductions of 4 to 6% in product carbon footprint. These developments are strengthening the Netherlands’ role as a reference market for sustainable leather chemical formulations.

Mexico Leather Chemicals Market: Automotive-Centric Application Development

Mexico’s leather chemicals market is increasingly aligned with automotive upholstery demand and nearshoring dynamics. In June 2025, Stahl inaugurated an enhanced Customer Center of Excellence in León, equipped with advanced application laboratories for leather finishing and performance testing. This facility is designed to support regional footwear manufacturers and Tier 1 automotive suppliers with rapid formulation customization.

Chemical demand is shifting toward performance attributes required by electric vehicle interiors. Local suppliers are prioritizing low-fogging and low-odor finishing agents to comply with updated global OEM specifications, reflecting the growing importance of cabin air quality and material compatibility in EV platforms. As a result, Mexico is emerging as a key testing and application hub for next-generation automotive leather chemicals serving both North American and Latin American markets.

Brazil Leather Chemicals Market: Volume Expansion Under Sustainability Certification

Brazil’s leather chemicals market is being driven by export volume growth combined with tightening sustainability criteria. Exports of hides and skins reached 49.8 million square meters in Q1 2025, an 8.2% year-on-year increase, intensifying demand for beamhouse chemicals, tanning agents, and post-tanning auxiliaries in major producing states such as Rio Grande do Sul and Paraná. This scale-driven demand is reinforcing the importance of reliable bulk chemical supply and process efficiency.

Sustainability certification is becoming a decisive market filter. The Centre for the Brazilian Tanning Industry is enforcing the Brazilian Leather Certification of Sustainability for 2026, requiring verified biodegradation profiles for chemicals used in certified tanneries. This is accelerating the shift toward biodegradable surfactants, low-impact degreasers, and compliant tanning systems, positioning Brazil as a volume-led yet sustainability-aligned sourcing base for global leather supply chains.

Leather Chemicals Market: Country-Level Strategic Snapshot

Leather Chemicals Market County Level Snapshot

|

Country

|

Primary Policy or Demand Driver

|

Key Chemical Focus Area

|

Market Implication

|

|

India

|

Public funding and export growth

|

REACH-compliant dyes, fatliquors, green tanning auxiliaries

|

Rapid modernization and volume-quality balance

|

|

China

|

Green standards and digitalization

|

Bio-based auxiliaries, low-VOC finishing resins

|

Efficiency gains and regulatory compliance

|

|

Netherlands

|

Portfolio realignment and EU regulation

|

Bisphenol-free retanning, renewable-powered production

|

Technology leadership and premium positioning

|

|

Mexico

|

Automotive and EV interiors

|

Low-fogging, low-odor finishing agents

|

Application-led growth tied to OEM demand

|

|

Brazil

|

Export volume and certification

|

Biodegradable beamhouse and tanning chemicals

|

Scale-driven demand with sustainability gating

|

Leather Chemicals Market Report Scope

Leather Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.1 Billion

|

|

Market Size (2034)

|

$34.1 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Product Type (Beamhouse Chemicals, Tanning Chemicals, Wet-End Chemicals, Finishing Chemicals), By Application (Footwear, Automotive Interiors, Furniture and Upholstery, Fashion and Garments, Leather Goods, Gloves and Protective Equipment), By Grade (Bio-Based and Sustainable Grade, Industrial Grade, High-Performance Grade)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Stahl Holdings, LANXESS, BASF, TFL Ledertechnik, Royal Smit and Zoon, Zschimmer and Schwarz, Pidilite Industries, Trumpler, Schill and Seilacher, DyStar Group, Pulcra Chemicals, Sudarshan Chemical Industries, Brother Enterprises Holding, Sisecam Chemicals, Indofil Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Leather Chemicals Market Segmentation

By Product Type

- Beamhouse Chemicals

- Tanning Chemicals

- Wet-End Chemicals

- Finishing Chemicals

By Application

- Footwear

- Automotive Interiors

- Furniture and Upholstery

- Fashion and Garments

- Leather Goods

- Gloves and Protective Equipment

By Grade

- Bio-Based and Sustainable Grade

- Industrial Grade

- High-Performance Grade

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Leather Chemicals Market

- Stahl Holdings

- LANXESS

- BASF

- TFL Ledertechnik

- Royal Smit and Zoon

- Zschimmer and Schwarz

- Pidilite Industries

- Trumpler

- Schill and Seilacher

- DyStar Group

- Pulcra Chemicals

- Sudarshan Chemical Industries

- Brother Enterprises Holding

- Sisecam Chemicals

- Indofil Industries

*- List not Exhaustive