Tanning Agents Market 2025–2034: $10.4 Billion to $15.7 Billion at 4.7% CAGR Driven by Chrome-Free Innovation, ZDHC Compliance, and Bio-Based Hybrids

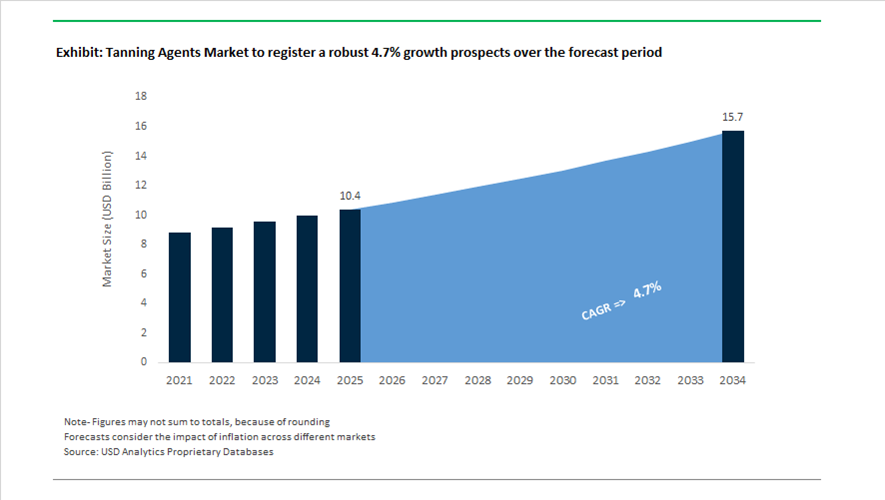

The global tanning agents market is valued at $10.4 billion in 2025 and is projected to reach $15.7 billion by 2034, expanding at a CAGR of 4.7%. Growth is increasingly defined by regulatory-driven reformulation, premium automotive and luxury leather demand, and rapid commercialization of chrome-free and hybrid tanning systems. The industry is undergoing structural transition from chromium-heavy chemistries toward zeolite-based, aldehyde-based, vegetable, and bio-synthetic alternatives aligned with ZDHC MRSL standards, EU chemical compliance frameworks, and brand-led decarbonization targets. Competitive positioning is now strongly tied to traceability, restricted substance compliance, and carbon-intensity reduction across leather processing stages.

Leadership realignment and strategic repositioning among major suppliers accelerated between 2024 and 2026. In June 2024, TFL Ledertechnik GmbH celebrated 100 years at its Huningue production site, a core European hub for advanced tanning and post-tanning chemistries serving automotive and luxury segments. In September 2024, Marc Schebben joined TFL’s Executive Board, strengthening operational oversight during a period of intensified R&D investment in eco-friendly tanning systems. In March 2025, TFL appointed André Lanning as Group CEO with a mandate to accelerate responsible innovation and sustainable portfolio expansion. In May 2025, TFL achieved ZDHC MRSL V3.1 Level 3 recertification—the highest compliance tier—ensuring independent validation of its restricted-substance controls. Meanwhile, in April 2025, LANXESS AG finalized the sale of its Urethane Systems business to UBE Corporation, completing its transformation into a specialty-focused chemical group with increased emphasis on high-margin leather intermediates and preservation chemistries.

Product innovation has centered on chrome-free, bisphenol-free, and hybrid mineral-organic systems. In July 2024, BASF SE launched Hapte 4.0, a recyclable polyurethane-based synthetic material incorporating tanning-like chemistry that reduces greenhouse gas emissions by 52% and water consumption by 30% compared to traditional leather processes. In November 2025, India’s CSIR-Central Leather Research Institute introduced bio-based polyphenol–aluminum hybrid tanning agents achieving nearly 98°C shrinkage temperature with 40% lower chemical input. In January 2026, TFL unveiled bisphenol-free tanning systems at the India International Leather Fair, directly addressing tightening endocrine disruptor regulations without compromising mechanical strength or hide fullness. In February 2026, Stahl Holdings BV received the adiFORMULATOR Award from Adidas for the second consecutive year, reinforcing leadership in ZDHC Level 3 compliance across tanning and finishing portfolios. Concurrently, Royal Smit & Zoon advanced its “Drops of Difference” 2030 strategy and expanded its Zeology zeolite-based chrome-free tanning range ahead of APLF 2026, signaling accelerating adoption of mineral-based white tanning systems with improved biodegradability.

Regulatory-Driven Transformation and High-Performance Opportunity Creation in the Tanning Agents Market

Regulatory Phase-Out of Chromium VI and Formaldehyde Accelerates Shift to Chromium-Free Automotive Tanning

The tanning agents market is undergoing a structural reset as automotive OEMs hardwire non-toxicity requirements into leather procurement specifications. Cabin air quality, lifecycle toxicity, and end-of-life recyclability have become board-level KPIs for European and premium Asian automakers, directly impacting tanning chemistry selection. Under evolving EU REACH Annex XVII restrictions, chromium VI and formaldehyde-based systems are no longer viewed as manageable risks but as outright disqualifiers for automotive interior programs.

The regulatory inflection point came in June 2025, when the European Chemicals Agency formally advanced an EU-wide restriction proposal covering 12 hexavalent chromium compounds. The proposal targets the elimination of approximately 17 tonnes of Cr(VI) emissions annually, creating immediate compliance pressure across wet-end operations supplying European OEM platforms. As a result, automotive leather sourcing has shifted decisively toward Wet White systems, vegetable tanning, and advanced chromium-free tanning agents based on titanium, zirconium, and organic polymer networks.

At an industrial level, this transition is not incremental. Polycarbamoyl sulfonate (PCMS) chemistries are emerging as a core replacement architecture rather than a niche alternative. Commercial-scale systems such as LANXESS’s X-Tan platform demonstrate why: PCMS cross-linking eliminates the acid pickling stage, historically the largest contributor to salt loading and sulfate discharge in tanneries. Beyond environmental compliance, these systems deliver the lightfastness, tear resistance, and hydrothermal stability demanded for premium automotive seating, positioning chromium-free tanning as both a regulatory necessity and a performance upgrade rather than a compromise.

Salt-Free Preservation and Green Beamhouse Chemistry Redefine Wet-End Economics

Parallel to chromium elimination, the tanning agents market is being reshaped by a fundamental rethinking of hide preservation and beamhouse chemistry. Traditional curing relies on applying 30–50% salt by hide weight, generating high Total Dissolved Solids loads that are increasingly incompatible with Zero Liquid Discharge and regional wastewater caps. This has pushed tanneries toward salt-free or low-salt preservation routes that require a new class of penetration-efficient tanning and pre-tanning agents.

Industrial validation accelerated in 2025 through the Green Tanning Initiative, where collaborative trials led by Stahl and Solidaridad in East Africa demonstrated pickle-free tanning at commercial scale. By combining probiotic beamhouse treatments with ZDHC Level 3–compliant tanning agents, these systems delivered measurable reductions in both Chemical Oxygen Demand and Total Dissolved Solids, directly addressing the two most expensive effluent parameters for tanneries operating under tightening discharge permits.

From an operational perspective, the shift is significant. Biocatalytic preservation methods lower biological oxygen demand at the earliest processing stage, shortening soak and liming cycles while reducing water intensity across the wet end. However, these systems depend on specialized tanning agents capable of diffusing into hides without acid-salt swelling. This is driving demand for next-generation polymeric and enzyme-compatible tanning agents that function effectively in near-neutral pH environments, fundamentally altering product development priorities for chemical suppliers.

Bio-Based Tanning Systems Gain Traction in Performance Sportswear and Footwear

A high-growth opportunity is emerging at the intersection of sustainability and performance, particularly within athletic footwear and sportswear leather applications. Global brands are actively moving away from fossil-derived syntans, not only for ESG reasons but also to future-proof supply chains against petrochemical volatility. This has created a clear market pull for bio-based tanning agents that can meet extreme flex resistance, abrasion durability, and moisture management requirements.

The momentum crystallized with the launch of The Next Stride initiative in September 2025, a multi-brand coalition involving adidas, Target, and Fashion for Good. While initially focused on footwear components, the program is establishing performance benchmarks that directly influence leather tanning chemistry, including repeated flex endurance, hydrolysis resistance, and uniform dye uptake. Bio-based polysaccharide systems and enzyme-mediated tanning architectures are being evaluated as drop-in replacements for fossil syntans, opening a scalable demand channel for plant-derived and circular carbon tanning agents.

R&D intensity is particularly high around modified vegetable tannins sourced from tara and mimosa. Through controlled polymerization, these tannins now deliver the soft handfeel, grain tightness, and shade consistency historically associated with chrome leather, while maintaining a fully bio-based carbon profile. For suppliers, this segment offers margin expansion opportunities, as performance footwear programs prioritize validated functionality over lowest-cost chemistry.

Integrated One-Shot Tanning and Finishing Systems Redefine Productivity Metrics

The second major opportunity lies in process integration rather than molecule substitution alone. Tanneries are under increasing pressure to reduce labor, water, and energy intensity per square meter of leather, driving adoption of compacted “one-shot” chemical systems that combine tanning, retanning, and fatliquoring into a single application stage.

Operational data from 2024–2025 shows that modern integrated systems can cut total processing time by 25–40%, while materially reducing rinse cycles and thermal energy demand. This is not a marginal efficiency gain; it fundamentally changes tannery throughput economics, especially in regions facing rising utility costs and water scarcity. Suppliers offering fully engineered one-shot solutions are therefore moving upstream in the value chain, selling process reliability and compliance assurance rather than individual chemicals.

Compliance alignment is a decisive enabler. By late 2024, leading suppliers had achieved ZDHC Gateway Level 3 compliance across the majority of their tanning and finishing portfolios, allowing tanneries to meet brand transparency and non-toxicity requirements through a single certified chemical suite. This simplifies audit complexity, shortens customer qualification cycles, and positions integrated systems as the default choice for export-oriented tanneries supplying automotive, footwear, and premium upholstery markets.

Tanning Agents Market Share and Segmentation Insights

Mineral Tanning Agents Lead Market with Chrome Tanning Efficiency and Industrial Scalability

Mineral tanning agents accounted for 58.60% of the tanning agents market in 2025, driven by the dominance of chrome tanning technology in global leather processing. Chromium salts enable fast processing cycles, high hydrothermal stability, softness, and superior dye uptake, making them the preferred choice for footwear leather, automotive upholstery, and furniture applications. Chrome tanning supports over 85% of global leather production, reinforcing its industrial relevance. The 2025 market trend focuses on chrome recovery and recycling systems, where tanneries implement closed-loop processes to reduce chromium discharge, lower raw material costs, and meet environmental compliance while maintaining consistent leather quality.

Footwear Leather Segment Drives Tanning Agents Demand with High-Volume Global Production

Footwear leather accounted for 42.80% of tanning agents market demand in 2025, reflecting the massive scale of global footwear manufacturing, with billions of pairs produced annually. Leather used in footwear requires durability, flexibility, and aesthetic consistency, making chrome-tanned leather the dominant material. Continuous product innovation in footwear design sustains demand for specialized tanning solutions. The 2025 industry shift highlights the athleisure and casual footwear trend, where demand for soft, lightweight, and breathable leather influences tanning chemistry and retanning processes, driving formulation advancements to meet evolving performance and comfort requirements.

Tanning Agents Market Competitive Landscape

The tanning agents market in 2026 is defined by decarbonized formulations, fermentation-derived chemistries, and vinyl sulphone cross-linking technologies. Leading players are replacing aldehydes and bisphenols with bio-based systems, targeting automotive upholstery and premium footwear segments requiring certified biogenic carbon content and circular leather processing.

Stahl Accelerates Bio-Based Tanning Innovation Under Henkel with Probiotic Beamhouse Technologies

Stahl, now integrated into Henkel following a €2.1 billion acquisition in 2026, is reinforcing leadership in specialty leather chemicals and coatings. Its Proviera® probiotics platform replaces conventional de-hairing chemicals, significantly lowering BOD levels in tannery wastewater. Expansion of Stay Clean® technology into tanning enables molecular-level stain resistance, meeting EV OEM specifications. Stahl maintains ZDHC Gateway Level 3 compliance across its wet-end portfolio, supporting ESG-driven procurement. Integration with Henkel enhances R&D capabilities for bio-based tanning agents and automotive leather solutions. Focus remains on fermentation-derived chemistries and high biogenic carbon formulations.

TFL Strengthens Metal-Free Leather Systems with Ultra-Low Bisphenol Synthetic Tannins and Localized Manufacturing

TFL is advancing sustainable tanning agents through next-generation syntans with ultra-low bisphenol content, aligned with stringent safety regulations. Under new leadership, the company is prioritizing "Local for Local" production across India, China, and Latin America. Its RODA® and White Line systems enable chrome-free and metal-free leather with high hydrothermal stability. Recovery from Brazil supply disruptions has strengthened logistics resilience and digital SDS integration. AI-enabled compliance tools enhance global regulatory alignment and supply chain transparency. TFL continues to lead in eco-friendly syntans for premium leather applications.

LANXESS Advances Circular Tanning Agents with Collagen Upcycling and Cost Optimization Strategy

LANXESS is focusing on high-margin specialty tanning agents supported by €5.673 billion revenue in 2025 and €150 million cost savings under its FORWARD! program. Its X-Biomer® technology upcycles collagen waste into functional retanning agents, enabling circular leather production. Portfolio restructuring, including divestment of urethane systems, sharpens focus on sustainable intermediates. The company is optimizing production networks to unlock additional €50 million in savings. Chrome-free technologies and resource efficiency align with EU sustainability mandates. Strategic emphasis remains on circular chemistry and green transformation in leather processing.

Royal Smit & Zoon Leads Bio-Based Retanning with Bisphenol-Free Systems and Zeolite-Based Alternatives

Royal Smit & Zoon is setting sustainability benchmarks with its BioTan XP 01L, a bisphenol-free retanning agent delivering phenolic-like performance. The company achieved EcoVadis Platinum status for three consecutive years, reflecting top-tier ESG performance. Its Zeo White system provides a viable chrome alternative with superior whiteness and dyeability for fashion and footwear leather. Compliance with EU CSRD through double materiality assessments ensures transparency and traceability. Strong focus on circular leather value chains supports adoption in premium segments. Bio-based chemistries and regulatory alignment define its competitive positioning.

Trumpler Pioneers Aldehyde-Free Vinyl Sulphone Tanning with Fully Compostable Leather Systems

Trumpler is driving innovation with its DyTan system, utilizing vinyl sulphone cross-linking to eliminate aldehydes, bisphenols, and metals. Independent testing confirms full biodegradability of DyTan-treated leather under industrial composting standards. Integration of LANGRO-CHEMIE enables a complete beamhouse-to-finishing chemical portfolio. Its TRUPOTAN® range supports low-temperature processing, reducing energy consumption in tanneries. Global manufacturing across Europe and Asia ensures supply diversification. Focus on circularity and end-of-life sustainability positions Trumpler at the forefront of next-generation tanning technologies.

Pulcra Chemicals Expands Bio-Based Tanning Platforms with High Renewable Carbon Content and Zeolite Systems

Pulcra Chemicals is advancing bio-based tanning through its Naturalis® and Natur Tanning® platforms, featuring over 90% renewable carbon content. The PellNatur system integrates zeolite and fermentation-derived agents to create a stable collagen matrix. Its Coratyl® and Peramit product lines support aldehyde-free, fossil-free leather processing. Launch of STABIFIX® NBF highlights expertise in high-exhaustion fixation technologies applicable to tanning systems. Pulcra’s pulcrACTIONS program provides technical consulting to optimize water use and process efficiency. Strong focus on bio-revolution and sustainable auxiliaries drives growth in eco-friendly leather chemicals.

Germany Tanning Agents Market Driven by Portfolio Focus, Regulatory Anticipation, and Automotive Pull

Germany’s tanning agents market is undergoing a structural shift toward high-margin, regulation-ready specialty chemistry. In May 2025, LANXESS AG reported a 31.7% increase in EBITDA under its FORWARD! action plan, reflecting a decisive exit from non-core polymer businesses and a sharpened focus on advanced tanning intermediates and specialty additives. This repositioning aligns closely with tightening European regulatory frameworks and premium customer requirements, particularly in automotive and luxury leather applications.

Regulatory anticipation has become a competitive differentiator. German tanneries and chemical suppliers are leading the transition toward bisphenol-free syntans ahead of expected EU REACH tightening in 2026. Companies such as Dermacolor upgraded formulations in late 2025 to meet emerging “Premium Quality” benchmarks, reducing toxicological risk while maintaining color consistency and fiber penetration. Parallel to formulation changes, sustainability governance has deepened. During 2024–2025, German producers aligned operations with the EU Corporate Sustainability Reporting Directive, enabling granular life-cycle disclosure across mineral, chrome-based, and synthetic tanning agents. Demand-side momentum remains strong from Germany’s automotive OEMs, including BMW and Mercedes-Benz, which accelerated adoption of chrome-free and bio-based tanning agents in 2025 to ensure low-VOC interior environments. On the manufacturing front, AI-monitored batch control systems introduced in mid-2025 reduced energy intensity in sulfonated phenolic syntan production by an estimated 12%, reinforcing Germany’s position as a technology benchmark market.

Italy Tanning Agents Market Anchored in Luxury Positioning and Metal-Free Chemistry

Italy continues to define the global innovation curve for tanning agents used in high-end fashion and footwear. A pivotal development occurred in November 2025 when Stahl completed the spin-off of its wet-end leather chemicals business into an independent entity, Muno. Headquartered in Italy, Muno is now fully dedicated to tanning and wet-processing innovation, reinforcing Italy’s role as a strategic R&D nucleus rather than a volume-driven manufacturing base.

At the cluster level, Arzignano and Santa Croce sull’Arno emerged in 2025 as global reference hubs for metal-free tanning. Local initiatives scaled zeolite-based and other non-metal systems to meet growing demand from luxury brands seeking certified metal-free supply chains. Italian chemical suppliers also introduced low-astringency tanning agents in late 2025, engineered to deliver fine-grain aesthetics and softness required for lightweight leathers in Spring/Summer 2027 luxury collections. Compliance leadership further strengthens Italy’s export positioning. By May 2025, major suppliers achieved ZDHC MRSL V3.1 Level 3 recertification, the highest standard for chemical safety in tanning. This combination of regulatory credibility, fashion-driven performance requirements, and formulation expertise cements Italy’s dominance in premium tanning chemistry.

China Tanning Agents Market Balancing Scale, Localization, and Transition Chemistry

China’s tanning agents market remains structurally anchored in scale, particularly through its dominance in footwear and mass leather production. In late 2025, producers including Zhejiang Jinke Household Chemical Materials completed major capacity expansions in northern chemical zones such as Tianjin Nangang. These investments prioritized oxygen-based bleach activators and sodium percarbonate used in pre-tanning, supporting large-volume processing while relocating operations into compliant national chemical parks.

Geopolitical and regulatory constraints are reshaping formulation pathways. China’s 2024–2025 export controls on antimony accelerated domestic R&D into titanium-based catalyst systems for syntan synthesis, reducing reliance on restricted inputs. While Basic Chromium Sulfate continues to underpin China’s footwear-driven tanning demand, particularly in the Pearl River Delta, pilot deployments of low-chrome systems expanded in 2025 to address environmental scrutiny. Beyond traditional leather, diversification is evident in cosmetics. In late 2025, private label manufacturers such as Metro Private Label scaled DHA-based self-tanning agents, leveraging short-cycle, social-commerce-driven demand from Gen Z consumers. This dual-track strategy of volume leather chemistry and fast-growing cosmetic tanning agents defines China’s current market structure.

India Tanning Agents Market Accelerated by Infrastructure and Export-Oriented Sustainability

India’s tanning agents market in 2025 reflects a convergence of policy support, infrastructure modernization, and export-led sustainability. At the India International Leather Fair 2025, domestic chemical producers showcased indigenous vegetable tannin blends and enzyme-based green dehairing systems designed to materially reduce sulfide loads in effluent streams. These innovations directly address compliance costs in water-stressed leather clusters.

India’s strategic relevance increased further following the global restructuring of Stahl, as Muno retained and expanded key Indian production assets after its late-2025 carve-out. This positions India as a global manufacturing and export hub for wet-end tanning solutions rather than a purely domestic consumption market. Fiscal policy has reinforced this trajectory. The 2025 GST rationalization reduced tax burdens on bio-based surfactants and tanning auxiliaries, aligning with Make in India objectives. Critically, environmental infrastructure scaled in parallel. During 2025, India commissioned 53 new Zero Liquid Discharge common effluent treatment plants across leather clusters, enabling the safe deployment of high-performance chemical tanning agents while supporting long-term regulatory compliance.

Brazil Tanning Agents Market Rebounding Through Sustainability and Supply Security

Brazil’s tanning agents market entered a recovery phase in 2025 following significant disruption in the prior year. After the May 2024 flood at its São Leopoldo facility, TFL Ledertechnik completed infrastructure restoration in early 2025, restoring full production capacity for technical tanning solutions serving Latin American markets. This recovery stabilized regional supply chains and restored confidence among export-oriented tanneries.

Structurally, Brazil’s long-term advantage lies in vegetable tanning. In 2025, producers achieved full FSC and PEFC certification of black wattle forest assets, ensuring a fully traceable and sustainable feedstock base. This positions Brazil at the center of the global bio-tanning movement, particularly as European and North American brands accelerate substitution away from metal-intensive systems. Brazil’s tanning agents market is therefore increasingly defined not by volume alone, but by its ability to guarantee sustainable origin at scale.

Comparative Summary: Tanning Agents Market by Country

Tanning Agents Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Demand Driver

|

Structural Advantage

|

|

Germany

|

Specialty syntans, regulatory-ready chemistry

|

Automotive interiors, EU compliance

|

Technology leadership and transparency

|

|

Italy

|

Metal-free, luxury-grade tanning

|

Fashion and footwear

|

Premium formulation expertise

|

|

China

|

Volume leather chemistry plus cosmetics

|

Footwear scale and Gen Z self-tan

|

Manufacturing scale and speed

|

|

India

|

Export-oriented sustainable tanning

|

Global wet-end solutions

|

Infrastructure and policy support

|

|

Brazil

|

Vegetable tanning recovery

|

Bio-tanning for global brands

|

Certified renewable feedstock

|

Tanning Agents Market Report Scope

Tanning Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.4 Billion

|

|

Market Size (2034)

|

$15.7 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Product Type (Mineral Tanning Agents, Vegetable Tanning Agents, Synthetic Tanning Agents, Aldehyde Tanning Agents, Bio-Based and Chrome-Free Tanning Agents), By Process Phase (Pre-Tanning Agents, Tanning Agents, Retanning Agents), By End-Use Application (Footwear Leather, Automotive Upholstery, Furniture and Décor, Garments and Accessories, Cosmetics and Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LANXESS AG, Stahl Holdings B.V., TFL Ledertechnik GmbH, BASF SE, Pulcra Chemicals Group, Zschimmer & Schwarz, Smit & Zoon, Silvateam S.p.A., Trumpler GmbH & Co. KG, Elementis plc, Dermacolor, Brother Enterprises Holding Co., Ltd., Sudarshan Chemical Industries Ltd., Kemiplas

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tanning Agents Market Segmentation

By Product Type

- Mineral Tanning Agents

- Vegetable Tanning Agents

- Synthetic Tanning Agents

- Aldehyde Tanning Agents

- Bio-Based and Chrome-Free Tanning Agents

By Process Phase

- Pre-Tanning Agents

- Tanning Agents

- Retanning Agents

By End-Use Application

- Footwear Leather

- Automotive Upholstery

- Furniture and Décor

- Garments and Accessories

- Cosmetics and Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Tanning Agents Market

- LANXESS AG

- Stahl Holdings B.V.

- TFL Ledertechnik GmbH

- BASF SE

- Pulcra Chemicals Group

- Zschimmer & Schwarz

- Smit & Zoon

- Silvateam S.p.A.

- Trumpler GmbH & Co. KG

- Elementis plc

- Dermacolor

- Brother Enterprises Holding Co., Ltd.

- Sudarshan Chemical Industries Ltd.

- Kemiplas

*- List not Exhaustive