Market Overview: Advanced Conductivity & High-Voltage Performance Driving Magnet Wires Market Expansion

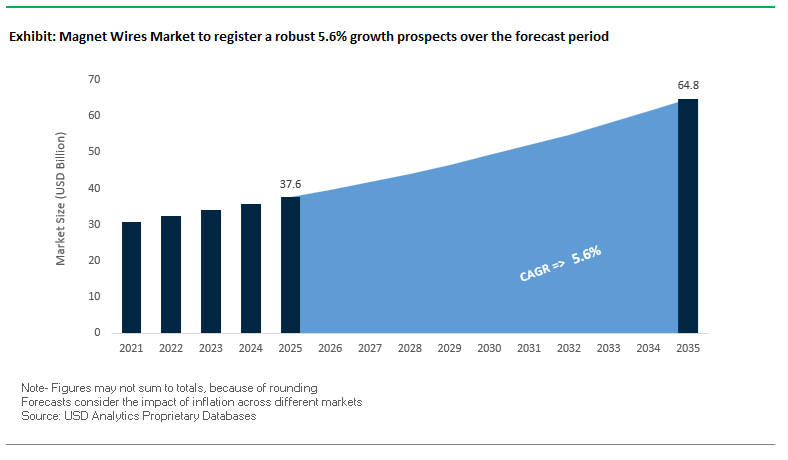

The Magnet Wires Market is projected to grow from USD 37.6 billion in 2025 to USD 64.8 billion by 2035, registering a steady CAGR of 5.6%. Market expansion is driven by high-efficiency motors, electrified transportation, power transformers, and industrial automation, all of which require high-purity copper or aluminum magnet wires with superior thermal endurance and dielectric strength. As EV architectures transition from 400V to 800V platforms, magnet wire manufacturers must meet stringent performance benchmarks—partial discharge resistance, high-temperature stability, and coating uniformity—creating a decisive shift toward Polyimide, PAI, and high-frequency enamel systems.

Modern production requirements are also shaped by the increasing adoption of hairpin winding, which enables higher slot fill factors and improved motor output density. This trend pushes vendors to scale rectangular and flat wire production with enhanced thermal classes up to 240°C. Manufacturers must therefore optimize enamel chemistry, surface uniformity, and PDIV resistance to remain competitive.

Key Insights for OEMs, Coil Manufacturers & Electrical System Integrators

- Copper dominates conductivity benchmarks, with thermal conductivity of 402 W/(m·K) essential for high-load motors and transformer cooling.

- High-temperature Polyimide and PAI insulation supports 240°C Class magnet wires, enabling downsizing in EV motors and aerospace systems.

- Hairpin / rectangular wire designs achieve >60% coil packing density, raising power density in traction motors.

- 800V EV platforms demand insulation rated above 1,000V, engineered for high PDIV resistance under PWM inverter switching.

Market Analysis: Investments, Sustainability Milestones & EV Acceleration Reshape Global Magnet Wires Market

The Magnet Wires industry is undergoing a strategic transformation as companies consolidate assets, expand rectangular wire capacity, and align with the high-growth electric mobility and renewable energy sectors. In May 2024, Superior Essex completed the acquisition of the remaining minority interest in Essex Furukawa Magnet Wire, creating a unified global entity capable of investing in next-generation magnet wire innovations. This consolidation strengthens its position across automotive, industrial motor, and transformer markets, enabling streamlined R&D programs in high-voltage winding wires (HVWW®) and solvent-free coatings.

Further supporting the EV transition, global manufacturers have announced targeted expansions. In October 2025, Furukawa Electric committed investments to establish a new production line specifically for rectangular magnet wire—a strategic decision driven by the rising demand for hairpin winding architectures in EV traction motors. The segment is gaining traction due to higher slot fill efficiency, improved thermal performance, and compatibility with automated coil insertion processes. Meanwhile, in January 2025, MP Materials began NdPr metal production in Texas, ensuring a stable non-Chinese source of high-purity rare earth metals for permanent magnet motors that rely heavily on magnet wire windings, thereby reducing geopolitical dependence in the motor supply chain.

Environmental compliance and sustainability are emerging as defining competitive differentiators. In November 2025, LS Cable & System successfully piloted its solvent-free enamel coating process, aligning with tightening European VOC restrictions and setting a precedent for green manufacturing in magnet wire production. During the same period, Superior Essex achieved a major sustainability milestone: its plants in Serbia and Germany reached 100% Zero Waste to Landfill (ZWTL) status, marking a critical achievement for OEMs evaluating upstream ESG performance. The launch of high-frequency magnet wires in October 2025, specifically engineered for PWM-rich EV inverter environments, addresses the rising need for dielectric robustness under high switching stress.

Market consolidation is also reshaping downstream demand. In September 2025, Honeywell’s acquisition of Carrier Global for USD 18.6 billion is expected to intensify magnet wire demand in the combined entity’s enhanced HVAC and industrial motor ecosystem. This large-scale integration signals increased investments in high-efficiency motors that rely on premium magnet wire categories. Meanwhile, Essex Furukawa extended its high-volume EV contract in October 2024, supplying 33,000 tons of HVWW® for next-generation 800V EV platforms—an indicator of the rapid commercialization of high-voltage insulation technologies and the robustness of the EV traction motor market.

Breakthrough Trends and Emerging Opportunities Reshaping High-Voltage, High-Temperature, and High-Density Magnet Wire Applications

Market Trend 1: Deployment of High-Temperature, Partial-Discharge–Resistant Insulation Systems for 800V+ EV Traction Motors

A defining technological shift in the magnet wires market is the rapid transition from traditional PEI/PAI enamel systems toward PEEK and Polyimide (PI) Class 220°C+ insulation architectures engineered specifically for 800V–1000V EV traction motors. PEEK demonstrates thermal reliability up to 260°C, representing a significant upgrade over Class 180°C–200°C wire coatings. This shift is largely driven by the harsh electrical conditions generated by fast-switching SiC inverters, where extreme dv/dt events accelerate insulation fatigue.

One of the most critical performance indicators is Partial Discharge Inception Voltage (PDIV). PEEK-based and composite insulation systems consistently deliver materially higher PDIV values compared to PAI coatings, significantly improving survivability during repetitive voltage overshoots. The high dielectric efficiency of extruded PEEK insulation also enables a 50% reduction in insulation thickness, which directly translates into higher copper fill factor, enabling up to 10% higher continuous torque output in traction motors.

Chemical durability is equally essential. PEEK-insulated magnet wires retain electrical integrity after 2,000 hours exposure to ATF cooling oils at 180°C, validating their use in direct-oil-cooled motor architectures that dominate next-generation EV platforms. Collectively, this trend underscores a decisive technology shift toward high-temperature, PD-resistant, chemically robust insulation systems that futureproof traction motors for ultra-fast charging and higher voltage architectures.

Market Trend 2: Strategic Scale-Up of Aluminum Magnet Wire to Reduce Weight and Cost in Mass-Produced Electric Motors

A second major trend is the accelerated adoption of aluminum magnet wire in automotive, HVAC, appliance, and auxiliary motor applications. Aluminum’s specific gravity of 2.7 g/cm³—just 30% of copper’s 8.9 g/cm³—offers a compelling weight reduction pathway in cost- and mass-sensitive systems. For EVs using dozens of small motors (pumps, compressors, fans), this weight reduction has direct energy efficiency implications.

However, aluminum magnet wires require strict metallurgical and mechanical control. To prevent cracking during high-speed winding, aluminum conductors must achieve ≥15% elongation and a minimum yield strength of 9,000 PSI. Electrical conductivity remains a trade-off: aluminum offers 61%–62% IACS conductivity compared to copper’s ~100% IACS, but due to its low density, an aluminum winding can match the DC resistance of copper at 50% of the total conductor weight.

Importantly, aluminum magnet wires are now being engineered for high thermal classes, with some PAI-coated aluminum wires qualifying for Class 220°C operation. This makes aluminum a viable and increasingly strategic choice for motors requiring high thermal endurance at lower material cost.

Market Opportunity 1: High-Fill, Formable Magnet Wires to Boost Motor Efficiency, Torque Density, and Thermal Utilization

A transformative opportunity exists in the commercialization of rectangular, flat, and hairpin-shaped magnet wires, engineered to maximize slot utilization and improve motor performance. Traditional round wires typically achieve 45%–65% slot fill, whereas hairpin and rectangular wire geometries can reach 70%–75% slot fill. This improvement enables a substantial increase in copper packing density, reducing DC resistance, boosting electromagnetic efficiency, and generating higher torque per unit volume.

Manufacturers report that increasing slot fill by 10% or more can elevate continuous motor torque output by ≥5% while enabling up to 20% motor size and weight reduction. Beyond electrical benefits, formable wires manufactured via precision extrusion achieve exceptional insulation uniformity, especially around corners—historically the weakest points for breakdown voltage. As EV traction motors evolve toward ultra-high efficiency architectures, shaped magnet wires represent a high-value opportunity for OEMs targeting improved range, lower thermal losses, and compact powertrain layouts.

Market Opportunity 2: Integration of Coolant-Compatible and Sensor-Enabled Insulation Systems for Smart, Thermally Managed Motors

A second emerging opportunity centers on next-generation insulation systems engineered for active cooling environments and embedded sensing capabilities. Advances in foamed PI insulation show that reducing the relative permittivity (εr) from 3.0 to 1.7 can drastically extend dielectric life. Demonstrations reveal that foamed PI wire withstands 2,500 minutes of breakdown testing at 900 Vp, compared to 78 minutes for traditional PI—representing a step-change for high-frequency inverter environments.

Coolant exposure resistance is also critical. Modern PAI coatings such as GP/MR-200R◉ pass refrigerant compatibility tests with R-134a and R-123, showing no degradation after prolonged immersion. For systems using oil-jet-cooled stators, Polyimide (ML) insulation remains one of the few materials that resist thermoplastic flow even above 400°C, ensuring insulation stability under direct contact with high-temperature fluids.

Looking ahead, embedding sensors into magnet wire insulation—such as micro-temperature sensors or strain-sensitive films—promises real-time health monitoring for power-dense EV motors and industrial drives. These innovations will create new product classes of smart magnet wires optimized for predictive maintenance, lifetime extension, and thermal load management.

Magnet Wires Market Share Analysis

Market Share by Conductor Material: Copper Magnet Wire Dominates Owing to Superior Conductivity, Efficiency, and Mechanical Reliability

Copper Magnet Wire holds the dominant market share—approximately 70%—because it delivers the highest electrical and mechanical performance required by modern motors, transformers, and high-efficiency power systems. As the benchmark conductor material, copper provides 100% IACS conductivity, far exceeding aluminum’s ~61%, which directly translates into lower resistive losses, reduced heat generation, and improved system efficiency. These advantages are crucial as global regulatory bodies continue tightening efficiency standards for industrial motors, EV traction systems, and energy equipment. Copper’s ability to carry higher current through a smaller cross-sectional area allows manufacturers to design more compact and lightweight motors—an essential advantage in electric vehicles, robotics, and consumer electronics where power density is a decisive metric. Its superior tensile strength, lower thermal expansion, and long-term stability ensure winding integrity even under extreme electrical, thermal, and centrifugal stresses, making it indispensable for high-speed and high-torque motor architectures. With rising electrification, the proliferation of high-efficiency motors, and advancements such as hairpin winding technologies, copper magnet wire remains the foundational material for next-generation electrical machines, securing its continued leadership in the global magnet wires market.

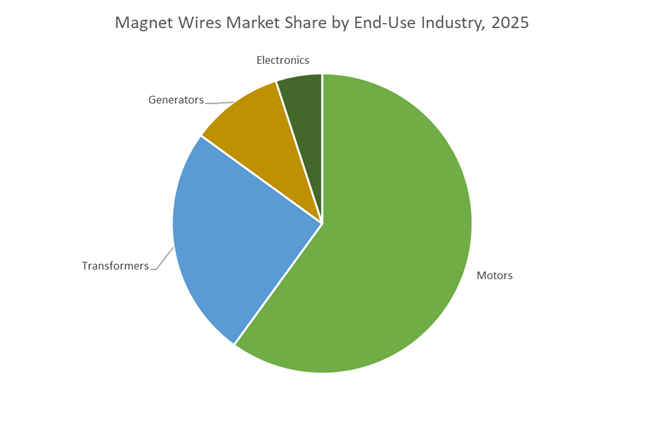

Market Share by End-Use: Motors Lead Due to Electrification, Industrial Automation, and High-Efficiency Motor Standards

The Motors segment accounts for the largest share of the global magnet wires market—approximately 60%—because electric motors are the most widespread and magnet-wire-intensive electromechanical devices across nearly every industrial, automotive, and consumer application. The most transformative driver is the global shift toward electric mobility, where EV traction motors, onboard auxiliary motors, and battery thermal management systems require large quantities of high-performance copper magnet wire, often in advanced rectangular or hairpin formats to achieve exceptional current density and thermal stability. Each EV can contain 3–4 times more copper magnet wire than a traditional internal combustion vehicle, creating exponential growth in material demand. Simultaneously, rapid industrial automation, robotics deployment, and the proliferation of high-duty-cycle industrial motors reinforce the segment’s dominance, as these applications rely on premium magnet wire to withstand continuous operation, high torque loads, and elevated operating temperatures. Global energy-efficiency mandates (IE3, IE4, and IE5 motor standards) further amplify copper demand, pushing manufacturers to adopt higher-grade windings to reduce energy loss and enhance overall system performance. Given its scale, regulatory pressure, and deep integration into electrification trends, the motors segment remains the unequivocal anchor of market demand for magnet wires worldwide.

Country Analysis: Global Magnet Wire Production, EV Electrification Demand, and Advanced Insulation Technology Trends

China: Rectangular Magnet Wire Manufacturing Leadership and NEV-Driven Demand Surge

China remains the global powerhouse in the Magnet Wires Market, driven by its massive NEV production ecosystem and large-scale shift toward rectangular magnet wire to increase electric motor output efficiency. Rectangular wires provide superior slot-fill ratios, enabling higher torque density and lower copper losses—attributes essential for competitive traction motor performance. Under the Made in China 2025 initiative, China continues to localize key EV components, including high-voltage magnet wire, reducing reliance on Japanese and Korean insulation technologies. This localization drive is paired with accelerating investments from leading producers such as Tongling Jingda, which announced major production line expansions dedicated to high-thermal-class rectangular wire designed specifically for high-speed, inverter-driven motors.

The country’s position as the world’s largest NEV manufacturer amplifies demand for Class 200+ magnet wire, corona-resistant insulation, and specialized conductor geometries for e-motors, inverters, and onboard chargers. China’s integrated supply chain allows magnet wire suppliers to rapidly scale output in sync with downstream automotive OEM expansion. Government-backed industrial policies and aggressive electrification goals continue reinforcing China’s dominance in volume manufacturing, shaping global capacity allocation and pricing structures for rectangular and enameled round magnet wire variants.

India: PLI-Driven Growth in EV Magnet Wire Manufacturing and AAT Localization Momentum

India is rapidly building a strong domestic market for high-performance magnet wires through major government stimulus packages targeting EVs, power electronics, and advanced materials. The country’s ₹25,938 crore PLI Scheme for Automobile and Auto Components directly incentivizes domestic production of Advanced Automotive Technology (AAT) components, including specialized magnet wires used in traction motors, DC fast chargers, and EV auxiliary systems. These incentives are creating attractive conditions for global and domestic suppliers to establish localized, high-specification wire production, particularly for high-temperature copper and aluminum conductor variants.

India’s ecosystem expansion is further reinforced by the PM E-DRIVE Scheme, a ₹10,900 crore initiative accelerating nationwide EV infrastructure deployment. This policy stimulates magnet wire demand beyond vehicles, extending into transformers, charging station electronics, and grid-side power management systems. Complementing these initiatives, the Ministry of Heavy Industries funds up to 80% of EV-related R&D costs, encouraging collaborations with academic institutions to develop next-generation insulation materials tailored for high-frequency e-Axle motors. As India positions itself as a major global EV and component supplier, magnet wire manufacturers benefit from a structurally expanding home market, reduced import dependency, and long-term policy stability.

Japan: Ultra-Fine Magnet Wire and Polyimide Film Excellence for High-Frequency and Aerospace Applications

Japan remains the global benchmark for precision magnet wire technology, with unmatched leadership in polyimide-filmed high-temperature magnet wires, ultra-fine wire manufacturing, and reliability-critical aerospace materials. Companies such as Sumitomo Electric Industries continue advancing polyimide-coated magnet wire solutions that deliver exceptional thermal stability, chemical resistance, and high Partial Discharge Inception Voltages (PDIV)—critical for high-frequency, inverter-driven EV motors and aerospace power systems. These materials are engineered to withstand harsh environments while maintaining dimensional integrity, enabling Japan to supply some of the highest-value magnet wire applications globally.

Japanese innovators such as Fujikura dominate the ultra-fine wire segment used in compact electronics, medical sensors, and precision actuators where millimeter-scale space constraints and extremely low resistance pathways are mandatory. Reinforcing this leadership, Sumitomo’s breakthrough in microcellular insulation technology—first announced in 2020—significantly improves the space factor and current density of EV drive motors. Japan's R&D investments, supply chain precision, and advanced insulation chemistry ensure its continued influence on the premium, high-performance segment of the Magnet Wires Market.

South Korea: 800V EV Architecture Acceleration and Advanced Flat-Wire Innovations for High-Power Motors

South Korea is at the forefront of high-voltage EV powertrain innovation, with OEMs like Hyundai and Kia accelerating adoption of 800V architectures, which significantly increase demands on magnet wire insulation systems. These high-voltage ECUs and traction motors require corona-resistant magnet wires with Class 200/220 thermal endurance and robust dielectric properties. This shift is catalyzing domestic demand for advanced insulation polymers such as Polyamide-Imide (PAI) and Polyetherimide (PEI), engineered to withstand high-frequency switching and thermal cycling in compact motor designs.

Korean cable and magnet wire suppliers, notably LS Cable & System, are scaling production to serve global markets, including North America. Their investment in 2023 to expand automotive magnet wire capacity reflects Korea's strategic intent to dominate the high-performance flat-wire segment essential for high-power-density motors. Additionally, South Korea’s leadership in EV battery and semiconductor manufacturing further strengthens its demand for ultra-reliable magnet wire solutions for drives, power modules, and auxiliary electronics.

United States: Re-shoring Magnet Wire Production and High-Efficiency Transformer Wire Innovation

The United States is prioritizing domestic production of high-efficiency magnet wires as part of its broader industrial re-shoring and grid modernization strategies. Leading suppliers such as Rea Magnet Wire Company and Elektrisola are investing in facility upgrades to expand output of advanced rectangular wire, self-bonding wire, and high-frequency inverter motor wire. These investments align with U.S. automotive electrification trends, industrial automation growth, and the rising demand for ANSI/UL-certified magnet wires with enhanced dielectric strength and longevity.

The U.S. is also experiencing a surge in demand for aluminum magnet wire as federal infrastructure programs increase investment in utility-scale transformers and renewable energy systems. Magnet wire R&D is benefiting from government grants focused on energy efficiency improvement and supply chain resilience, fueling innovation in high-purity conductor manufacturing, advanced enamels, and environmentally friendly coating technologies. With the electrification of transport, energy, and manufacturing accelerating nationwide, the U.S. market is transitioning toward high-value, high-performance magnet wire products.

Mexico: Rapid Magnet Wire Manufacturing Growth Under Nearshoring and North American EV Supply Chain Realignment

Mexico has emerged as a critical manufacturing hub within the North American automotive and EV supply chain, driven by nearshoring shifts and USMCA-related incentives. Its rapidly expanding automotive ecosystem is attracting magnet wire manufacturers that support e-motor winding, power electronics, and charging equipment assembly for U.S. and Canadian OEMs. With companies like LS Cable & System strengthening their production footprint in Mexico, the country is becoming strategically important for supplying flat and enameled round magnet wires tailored for EV traction motors, 800V powertrains, and high-capacity alternators.

Mexico’s proximity to the U.S. market—combined with strong logistics connectivity and competitive labor advantages—positions it as a preferred location for magnet wire winding, conductor shaping, and component integration activities. As North America intensifies investments in EV and renewable energy infrastructure, Mexico's magnet wire sector is expected to grow significantly, supporting both OEM production and after-market components for motor repair and transformer rewinding.

Competitive Landscape: Technology Leadership, EV Specialization & Sustainability Define Market Positioning

Global competition in the magnet wires market centers around EV traction motor specialization, high-frequency enamel systems, advanced insulation materials, and regional manufacturing resilience. Companies differentiate through insulation chemistry, thermal class engineering, and ability to meet automotive-grade PDIV and mechanical endurance requirements. As sustainability regulations tighten and OEMs push toward 800V system adoption, manufacturers with vertically integrated production, green coating technologies, and proven partnerships with EV and industrial OEMs are best positioned for long-term growth.

Superior Essex – Superior Essex strengthens global dominance in EV-grade high-voltage magnet wires

Superior Essex (sole owner of Essex Furukawa) is a leading force in the high-performance segment, offering HVWW®, high-purity magnet wire, and Litz wire solutions for advanced motors and transformers. With a strategic emphasis on EV platforms—particularly 800V systems—the company specializes in enamel technologies offering Class 240°C thermal stability and superior dielectric endurance. Its global footprint across North America, Europe, and Asia ensures supply resilience for automotive OEMs navigating rapidly scaling EV production. Superior Essex is also a front-runner in sustainability; its Serbian and German plants achieving Zero Waste to Landfill in November 2025 demonstrates leadership in responsible manufacturing. The launch of high-frequency magnet wires in October 2025 further positions the company at the forefront of next-generation inverter-driven motor applications.

LS Cable & System Ltd. – LS Cable leads Asia’s shift to green magnet wire production and advanced enameled wire technologies

LS Cable & System is recognized for its extensive portfolio of round, flat, and rectangular enameled wire, with thermal ratings from 120°C to 200°C. A technology leader in Asia, the company is pioneering solvent-free coating processes, successfully piloted in November 2025, aligning with global efforts to reduce VOC emissions. Its integration into major power grid and HVDC projects strengthens its position in large-scale transformer and generator segments. LS Cable’s expertise in high-function magnet wires also supports emerging renewable energy, HVAC, and industrial motor applications. Its parent company’s infrastructure footprint provides a strategic advantage in tapping utility, power generation, and smart grid opportunities.

Sumitomo Electric Industries, Ltd. – Sumitomo expands automotive-grade rectangular magnet wire capacity for EV powertrains

Sumitomo Electric is deeply embedded within Japanese and global automotive supply chains, co-developing advanced magnet wire solutions with major EV OEMs. The company excels in rectangular magnet wires, engineered with high scrape resistance and fusion-bonded insulation ideal for automated winding and hairpin motor production. Sumitomo’s current global expansion programs aim to scale rectangular wire capacity to meet surging EV traction motor demand. Its thermal-resistant wire technologies support durability in high-temperature, high-frequency switching environments, making it a preferred partner for Tier-1 motor manufacturers in Japan, the U.S., and Europe.

Tongling Jingda Special Magnet Wire Co., Ltd. – Jingda drives high-volume, cost-efficient magnet wire production for global appliance and motor markets

Tongling Jingda is a global volume leader with extensive capabilities in enameled copper and aluminum magnet wire, serving appliance, industrial motor, and general-purpose markets. The company’s competitive advantage lies in high production capacity, cost efficiency, and wide material compatibility across Polyimide, Polyesterimide, and hybrid insulation systems. Its large portfolio supports diverse applications—from micro-motors to large industrial drives—positioning Jingda as a reliable supplier for OEMs seeking scalable, economically viable magnet wire solutions. With strong penetration in China and exports across Asia, Europe, and the Americas, Jingda remains a central supplier in the global ecosystem.

Furukawa Electric Co. Ltd. – Furukawa advances high-frequency magnet wire technologies and EV hairpin production capabilities

Furukawa Electric leverages its strong materials science foundation to develop high-frequency and Litz wire solutions for inductors, wireless charging pads, and advanced power electronics. Its production portfolio includes wires engineered for PWM-intensive environments, offering superior dielectric strength and mechanical resilience. In October 2025, the company announced investments in a new production line dedicated to rectangular magnet wire, supporting the global shift toward hairpin windings in EV powertrains. Furukawa’s R&D remains focused on delivering next-generation heat-resistant insulation systems and electromagnetic performance improvements to meet stringent EV motor efficiency standards.

Von Roll Holding AG – Von Roll leverages insulation expertise to supply high-reliability magnet wires for generators and aerospace

Von Roll specializes in high-temperature magnet wires integrated with mica-based insulation systems, enabling exceptional dielectric robustness for high-voltage industrial motors, wind turbine generators, and aerospace electrical systems. With expertise spanning resins, tapes, composites, and insulation materials, the company delivers complete electrical insulation solutions rather than just wire products. Its differentiation lies in long-life, failure-intolerant applications such as rail, wind energy, and aerospace platforms. Von Roll’s vertically integrated insulation portfolio ensures consistent quality and enhances its competitiveness in sectors demanding extreme reliability and thermal endurance.

Magnet Wires Market Report Scope

Magnet Wires Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.6 Billion

|

|

Market Size (2035)

|

$64.8 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Conductor Material (Copper, Aluminum, Copper-Clad Aluminum), By Wire Shape (Round, Rectangular/Flat, Square, Litz Wire), By Insulation Material/Thermal Class (Polyester/Polyurethane, Polyesterimide, Polyamide-Imide/Polyimide, Enamelled Wire, Fiber/Film Covered Conductors), By End-Use Application (Motors, Transformers, Generators, Electronics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sumitomo Electric, LS Cable & System, Tongling Jingda, Rea Magnet Wire, Hitachi Metals, Furukawa Electric, Sam Dong, Von Roll, Essex Solutions, IRCE, Elektrisola, Fujikura, Ningbo Jintian Copper, Condumex, Madhav Copper

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Magnet Wires Market Segmentation

By Conductor Material

- Copper Magnet Wire

- Aluminum Magnet Wire

- Copper-Clad Aluminum (CCA)

By Wire Shape

- Round Magnet Wire

- Rectangular / Flat Magnet Wire

- Square Magnet Wire

- Litz Wire

By Insulation Material / Thermal Class

- Polyester / Polyurethane

- Polyesterimide

- Polyamide-Imide (PAI) / Polyimide (PI)

- Enamelled Wire

- Fiber / Film Covered Conductors

By End-Use Industry

- Motors

- Transformers

- Generators

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Magnet Wires Market

- Sumitomo Electric

- LS Cable & System

- Tongling Jingda

- Rea Magnet Wire

- Hitachi Metals

- Furukawa Electric

- Sam Dong

- Von Roll

- Essex Solutions

- IRCE

- Elektrisola

- Fujikura

- Ningbo Jintian Copper

- Condumex

- Madhav Copper

*- List not Exhaustive

Research Coverage: Magnet Wires Market

This USDAnalytics report investigates how the global magnet wires market is being reshaped by high-efficiency motors, EV traction platforms, high-voltage transformers, and automation-driven industrial drives, providing deep dives into materials science breakthroughs, manufacturing upgrades, and insulation technology transitions. It delivers analysis reviews on the shift from round to hairpin and rectangular conductors, evaluates thermal and dielectric performance benchmarks for both copper and aluminum winding wires, and highlights how regulatory efficiency standards, 800V architectures, and sustainability mandates are altering sourcing, specification, and design strategies across OEMs and coil manufacturers. The study maps investments in high-temperature enamel systems, solvent-free coating lines, and regional capacity additions, while benchmarking leading producers on technology readiness, EV alignment, and green manufacturing credentials; as such, this report is an essential resource for decision-makers seeking to de-risk supply chains, qualify next-generation high-voltage winding solutions, and capture long-term growth in the global magnet wires ecosystem.

Scope Highlights

- Segmentation By Conductor Material: Copper magnet wire, aluminum magnet wire, copper-clad aluminum (CCA)

- Segmentation By Wire Shape: Round winding wire, rectangular/flat magnet wire, square magnet wire, Litz construction

- Segmentation By Insulation / Thermal Class: Polyester and polyurethane coatings, polyesterimide systems, PAI/PI high-temperature enamels, standard enamelled wire families, fiber- and film-covered conductors for specialized duty

- Segmentation By End-Use Industry: Electric motors, power and distribution transformers, generators, and electronic devices / components

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, covering both established electrical equipment hubs and emerging EV manufacturing clusters.

- Timeframe: Historic assessment from 2021 to 2025 paired with quantitative forecasts and qualitative outlooks from 2026 to 2034, capturing the shift to 800V architectures, advanced insulation systems, and rectangular wire adoption.

- Companies: In-depth analysis and profiling of 15+ key players across the value chain, including global leaders in magnet wire production, specialty insulation, and EV-focused high-voltage winding technologies.