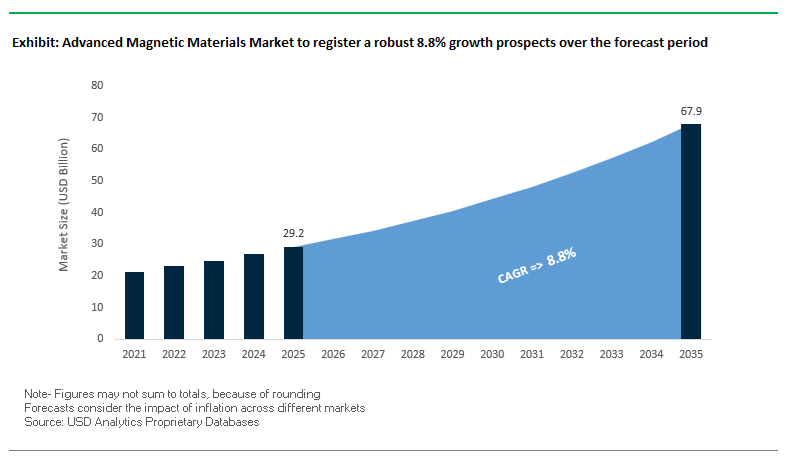

The Advanced Magnetic Materials Market, valued at USD 29.2 billion in 2025, is projected to reach USD 67.9 billion by 2035, growing at a CAGR of 8.8% (2025–2035). As electrification accelerates across EVs, aerospace, robotics, renewable energy, and high-frequency power electronics, demand is shifting from traditional ferrites toward advanced NdFeB, SmCo, nanocrystalline soft magnetic alloys, and rare-earth-reduced magnet technologies. The latest performance benchmarks provide clear guidance, showing that advanced magnetic materials are essential for achieving high-efficiency, high-temperature, and high-power-density motor and power conversion designs.

- SmCo high-temperature stability: Samarium Cobalt permanent magnets validated for 300°C service temperature (Nov 2025), making them essential for aerospace propulsion and high-performance EV traction motors.

- NdFeB energy product trade-off: N42-grade NdFeB achieves 42 MGOe BHmax, but its 140°C thermal limit restricts performance without Dy/Tb enhancement.

- Soft magnet thermal stability: New Fe–Cr–Co–Si soft magnetic alloys retain performance with only 0.03% magnetic induction loss per Kelvin up to 400°C, enabling high-frequency inverters and EV power electronics.

- Heavy rare-earth reduction: Grain boundary diffusion achieves up to 50% less Dy/Tb, mitigating geopolitical risk and improving supply chain resilience.

- Nanocrystalline efficiency: Next-gen nanocrystalline materials deliver 65–80% lower core loss versus silicon steel at >10 kHz, a crucial advantage for 5G, data center power modules, and EV fast chargers.

The advanced magnetic materials industry underwent significant transformation across 2024–2025, driven by geopolitical licensing rules, rare-earth material consolidation, breakthrough magnet innovations, and increased AI-driven R&D workflows. The most disruptive shift occurred in April 2025, when the Chinese government introduced new export licensing rules for NdFeB and SmCo materials, amplifying supply chain uncertainty for OEMs in EV, defense, wind turbines, and industrial automation. The policy milestone accelerated diversification strategies, pushing manufacturers toward Vietnam, North America, and Europe for NdFeB processing capacity. By June 2025, Proterial completed a major NdFeB magnet processing plant in Vietnam, strengthening non-China production routes for its NEOMAX® magnet range, while September 2025 saw American Axle acquire Dowlais Group (including GKN Powder Metallurgy) for USD 1.44 billion, consolidating magnetic component manufacturing and e-drive technology capabilities within Western markets.

Magnetic innovation accelerated in parallel. In November 2025, TDK launched its PZ-series power ferrites reducing core loss by 30% at 2 MHz, directly addressing miniaturization and thermal control needs in high-frequency converters used in 5G equipment, EV onboard chargers, and aerospace power electronics. October 2025 marked a major advance by Shin-Etsu Chemical with a proprietary anti-corrosion coating for NdFeB magnets, extending their life in harsh EV environments. In December 2025, industry R&D momentum shifted further with widespread adoption of AI-driven magnetic geometry simulation, delivering up to 40% reduction in material development cycles by optimizing flux pathways and reducing trial-and-error in stator/rotor design. Across the same period, multinational alliances reshaped the rare-earth value chain: in November 2025, VAC, Ucore, and Aclara established a strategic mine-to-magnet cooperation to support Western production of NdFeB and SmCo magnets, stimulating regional supply chain resilience against geopolitical pressures.

The year also saw rapid advancements in rare-earth-saving technologies. In March 2025, Daido Steel signed a cross-licensing agreement with a European automotive supplier to accelerate adoption of its Dy-free hot-deformed NdFeB magnets, enhancing thermal stability while reducing dependence on critical heavy rare earths. Meanwhile, soft magnetic material innovation expanded in response to megatrends like EV fast chargers and high-frequency renewable energy systems. Nanocrystalline alloys demonstrated 65–80% core loss reduction, providing superior efficiency for compact, high-power-density systems. Collectively, these developments confirm a global shift toward next-generation magnetic materials optimized for temperature, efficiency, sustainability, and supply chain de-risking, redefining competitive strategy from 2025 onward.

Trend 1: Intensified R&D and Pilot Production of Heavy Rare Earth-Free Permanent Magnets to Reduce Global Supply Dependency

A significant, industry-wide shift toward heavy rare earth-free permanent magnets is underway as geopolitical tensions and material scarcity accelerate the search for alternatives to Dysprosium (Dy) and Neodymium (Nd). Manufacturers, governments, and investors are deploying capital toward scalable MnBi and Fe-N magnets, aiming to mitigate strategic vulnerabilities in EVs, wind turbines, robotics, and defense systems.

Key developments driving this transition include:

- Government-backed localization programs, exemplified by India’s landmark ₹7,280 crore (~$875 million) initiative to promote domestic Sintered Rare Earth Permanent Magnet (REPM) manufacturing, adding 6,000 MTPA capacity to support automotive and defense applications.

- Strong private funding momentum, with Niron Magnetics raising $25 million from major automotive and electronics giants (Samsung Ventures, GM Ventures, Stellantis Ventures, Volvo Cars Tech Fund) to expand pilot manufacturing for its Clean Earth Magnet portfolio.

- High-performance breakthroughs in MnBi magnets, demonstrating coercivity above 1.6 Tesla and attaining a rare advantage-increasing coercivity with temperature at +0.1% per °C up to 150°C, directly benefiting EV traction motors exposed to high thermal loads.

- Temperature-stable alternatives like MnBi and Fe-N are being engineered to compete with mid-range NdFeB grades, especially for 80°C–150°C operating ranges, unlocking new opportunities for automotive electrification, drones, and aerospace systems.

This trend marks the beginning of a fundamental industry pivot, positioning rare-earth-free magnets as the next frontier in strategic material independence.

Trend 2: Integration of Soft Magnetic Composites to Enable High-Frequency, High-Efficiency EV Traction Drive Systems

The rapid electrification of transportation and adoption of SiC- and GaN-based inverters are transforming electric motor design. EV manufacturers are now shifting from laminated electrical steel to Soft Magnetic Composites (SMCs), which support higher frequencies, reduce core losses, and enable new topologies such as Axial Flux Motors (AFMs).

Key technical drivers include:

- Lower high-frequency loss characteristics, where SMCs outperform 0.5 mm laminated steel above 200 Hz, reducing heat generation and boosting traction motor efficiency.

- Superior suppression of harmonic-related losses, as inverter-fed motors experience only ≈3% increase in core losses with SMCs versus ≥10% with laminated steel under high-harmonic conditions.

- Torque and efficiency gains in axial flux designs, with Soft Magnetic Powder Composites (SMPCs) enabling 1.6× higher torque and up to 1% efficiency improvement-a major advantage for motors targeting compact packaging and high torque density.

- Commercial readiness of SMC grades optimized for >2 kHz and >4 kHz switching frequencies, aligned with next-generation SiC/GaN inverter architectures.

This trend underscores a major transition toward 3D magnetic flux materials that can support the industry’s move toward compact, lightweight, high-performance EV motor platforms.

Opportunity 1: Supplying High-Permeability, Low-Loss Magnetic Materials for AI Data Center Power Conversion Systems

AI-driven hyperscale data centers-powered by racks exceeding 50 kW-require ultra-high-efficiency power conversion to manage thermal loads and minimize system size. This creates an immense opportunity for suppliers of nanocrystalline and amorphous magnetic materials, which outperform ferrites at high switching frequencies.

Key growth enablers include:

- Extremely high permeability, with nanocrystalline alloys such as FINEMET achieving permeability ranges of 50,000–120,000, supporting significant reductions in transformer and inductor size.

- Low core loss performance at MHz-class frequencies, where amorphous and nanocrystalline ribbons exhibit losses up to 10× lower than soft ferrites, preventing overheating in confined server environments.

- High saturation flux density (Bs) in advanced alloy systems, enabling higher power density and smaller magnetic component footprints-critical for 1 MHz switch-mode converters.

- Growing adoption of WBG semiconductors (SiC and GaN), which push conversion frequencies from 100 kHz to 1 MHz, strengthening the market pull for low-loss magnetic materials capable of maintaining efficiency at ultra-high switching speeds.

As AI infrastructure expands globally, vendors with high-frequency magnetic material portfolios will gain significant traction in the evolving power electronics supply chain.

Opportunity 2: Commercialization of Magnetocaloric Materials for Compact, Refrigerant-Free Heat Pumps

Environmental regulations targeting high-GWP refrigerants are catalyzing a shift toward solid-state magnetocaloric cooling systems, which promise higher efficiency, lower emissions, and compact form factors suitable for residential appliances, automotive HVAC, and premium cooling solutions.

Key opportunity drivers:

- Regulatory pressure, particularly the EU F-Gas Regulation (EU 2024/573) mandating 85% reduction in HFC use by 2036, accelerating investment into refrigerant-free cooling systems.

- Efficiency improvements of up to 25%, where magnetocaloric heat pumps outperform vapor compression systems; automotive prototypes are targeting COP > 5, more than double that of conventional A/C systems.

- Pilot-scale production advances, demonstrated by General Engineering & Research, which achieved 20% performance improvement and an initial scale of 1 kg/day in magnetocaloric material output.

- Projected 20–30% energy savings in residential systems, supported by U.S. Department of Energy (DOE) research validating the economic and environmental benefits of solid-state refrigeration.

This opportunity represents a high-growth frontier in sustainable cooling, aligning with global decarbonization mandates and next-generation home and automotive HVAC technologies.

Advanced Magnetic Materials Market Share Analysis

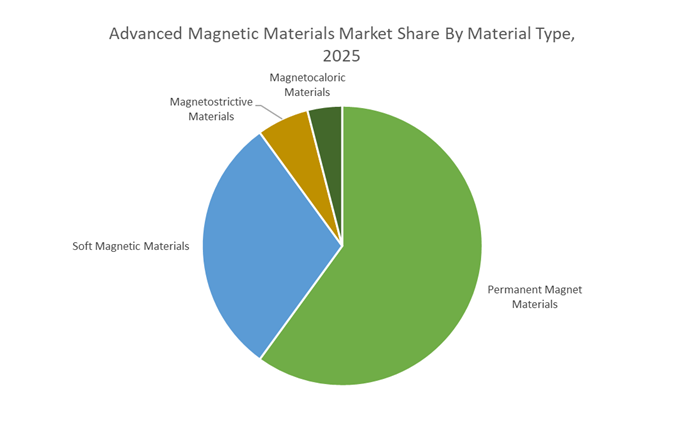

Market Share by Material Type: Permanent Magnet Materials Lead Through Exceptional Energy Product, High Coercivity, and Power-Density Advantages

Permanent magnet materials hold a commanding 60% share of the Advanced Magnetic Materials Market because they remain the foundational enabler of high-efficiency electromechanical energy conversion across modern industries—from EV traction motors to robotics, consumer electronics, and renewable energy systems. Their dominance is directly linked to the unmatched performance of rare-earth permanent magnets, especially Neodymium Iron Boron (NdFeB), which deliver the highest Maximum Energy Product (BHmax) among commercially available magnet classes. With BHmax values exceeding 50 MGOe (400 kJ/m³)—over 10–15 times stronger than ferrite magnets—NdFeB materials support the ongoing global shift toward miniaturization and high-power-density systems. This high energy product enables designers to produce smaller, lighter motors and actuators without compromising torque or speed, a critical requirement in compact EV powertrains and high-speed industrial automation.

Another decisive factor behind this segment’s market share is the high magnetic coercivity (Hc) of rare-earth magnets, which allows them to retain magnetic strength even under severe thermal and demagnetizing-field conditions. This stability is essential in applications such as high-speed motors and turbo machinery, where peak loads generate strong reverse fields capable of degrading lower-grade materials. Their ability to remain magnetically stable at elevated temperatures—often through engineered dysprosium (Dy) or terbium (Tb) doping—further reinforces their adoption in automotive and aerospace environments. As industries prioritize efficiency, reduced energy consumption, and system miniaturization, permanent magnet materials offer the most compelling performance-to-cost ratio, securing their dominant share in the advanced magnetic materials ecosystem.

Market Share by Application: EV Traction Motors Dominate as Permanent-Magnet Synchronous Motors Enable Peak Efficiency, High Torque Density, and Extended Range

Electric Vehicle (EV) traction motors represent the largest application category with 45% share, driven by the widespread adoption of Permanent Magnet Synchronous Motors (PMSMs)—the global standard for EV powertrains. PMSM architecture delivers the highest power density, efficiency, and torque performance among motor technologies, enabling automakers to achieve longer driving ranges, faster acceleration, and lower system weight—core performance metrics shaping EV competitiveness. Currently, 80–90% of EVs sold globally use PMSM technology, highlighting the degree to which EV development is fundamentally dependent on high-performance permanent magnets.

A key contributor to this segment’s dominance is the superior efficiency profile of PMSMs, which routinely exceed 95% efficiency across broad operating conditions because they generate rotor flux without consuming electrical energy for magnetization, unlike induction motors. This efficiency advantage alone can deliver 5–15% additional driving range, making PMSMs the preferred solution for OEMs optimizing battery utilization and meeting tougher fuel economy and emissions standards. Meanwhile, the torque density advantage—with leading PMSM designs achieving >30 Nm/L—supports compact motor housings and improved vehicle packaging, crucial for next-generation EV architectures.

In addition, as fast-charging, high-voltage (800V) platforms become mainstream, PMSMs provide the thermal stability and magnetic robustness required for sustained high-power operation. The synergy between rare-earth permanent magnets and EV traction motor performance ensures continued dominance of this segment, making it the largest demand driver within the global advanced magnetic materials landscape.

Country Analysis: Global Advanced Magnetic Materials Innovation and Manufacturing Hubs

China – Rare Earth Magnet Production Dominance and Next-Generation EV Motor Materials

China remains the cornerstone of the global Advanced Magnetic Materials Market, commanding the world’s largest supply chain for NdFeB permanent magnets, supported by state-driven policies, vertically integrated rare earth extraction hubs, and a booming EV and wind turbine manufacturing base. The introduction of new Rare Earth Magnet export controls in October 2024 marks a significant geopolitical inflection point. By requiring export licenses for NdFeB and SmCo magnet technologies, China aims to secure domestic supply and limit foreign dependence on strategic magnetic material categories. This regulatory tightening directly impacts global motor manufacturers, aerospace companies, and clean energy integrators who rely heavily on Chinese high-performance magnet grades.

China’s rapid downstream expansion is equally influential. Baotou Rare Earth Group’s USD 1.5 billion investment (2025) to scale sintered NdFeB magnet manufacturing underscores China’s long-term plan to dominate high-end EV traction motor magnet production. Material innovation is advancing rapidly through the adoption of grain boundary diffusion (GBD) technology, which significantly reduces the use of critical heavy rare earths like Dysprosium (Dy) and Terbium (Tb) while maintaining high coercivity. In parallel, research institutes such as the China Academy of Sciences are broadening the material ecosystem with breakthroughs in Mn-based rare earth-free magnets, an advancement that could alleviate cost and supply chain pressure by providing an alternative for mid-grade bonded magnet applications. As China continues reinforcing its rare earth monopoly and accelerating innovation in magnetic materials, it sets the pace for the global competitive landscape.

United States – Rare Earth Magnet Supply Chain Rebuilding and Breakthrough Recycling Technologies

The United States is advancing an aggressive industrial strategy focused on rebuilding a domestic Rare Earth Magnet supply chain, driven by national security priorities and federal incentives targeting mining, refining, magnet manufacturing, and recycling. In 2024, the U.S. Department of Defense and the Department of Energy jointly awarded over $250 million in Defense Production Act (DPA) funding to companies including MP Materials and TDA Magnetics to establish an end-to-end NdFeB magnet ecosystem inside the country. This funding is designed to minimize exposure to foreign-controlled magnet supply chains and ensure availability for defense-critical applications such as missile guidance, satellites, and high-performance propulsion systems.

A parallel innovation stream is emerging through rare earth-free magnet development. Niron Magnetics’ USD 20 million DOE grant (2025) positions Fe16N2 iron nitride magnets as one of the most promising NdFeB substitutes. These high-magnetization materials, once scaled, can disrupt applications currently reliant on rare earths, particularly in EV motors and industrial machinery. Additionally, the DOE’s USD 40 million allocation to Soft Magnetic Composite (SMC) R&D drives technological progress for next-generation power electronics, wireless charging systems, and high-frequency transformers. Together, U.S. federal initiatives are reshaping the magnetic materials landscape by building a resilient supply chain, accelerating recycling innovation, and nurturing rare earth-independent magnet technologies.

Japan – High-Coercivity Sintered Magnet Leadership and Rare Earth Reduction in EV Motors

Japan continues to lead the global market in high-coercivity, high-temperature Sintered NdFeB Magnets, essential for advanced automotive, industrial robotics, and aerospace systems that require stringent thermal stability and high magnetic performance. Japanese manufacturers such as Hitachi Metals (Resonac) remain unmatched in developing NdFeB technologies that dramatically reduce Dysprosium usage while sustaining heat resistance up to 180°C, addressing both cost and supply vulnerability challenges. This capacity to deliver premium magnet grades makes Japan a preferred supplier for Tier-1 automotive OEMs transitioning to high-efficiency electric drive architectures.

Beyond materials engineering, Japan is investing heavily in rare earth-free magnet R&D to secure long-term resource independence. In 2025, Honda and academic partners successfully developed and tested a new production EV motor prototype using heavy rare earth-free magnetic materials—one of the most significant breakthroughs in next-generation magnet sustainability. Companies like Shin-Etsu Chemical, global licensees of advanced NdFeB intellectual property, continue scaling high-precision sintering and binder technologies to ensure consistency and reliability across mass production. Japan’s focus on rare earth minimization, high-performance material design, and strategic EV integration cements its status as a technological powerhouse in advanced magnetic materials.

Germany / Europe – Wind Turbine Magnet Demand and Rare Earth-Free Materials Under EU Industrial Strategy

Europe is intensifying its push to develop domestic capacity for advanced magnetic materials, propelled by the Critical Raw Materials Act (CRMA) and the continent’s expanding fleet of offshore wind turbines and electrified vehicles. Germany, in particular, stands at the center of this transformation. Vacuumschmelze (VAC), a global leader in Soft Magnetic Materials and permanent magnets, announced a €100 million expansion in 2025 to boost production of NdFeB magnets and proprietary rare earth-free alloy materials. This expansion is essential for strengthening the European magnet supply chain and reducing reliance on Asian imports.

Wind energy remains Europe’s strongest demand driver. The European Commission projects an 8× increase in NdFeB magnet demand by 2030, largely driven by direct-drive offshore wind turbines that rely on heavy-duty permanent magnets for high torque and reliability. In parallel, European automotive OEMs and research centers are advancing next-generation Soft Magnetic Materials for EV inverters. A 2024 project led by Siemens and German Technical Universities focuses on optimizing amorphous and nanocrystalline soft magnetic cores for 800-V EV powertrains, achieving energy loss reductions of up to 30% compared to conventional silicon steel. Europe’s strategic focus on clean energy, low-carbon technologies, and raw material independence is positioning the region as a critical innovation hub for the future of magnetic materials manufacturing.

Competitive Landscape: Leading Manufacturers, Performance Metrics & Strategic Expansion

A diverse ecosystem of global leaders shapes the Advanced Magnetic Materials Market, with competitive advantages rooted in rare-earth processing technologies, soft magnetic alloy innovation, high-temperature magnet performance, and geographically diversified supply chains. Companies are competing not only on magnetic performance but also on sustainability, rare-earth efficiency, and the ability to deliver stable material supply under geopolitical constraints.

Proterial (formerly Hitachi Metals) remains a dominant force in NdFeB magnet technology, primarily through its NEOMAX® high-coercivity magnet line. These magnets maintain a BHmax > 40 MGOe at 150°C, offering robust thermal performance for traction motors and aerospace systems. Proterial’s Q2 2025 completion of a new Vietnam NdFeB processing facility significantly strengthens non-China capacity, supporting global OEMs seeking supply chain redundancy. Aligned with Hitachi’s Inspire 2027 sustainability strategy, Proterial is integrating Green Transformation (GX) principles targeting a 75% reduction in GHG emissions by 2030, positioning NEOMAX® as both high-performance and environmentally optimized.

VAC holds global leadership in amorphous and nanocrystalline soft magnetic materials, including its flagship VITROPERM® series. These materials deliver up to 75% switching loss reduction in EV on-board chargers, enabling compact system design. In November 2025, VAC partnered with Ucore and Aclara to develop a non-China mine-to-magnet supply chain, supporting Western production of SmCo and NdFeB magnets. VAC also supplies magnetic components for 80% of global MRI and CT scanner systems, demonstrating unmatched reliability in mission-critical applications.

Shin-Etsu Chemical maintains global dominance in rare-earth magnet production with vertically integrated refining and manufacturing assets. In Q4 2025, it introduced a new corrosion-resistant coating that extends NdFeB magnet lifetime in humid and high-vibration automotive environments by 15%. The company is also advancing Dy-reduced high-coercivity magnets, balancing cost stability with performance. Shin-Etsu’s magnets meet a stringent <2% demagnetization drift over 10 years, making them ideal for precision robotics and actuator systems.

TDK is a key supplier of soft magnetic ferrites, including EPCOS power ferrite cores used in inductors, transformers, and noise suppression components. Its November 2025 PZ-series ferrites provide 30% lower core loss at 2 MHz, supporting miniaturized high-speed power conversion in 5G infrastructure, EV chargers, and data centers. In Q3 2025, TDK expanded ferrite core production by 20% to meet surging demand from automotive sensor and power electronics markets.

Daido Steel is a leader in hot-deformed NdFeB magnets (Neoquench), offering superior thermal stability and radial magnetic orientation for high-torque EV motors. Its magnets retain up to 95% remanence at 180°C, outperforming conventional sintered NdFeB. A March 2025 cross-licensing agreement with a European automotive supplier accelerates adoption of its Dy-free magnet solutions, supporting EV platforms seeking reduced rare-earth dependency.

Arnold Magnetic Technologies provides ITAR-compliant magnet systems essential for aerospace and defense. Its Alnico 8 materials can operate at 540°C, offering unmatched thermal endurance for high-temperature sensors and turbine applications. Arnold also supplies cryogenic-compatible SmCo alloys capable of maintaining magnetic stability near 4 K, serving scientific and space applications. The company operates a U.S.-based rare-earth magnet recycling facility, reinforcing its strategy around circularity and domestic sourcing security.

Advanced Magnetic Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$29.2 Billion

|

|

Market Size (2035)

|

$67.9 Billion

|

|

Market Growth Rate

|

8.8%

|

|

Segments

|

By Material Type (Permanent Magnet Materials, Soft Magnetic Materials, Magnetostrictive Materials, Magnetocaloric Materials), By Manufacturing Process (Sintered Magnets, Bonded Magnets, Hot-Pressed Magnets), By Application – Permanent Magnets (EV Traction Motors, Wind Power Generators, Robotics & Automation, Hard Disk Drives, Medical Devices), By Application – Soft Magnetic Materials (Power Electronics, High-Frequency Inverters, Electric Motors, EMI Suppression), By Raw Material Focus (Rare-Earth Reduction Magnets, Pr-Rich Magnets, Rare-Earth-Free Magnets, Grain Boundary Diffusion Technology)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hitachi Metals (Resonac Group), VACUUMSCHMELZE GmbH & Co. KG, Shin-Etsu Chemical Co. Ltd., MP Materials Corp., TDK Corporation, Arnold Magnetic Technologies, JFE Steel Corporation, Daido Steel Co. Ltd., Advanced Technology & Materials Co. Ltd., Ugimag S.A., Niron Magnetics, Ningbo Yunsheng Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Magnetic Materials Market Segmentation

By Material Type

- Permanent Magnet Materials

- Rare Earth Magnets (NdFeB, SmCo)

- Ferrite Magnets

- Soft Magnetic Materials

- Soft Ferrites

- Silicon Steel

- Amorphous/Nanocrystalline Metals

- Magnetostrictive Materials

- Magnetocaloric Materials

By Manufacturing Process (Permanent)

- Sintered Magnets

- Bonded Magnets

- Hot-Pressed Magnets

By Application of Permanent Magnets

- Electric Vehicle (EV) Traction Motors

- Wind Power Generators

- Robotics & Automation

- Hard Disk Drives (HDDs)

- Medical Devices (MRI)

By Application of Soft Magnetic Materials

- Power Electronics (Inductors, Transformers)

- High-Frequency Inverters (EVs)

- Electric Motors (Stators/Rotors)

- EMI Suppression (Filters)

By Raw Material Focus

- Dysprosium (Dy) Reduction Magnets

- Praseodymium (Pr) Rich Magnets

- Iron Nitride (Fe16N2) Magnets (Rare Earth-Free)

- Grain Boundary Diffusion (GBD) Technology

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Advanced Magnetic Materials Suppliers

- Hitachi Metals, Ltd. (Resonac Group)

- VACUUMSCHMELZE GmbH & Co. KG (VAC)

- Shin-Etsu Chemical Co., Ltd.

- MP Materials Corp.

- TDK Corporation

- Arnold Magnetic Technologies

- JFE Steel Corporation

- Daido Steel Co., Ltd.

- Advanced Technology & Materials Co., Ltd. (AT&M)

- Ugimag S.A. (Demeter Group)

- Niron Magnetics

- Ningbo Yunsheng Co., Ltd.

*- List not Exhaustive