Market Overview: High-Performance Permanent Magnets Enabling EVs and Renewables

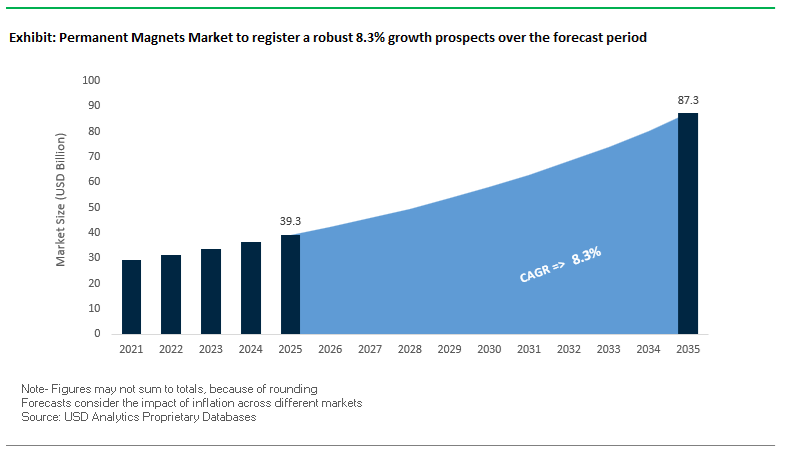

The Permanent Magnets Market is projected to grow from USD 39.3 billion in 2025 to USD 87.2 billion by 2035, registering a strong CAGR of 8.3% (2025–2035). This expansion is tightly linked to the rapid deployment of EV traction motors, offshore wind turbines, and high-efficiency industrial drives, where NdFeB permanent magnets and ferrite magnets are critical for compact, high-torque designs. For magnet manufacturers, OEMs, and material suppliers, the market is increasingly defined by energy density, thermal stability, and rare earth supply security, with an active shift toward HREE-optimized or HREE-free permanent magnet solutions. Vendors that can combine high energy product grades (N52 and above) with secure rare earth sourcing and recycling capabilities are best positioned to capture the next wave of electrification and renewable energy demand.

Key insights for permanent magnet manufacturers and OEMs

- High energy density benchmark: High-grade sintered NdFeB permanent magnets (e.g., N52) deliver a maximum energy product up to 55 MGOe, enabling motor designs up to 70% smaller and lighter than legacy magnet technologies—crucial for high-efficiency EV traction motors and compact industrial drives.

- Ferrite magnets for high-temperature stability: Ferrite permanent magnets exhibit a positive intrinsic coercivity temperature coefficient (~+0.27%/°C), meaning their resistance to demagnetization improves with temperature, supporting reliable operation at ~300°C in motors and generators used in harsh environments.

- Heavy rare earth dependency at high temperatures: High-performance NdFeB magnets for hybrid vehicle motors and direct-drive wind turbines often require dysprosium (Dy) or terbium (Tb) to maintain coercivity up to 200°C, making HREE supply risk a central strategic issue for the permanent magnets industry.

- Magnet intensity in renewable systems: Large permanent magnet synchronous generators (PMSGs) for offshore wind can incorporate over 3 metric tons of NdFeB magnets per turbine, underlining how renewable energy growth directly translates into strong volume demand for rare earth permanent magnets.

Market Analysis: Policy Shifts, Capacity Expansion, and Material Innovation

The global Permanent Magnets Market is being reshaped by parallel forces of electrification, policy intervention, and material innovation. In November 2024, global EV motor production reached 22.9 million units, with permanent magnet synchronous motors (PMSMs) representing the majority of these drives, sharply increasing demand for NdFeB traction motor magnets. On the renewable energy side, Siemens Gamesa’s 15 MW offshore wind turbine, launched in May 2024, uses high-performance neodymium magnets in a direct-drive generator, reinforcing the role of large PMSGs as a structural demand pillar for NdFeB. At the same time, European policy under the Critical Raw Materials Act (October 2025) aims to secure at least 10% domestic extraction of critical raw materials by 2030, including rare earths, pushing OEMs and magnet producers to diversify supply chains beyond China and accelerate investment in European magnet and rare earth processing capacity.

On the supply and technology side, China and Western suppliers are taking divergent but complementary routes. In August 2025, a major Chinese magnet producer announced an approximately USD 150 million capacity expansion for sintered NdFeB, targeting rising demand from industrial automation, robotics, and EVs, reinforcing China’s position as the largest source of NdFeB magnet capacity. Conversely, VACUUMSCHMELZE (VAC) introduced VACODYM 902 TP in September 2025, a heavy rare earth-free NdFeB alloy manufactured entirely in the Western Hemisphere, directly addressing HREE risk and regional supply security. At the same time, researchers reported a breakthrough in April 2025 on rare earth-free permanent magnets based on manganese–gallium (MnGa) with properties approaching NdFeB at 150°C, suggesting early-stage pathways for future magnet chemistries that could partially decouple performance magnets from rare earth constraints.

The competitive and strategic landscape is also evolving through M&A and sustainability initiatives. In November 2025, Arnold Magnetic Technologies completed the acquisition of a rare earth magnet processing firm, consolidating its capabilities in high-performance magnet assemblies for aerospace and defense, where reliability at extreme temperatures is paramount. Meanwhile, collaborations announced in December 2025 among leading magnet manufacturers are focused on new chemical processes for recycling NdFeB magnets from end-of-life wind turbines, linking circularity with long-term rare earth supply security. This aligns with broader moves toward closed-loop magnet recycling and lower embedded carbon footprints, which are increasingly required by automotive OEMs and wind developers in their sustainability-linked procurement criteria. Together, these developments position the Permanent Magnets Industry at the intersection of advanced materials, geopolitics, and net-zero investment cycles.

Strategic Trends and High-Impact Opportunities Defining the Next Generation of Permanent Magnet Technologies

Market Trend 1: Vertical Mine-to-Magnet Integration Intensifies as Countries Move to Reduce NdFeB Supply Chain Dependency

One of the most defining shifts in the permanent magnets market is the accelerated push toward fully integrated mine-to-magnet supply chains, driven by the extreme concentration of Rare Earth Element (REE) processing in China. With China controlling 90%–91% of global REE separation and refining capacity, the midstream “oxide bottleneck” represents the most significant geopolitical risk for NdFeB magnet manufacturing. This bottleneck directly impacts global access to Neodymium (Nd) and Praseodymium (Pr), the fundamental REEs used in high-performance NdFeB magnets.

Compounding this challenge is China’s dominance in finished magnet production. The country is responsible for 93%–94% of global sintered permanent magnet output, including magnets critical for electric vehicles (EVs), industrial motors, and wind turbines. As a result, Western economies and advanced manufacturing hubs are rapidly mobilizing investment toward domestic processing, metalmaking, and magnet sintering capacity. The strategic objective is to reduce near-total dependency on China and build a resilient, regionally diversified NdFeB magnet manufacturing ecosystem.

This trend is further reinforced by national security considerations, rapid EV market growth, and stringent renewable energy targets, each of which requires stable access to high-performance magnet materials. The long-term structural shift toward vertical integration will redefine global supply chain configurations, cost structures, and technology partnerships.

Market Trend 2: Grain Boundary Diffusion (GBD) Accelerates as a Core Method for Reducing Heavy Rare Earth (HRE) Consumption

A second profound trend reshaping the permanent magnets landscape is the rapid industrial adoption of Grain Boundary Diffusion (GBD) technology to lower dependence on expensive Heavy Rare Earth elements (HREEs)—primarily Dysprosium (Dy) and Terbium (Tb). These elements are essential for improving the high-temperature performance of NdFeB magnets, but they are expensive, supply-constrained, and geographically concentrated.

GBD technology enables manufacturers to reduce Dy/Tb consumption by 40%–70% compared to uniform alloying, while still achieving equal or superior magnetic performance. The diffusion introduces Dy/Tb selectively at grain boundaries—precisely where coercivity enhancement is most effective. This localized addition can increase intrinsic coercivity (Hcj) by up to 60%, significantly improving the magnet’s resistance to demagnetization.

A key advantage is that GBD improves high-temperature stability. For example, one NdFeB grade showed a thermal coefficient of coercivity improvement from –0.55%/°C to –0.48%/°C, meaning GBD-treated magnets lose less coercivity at elevated operating temperatures such as 150°C. Importantly, unlike traditional HRE alloying, GBD enhances coercivity without reducing remanence (Br). This positions GBD as the leading engineering solution for producing high-performance magnets while dramatically lowering HRE cost exposure.

Market Opportunity 1: Accelerated Commercialization of MnBi and MnAlC Magnets for Mid-Temperature and Cost-Sensitive Applications

A major commercial opportunity is emerging around manganese-based permanent magnets, especially MnBi and MnAlC, as industries seek REE-free alternatives for applications not requiring the extreme power density of NdFeB. MnBi’s unique thermal behavior is particularly attractive—it exhibits a positive temperature coefficient of coercivity (dHcj/dT > 0) below 300°C. This means that as temperature rises, MnBi becomes more coercive, unlike NdFeB, which weakens at elevated temperatures.

MnBi maintains stable coercivity up to approximately 200°C, making it suitable for sensors, actuators, industrial motors, and automotive components operating in mid-temperature environments. While its maximum energy product (BHmax) of 20–25 MGOe is lower than the 40–50 MGOe typical of NdFeB, the combination of thermal resilience, cost advantages, and reduced supply chain risk makes MnBi highly competitive for targeted applications.

MnBi also possesses a theoretical density about 20% higher than NdFeB, an attribute that influences magnet geometry and motor design but opens pathways to higher volumetric efficiency. As industries pursue diversification away from heavily constrained REE supply chains, MnBi and MnAlC alloys represent the most commercially viable non-REE magnet families on the near-term horizon.

Market Opportunity 2: Creation of High-Purity Closed-Loop Recycling Ecosystems for NdFeB Magnet Recovery

A second major opportunity lies in building a closed-loop recycling framework capable of recovering Nd, Pr, Dy, and Tb from end-of-life NdFeB magnets. Hard Disk Drives (HDDs), in particular, are a high-quality scrap source; a single 3.5-inch HDD contains approximately 17.87 g of NdFeB magnet mass. With enterprise HDD recycling programs achieving collection efficiencies as high as 90%, this represents an extraordinary reservoir of secondary REEs.

Advanced extraction technologies are achieving high recovery performance. Liquid Metal Extraction (LME) using magnesium can produce Nd sponge with 95%–98% purity, suitable for reprocessing into magnet alloys. Direct recycling pathways such as sintering-grade powder recovery also preserve magnetic microstructure, enabling the recreated magnets to maintain high performance.

Given that NdFeB magnets contain roughly 20% REEs by weight, scrap magnet feedstock offers a higher-grade REE concentration than natural ores, making recycling an economically compelling and environmentally critical pathway. Establishing a global, industrial-scale closed-loop system will significantly reduce dependency on primary mining and strengthen supply stability for EVs, robotics, renewable energy, and industrial automation.

Permanent Magnets Market Share Analysis

Market Share by Material Type: NdFeB Magnets Dominate Through Highest Energy Density and Electrification Demand

Neodymium-Iron-Boron (NdFeB) Permanent Magnets hold the largest share of the global permanent magnets market—approximately 55%—because their superior magnetic energy density makes them fundamentally irreplaceable in high-performance, compact, and energy-efficient systems. NdFeB magnets exhibit the highest BHmax (maximum energy product) of any commercial magnet material, enabling engineers to design significantly smaller and lighter motors, actuators, and electronic components without sacrificing torque or power output. This performance advantage is crucial in rapidly expanding markets such as electric vehicle (EV) traction motors, where NdFeB’s outstanding power-to-weight ratio directly increases vehicle range and reduces energy losses. The segment also benefits from the widespread adoption of NdFeB magnets in direct-drive wind turbines, robotics, industrial automation equipment, and high-end consumer electronics. Sintered NdFeB—recognized as the strongest grade—accounts for the majority of this segment’s revenue due to its high intrinsic coercivity and thermal stability. Although Ferrite magnets dominate on a volume basis, the strategic importance and high value of NdFeB magnets in electrification, renewable energy, and miniaturized electronics ensure their commanding position in market share and revenue contribution.

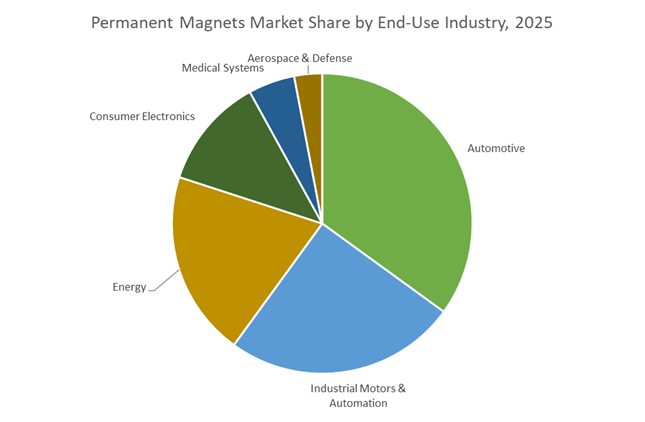

Market Share By End-Use Industry: Automotive Sector Leads Due to EV Traction Motor Intensification

The Automotive sector represents the largest end-use share in the global permanent magnets market—approximately 35%—driven extensively by the rapid global acceleration of electric vehicle manufacturing. Permanent magnets, particularly NdFeB types, are indispensable for EV traction motors, where efficiency, torque density, and compactness directly define battery range and drivetrain performance. Unlike traditional internal combustion engine (ICE) vehicles that use minimal magnet content (≈0.1 kg), modern battery electric vehicles require 1 to 5 kilograms of NdFeB magnets across the traction motor and auxiliary subsystems, including pumps, cooling systems, electric power steering (EPS), HVAC modules, and advanced sensors. The automotive industry’s transition toward magnet-intensive architectures for hybrid electric vehicles (HEVs) and BEVs magnifies this demand, with EV traction motors often achieving efficiencies exceeding 95% due to rare-earth magnet technology. Beyond propulsion, the rise of ADAS, autonomous driving modules, and increasingly electrified vehicle platforms further increases magnet dependence. Market projections consistently show the automotive segment emerging as the single largest consumer of high-strength rare earth magnets, validating its dominant share and reinforcing its central role in shaping global demand trajectories for permanent magnet materials.

Country Analysis: Global Strategic Power Centers Shaping the Permanent Magnets Market

China: Export-Control Power, NdFeB Production Dominance, and Technology Scaling for NEVs

China remains the most influential global force in the Permanent Magnets Market, reinforced by unmatched refining, alloy-making and NdFeB magnet manufacturing capacity. With over 90% of global sintered NdFeB production, China controls virtually the entire value chain—from rare earth mining and chemical separation to alloy processing, powder metallurgy, and finished magnet machining. This structural dominance gives China significant leverage over the global electric mobility and electronics industries, which depend on high-performance permanent magnets for motors, sensors, and precision components.

China’s April 2025 export controls on selected rare earth magnets signal a strategic tightening of supply that immediately drove international magnet buyers to pay 2x–4x premiums for non-Chinese Dysprosium Oxide and heavy rare earth supplies. These policy moves, paired with declining imports of heavy rare earth feedstock from Myanmar in 2025, underscore an increasingly protectionist posture designed to preserve domestic supply for New Energy Vehicle (NEV) expansion and high-tech manufacturing. Chinese manufacturers are also upgrading production lines with advanced strip-casting, hydrogen decrepitation, and powder processing to deliver high-coercivity NdFeB grades required for robotics, wind turbines, and EV traction motors, reinforcing China’s technological and economic leadership in the Permanent Magnets Market.

India: REPM Mega-Scheme and Integrated Magnet Manufacturing for EV and Renewable Energy Independence

India has entered a transformative phase in the Permanent Magnets Market with the approval of a ₹7,280-crore Rare Earth Permanent Magnet (REPM) Manufacturing Scheme in November 2025. This landmark initiative aims to build 6,000 MTPA of fully integrated domestic capacity—covering the entire chain from rare earth oxide → metal → alloy → finished permanent magnets. With a current dependency of nearly 90% on Chinese magnet imports, the scheme marks India’s most significant strategic intervention to date in securing magnet supply for electric vehicles, wind turbines, industrial automation, medical devices, and defence platforms.

The programme allocates ₹6,450 crore in sales-linked incentives and ₹750 crore in capital subsidy to five major beneficiaries, ensuring large-scale industrialization of NdFeB, SmCo, and bonded magnets within India. This policy is tightly aligned with national goals in EV localization, renewable energy capacity expansion, and defence indigenization. As India accelerates its transition to EV manufacturing under the PLI-Auto scheme and expands wind turbine installations domestically, the REPM scheme positions the country to become a significant regional supplier of high-performance permanent magnets.

United States: Domestic Supply Chain Rebuilding, Magnet Recycling Scale-Up, and Federal Funding Infusion

The United States is intensifying its push to decouple its magnet supply chain from China through a combination of federal funding, strategic recycling initiatives, and investments in rare earth separation. In November 2025, the Department of Defense (DoD) issued a $150 million loan guarantee to strengthen U.S.-based rare earth separation and magnet manufacturing capabilities. This complements Department of Energy (DOE) funding directed at establishing refining, metalizing, and alloying operations essential for producing NdFeB and SmCo magnets domestically.

One of the most notable developments is the country’s strong emphasis on Hydrogen Processing of Magnet Scrap (HPMS), which enables efficient recovery of critical elements such as Neodymium (Nd), Dysprosium (Dy) and Terbium (Tb) from end-of-life EV motors, hard drives, and industrial equipment. The U.S. is hoping to convert large-scale magnet recycling into a strategic buffer against foreign supply disruptions. As EV adoption accelerates and electrification drives demand for high-efficiency motors, the U.S. is reinforcing its position as a critical innovation hub for rare earth recycling, magnet reprocessing, and low-carbon magnet manufacturing technologies.

European Union/Germany: CRMA-Driven Circularity, Non-Rare Earth Magnet R&D, and Recycling Commercialization

Europe—particularly Germany—is rapidly reshaping its rare earth and permanent magnet ecosystem through policy enforcement under the Critical Raw Materials Act (CRMA), adopted in 2023. The CRMA sets clear strategic targets for domestic refining, sustainable mining, and mandatory recycling, aiming to reduce Europe’s 90%+ import dependency on Chinese REPMs. This regulatory environment has spurred major industrial and research initiatives focused on hydrometallurgical, electrochemical, and direct recycling methods for recovering rare earth elements from scrap magnets.

The EU is also investing heavily in alternative magnet chemistries. Collaborative research projects are revisiting Manganese Aluminum Carbide (MnAlC) and high-performance Iron Nitride (α′′-Fe₁₆N₂) as potential replacements for NdFeB magnets in motors and robotics applications, especially in segments requiring high energy product but reduced rare earth intensity. Germany’s strong automotive base accelerates this innovation, as OEMs seek permanent magnet technologies that meet both performance requirements and strict sustainability mandates. As circular magnet manufacturing scales in Europe, the region is emerging as a strategic counterweight to Asian supply concentration.

Japan: Grain Boundary Diffusion (GBD) Mastery and Magnet-to-Magnet Recycling for High-Coercivity NdFeB

Japan continues to lead global innovation in high-performance permanent magnets through advancements in Grain Boundary Diffusion (GBD), a technique that significantly reduces heavy rare earth usage while achieving exceptional coercivity and thermal stability. Japanese companies have perfected diffusion processes enabling magnets to maintain performance in high-temperature environments, critical for EV traction motors, industrial robotics, and aerospace applications.

Japan is also a pioneer in direct magnet-to-magnet recycling, which bypasses complex chemical separation and instead reprocesses sintered magnets directly into new powder feedstock. This approach delivers substantial reductions in waste, cost, and reliance on imported rare earth oxides. With its strong automotive and industrial electronics sectors, Japan’s progress in HREE-efficient NdFeB magnets positions it as a global center for sustainable, high-performance magnet technology.

South Korea: HREE-Free Magnet Innovations and Integration into High-Efficiency EV Motors

South Korea is emerging as a pivotal innovation hub for heavy rare earth-free (HREE-free) permanent magnets and high-efficiency motor technologies. The Korea Institute of Materials Science (KIMS) achieved a major breakthrough through a two-step GBD process that enables the production of high-performance magnets without Dysprosium or Terbium—elements facing severe supply risks and price volatility.

This innovation aligns with the needs of South Korea’s EV manufacturers, who are aggressively deploying high-efficiency Permanent Magnet Synchronous Motors (PMSMs) designed for compact architectures and high power density. As Korean automakers expand globally with 800V charging EV platforms, the demand for thermally stable, high-coercivity NdFeB magnets is accelerating, driving further material R&D and integration of advanced, HREE-lean magnet systems across mobility and home appliance sectors.

Competitive Landscape: Rare Earth Magnet Leaders and Supply Chain Strategies

The global Permanent Magnets Market is highly concentrated among a group of Japanese, European, American, and Chinese players that combine materials science expertise, rare earth processing, and magnet assembly capabilities. Competitive differentiation hinges on grain boundary engineering, coercivity at high temperatures, heavy rare earth optimization, and vertical integration from rare earth oxides to finished magnet assemblies. Companies that can offer high-performance NdFeB grades, ferrite alternatives, and rare-earth-free R&D pipelines, while managing multi-regional production footprints, are best positioned to support fast-growing segments such as EV traction motors, wind turbines, industrial automation, robotics, and aerospace drives.

Shin-Etsu Chemical focuses on globally integrated rare earth magnet supply

Shin-Etsu Chemical is a leading provider of rare earth NdFeB magnets for automotive and industrial use, underpinned by an integrated supply chain that spans from rare earth separation and refinement to sintered magnet production. The company’s strategy is to secure high-performance NdFeB magnets by controlling key upstream steps, which helps manage quality, cost, and rare earth availability for major OEMs. Shin-Etsu has established overseas production bases in 17 countries, creating a highly diversified and resilient manufacturing footprint that mitigates geopolitical and logistics risk for global automotive and industrial customers. This global supply system allows the company to deliver magnets tailored to EV traction motors, industrial drives, and consumer electronics with consistent performance. By coupling materials R&D with regional application engineering, Shin-Etsu strengthens its position as a cornerstone supplier in the Permanent Magnets Market.

Proterial (Hitachi Metals) pushes NEOMAX® high-heat NdFeB magnet technology

Proterial, Ltd. (formerly Hitachi Metals) is renowned for its NEOMAX® high-performance NdFeB magnets as well as ferrite and specialty magnet alloys, positioning it as a key technology provider for premium EV traction motors and industrial machinery. The company’s R&D strategy centers on proprietary grain boundary diffusion technologies that dramatically boost coercivity at elevated temperatures, enabling NdFeB magnets to operate reliably in high-heat environments such as hybrid vehicle motors. Proterial also invests heavily in digital manufacturing and AI-driven process control to optimize sintering and heat treatment, delivering tight property distributions across high-performance magnet grades. This digitalization focus enhances yield, quality, and traceability, which are crucial for automotive and aerospace qualification. By offering a full lineup of NEOMAX® and ferrite solutions, Proterial addresses both performance-critical and cost-sensitive permanent magnet applications.

VACUUMSCHMELZE (VAC) delivers Western heavy rare earth-free NdFeB solutions

VACUUMSCHMELZE GmbH & Co. KG (VAC) is a European specialist in NdFeB (VACODYM®) and samarium cobalt (VACOMAX®) magnets, with strong capabilities in complex magnet assemblies for aerospace, energy, and industrial customers. With the launch of VACODYM 902 TP, a heavy rare earth-free NdFeB alloy manufactured entirely in the Western Hemisphere, VAC is directly addressing customer concerns around HREE availability and regional supply dependence. The company combines magnet alloy development with finite element analysis (FEA)-based magnetic circuit design, enabling optimized permanent magnet assemblies for high-speed motors, generators, and precision sensors. VAC’s integrated approach—from alloy production through to assembled sub-systems—allows it to serve demanding markets where thermal stability, demagnetization resistance, and long service life are crucial. This positions VAC as a key partner for OEMs seeking secure, non-Asian NdFeB magnet supply.

TDK Corporation leverages magnet portfolio for automotive and ICT growth

TDK Corporation maintains a broad portfolio of neodymium (NdFeB), ferrite (hard ferrite), and rare-earth-free magnets, supporting a wide range of automotive and ICT applications. The company’s strategic focus is on supplying high-quality magnets for small motors, actuators, and sensors used in vehicles, consumer electronics, and communication devices. TDK actively invests in improving ferrite magnet performance and developing rare-earth-free alternatives, helping customers reduce dependency on critical rare earths while controlling costs. Its strong integration with electronic components and modules allows TDK to design magnets optimized for system-level performance in compact assemblies. By combining material innovation with a deep understanding of automotive and ICT miniaturization trends, TDK remains a pivotal player in the Permanent Magnets Industry, particularly on the high-volume, small-form-factor side of the market.

Arnold Magnetic Technologies targets aerospace, defense, and high-speed motors

Arnold Magnetic Technologies operates across sintered NdFeB, Alnico, SmCo, and flexible magnets, with a pronounced emphasis on aerospace, defense, and high-speed motor applications. The company’s core strength lies in delivering magnet and magnetic assemblies that can withstand extreme temperatures, high rotational speeds, and stringent reliability requirements. In November 2025, Arnold completed the acquisition of a rare earth magnet processing firm, which deepened its vertical integration in rare earth magnet processing and finishing, improving control over lead times, quality, and specialized geometries. This integration enables Arnold to provide precision-engineered magnetic components with tight tolerances, tailored to advanced propulsion systems, aerospace actuators, and specialized defense electronics. By focusing on **end-to-end capabilities—from material selection to final magnet assembly—**Arnold is strengthening its role as a high-value niche supplier in the global Permanent Magnets Market.

Permanent Magnets Market Report Scope

Permanent Magnets Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$39.3 Billion

|

|

Market Size (2035)

|

$87.2 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Material Type (NdFeB, Ferrite Magnets, SmCo, Alnico Magnets), By Form/Manufacturing Process (Sintered Magnets, Bonded Magnets, Flexible Polymer-Bonded Magnets), By End-Use Application (Automotive, Industrial Motors & Automation, Energy, Consumer Electronics, Medical Systems, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hitachi Metals (Metglas), VACUUMSCHMELZE, Arnold Magnetic Technologies, Ningbo Yunsheng, Beijing Zhong Ke San Huan, Shin-Etsu Chemical, TDK Corporation, San-Huan, Alliance Creative Group, Electron Energy Corporation, Tengam Engineering, JL MAG Rare-Earth, Baotou Rare Earth, Daido Steel, Dura Magnetics

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Permanent Magnets Market Segmentation

By Material Type

- Neodymium-Iron-Boron (NdFeB)

- Ferrite (Ceramic) Magnets

- Samarium Cobalt (SmCo)

- Alnico Magnets

By Form / Manufacturing Process

- Sintered Magnets

- Bonded Magnets

- Flexible Polymer-Bonded Magnets

By End-Use Industry

- Automotive

- Industrial Motors & Automation

- Energy (Wind turbines, power tools)

- Consumer Electronics

- Medical Systems

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Permanent Magnets Market

- Hitachi Metals (Metglas)

- VACUUMSCHMELZE (VAC)

- Arnold Magnetic Technologies

- Ningbo Yunsheng

- Beijing Zhong Ke San Huan

- Shin-Etsu Chemical

- TDK Corporation

- San-Huan

- Alliance Creative Group

- Electron Energy Corporation

- Tengam Engineering

- JL MAG Rare-Earth

- Baotou Rare Earth

- Daido Steel

- Dura Magnetics.

*- List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global Permanent Magnets Market in the context of fast-growing EV traction motors, offshore wind turbines, robotics, and high-efficiency industrial drives, delivering detailed analysis reviews of how NdFeB, ferrite, SmCo, and Alnico technologies compete and coexist under tightening rare earth supply constraints. It highlights breakthroughs in grain boundary diffusion (GBD), mine-to-magnet vertical integration, heavy rare earth (HREE)-lean magnet chemistries, and closed-loop NdFeB recycling ecosystems that are redefining cost structures, coercivity performance, and regional supply security. The study maps policy-driven shifts under CRMA, U.S. and Indian REPM schemes, and Chinese export controls to quantify their impact on capacity expansion, price formation, and OEM sourcing strategies. With deep dives into automotive, wind energy, industrial motors, consumer electronics, medical, aerospace, and defense demand, this report is an essential resource for industry professionals seeking to benchmark energy product grades, evaluate alternative magnet families such as MnBi and MnAlC, and align procurement or investment decisions with long-term electrification, decarbonization, and resilience objectives in the permanent magnets industry.

Scope Highlights

- Segmentation:

• By Material Type: Neodymium-Iron-Boron (NdFeB); Ferrite (Ceramic) Magnets; Samarium Cobalt (SmCo); Alnico Magnets

• By Form / Manufacturing Process: Sintered Magnets; Bonded Magnets; Flexible Polymer-Bonded Magnets

• By End-Use Industry: Automotive; Industrial Motors & Automation; Energy (Wind turbines, power tools); Consumer Electronics; Medical Systems; Aerospace & Defense

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ leading players across the permanent magnets value chain, from rare earth processors to magnet alloy producers and assembly specialists.