Soft Magnetic Powder Market Surges On High-Flux Materials For Electrification, Sic/Gan Devices & Advanced Magnetics

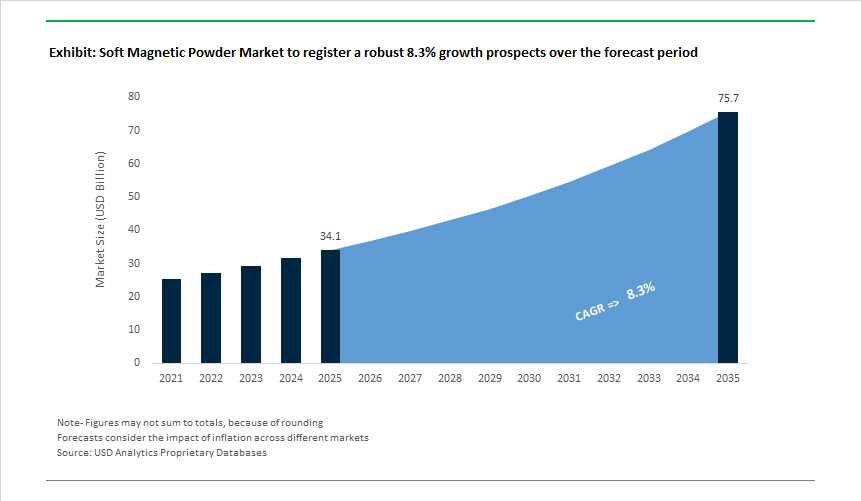

The Soft Magnetic Powder (SMP) market, valued at USD 34.1 billion in 2025, is projected to reach USD 75.7 billion by 2035, expanding at a CAGR of 8.3% as power electronics rapidly transition toward SiC/GaN high-frequency architectures, compact inductive components, and high-efficiency magnetic designs for EVs, renewable energy systems, and aerospace electrification. The shift to >50-500 kHz switching frequencies in next-generation converters is redefining material requirements, compelling manufacturers to engineer powders and Soft Magnetic Composites (SMCs) with ultra-low core loss, high saturation flux density, tailored permeability profiles, and robust DC-bias tolerance that suppress early saturation under high ripple currents.

OEMs are increasingly specifying SMP and SMC platforms capable of achieving <150 mW/cm³ core loss at 100 kHz/50 mT, Bsat values approaching 1.8 T in advanced iron-based alloys, and ≥50% permeability retention under 100 Oe DC bias, metrics that directly dictate inductor downsizing, thermal stability, and power density in high-frequency power stages. Manufacturers are also being evaluated on their ability to deliver powders compatible with press-and-sinter SMCs, molded inductors, direct-winding formats, and PCB-integrated magnetics, all of which require controlled particle size distribution, optimized insulation coatings, and high-temperature compaction binders. As EV traction inverters, on-board chargers, telecom power modules, and industrial drives continue to push toward miniaturization and higher efficiency, SMP suppliers face intensifying demand for thermally stable insulation layers, elevated resistivity, low magnetostriction, and heat-treated microstructures that maintain magnetic performance across wide temperature and frequency ranges.

Market Analysis: Product Launches, Aerospace Validation, EV Adoption and Capacity Expansions

The soft magnetic powder market is advancing across multiple fronts-material coatings and powder insulation, core loss reduction, higher saturation alloys, and large-scale capacity responses to automotive electrification. In September 2024, Sumitomo Electric unveiled a novel insulation coating for Soft Magnetic Composites that enabled direct copper winding, materially reducing axial-flux motor assembly size and cost and accelerating SMC adoption in next-generation EV motors. Building on material optimization, December 2024 saw TDK introduce XFlux® Ultra with roughly 20% core loss improvement, while December 2024 also featured TDK/TDK-class rivals developing high-temperature MnZn ferrites (PEM95) targeted at EV fast-charging transformers demanding thermal resilience.

Through 2025, R&D and industrial adoption intensified. In March 2025, Höganäs (Somaloy®) announced capital deployment to expand SMC production capacity-a direct response to accelerating demand from automotive electrification and industrial motors. Academic-industry breakthroughs in May 2025 produced an iron-based SMC with a novel insulation coating achieving resistivity >100 Ω·cm, suppressing eddy currents at ~500 kHz and marking a key step toward low-loss, high-frequency powder cores. In August 2025, a major EV motor OEM publicly adopted SMCs for an axial-flux stator, realizing ≈20% motor power-density gains due to 3-D flux path advantages. The tail end of 2025 saw material and application validation continue: October 2025 featured VAC qualifying high-saturation, low-loss CoFe alloys for compact e-flight motor components, and November 2025 brought Magnetics’ Kool Mμ Ultra line with improved DC bias and core-loss performance-indicating an industry shift from commodity ferrites to engineered powder and nanocrystalline solutions across e-mobility, aerospace, renewable inverters, and high-frequency power electronics.

Soft Magnetic Powder Market: Trends and Opportunities

High-Frequency, Low-Loss Iron-Based Composite Powders Power the WBG Transition

The rapid adoption of wide-bandgap (WBG) semiconductors—notably GaN and SiC—is forcing a fundamental redesign of magnetic materials as switching frequencies move from tens of kilohertz into the hundreds of kilohertz and MHz range. Traditional laminations and ferrites suffer unacceptable eddy-current losses under these conditions, accelerating the shift toward iron-based soft magnetic composite (SMC) powders with nanoscale insulation. In August 2025, peer-reviewed work demonstrated that Al₂O₃ sol-gel coatings on iron powders delivered a 71% reduction in core loss versus uninsulated particles; critically, calcination at 1100°C formed uniform α-Al₂O₃ shells that preserved a quality factor (Q) of ~94 at 1 MHz, enabling real miniaturization of high-power inductors.

Hybrid insulation stacks are compounding gains. 2025 studies confirmed that SiO₂–resin composite layers cut eddy-current losses by ~33% at 1 MHz, allowing “cool-running” converters compatible with the fast slew rates of GaN on-board chargers. Meanwhile, APTES surface modification is improving resin–powder compatibility in compacted cores, pushing magnetic efficiency toward ~99% up to 80 kHz and outperforming ferrites and dust cores in high-flux designs. Collectively, these advances mark a shift from material substitution to interface engineering, where coating chemistry and thickness control now dictate performance at frequency.

Vertical Integration Accelerates SMC Adoption in EV Traction Drives

Automotive Tier-1 suppliers are vertically integrating into SMC motor-core manufacturing to secure supply for axial-flux motors, whose 3D flux paths cannot be realized with laminated steels. Between mid-2024 and 2025, Sumitomo Electric Industries expanded mass production of SMC axial-flux cores—scaling from consumer electronics into automotive traction—meeting the efficiency and torque-density targets of next-gen EVs. This move shortens development cycles, stabilizes quality, and locks in powder specifications early in motor design.

Policy and geopolitics are reinforcing the trend. In June 2025, India’s Ministry of Heavy Industries launched incentives under the National Critical Minerals Mission to promote rare-earth-free motors, explicitly encouraging iron-based SMCs. The strategic rationale is clear: tariffs and neodymium constraints have lifted motor costs by an estimated 15–20%, while SMC architectures reduce reliance on rare-earth magnets without sacrificing power-to-weight ratios. As OEMs redesign traction drives around axial-flux topologies, powder-based soft magnets are transitioning from niche enablers to core drivetrain materials.

Ultra-High-Speed Motors Create a New Aerospace Pull for Soft Magnetic Powders

Electrification of aerospace systems—spanning More-Electric Aircraft (MEA), eVTOL, and electrified auxiliaries—demands motors that operate above 20,000 RPM and >10 kHz electrical frequencies under severe thermal and mechanical stress. Soft magnetic powders with high resistivity and isotropic flux capability are emerging as the preferred solution. August 2025 workshop data showed that motors built with cobalt-based nanocomposites and SMC powders achieved ~70% size reduction versus silicon steel designs, alongside an ~83% reduction in NdFeB magnet volume—a decisive advantage in mass-constrained airframes.

Component-level deployments are following. Arnold Magnetic Technologies is collaborating with Tier-1 aerospace suppliers to deploy thin-section Arnon™ silicon steels and SMCs in cabin air compressors and auxiliary power units (APUs), engineered to suppress parasitic eddy currents at high drive frequencies in pressurized environments. At the frontier, metal amorphous nanocomposite (MANC) powders targeted for 1–10 kHz switching are enabling high induction with stable losses—unlocking power densities previously achievable only with larger, liquid-cooled industrial drives.

Powder Cores Enable High-Power Wireless Charging and 3D Flux Control

As wireless EV charging scales from 7.2 kW residential systems to 50 kW+ public stations, the bottleneck has shifted to magnetic flux management in compact, misalignment-tolerant geometries. Spherical soft magnetic alloy powders (e.g., Fe-Si-Cr) are displacing flat laminations because they can be molded into complex 3D flux collectors that optimize coupling between ground pads and vehicle receivers. Technical disclosures in 2025 highlighted how powder cores improve field shaping and reduce leakage—critical for efficiency and safety at higher power.

Thermal stability under high flux further differentiates powders. Soft magnetic alloys maintain consistent permeability across wide temperature swings, supporting reliable operation in uncooled outdoor installations—a requirement that also benefits compact inductors in 5G and IoT infrastructure. With global EV sales accelerating in 2025, demand for low-coercivity powder cores is rising to minimize losses in the high-frequency transformers used for both static and dynamic (in-motion) wireless charging. The result is a clear opportunity for powder suppliers that can deliver geometry-enabled magnetics at scale.

Soft Magnetic Powder Market Share Analysis

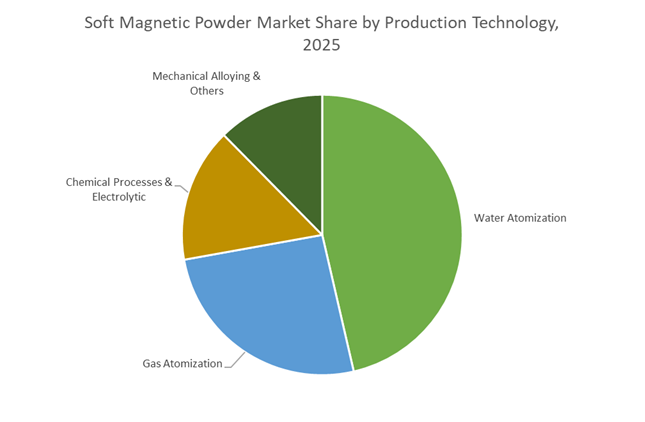

Market Share by Production Technology: Water Atomization Dominates High-Volume Magnetic Powder Supply

Water atomization accounts for approximately 45% of global production in the Soft Magnetic Powder Market, reflecting its position as the most commercially efficient and manufacturing-friendly powder production technology. This segment leads because water atomization produces irregularly shaped particles with an interlocking morphology, which directly improves the green strength of pressed components before sintering. Higher green strength enables manufacturers to handle and transport complex motor cores and magnetic parts with lower breakage risk, translating into measurable reductions in scrap rates and rework costs at scale. Market share is further reinforced by the cost efficiency of water atomization, as the use of water instead of inert gases significantly lowers operating expenses, making it the preferred choice for high-volume iron and iron-based soft magnetic powders. The technology’s ability to deliver a broad particle size distribution enhances powder packing density during compaction, resulting in higher final part density and improved magnetic flux performance—key drivers for motor and generator applications. Rapid cooling during atomization also contributes to fine-grained microstructures within individual particles, improving mechanical durability in finished magnetic cores. Together, these structural, economic, and processing advantages position water atomization as the workhorse production method underpinning the largest share of global soft magnetic powder supply.

Market Share by Application: Motors and Generators Drive Demand Through Electrification and Efficiency Gains

The motors and generators segment represents approximately 30% of total demand in the Soft Magnetic Powder Market, making it the largest and most strategically important application area. This dominance is directly tied to the global acceleration of electric vehicle adoption and industrial automation, where motor efficiency, compactness, and thermal performance are critical design priorities. Soft magnetic powders enable the production of soft magnetic composites (SMCs) with three-dimensional magnetic flux capabilities, allowing engineers to move beyond the limitations of traditional laminated steel designs. These 3D flux characteristics support more compact motor architectures and higher power density, which are especially valuable in space-constrained EV drivetrains. Market share is further strengthened by the reduction of eddy current losses at high operating frequencies, as insulated powder particles suppress energy losses that plague conventional laminations, delivering measurable efficiency gains in high-speed motors. The powder metallurgy process also minimizes material waste through near-net-shape manufacturing, improving cost competitiveness and sustainability metrics for OEMs. As electrification trends intensify and efficiency standards tighten, motors and generators remain the primary demand anchor for soft magnetic powders globally.

Competitive Landscape: Suppliers Defining Low-Loss, High-Bsat, Aand 3-D Flux Solutions

Market leadership is split between long-established ferrite and powder metallurgy houses, SMC specialists enabling net-shape magnetic circuits, and precision alloy makers producing nanocrystalline and Co-Fe high-saturation materials. Differentiation rests on powder chemistry, insulation/coating tech, compaction/sintering processes, frequency-loss optimization, and system-level collaboration with motor and power-electronics OEMs.

TDK Corporation - Material Heritage and End-To-End Integration For Gan/Sic Power Systems

TDK leverages 85+ years of magnetic materials expertise to produce advanced Mn-Zn ferrites (e.g., PEM95) and multilayer inductor solutions optimized for high-temperature, low-loss operation in EV fast chargers and renewable inverters. The company’s strength lies in atomic-level powder synthesis, sintering control, and electromagnetic simulation, enabling end-to-end component integration that aligns with GaN/SiC semiconductor roadmaps to minimize system losses and improve power density. TDK’s portfolio targets e-mobility and renewable energy sectors with materials engineered for thermal stability and high-frequency switching.

Höganäs AB - Somaloy® SMC Leader Enabling 3-D Flux Path Motors and Net-Shape Efficiency

Höganäs’ Somaloy® Soft Magnetic Composites are a market reference for electrically insulated iron powders that enable complex 3-D flux paths, net shaping via powder metallurgy, and reduced machining waste. Somaloy’s capacity expansion (announced March 2025) and product versatility (coated/uncoated powders, Fe-Si alloys) support axial-flux motor designs, compact industrial drives, and high-DC-bias inductors. Customers benefit from Somaloy’s ability to balance low magnetostriction (noise) and DC-bias permeability retention for high-current motor applications.

Magnetics (Spang & Company) - Precision Powder Cores and Continual Low-Loss Innovation

Magnetics offers a broad precision magnetic component range-Kool Mμ (Sendust), XFlux (Si-Fe), MPP and powder cores-with continual product refinements such as the Kool Mμ Ultra and XFlux® Ultra delivering improved DC bias and up to 20% lower core loss. Magnetics’ no-organic-binder powder core manufacturing prevents thermal aging and preserves long-term stability, making its materials attractive for high-reliability UPS, renewable inverters, and high-frequency power supplies where consistent performance across temperature ranges is mandatory.

VACUUMSCHMELZE (VAC) - Vacuum-Melted Nanocrystalline and Cofe Alloys For Ultra-High Bsat and E-Flight Motors

VAC’s vacuum-induction melting and precision alloying produce high-purity CoFe and nanocrystalline (VITROPERM®) materials with saturation flux densities up to ~2.4 T, enabling 20-30% higher power density in motors and generators versus electrical steel. Qualification of VACOFLUX® and related alloys for e-flight (announced Oct 2025) positions VAC as the supplier of choice for compact, high-power aerospace and scientific equipment where maximum Bsat, low loss, and tightly controlled magnetic properties are required. VAC’s full production-chain control allows tailor-made magnetic solutions for regulated, high-performance markets.

India’s soft magnetic powder market is entering a scale-up phase under the third round of the Production Linked Incentive (PLI 1.2) scheme, which explicitly prioritizes electrical steel and high-value specialty alloys used in soft magnetic composites (SMCs). By tying incentives to incremental sales over a five-year window, the program is reshaping procurement strategies for EV motors, traction inverters, and fast-charging infrastructure. The deployment of capital commitments toward specialty capacity is reducing dependence on imported high-grade iron powders and enabling localized production of low-loss materials suited for 800V EV architectures. From a supply-chain perspective, the scheme strengthens upstream security for amorphous and nanocrystalline powders, positioning India as a cost-competitive manufacturing base for regional automotive and energy OEMs.

United States’ Critical Minerals Strategy and Upstream Powder Security

The United States is anchoring its soft magnetic powder strategy in upstream resilience by linking mining, processing, and advanced materials manufacturing to national defense and grid modernization. Federal funding programs administered by U.S. Department of Energy are catalyzing pilot-scale processing for iron- and nickel-based alloys critical to amorphous powders with ultra-low core losses. The Critical Minerals and Materials Accelerator is fostering industry-led demonstrations to de-risk domestic atomization and spheroidization technologies. Concurrently, tariff impact reviews are reshaping sourcing for gas-atomized spherical powders used in aerospace and defense inductors, reinforcing a shift toward domestic suppliers capable of meeting stringent purity and performance specifications.

Japan’s Materials DX Platform and RE-Free Magnet Innovation

Japan continues to lead in high-permeability, low-loss soft magnetic materials by embedding data-driven discovery into materials R&D. The Materials Research DX Platform overseen by Ministry of Education, Culture, Sports, Science and Technology has reached full operational maturity, enabling machine-learning-led optimization of alloy chemistries for elevated temperature stability. Industry momentum is reinforced by workshops hosted by National Institute for Materials Science, where RE-free magnet pathways are being translated into manufacturable powder grades. Corporate expansions by Proterial and TDK in nanocrystalline powders are directly aligned with miniaturized power modules for 5G/6G infrastructure and high-frequency converters.

European Union (Germany & Finland): Green Steel Pathways and Circular Powder Supply

Across the European Union, decarbonization policy is intersecting with soft magnetic powder production through near-zero-carbon steelmaking and circularity incentives. Breakthrough funding under the Research Fund for Coal and Steel is de-risking hydrogen-based routes and electric arc furnace (EAF) transitions that generate low-emission feedstock suitable for SMC production. In Finland, projects led by Blastr Green Steel are establishing hydrogen-DRI-EAF capacity to supply recycled and low-carbon inputs for magnetic powders. EU-approved state aid further accelerates EAF adoption, improving the availability and quality of recycled magnetic scrap for domestic powder metallurgy.

China’s “Three-High” Focus and Electronic-Grade Powder Leadership

China remains the world’s largest producer and consumer of soft magnetic iron powders, with industrial policy emphasizing “High-quality, High-efficiency, High-end” development. Under the concluding 14th Five-Year Plan, dozens of R&D centers are advancing electronic-grade SMCs and nanocrystalline powders to meet surging domestic demand from 800V EV platforms. Capacity expansions in water and gas atomization across key provinces are supplying Sendust and iron–silicon–aluminum powders to global Tier-1 automotive suppliers. The Ministry of Industry and Information Technology 2025 guidelines further mandate intelligent manufacturing to cut atomization energy intensity, enhancing competitiveness while improving consistency for high-frequency power electronics.

National Strategic Incentives and Focus Areas (2025)

Soft Magnetic Powder Market Development Matrix by Country

|

Country / Region

|

Primary Policy or Program

|

Key Investment / Funding

|

Strategic Focus for Soft Magnetic Powders

|

|

India

|

PLI 1.2 (Specialty Steel)

|

₹43,874 Cr (~$5.2B) commitments

|

Electrical steel, SMCs, import substitution

|

|

United States

|

Critical Minerals Accelerator

|

$355M (Nov 2025)

|

Domestic mining, processing, amorphous powders

|

|

Japan

|

Materials Research DX Platform

|

Ongoing national funding

|

RE-free magnets, nanocrystalline powders

|

|

European Union

|

RFCS “Big Ticket” Calls

|

€175M (2025 budget)

|

Near-zero-carbon steel, circular powders

|

|

China

|

14th Five-Year Plan (“Three-High”)

|

Multi-center R&D rollout

|

Electronic-grade SMCs, EV power electronics

|

Soft Magnetic Powder Market Report Scope

Soft Magnetic Powder Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34.1 Billion

|

|

Market Size (2035)

|

$75.7 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Material Type (Soft Ferrite Powder, Carbonyl Iron Powder, Iron-Silicon Powder, Sendust Powder, Amorphous & Nanocrystalline Powder, Nickel-Iron Powder, Soft Magnetic Composites), By Production Technology (Water Atomization, Gas Atomization, Chemical Vapor Deposition, Mechanical Alloying, Electrolytic Process), By Application (Motors & Generators, Transformers, Inductors & Chokes, Sensors & Actuators, Wireless Power Transfer), By End-User Industry (Automotive, Consumer Electronics, Telecommunications, Renewable Energy, Aerospace & Defense, Industrial Automation & Robotics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Höganäs AB, GKN Powder Metallurgy, BASF SE, Proterial Ltd., JFE Steel Corporation, VACUUMSCHMELZE GmbH & Co. KG, Rio Tinto Metal Powders, Kyocera Corporation, Magnetics, TDK Corporation, Arnold Magnetic Technologies, Jiangxi Yuean Advanced Materials Co., Ltd., Sandvik AB, Sumitomo Electric Industries Ltd., Daido Steel Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Soft Magnetic Powder Market Segmentation

By Material Type

- Soft Ferrite Powder

- Carbonyl Iron Powder

- Iron-Silicon Powder

- Sendust Powder

- Amorphous and Nanocrystalline Powder

- Nickel-Iron Powder

- Soft Magnetic Composites

By Production Technology

- Water Atomization

- Gas Atomization

- Chemical Vapor Deposition

- Mechanical Alloying

- Electrolytic Process

By Application

- Motors and Generators

- Transformers

- Inductors and Chokes

- Sensors and Actuators

- Wireless Power Transfer

By End-User Industry

- Automotive

- Consumer Electronics

- Telecommunications

- Renewable Energy

- Aerospace and Defense

- Industrial Automation and Robotics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Soft Magnetic Powder Market

- Höganäs AB

- GKN Powder Metallurgy

- BASF SE

- Proterial, Ltd.

- JFE Steel Corporation

- VACUUMSCHMELZE GmbH & Co. KG

- Rio Tinto Metal Powders

- Kyocera Corporation

- Magnetics

- TDK Corporation

- Arnold Magnetic Technologies

- Jiangxi Yuean Advanced Materials Co., Ltd.

- Sandvik AB

- Sumitomo Electric Industries, Ltd.

- Daido Steel Co., Ltd.

*- List not Exhaustive