Market Overview: High-Performance Neodymium Magnets Driving EVs and Wind Turbines

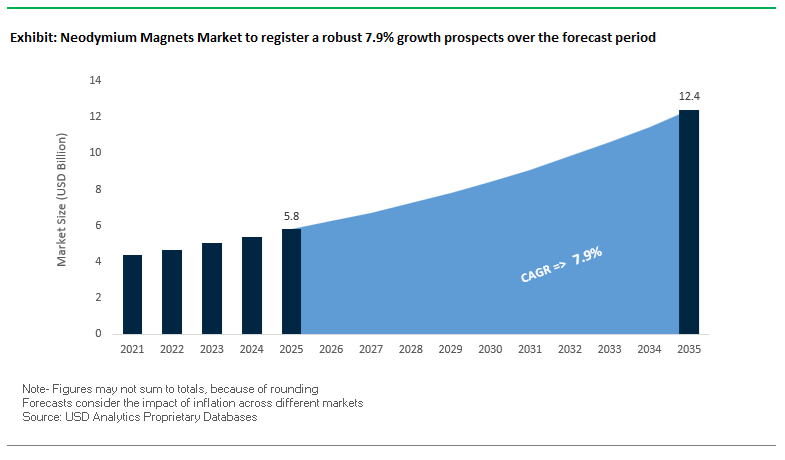

The global Neodymium Magnets Market is projected to grow from USD 5.8 billion in 2025 to USD 12.4 billion by 2035, registering a robust CAGR of 7.9% (2025–2035). This expansion is underpinned by the rapid electrification of transport, deployment of direct-drive wind turbines, and increasing adoption of high-efficiency motors in automation and robotics. For manufacturers and vendors of NdFeB (neodymium-iron-boron) magnets, the market is increasingly defined by high-temperature performance requirements, heavy rare earth (HREE) optimization, and supply-chain localization efforts in the US, Europe, and India.

High-grade sintered NdFeB magnets designed for EV traction motors and large wind turbine generators must sustain severe thermal and mechanical stress without demagnetization. This is forcing magnet producers to engineer compositions with intrinsic coercivity (Hcj) ≥30 kOe and operating temperature limits of up to 200°C, while carefully optimizing the use of dysprosium and terbium. On the demand side, each electric vehicle can consume close to a kilogram of NdFeB magnets, while a single megawatt of direct-drive wind capacity may require hundreds of kilograms of permanent magnets, making this market strategically critical for OEMs and governments focused on clean energy transitions.

Key insights for neodymium magnet manufacturers and vendors:

- High-temperature stability is non-negotiable: Sintered NdFeB grades for EV traction motors and wind turbines must deliver Hcj ≥30 kOe to guarantee reliable performance at peak temperatures approaching 200°C.

- Heavy rare earths constrain scaling: Achieving operational temperature limits of 180–210°C often requires 4–8% Dy/Tb content, exposing producers to heavy rare earth price volatility and geopolitical risk.

- EVs are a structural demand anchor: A single electric vehicle motor typically consumes 0.5–1.2 kg of NdFeB magnets, translating to 20–60 g of dysprosium per vehicle for high-heat grades.

- Wind turbines are magnet-intensive assets: Direct-drive wind turbines can require 200–300 kg of NdFeB magnets per MW, tying long-term magnet demand to renewable energy capacity additions.

- Supply is highly concentrated: Over 90% of global dysprosium and terbium oxide supply is concentrated in a single major source, reinforcing the strategic urgency of geographic diversification and recycling.

Market Analysis: Export Controls, Incentive Schemes and New NdFeB Capacity Pipelines

The global neodymium magnets market is entering a structurally tight yet strategically diversified phase where demand from EVs, wind turbines, industrial automation, and defense intersects with increasingly politicized raw material supply. On the demand side, long-term decarbonization targets and EV adoption curves are locking in multi-decade requirements for high-performance NdFeB magnets. On the supply side, governments in India, Europe, and North America are actively funding localized permanent magnet capacity to reduce dependence on a highly concentrated heavy rare earth supply chain.

A key inflection occurred in November 2025, when the Government of India approved a rare earth permanent magnet scheme with a financial outlay of Rs 7,280 crore (~USD 815 million) to build up to 6,000 TPA of integrated sintered REPM (rare earth permanent magnet) capacity. This creates a strong policy-backed opportunity for magnet producers and component suppliers to establish manufacturing footprints within India’s emerging EV and electronics ecosystem. Parallel to this, GKN Powder Metallurgy’s pilot plant in Germany, scheduled for early 2025, and Neo Performance Materials’ Narva facility in Estonia, targeting 2025 startup with 2,000 TPA expandable to 5,000 TPA, signal Europe’s intent to build a regionally resilient magnet value chain aligned with the European Green Deal and OEM localization strategies.

At the same time, supply risk has intensified due to China’s expanded rare earth export controls announced in October 2025, covering not only oxides and metals but also “parts, components and assemblies” containing Chinese-sourced rare earths. The International Energy Agency (IEA) in October 2025 highlighted that alternative Western sources currently offer less than 10% of global HREE supply, placing further emphasis on diversification, recycling and efficiency measures such as grain boundary diffusion to reduce Dy/Tb usage per magnet. In North America, MP Materials’ Fort Worth magnet plant, scheduled for commercial production in 2025 with an initial 2,000 TPA block capacity, and E-VAC Magnetics’ Sumter, South Carolina facility, targeted for late Fall 2025 and backed by a USD 94.1 million US Department of Defense agreement, are central to building a domestic end-to-end rare earth-to-magnet supply chain aimed at EV, defense and industrial applications.

Industry structure is thus shifting from a single-region supply dominance to a more distributed but still constrained ecosystem, where long-term offtake contracts and strategic partnerships are critical. The Hitachi Metals–Magna partnership announced in November 2024 explicitly targets EV permanent magnets, while MP Materials’ supply agreement with General Motors anchors its Fort Worth plant around Ultium traction motors. For OEMs and magnet producers, this environment demands a combined strategy of technology innovation (HREE-efficient NdFeB), geographic diversification, and long-term contracting, as competition for secure, sustainable neodymium magnet supply intensifies across the EV, wind, robotics, and defense sectors.

High-Impact Trends Driving Onshoring, Rare-Earth Efficiency, and Next-Generation High-Temperature Magnet Manufacturing

Market Trend 1: Rapid Onshoring of Sintered NdFeB Magnet Production to Mitigate Supply Concentration Risks

A defining global trend in the NdFeB Magnets Market is the accelerated push toward supply chain diversification and domestic sintered magnet manufacturing, especially in major consuming regions such as North America, Europe, and Japan. Prior to recent industrial policy interventions, the United States imported ≈75% of its sintered NdFeB magnets from a single country, underscoring extreme concentration risk for critical technologies including electric vehicle motors, wind turbines, and defense systems.

Domestic production capacity was essentially nonexistent—near zero in the early 2020s—forcing reliance on imported rare-earth feedstocks and finished magnets. To address this vulnerability, government-industry coalitions have announced ambitious plans targeting 10,000+ tonnes/year of domestic sintered NdFeB magnet capacity, a multi-fold increase from the current low single-kilotonne baseline.

However, the transition to localized production is not instantaneous. New sintered NdFeB facilities must undergo multi-year qualification cycles with automotive, aerospace, and defense customers. Announced capacity for 2027 may not produce meaningful commercial output until 2029–2030, highlighting the strategic, long-horizon nature of these investments. This onshoring trend is redefining global rare-earth magnet flows and reshaping long-term supply resilience strategies.

Market Trend 2: Acceleration of Grain Boundary Diffusion (GBD) and Cerium-Substitution R&D to Reduce Dysprosium Dependency

A second major trend reshaping the NdFeB Magnets Market is the intense research focus on Grain Boundary Diffusion (GBD) technologies and high-Ce substitution strategies designed to reduce dependence on heavy rare earth elements (HREEs)—specifically Dysprosium (Dy) and Terbium (Tb). GBD technology has demonstrated the capability to reduce total HREE consumption by 70–90% while still achieving the necessary coercivity (HcJ) for high-temperature EV traction motors.

GBD coats grain boundaries with Dy/Tb only where magnet degradation initiates, dramatically improving resource efficiency. In some Ce-containing magnet grades, GBD has been shown to increase coercivity by up to 47%, enabling stable operation under high thermal loads.

Traditional NdFeB compositions without HREEs exhibit performance loss above ≈80°C, but GBD-optimized magnets with lower Dy fractions maintain stability at temperatures up to 200°C—meeting EV and industrial motor requirements.

Simultaneously, material scientists are pushing to replace ≥5 wt% of Nd with abundant Cerium (Ce) while employing GBD to counteract the usual negative magnetic impacts. This dual-path innovation—Dy minimization + Ce substitution—is central to establishing a cost-effective, resource-secure next generation of NdFeB magnets.

Emerging Opportunities in Closed-Loop Rare-Earth Recovery and High-Volume Bonded Magnet Applications

Market Opportunity 1: Scaling Closed-Loop NdFeB Magnet Recycling for High-Performance Magnet-to-Magnet Manufacturing

End-of-life NdFeB magnets represent one of the world’s richest secondary rare-earth resources, containing 27–31 wt% rare earth elements, far exceeding ore-grade deposits. This makes recycling a high-value opportunity for regions seeking rare-earth supply independence.

Technologies such as Hydrogen Processing of Magnet Scrap (HPMS) are achieving >90% REE recovery rates, enabling true magnet-to-magnet recycling. Critically, magnets sintered from HPMS-derived powder demonstrate magnetic performance within 5% of virgin materials, validating recycled feedstock for traction motors, industrial motors, aerospace actuators, and other high-performance applications.

Life Cycle Assessment (LCA) studies show that recycling can reduce Global Warming Potential (GWP) by 30–70× compared to virgin rare-earth mining and separation. As environmental requirements tighten and OEMs seek low-carbon materials, closed-loop NdFeB recycling positions itself as a strategic pillar of sustainable magnet supply.

Market Opportunity 2: Engineering Bonded NdFeB Feedstocks for High-Volume, Complex-Geometry EV Components

The rise of compact, integrated electric drive systems is generating strong demand for bonded NdFeB magnets tailored for complex geometries and multi-pole patterns. Bonded magnets manufactured through injection molding, compression molding, or additive processes can achieve dimensional tolerances of ±0.05 mm, enabling net-shape production without costly machining—a major advantage for high-volume EV parts.

While bonded magnets exhibit lower density—typically ≈80% of theoretical maximum due to polymer binders—their formability enables magnetization patterns impossible or cost-prohibitive for brittle sintered magnets. Their (BH)max values of 10–15 MGOe are lower than the 50+ MGOe of premium sintered grades but remain ideal for sensors, auxiliary motors, actuators, pumps, window and seat motors, and other EV subsystems.

The ability to produce multi-pole magnetization in a single forming step provides manufacturing efficiency and performance benefits for high-speed motor designs, reducing assembly complexity and improving torque ripple behavior. As EV platforms electrify more components, bonded NdFeB magnets will play a critical enabling role in cost-optimized magnet architectures.

Neodymium Magnets Market Share Analysis

Market Share by Manufacturing Process: Sintered Neodymium Magnets Dominate High-Performance Motor and Generator Applications

Sintered neodymium magnets command an overwhelming ~90% share of the global NdFeB magnet market in 2025, reflecting their unmatched magnetic strength, thermal stability, and suitability for high-performance applications where efficiency and power density are critical. The sintering process—based on high-temperature powder metallurgy—allows for precise control of grain size, orientation, and composition, enabling magnets with the highest achievable remanence, coercivity, and maximum energy product (BHmax) among all commercially produced permanent magnets. This superior magnetic performance is integral to the design of compact, lightweight, and high-efficiency systems such as Electric Vehicle (EV) traction motors, industrial servo drives, and direct-drive wind turbine generators, all of which require strong magnetic fields to deliver torque density and system efficiency gains. The dominance of sintered NdFeB magnets is further reinforced by their essential role in Permanent Magnet Synchronous Motors (PMSMs)—the leading architecture for EV powertrains, used in roughly 95% of electric cars globally. Their extended operational temperature range and ability to maintain magnetic stability under heavy loads make them indispensable for high-torque and high-speed environments. While bonded and hot-deformed magnets offer design flexibility or isotropic properties for lower-power applications, they cannot match the strength-to-volume ratio of sintered magnets, ensuring this segment remains the backbone of global magnet demand across energy, transportation, automation, and industrial power sectors.

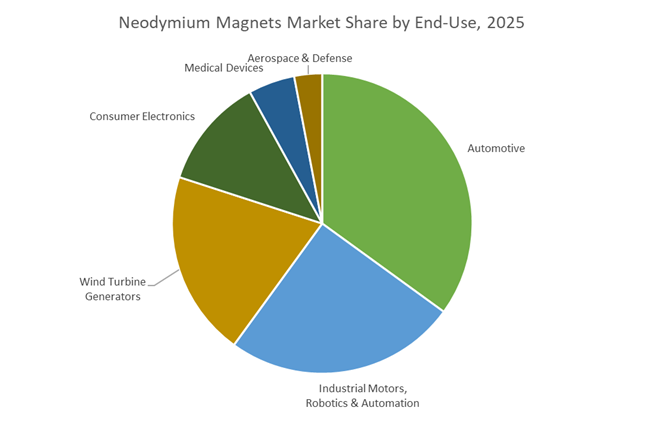

Market Share by End-Use: Automotive Sector Leads Due to Explosive Growth in EV Traction Motor Demand

The automotive industry accounts for approximately 35% of the global neodymium magnet market, driven by the rapid global adoption of electric vehicles (EVs) and the sector’s reliance on high-performance Permanent Magnet Synchronous Motors (PMSMs). Each battery-electric vehicle incorporates between 1–3 kg—and in some models up to 5 kg—of NdFeB magnets, primarily within the main traction motor that demands maximum torque density, high power conversion efficiency, and reliable performance across a wide temperature range. Compared to internal combustion engine (ICE) vehicles, which use minimal quantities of neodymium magnets in small auxiliary motors, EVs represent an order-of-magnitude increase in magnet intensity per unit produced. The sector’s leadership is reinforced by the fact that PMSM-based drivetrains deliver 93–97% efficiency, directly influencing vehicle range—a decisive factor in consumer adoption and automaker strategy. Beyond traction systems, the automotive sector integrates NdFeB magnets across dozens of subsystems, including ADAS sensor assemblies, power steering motors, ABS units, battery cooling pumps, and comfort features, further magnifying total magnet consumption. With global EV production scaling dramatically—supported by government mandates, emissions regulations, and OEM electrification roadmaps—the automotive segment remains both the largest and fastest-growing end-use category, anchoring long-term demand for sintered NdFeB magnets across global supply chains.

Country Analysis: Global Drivers in Neodymium Magnets Development

China: Unmatched NdFeB Production Scale, Vertical Integration, and Export-Control-Driven Supply Realignment

China remains the undisputed global powerhouse in the Neodymium Magnets Market, commanding the majority of global NdFeB production capacity through large-scale manufacturing, robust mining reserves, and complete vertical integration from rare earth ore to finished magnets. Leading firms such as JL MAG Rare-Earth Co., Ltd. are executing aggressive expansion strategies, targeting 40,000+ tons per year of NdFeB magnet output by 2025 to meet accelerating EV, robotics, and automation demand. Meanwhile, specialized producers such as Jiangmen Maxwell Magnet Industry Co., Ltd. maintain globally recognized certifications, including IATF 16949:2016, enabling consistent supply of automotive-grade injection-molded magnets for EV motors, actuators, sensors, and appliance systems. This quality emphasis aligns with rapid growth in China’s vehicle electrification and smart device manufacturing ecosystems.

China’s dominance is reinforced through unprecedented levels of vertical integration, controlling mining, refining, alloying, powder metallurgy, sintering, machining, and magnet coating processes. This structure provides pricing stability, supply assurance, and accelerated innovation cycles unmatched by global competitors. However, the nation's 2024–2025 export control measures have reshaped global sourcing strategies by restricting not only raw materials but also technical expertise and processing equipment. These restrictions magnify the geopolitical risk associated with NdFeB supply chains and are prompting major EV, defense, and industrial motor manufacturers worldwide to diversify sourcing and pursue domestic magnet-making capacity. China's continued supply chain control will remain a defining factor influencing global magnet pricing, technology development, and foreign industrial policy.

United States: Government-Backed Mining-to-Magnet Reshoring and Strategic Capacity for Defense & EV Security

The United States is rapidly building a domestic Neodymium Magnet supply chain to reduce reliance on foreign suppliers and strengthen national security, EV production, and critical defense programs. A cornerstone of this effort is the emergence of Vulcan Elements, which is developing a fully vertically integrated 10,000-metric-ton annual NdFeB magnet facility in North Carolina—supported by direct U.S. government investment and a $50 million equity stake through the Department of Commerce. This represents the strongest U.S. commitment to restoring rare earth magnet manufacturing in decades. Complementing this effort, the U.S. Department of Energy (DOE) announced up to $134 million in December 2025 to scale REE recovery technologies from waste coal, mine tailings, and e-waste, aiming to produce commercially viable sources of Neodymium and Dysprosium for domestic magnet production.

Upstream, MP Materials continues to advance mining and separation capabilities at Mountain Pass, the largest rare-earth resource outside China, focusing on producing high-purity NdPr oxides for downstream magnet producers. The combination of mining, oxide production, metalmaking, alloying, and magnet fabrication within U.S. borders is essential for electrified transportation, grid-scale wind power, industrial automation, and classified defense systems. The strategic reshoring of NdFeB production—backed by strong federal procurement preference—is set to transform the U.S. into a scalable and geopolitically secure magnet manufacturing ecosystem by the late 2020s.

Japan: Engineering Leadership in HRE-Reduced and High-Temperature NdFeB Magnets for EV Traction Motors

Japan maintains a world-leading position in advanced Neodymium Magnet innovation, particularly in reducing dependence on critical Heavy Rare Earth Elements (HREs) such as Terbium (Tb) and Dysprosium (Dy), which are essential for high-temperature EV traction motors but subject to extreme price and supply volatility. Toyota Motor Corporation remains at the forefront of this effort with its breakthrough HRE-free NdFeB magnet, replacing a portion of Neodymium with abundant Lanthanum (La) and Cerium (Ce) while maintaining high coercivity and heat resistance. This innovation—first announced in 2018 and still central to Toyota’s electrification materials strategy—has become pivotal in driving cost-efficient EV motor production across Japan’s automotive industry.

Japan also excels in producing high-performance sintered NdFeB magnets—with magnetic energy products reaching up to 50 MGOe—and remains a technological leader in hot-deformed NdFeB magnets, which offer exceptional structural uniformity and thermal stability. Manufacturers such as Proterial, Ltd. and Shin-Etsu Chemical Co., Ltd. continue to advance hot-deformed magnet technology for use in wind turbine generators, robotics, industrial motors, and hybrid/EV drive systems. This focus on HRE reduction, high-temperature performance, and premium magnet reliability ensures Japan remains a crucial innovator in the global move toward sustainable, efficient electric mobility.

European Union (Germany): Rare-Earth Magnet Recycling, CRMA Compliance, and Domestic Manufacturing Initiatives

Germany and the broader European Union are prioritizing supply chain resilience through advanced recycling, domestic production, and strategic investment under the Critical Raw Materials Act (CRMA). The CRMA mandates that by 2030, at least 25% of EU rare earth consumption must be met through recycling, while 20% of demand should be fulfilled via domestic extraction, refining, or manufacturing. This regulatory shift is powering large-scale circular economy initiatives, including the EU-funded HARMONY project, which brings together more than 20 partners to create a closed-loop recycling process for NdFeB magnets from end-of-life EV motors, wind turbines, and electronic devices. Full-scale manufacturing from recycled feedstocks is expected by 2028, dramatically reducing reliance on imported materials.

Additionally, the European Raw Materials Alliance (ERMA) has identified 14 domestic mine-to-magnet projects with projected investment exceeding €1.7 billion. These projects aim to secure roughly 20% of EU magnet demand by 2030. Germany’s VACUUMSCHMELZE (VAC) remains a technological leader in specialty NdFeB alloys and integrated magnet-to-stator production for European automotive electrification. As Europe intensifies its clean energy transition and strengthens strategic autonomy, domestic NdFeB magnet production and recycling will play a pivotal role in the continent’s industrial competitiveness.

India: Government-Backed REPM Manufacturing Scheme and Strategic Raw Material Sourcing for EV Growth

India is entering the Neodymium Magnets Market with strong government backing aimed at reducing import dependence and supporting its rapidly expanding EV and renewable energy sectors. The Indian government is preparing to launch a ₹72.8 billion Rare-Earth Permanent Magnet (REPM) incentive scheme, scheduled to begin accepting bids by January 2026, with the goal of establishing 6,000 metric tons per year of fully integrated REPM manufacturing capacity. This initiative aligns directly with India’s EV30@30 target, which aims for 30% electric vehicle penetration by 2030, making domestic magnet production essential for traction motors, inverters, and renewable power equipment such as wind turbine generators.

To ensure feedstock stability, India is proactively working to secure rare earth oxides from suppliers in South America, Africa, and Australia, mitigating challenges associated with domestic monazite processing and radiation-handling requirements. This global raw material diversification strategy is key to building a reliable and cost-competitive domestic magnet industry. As India strengthens its manufacturing ecosystem through PLI schemes, defense offsets, and renewable energy expansion, the country is poised to become an influential regional center for NdFeB magnet production by the late 2020s.

Competitive Landscape: Key Neodymium Magnet Producers Reshaping Global Supply

The neodymium magnets industry is characterized by a mix of long-established technology leaders and rapidly scaling integrated producers that are repositioning around EV, wind and defense demand. Legacy Japanese and European players bring deep materials science capabilities (e.g., grain boundary diffusion, hot-working technologies), while newer North American and European entrants are leveraging policy-driven capex to onshore critical magnet capacity. This combination is reshaping competitive dynamics, reducing single-country dependence, and creating a multi-polar NdFeB magnet supply ecosystem.

Hitachi’s advanced NdFeB magnet technology underpins EV and industrial growth

Hitachi, through its legacy Hitachi Metals / Arnold Magnetic Technologies magnet portfolio, remains a cornerstone technology leader in high-performance sintered NdFeB magnets for automotive and industrial markets. The company is known for NH and other high-grade series that deliver superior coercivity and thermal stability, meeting the demanding specifications of EV traction motors and heavy-duty industrial drives. Its deep patent base and know-how in grain boundary diffusion allow it to enhance heat resistance while minimizing the quantity of expensive dysprosium and terbium required, a key differentiator as HREE prices and export controls tighten. In November 2024, Hitachi entered a strategic partnership with Magna International to co-develop and manufacture advanced permanent magnets tailored to EV platforms, cementing its role as a critical technology and supply partner to global automotive OEMs as electrification scales.

Daido Steel optimizes hot-working NdFeB magnets for high-efficiency motors

Daido Steel is a leading specialist in magnetic materials and specialty steels, recognized for its pioneering work in hot-working NdFeB magnets such as MQ3 / NEOQUENCH-DR®. These magnets are manufactured by molding rapidly solidified alloy powders at elevated temperatures, delivering a strong combination of high magnetic force, improved mechanical properties, and reduced heavy rare earth usage. Daido’s proprietary hot-worked radial anisotropic ring magnet technology is designed specifically to save Dy/Tb while maintaining the high heat resistance and anisotropy needed for compact motors, notably in electric power steering (EPS) and other automotive applications. Under its 2030 Vision, Daido positions its advanced magnet products as enablers of a “green society,” with key applications spanning EV drive motors, robotics and factory automation, where compact, high-torque, high-efficiency motors are essential.

VAC Group builds non-Chinese NdFeB magnet capacity for defense and EVs

VACUUMSCHMELZE GmbH & Co. KG (VAC Group) is a global leader in advanced magnetic materials, offering a broad portfolio of sintered NdFeB magnets (VACODYM series) and injection molded NdFeB bonded magnets for complex geometry parts. VAC’s materials are engineered for high coercivity and thermal stability, making them suitable for mission-critical applications in aerospace, automotive braking, power systems, and industrial drives. Through its US subsidiary E-VAC Magnetics, VAC is constructing a major sintered NdFeB magnet facility in Sumter, South Carolina, targeted for operation in Fall 2025 and supported by a USD 94.1 million US Department of Defense agreement. This project positions VAC as a cornerstone non-Chinese supplier for defense and strategic industries, contributing to a secure domestic magnet supply in North America while also serving high-growth EV and industrial markets.

MP Materials advances fully integrated US rare earth–to–magnet value chain

MP Materials Corp. is unique in its pursuit of a fully integrated North American rare earth and NdFeB magnet value chain, from mining to finished magnet block. Leveraging its Mountain Pass operation in California, MP Materials produces rare earth concentrates that will feed downstream alloying and sintered NdFeB magnet production at its new plant in Fort Worth, Texas. The Fort Worth facility is on track for commercial production in 2025, with an initial capacity of around 1,000–2,000 TPA of magnet block, sufficient to supply magnets for approximately 1.5 million EVs annually. Under a long-term commercial agreement with General Motors (GM), these magnets are intended for use in Ultium-based EV traction motors, giving MP a secure demand anchor. By closing the loop from mine to motor, MP Materials significantly reduces reliance on imported magnets and establishes itself as a strategically vital player in the US EV and defense supply chain.

Neo Performance Materials strengthens European NdFeB magnet independence

Neo Performance Materials Inc. occupies a critical niche as a non-Chinese producer of rare earth specialty materials, including high-purity rare earth oxides and advanced magnetic powders such as its Magnequench brand. These powders are essential feedstock for producing both bonded and sintered NdFeB magnets with tightly controlled compositions and performance characteristics. To directly serve European OEMs and align with the EU’s energy independence and green transition goals, Neo is building a permanent magnet facility in Narva, Estonia, targeting 2025 startup with an initial 2,000 TPA capacity, ultimately expandable to 5,000 TPA. The project is partly funded by the EU’s Just Transition Fund, underscoring its strategic relevance to the European Green Deal. Combining its expertise in rare earth separation and powder engineering, Neo is positioned as a key supplier of high-performance, heat-resistant NdFeB magnets for European EV, wind, and industrial applications, helping regional customers mitigate the risks associated with concentrated HREE supply.

Neodymium Magnets Market Report Scope

Neodymium Magnets Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.8 Billion

|

|

Market Size (2035)

|

$12.4 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Manufacturing Process (Sintered Neodymium Magnets, Bonded Neodymium Magnets, Hot-Deformed Neodymium Magnets), By Composition/Grade (Standard Grades, High-Temperature Grades, Heavy Rare Earth–Reduced Magnets), By Coating/Plating Type (Nickel-Copper-Nickel, Epoxy Coating, Zinc Coating, PTFE/Teflon, Phosphate/Passivation), By End-Use Application (Automotive, Wind Turbine Generators, Industrial Motors & Robotics, Consumer Electronics, Medical Devices, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shin-Etsu Chemical, Proterial, TDK Corporation, JL MAG Rare-Earth, VACUUMSCHMELZE, Ningbo Yunsheng, MP Materials, Zhenghai Magnetic Material, Arnold Magnetic Technologies, Aichi Steel, Electron Energy Corporation, Baotou Tianhe Magnetics, Lynas Rare Earths, Hangzhou Permanent Magnet Group, Ningbo Zhaobao Magnet

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Neodymium Magnets Market Segmentation

By Manufacturing Process

- Sintered Neodymium Magnets

- Bonded Neodymium Magnets

- Hot-Deformed Neodymium Magnets

By Composition / Grade

- Standard Grades (N35–N45)

- High-Temperature Grades (H, SH, UH, EH, AH)

- Heavy Rare Earth–Reduced Magnets

By Coating / Plating Type

- Nickel–Copper–Nickel

- Epoxy Coating

- Zinc Coating

- PTFE / Teflon

- Phosphate / Passivation

By End-Use Industry

- Automotive (EV & HEV Motors, EPS, Sensors)

- Wind Turbine Generators

- Industrial Motors, Robotics & Automation

- Consumer Electronics

- Medical Devices

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Neodymium Magnets Market

- Shin-Etsu Chemical

- Proterial (formerly Hitachi Metals)

- TDK Corporation

- JL MAG Rare-Earth

- VACUUMSCHMELZE

- Ningbo Yunsheng

- MP Materials

- Zhenghai Magnetic Material

- Arnold Magnetic Technologies

- Aichi Steel

- Electron Energy Corporation

- Baotou Tianhe Magnetics

- Lynas Rare Earths

- Hangzhou Permanent Magnet Group

- Ningbo Zhaobao Magnet.

*- List not Exhaustive

Research Coverage

The USDAnalytics Neodymium Magnets Market report investigates how electrification, renewable energy build-out, and supply-chain realignment are reshaping demand for high-performance NdFeB magnets across EVs, wind turbines, robotics, and defense applications. It highlights technology breakthroughs in high-temperature grades, heavy rare earth reduction, grain boundary diffusion, hot-deformed manufacturing, and closed-loop recycling, while our analysis reviews policy-led onshoring programs in the US, Europe, India, and other key regions. The study examines evolving OEM sourcing strategies, long-term offtake structures, and CAPEX pipelines for new sintered and bonded magnet capacity, linking them to traction motor, generator, and automation platform design trends. It also quantifies how export controls, resource concentration, and rare earth substitution programs are likely to influence cost curves and margin structures over 2026–2034. By connecting materials science advances with real-world deployment in EV platforms, direct-drive wind turbines, industrial drives, and strategic defense systems, this report is an essential resource for product planners, procurement leaders, investors, and policymakers who need a data-backed view of neodymium magnet supply, pricing risk, and technology pathways over the next decade.

Scope Highlights

- Segmentation:

By Manufacturing Process – Sintered Neodymium Magnets, Bonded Neodymium Magnets, Hot-Deformed Neodymium Magnets

By Composition / Grade – Standard Grades (N35–N45), High-Temperature Grades (H, SH, UH, EH, AH), Heavy Rare Earth–Reduced Magnets

By Coating / Plating Type – Nickel–Copper–Nickel, Epoxy, Zinc, PTFE / Teflon, Phosphate / Passivation

By End-Use Industry – Automotive (EV & HEV motors, EPS, sensors), Wind Turbine Generators, Industrial Motors/Robotics & Automation, Consumer Electronics, Medical Devices, Aerospace & Defense

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, covering both consumption centers and emerging production hubs.

- Time Horizon: Historic data from 2021–2025 with detailed market forecasts, technology outlooks, and policy scenarios from 2026–2034.

- Companies Covered: Competitive analysis and profiles of 15+ leading players, including integrated rare earth–to–magnet suppliers, specialist sintered and bonded magnet manufacturers, and emerging regional challengers.