Market Overview: Rapidly Scaling Rare Earth Metals Market Under Supply-Control Regime

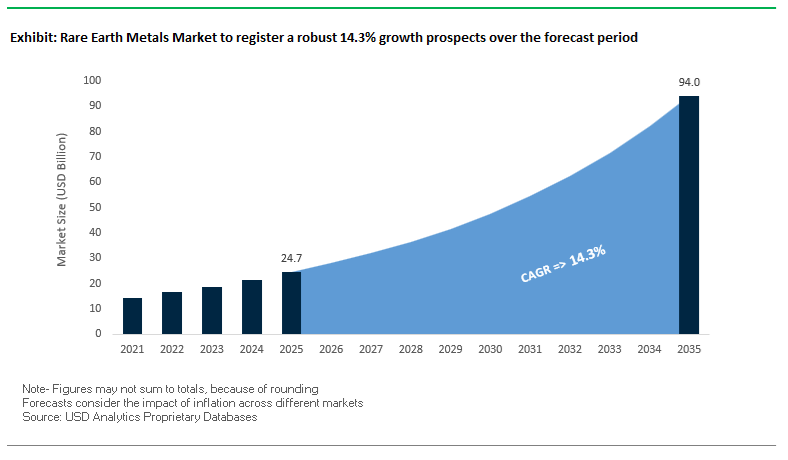

The Rare Earth Metals Market is projected to rise from USD 24.7 billion in 2025 to around USD 94 billion by 2035, reflecting a strong CAGR of 14.3% (2025–2035). This high-growth trajectory is underpinned by accelerating demand for NdPr, Dy, and Tb in permanent magnets used across electric vehicles, wind turbines, industrial motors, and defense systems. At the same time, the market remains structurally constrained by Chinese production quotas and limited heavy rare earth element (HREE) resources, forcing OEMs and magnet manufacturers to redesign supply chains, secure long-term offtake, and invest in recycling and non-Chinese refining capacity. For manufacturers and vendors, this means that security of supply, oxide purity, and mine-to-magnet integration are becoming as strategically important as cost per kilogram.

Key insights for manufacturers, magnet vendors, and OEMs:

- Tight upstream control via Chinese quotas: China’s MIIT rare earth oxide (REO) mining quota of ~240,000 tonnes in 2023 underscores that primary feedstock for rare earth metals and oxides is administratively controlled, not purely market-driven.

- LREE vs HREE geographic imbalance: Bayan Obo remains a predominantly LREE (Nd, Pr, La, Ce) resource, while critical HREEs like Dy and Tb are concentrated in ion-adsorption clays, mostly in southern China and select non-Chinese projects – a structural risk for high-temperature magnet supply.

- Magnet-centric demand concentration: Over 80% of value-driven rare earth demand is tied to the four magnetic REEs (Nd, Pr, Dy, Tb), meaning NdPr oxide and HREE availability directly determine pricing, margin structure, and long-term contracts in EV and wind industries.

- Recycling underdeveloped but strategically critical: Despite high value, recycling and REE recovery from end-of-life magnets, electronics, and batteries is still nascent; the U.S. remains >95% import-reliant for rare earth compounds and metals, highlighting a major opportunity for recycling technologies and closed-loop magnet programs.

Market Analysis: Export Controls, Mine-to-Magnet Strategies, and Non-Chinese Capacity Build-Out

The global rare earth metals market is entering a structurally tighter and more politicized phase, with export controls and national industrial strategies reshaping trade flows and investment decisions. In October 2025, China’s MOFCOM announced broad new export controls on medium and heavy rare earth materials, technologies, and equipment (effective November 2025). This move escalates geopolitical risk for downstream manufacturers of high-performance magnets, EV motors, defense systems, and advanced electronics, forcing OEMs in the U.S., Europe, Japan, and Korea to accelerate diversification away from single-country dependence. These controls sit atop the earlier MIIT quota system and effectively add a second layer of policy risk: even if mined volumes are high, cross-border availability can be throttled for strategic reasons, pushing up premiums for non-Chinese NdPr oxide and HREE supply.

Against this backdrop, non-Chinese producers are rapidly upgrading from concentrate suppliers to fully integrated metal and magnet producers. In January 2025, MP Materials commenced NdPr metal production at its Fort Worth, Texas facility with an initial capacity target of 1,000 tonnes per year, forming the downstream pillar of its mine-to-magnet strategy rooted in Mountain Pass feedstock. By July 2025, MP Materials had secured a landmark public-private partnership with the U.S. Department of Defense (DoD), which includes a price floor of USD 110/kg for NdPr and a commitment to purchase 100% of magnets from the new facility—effectively de-risking capex, stabilizing revenue visibility, and strengthening U.S. industrial security. In Q3 2025, the company further signaled its strategic pivot by halting low-margin concentrate sales to former Chinese customers, redirecting material into its own metal and magnet value chain.

In parallel, Lynas Rare Earths and Australian stakeholders are consolidating their position as the major non-Chinese alternative. In May 2024, the Australian government reaffirmed funding support for Iluka Resources’ Eneabba Rare Earths Refinery, a project designed to build a new domestic rare earth separation chain, especially for NdPr and byproduct HREEs from mineral sands monazite. Subsequently, Lynas Rare Earths announced in October 2025 an A$180 million self-funded expansion of its Malaysian facility to add up to 5,000 tpa of heavy rare earth separation capacity, with first Samarium production from Mt Weld feedstock forecast around April 2026. These moves significantly increase non-Chinese processing capacity for both LREE and HREE, offering magnet makers alternative sources for Nd, Pr, Dy, and Tb.

Policy dynamics in Western markets are also reshaping demand patterns and incentivizing localized supply. In October 2024, the U.S. government increased tariffs on Chinese EV exports from 27.5% to 102.5%, implicitly incentivizing non-Chinese EV supply chains and thereby magnifying the importance of diversified NdFeB magnet and REE sourcing. Parallel to this, emerging price benchmarks and financial infrastructure—such as Argus and other agencies introducing new assessments for key REE products—are expected to follow similar moves seen in related metals, improving price transparency and bankability of new projects. Combined, these industrial policies, export controls, and strategic funding programs are pushing the rare earth metals industry into a new era of regionalized, vertically integrated, and security-driven growth rather than purely cost-driven sourcing.

Strategic REE Trends and High-Value Opportunities Driving Mine-to-Magnet Transformation and Advanced Material Innovation

Market Trend 1: Massive Global Capital Shift Toward Non-Chinese Mine-to-Magnet Supply Chains Amid 90% Processing Concentration Risk

A defining trend for the Rare Earth Elements Market is the unprecedented acceleration in supply chain restructuring driven by geopolitical exposure and overwhelming midstream concentration. China currently controls ~90% of global rare earth processing, giving it near-total leverage over the oxide, metal, and magnet supply chain. Even developed economies remain vulnerable: the EU imports ~17,000–18,000 tonnes of NdFeB magnets annually from China, representing an ~85% dependency rate for finished permanent magnets. This reliance exposes automotive, wind energy, defense, and electronics manufacturers to systemic supply risk.

In response, governments and private investors are directing US$4.2 billion in 2025 alone toward new mining, separation, and magnet production facilities outside China. These investments are aimed at creating vertically integrated “mine-to-magnet” ecosystems capable of producing high-purity oxides, metals, alloys, and sintered magnets domestically. Resource development is also expanding globally, with Malaysia confirming 16.1 million tonnes of non-radioactive REE reserves, positioning it as a strategic long-term supply hub. As global electrification and defense requirements surge, this trend signals a structural rebalancing of the REE midstream industry.

Market Trend 2: Technological Breakthroughs in Heavy Rare Earth (HRE) Reduction for High-Temperature NdFeB Magnet Performance

The second major trend is the aggressive global push to reduce dependence on expensive and supply-constrained Heavy Rare Earth Elements (HREEs) such as Dysprosium (Dy) and Terbium (Tb) used in high-temperature NdFeB magnets. Grain Boundary Diffusion (GBD) technology is enabling a 70%–100% reduction in Dy/Tb content, dramatically lowering exposure to HREE supply instability.

GBD innovation focuses on concentrating Dy/Tb at the grain boundaries, the most efficient microstructural position for enhancing Intrinsic Coercivity (HcJ). This targeted method has enabled magnet manufacturers to achieve previously unattainable high-performance grades such as N55H, 56SH, and 52UH—characterized by advanced composite metrics where HcJ (kOe) + (BH)max (MGOe) > 83. These technologies are essential for EV traction motors, where elevated operating temperatures rapidly degrade coercivity. HREE-diffused magnets experience slower HcJ decline under heat, ensuring reliability and thermal stability during high-load operation.

This trend is transforming the NdFeB magnet industry from volume-based to microstructure-engineered production, enabling both cost optimization and significantly improved high-temperature performance.

Market Opportunity 1: Large-Scale REE Recovery from End-of-Life Magnets to Create Circular Magnet Supply Chains

The most immediate opportunity for supply diversification lies in industrial-scale magnet recycling. Spent NdFeB magnets are exceptionally rich in REEs—containing 20%–30% Nd, Dy, and Pr, compared with <5% REE concentration in natural ores. This makes magnet scrap one of the highest-grade rare earth feedstocks available globally.

Hydrometallurgical recycling methods are achieving up to 99.3% recovery of Nd and 98% recovery of Dy, surpassing most primary ore processing efficiencies. In addition, direct recycling technologies such as Hydrogen Processing of Magnet Scrap (HPMS) allow magnet powder to be re-sintered into new magnets with <5% performance deviation relative to magnets made with virgin materials—enabling circular manufacturing with minimal value loss.

Environmental benefits are equally compelling. Traditional hydrometallurgy generates 10–15 tonnes of wastewater per tonne of REE recovered, but advancements such as ionic liquid extraction are reducing wastewater volumes by ~70%, making recycling both economically and environmentally superior. As global EV and wind turbine waste streams expand, the recycling opportunity will become one of the highest-impact contributors to secure REE supply.

Market Opportunity 2: Rare Earth Integration in High-Temperature Ceramics and Superalloys for Extreme Thermal Environments

A second high-value opportunity is the rapidly growing use of REEs in Thermal Barrier Coatings (TBCs) and advanced ceramics for aerospace and industrial gas turbine engines. Rare-earth oxides such as La, Gd, Yb dramatically lower thermal conductivity to <1 W/(m·K), enabling turbine components to withstand temperatures >1,300°C—critical for efficiency gains in next-generation propulsion systems.

Rare earth dopants improve sintering resistance, preventing pore collapse that can otherwise increase thermal conductivity by nearly 50% after 20 hours at 1,200°C. In parallel, rare-earth zirconates (e.g., La₂Zr₂O₇) exhibit superior phase stability above 1,200°C, avoiding the degradation problems seen in traditional Yttria-Stabilized Zirconia (YSZ) coatings.

Emerging multilayer architectures, such as double-ceramic-layer coatings combining YSZ with rare-earth zirconates, deliver up to 6× longer thermal cycling life. These advancements directly support ultra-high-efficiency gas turbines, hypersonic aerospace systems, and industrial furnaces—creating sustained long-term demand for specialized REE oxides and compounds.

Rare Earth Metals Market Share Analysis

Market Share by Rare Earth Group: Light Rare Earth Elements (LREE) Lead Due to Abundance, Lower Processing Cost, and Dominance in High-Volume Applications

Light Rare Earth Elements (LREE)—including Neodymium (Nd), Praseodymium (Pr), Cerium (Ce), and Lanthanum (La)—hold an overwhelming ~85% share of the global rare earth metals market because they are both geologically abundant and central to the highest-volume industrial applications. LREE-enriched minerals like Bastnäsite and Monazite occur in large, economically extractable deposits, providing significantly higher ore grades compared to Heavy Rare Earth Elements (HREE), which are scarcer and dispersed. This geological advantage translates into lower mining and separation costs, making LREE the backbone of commercial-scale production. Cerium alone accounts for 40–50% of global production due to its essential use in automotive catalysts and glass polishing. Moreover, Nd and Pr—core components of NdFeB permanent magnets—drive high-value demand across electrification, robotics, and advanced manufacturing. The processing chemistry for LREE is also more mature, scalable, and cost-efficient, amplifying their dominance in global supply chains. As industries accelerate production of electric motors, catalytic converters, and precision polishing consumables, LREE remain the foundational, highest-volume segment, maintaining the largest market share across the rare earth metals ecosystem.

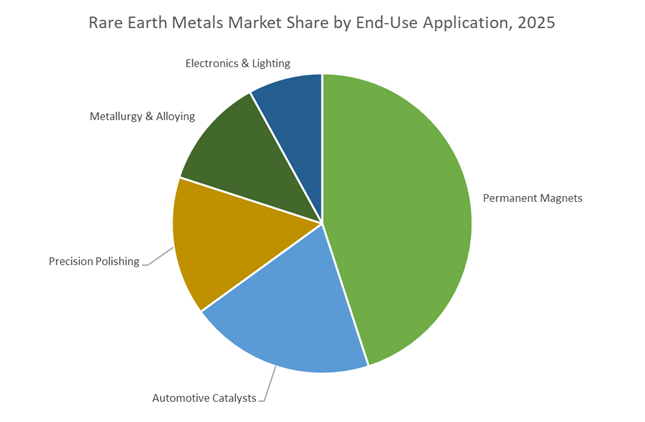

Market Share By End-Use Industry: Permanent Magnets Dominate as Electrification and Renewable Energy Drive High-Value Demand

Permanent Magnets represent the largest end-use segment, accounting for ~45% of global rare earth demand, because rare earth magnet materials—especially Neodymium and Praseodymium (NdPr)—are indispensable for high-efficiency, compact motor systems used across clean energy and electrification technologies. NdFeB magnets offer the highest energy product and magnetic strength of any commercial magnet material, enabling superior torque density, efficiency, and miniaturization—properties that are essential for EV traction motors, industrial automation, consumer electronics, and aerospace actuators. In renewable energy, direct-drive wind turbines rely heavily on NdFeB magnets to eliminate gearboxes, reduce maintenance, and boost power conversion efficiency. Rapid EV adoption and wind capacity expansion are causing NdPr demand to surge at some of the fastest growth rates within the rare earth sector, with permanent magnets expected to absorb nearly 80% of all magnet-grade rare earth consumption over the coming decade. Although catalysts and polishing applications consume larger volumes of lower-value elements like Cerium, the high unit value of NdPr and their non-substitutable role in global electrification firmly position permanent magnets as the dominant, revenue-leading segment in the rare earth metals market.

Country Analysis: Strategic Rare Earth Metals Supply, Refining, and Magnet Manufacturing Leadership Across Global Markets

China: Near-Total Refining Dominance and Escalating Export Controls Reshaping Global Heavy Rare Earth Supply

China remains the central force in the Rare Earth Metals Market, with an overwhelming 91% share of global rare-earth refining in 2024 (IEA). This dominant position gives China unprecedented influence over the high-value separation, oxide refining, and metallization steps that ultimately determine supply availability for NdFeB magnets, EV motors, wind turbines, and semiconductor components. Its introduction of expanded export licensing requirements on 12 key elements in late 2025—specifically dysprosium and terbium—triggered a 50–75% surge in dysprosium oxide prices, demonstrating how China's policy can dictate market volatility globally. Equally significant was the brief rollout of an extraterritorial control proposal in October 2025, requiring foreign magnet producers to meet Chinese ownership restrictions—an unmistakable signal of China’s willingness to leverage policy to steer global magnet supply chains.

China’s heavy rare earth vulnerabilities were magnified when Myanmar’s feedstock imports collapsed in early 2025, threatening over half of China’s dysprosium and terbium inputs. The event reinforced Beijing’s urgency to diversify supply through overseas investments, recycling, and new domestic extraction technologies. Concurrently, China is expanding its geopolitical influence through the International Economic and Trade Cooperation Initiative on Green Mining and Minerals, launched at the G20 Summit 2024, which analysts interpret as a strategic attempt to shape emerging global standards in responsible rare earth extraction. In parallel, China continues scaling NdFeB magnet production, retaining the world’s largest installed capacity and setting the competitive tone for all downstream industries reliant on Rare Earth Metals.

United States: National Security-Driven Rare Earth Processing and Multi-Partner Supply Chain Diversification

The U.S. approach to strengthening the domestic Rare Earth Metals supply chain is centered on de-risking defense, aerospace, and semiconductor manufacturing. The 2025 USGS Critical Minerals List expanded to 60 minerals—highlighting dysprosium, neodymium, and terbium as strategic vulnerabilities with the potential for major economic disruption. Federal emphasis on supply chain resilience has intensified investment in the National Defense Stockpile, ensuring adequate buffer reserves for high-purity rare earth oxides and metals critical for guidance systems, jet propulsion, advanced sensors, and precision munitions.

To reinforce processing capacity—historically the weakest link in the U.S. rare earth value chain—the Department of Energy committed $134 million to domestic separation and refining projects capable of producing magnet-grade NdPr and heavy rare earth elements. These initiatives complement new international partnerships with Australia, Japan, and Malaysia, each designed to foster non-Chinese refining capacity and facilitate long-term feedstock diversification. As geopolitical strains persist, the U.S. continues to pursue end-to-end rare earth autonomy, from mining and hydrometallurgy to magnet qualification, marking one of the largest strategic industrial repositionings in the global Rare Earth Metals Market.

Australia: Integrated Rare Earth Mining-to-Separation Expansion Strengthening Global Non-Chinese Supply Capacity

Australia continues to emerge as the world’s most important non-Chinese rare earth alternative, supported by large-scale reserves, advanced processing projects, and strong government policy alignment. The proposal for an A$1.2 billion strategic minerals reserve—crafted with potential U.S. collaboration—signals Canberra’s intention to position rare earths as a sovereign industrial asset. The Nolans Project by Arafura Rare Earths exemplifies Australia's shift from simple ore exports to a fully integrated extraction, separation, and processing ecosystem, with a planned 30-year mine life and the capability to supply NdPr oxide essential for EV traction motors and wind turbines.

Policies under the Critical Minerals Strategy 2023–2030 and the Future Made in Australia initiative reinforce downstream ambitions, including magnet manufacturing, oxide upgrading, and metallization capacity. Complementing industrial development, Australia's CSIRO is pioneering new recovery pathways, including advanced hydrometallurgical processes and magnet recycling systems capable of reclaiming 3,000–5,000 tonnes annually. The result is a rapidly expanding rare earth value chain geared toward reducing Western reliance on Chinese refining while supporting global electrification demand.

Japan: Global Leader in Heavy Rare Earth Reduction, Closed-Loop Recycling, and Advanced Magnet Innovation

Japan remains at the forefront of Rare Earth Permanent Magnet (REPM) innovation, particularly in reducing dependence on Heavy Rare Earth Elements (HREEs) such as dysprosium and terbium. At the REPM2025 international workshop, Japan’s National Institute for Materials Science (NIMS) revealed breakthroughs in dysprosium-free and HREE-lean magnet chemistries, including advanced grain boundary diffusion techniques that significantly reduce HREE consumption while maintaining high coercivity—critical for EV traction motors operating under thermal stress.

Japan’s leadership extends into rare earth recycling, where it maintains the world’s most sophisticated ecosystem for recovering Nd, Pr, Dy, and Tb from end-of-life electronics, including hard drives, motors, and HVAC systems. This closed-loop infrastructure supports Japan’s automotive and electronics sectors, reducing exposure to volatile global supply. Automotive OEMs and magnet makers are investing in next-generation, high-performance magnets optimized for miniaturized EV drivetrains. Through its recycling strength, materials research sophistication, and magnet-processing expertise, Japan remains a crucial innovation hub in the Rare Earth Metals Market.

Europe (Estonia / EU): Onshoring Rare Earth Magnet Manufacturing to Achieve Strategic Autonomy Under CRMA

Europe made a major leap toward supply chain independence with the September 2025 launch of its largest rare earth magnet plant in Narva, Estonia—developed by Neo Performance Materials and backed by €14.5 million from the EU’s Just Transition Fund. This facility directly supports the EU’s Critical Raw Materials Act (CRMA), which mandates the reduction of European dependency on Chinese magnet imports (currently exceeding 90%). With an initial capacity of 2,000 tonnes annually, scalable to 5,000 tonnes, the Narva plant has the potential to supply magnets for more than one million EVs per year, significantly bolstering Europe’s electrification infrastructure.

The plant marks the EU’s first serious move toward establishing a domestic, integrated rare earth magnet production chain, from NdPr metal feedstock to finished magnets for EVs, wind turbines, robotics, and defense technologies. The project is expected to catalyze additional investments across upstream separation facilities and downstream EV and wind supply chains. As Europe commits to large-scale sustainability transitions, securing domestic REPM manufacturing becomes a foundational element of long-term industrial resilience.

India: PLI-Backed Rare Earth Permanent Magnet Manufacturing to Build a Self-Sufficient EV Supply Chain

India’s rare earth strategy has shifted rapidly toward self-reliance, marked by the November 2025 approval of a ₹7,280 crore PLI Scheme dedicated exclusively to Sintered Rare Earth Permanent Magnet (REPM) manufacturing. This groundbreaking initiative targets the creation of 6,000 MTPA of integrated magnet capacity, covering oxide conversion, alloying, and final magnet production—effectively establishing India’s first complete REPM value chain. These magnets are essential inputs for electric vehicles, robotics, consumer electronics, and renewable energy technologies.

The scheme includes ₹6,450 crore in sales-linked incentives and ₹750 crore in capital support, offering financial momentum for up to five leading firms. This policy aligns squarely with India’s broader EV manufacturing ambitions, reinforcing the value chain for motors, drivetrains, and grid-scale renewable systems. With strong state and central support, India is positioning itself as a competitive production base for rare earth magnets while reducing strategic vulnerabilities tied to imports of NdFeB components.

Vietnam: Emerging Rare Earth Processing Competitor Through New Legal Framework and Resource Nationalism

Vietnam is stepping into the spotlight of the global Rare Earth Metals Market through its new Rare Earth Legal Framework, designed to restructure licensing, strengthen environmental compliance, and promote domestic value addition rather than exporting raw concentrates. This regulatory shift signals Vietnam’s intention to evolve from a major ore holder into a refining and deep-processing center, supporting national industrialization goals.

The strategy reflects a broader trend toward resource nationalism, where Vietnam seeks to control foreign participation, ensure sustainable extraction, and capture higher economic value from downstream processes like separation, oxide production, and magnet precursors. With substantial reserves—reportedly among the largest outside China—Vietnam is increasingly recognized as a future strategic alternative for global supply diversification, particularly for NdPr oxide and midstream processing.

Competitive Landscape: Global Rare Earth Metals Producers and Vertical Integration Strategies

The competitive landscape of the Rare Earth Metals Industry is increasingly defined by vertical integration (mine-to-magnet), regional supply security, and the ability to process both LREE and HREE feedstock at scale. While Chinese state-aligned groups still dominate global rare earth oxide and metal supply, a new cohort of non-Chinese players in the U.S. and Australia are building out separation, metal, and magnet production to reduce geopolitical exposure. For OEMs and magnet vendors, partnering with producers that combine secure upstream feedstock, midstream separation technology, and downstream alloy/magnet capabilities is becoming a key procurement strategy. At the same time, specialized companies like Iluka and Ucore are targeting midstream bottlenecks—especially HREE separation and advanced solvent extraction alternatives—to unlock additional, non-Chinese capacity.

MP Materials Corp. (USA): MP Materials accelerates U.S. mine-to-magnet integration

MP Materials is the cornerstone of the U.S. rare earth metals strategy, leveraging its Mountain Pass deposit to progress from concentrate production toward a fully integrated mine-to-magnet business model. The company now produces NdPr oxide and, from January 2025, began NdPr metal production in Fort Worth, Texas, with an initial target of 1,000 tpa to feed domestic NdFeB magnet manufacturing. In July 2025, MP Materials secured a landmark partnership with the U.S. Department of Defense, which includes a price floor of USD 110/kg for NdPr and a commitment to procure 100% of magnets produced at the Texas facility—insulating the company from extreme price volatility. By Q3 2025, MP had stopped selling low-margin concentrates to Chinese customers, signaling full strategic alignment around higher-value alloys and magnets. This integrated strategy positions MP Materials as a pivotal supplier for EV, wind, and defense OEMs seeking non-Chinese, secure rare earth magnet supply.

Lynas Rare Earths Ltd. (Australia): Lynas expands non-Chinese NdPr and HREE separation capacity

Lynas Rare Earths is currently the only large-scale integrated rare earth producer outside China, operating the Mt Weld mine in Australia and a major processing facility in Gebeng, Malaysia. The company supplies NdPr oxide, as well as dysprosium and terbium-containing streams, making it crucial for non-Chinese HREE availability. In October 2025, Lynas announced an A$180 million expansion of its Malaysian facility to add up to 5,000 tonnes per year of heavy rare earth separation capacity, significantly easing a key bottleneck in global HREE processing. First production of Samarium from Mt Weld feedstock at the expanded facility is projected around April 2026, further diversifying non-Chinese REE output. Lynas’ ability to deliver both LREE and HREE products at scale positions it as a preferred partner for magnet producers targeting China-plus-one sourcing strategies.

China Northern Rare Earth (Group) High-Tech Co., Ltd.: China Northern Rare Earth maintains LREE cost leadership

China Northern Rare Earth is the dominant producer of light rare earth elements (LREEs) within China’s state-controlled system, drawing primarily on the giant Bayan Obo deposit. The company’s core products include Neodymium, Praseodymium, Lanthanum, and Cerium, which form the backbone of global NdPr oxide supply for permanent magnets. With decades of process optimization and massive production scale, China Northern Rare Earth maintains some of the lowest NdPr oxide production costs worldwide, giving it significant pricing power in the LREE market. Its close coordination with Chinese industrial policy and vertically integrated domestic customers ensures stable demand for its oxides and metals. As export controls tighten and quotas remain binding, China Northern Rare Earth will continue to be a central price-setting force in the global rare earth metals market, especially for magnet-grade LREEs.

China Minmetals Rare Earth Co., Ltd.: China Minmetals Rare Earth consolidates heavy rare earth supply

China Minmetals Rare Earth specializes in heavy rare earth elements (HREEs) such as dysprosium, terbium, and yttrium, which are critical dopants for high-temperature NdFeB magnets used in EV traction motors and aerospace systems. Operating under a central government-controlled group, the company has been at the forefront of consolidating smaller ion-adsorption clay operations into a more tightly regulated HREE sector. This consolidation allows Minmetals Rare Earth to better control HREE production volumes, environmental compliance, and pricing, protecting the strategic value of Dy and Tb. Its role as a state-aligned HREE champion means it sits at the center of policies like the October 2025 export controls, giving it substantial influence over the availability of high-temperature magnet materials to foreign customers. For global OEMs, this raises the urgency of securing non-Chinese HREE sources or adopting magnet designs that minimize Dy/Tb content.

Iluka Resources Limited (Australia): Iluka leverages mineral sands to enter rare earth refining

Iluka Resources is evolving from a mineral sands producer into a key rare earth feedstock and midstream player. Its core strength lies in producing monazite concentrate—a REE-rich mineral co-produced with zircon and rutile—from its established sands operations. Recognizing the strategic value of this feedstock, Iluka secured substantial Australian government funding in May 2024 to build the Eneabba Rare Earth Refinery, which will move the company into rare earth separation for both LREE and HREE streams. This vertical expansion allows Iluka to transform an existing resource base into NdPr and HREO products, contributing to a diversified, non-Chinese supply chain. By integrating mining, concentrating, and separation, Iluka is positioned to become a foundational supplier of rare earth oxides to magnet manufacturers in Asia, Europe, and North America seeking alternative, ESG-compliant sources.

Ucore Rare Metals Inc. (Canada): Ucore advances RapidSX technology for North American REE separation

Ucore Rare Metals is focused on solving the midstream separation bottleneck in the North American rare earth metals value chain. Its strategy centers on the planned Alaska Strategic Metals Complex and the deployment of its proprietary RapidSX™ separation technology, which is designed to offer faster, more cost-effective, and environmentally compliant separation of both LREEs and HREEs. By targeting separation rather than mining alone, Ucore aims to process feedstock from multiple sources into high-purity REE oxides and metals, supporting downstream NdFeB magnet and alloy production in North America. The company is strategically aligned with government and defense objectives to build a fully integrated domestic rare earth supply chain that is less exposed to geopolitical disruption. If successfully scaled, RapidSX could become a critical differentiator in securing regional supply of both NdPr and key HREEs for EVs, wind turbines, and defense applications.

Rare Earth Metals Market Report Scope

Rare Earth Metals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.7 Billion

|

|

Market Size (2035)

|

$94 Billion

|

|

Market Growth Rate

|

14.3%

|

|

Segments

|

By Rare Earth Group (Light Rare Earth Elements, Heavy Rare Earth Elements), By Product Form (Rare Earth Oxides, Rare Earth Metals & Alloys, Rare Earth Permanent Magnets, Polishing Compounds, Catalyst Materials), By Purity Grade (3N, 4N, 5N), By End-Use Application (Permanent Magnets, Automotive Catalysts, Precision Polishing, Metallurgy & Alloying, Electronics & Lighting)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

China Northern Rare Earth Group, China Minmetals Rare Earth, Shenghe Resources, MP Materials, Lynas Rare Earths, Neo Performance Materials, Hitachi Metals, Shin-Etsu Chemical, Vacuumschmelze (VAC), Treibacher Industrie, Galanos Group, Arafura Rare Earths, IREL India, Hastings Technology Metals, Greenland Minerals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rare Earth Metals Market Segmentation

By Rare Earth Group

- Light Rare Earth Elements (LREE)

- Heavy Rare Earth Elements (HREE)

By Product Form

- Rare Earth Oxides (REOs)

- Rare Earth Metals & Alloys

- Rare Earth Permanent Magnets (NdFeB, SmCo)

- Polishing Compounds

- Catalyst Materials

By Purity Grade

- 3N (≥99.9%)

- 4N (≥99.99%)

- 5N (≥99.999%)

By End-Use Industry

- Permanent Magnets

- Automotive Catalysts

- Precision Polishing

- Metallurgy & Alloying

- Electronics & Lighting

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Rare Earth Metals Market

- China Northern Rare Earth Group

- China Minmetals Rare Earth

- Shenghe Resources

- MP Materials

- Lynas Rare Earths

- Neo Performance Materials

- Hitachi Metals

- Shin-Etsu Chemical

- Vacuumschmelze (VAC)

- Treibacher Industrie

- Galanos Group

- Arafura Rare Earths

- IREL India

- Hastings Technology Metals

- Greenland Minerals

*- List not Exhaustive

Research Coverage: Rare Earth Metals Market

This USDAnalytics report investigates the rapidly evolving Rare Earth Metals Market under a tightly managed supply regime, delivering in-depth analysis reviews of demand for NdPr, Dy, Tb and other key oxides across EV traction motors, direct-drive wind turbines, industrial drives, catalysts, polishing, and advanced ceramics. It highlights how export controls, production quotas, and processing concentration are reshaping mine-to-magnet strategies, pricing benchmarks, and long-term offtake structures, while examining breakthroughs in heavy rare earth reduction, magnet microstructure engineering, and large-scale recycling technologies. The study maps policy-driven shifts in the U.S., Europe, China, Australia, Japan, India, and emerging Asian producers, assesses capital flows into non-Chinese separation and magnet manufacturing, and quantifies the competitive positioning of integrated players across the value chain. By combining granular supply–demand modelling with scenario-based risk assessment on security of supply, technology substitution, and circular flows, this report is an essential resource for OEMs, magnet manufacturers, investors, and policymakers seeking data-backed insights into the strategic trajectory of the global Rare Earth Metals Market.

Scope Highlights

- Segmentation:

By Rare Earth Group – Light Rare Earth Elements (LREE) and Heavy Rare Earth Elements (HREE).

By Product Form – Rare Earth Oxides (REOs); Rare Earth Metals & Alloys; Rare Earth Permanent Magnets (NdFeB, SmCo); Polishing Compounds; Catalyst Materials.

By Purity Grade – 3N (≥99.9%); 4N (≥99.99%); 5N (≥99.999%).

By End-Use Industry – Permanent Magnets; Automotive Catalysts; Precision Polishing; Metallurgy & Alloying; Electronics & Lighting.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ companies across mining, separation, metals & alloys, and permanent magnet manufacturing portfolios.