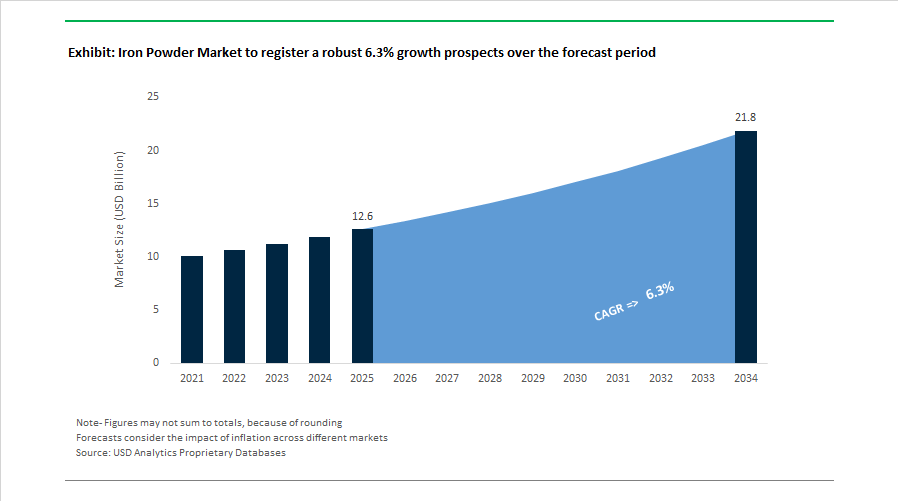

Iron Powder Market to Reach $21.8 Billion by 2034 as EV Drivetrains and Green Metallurgy Reshape Powder Metallurgy Value Chains

The Iron Powder Market is projected to expand from $12.6 billion in 2025 to $21.8 billion by 2034, registering a CAGR of 6.3%. Structural growth is being driven by electrified automotive platforms, hydrogen infrastructure, renewable energy systems, and the transition toward low-carbon metallurgical processes. Iron powder is no longer confined to traditional press-and-sinter automotive parts; it is increasingly positioned as a functional material for filtration, electrolysis, advanced alloys, and additive manufacturing.

A defining inflection point occurred on February 3, 2026, when Dauch Corporation finalized the acquisition of Dowlais Group plc, including its subsidiary GKN Powder Metallurgy. This transaction consolidates one of the world’s largest iron powder technology platforms under a driveline-focused industrial group, strengthening integration between powder metallurgy components and next-generation EV propulsion systems. GKN’s 2024 launch of advanced Porous Transport Layers (PTL) for hydrogen electrolysis illustrates the strategic pivot toward green energy infrastructure, where precision iron powders enable proton exchange membrane efficiency and durability. In June 2025, GKN further diversified into high-value industrial filtration with its new metallic membrane cartridge filters, highlighting the migration of iron powders into chemical processing and food-grade separation markets.

Sustainability is rapidly becoming a competitive differentiator. In June 2025, Höganäs introduced re-Astaloy 85 Mo, a carbon-reduced iron powder produced using recycled feedstock and enhanced environmental controls. Earlier, in January 2025, its Busan facility became the company’s first plant to operate entirely on solar power, signaling a broader decarbonization of atomization and reduction processes. Höganäs reinforced this strategy in March 2025 through a partnership with Porite Taiwan to develop near-zero sponge iron powder for high-precision electronics and automotive components. Meanwhile, Rio Tinto advanced its BlueSmelting™ technology throughout 2024–2025, targeting a 95% reduction in greenhouse gas emissions relative to conventional methods. Complementing this, Rio Tinto and Aymium formed Évolys Québec Inc. to produce renewable biocarbon as a substitute for fossil-based reductants in iron production.

Asia is emerging as a strategic production hub. In December 2025, JFE Steel and JSW Steel finalized an integrated steel joint venture in India, incorporating high-grade industrial powder and electrical steel production to support both domestic EV growth and export markets. In April 2025, JFE commenced hydrogen-based steelmaking trials at its Kurashiki facility, constructing a large-scale electric arc furnace under Japan’s hydrogen utilization initiative. Hydrogen-reduced iron feedstock is expected to become critical for premium atomized powders requiring ultra-low impurity levels.

Innovation pipelines are broadening the application base. Höganäs’ September 2025 launch of the global “PowdrIQ” challenge reflects an effort to accelerate iron powder adoption in renewable energy storage and advanced filtration systems. Concurrently, Rio Tinto and the Canada Growth Fund invested C$25 million to expand scandium oxide production at Sorel-Tracy in November 2025, integrating with its iron operations to produce high-purity alloy powders for aerospace and energy applications.

The iron powder market is transitioning from a volume-driven automotive supply segment into a technology-intensive materials platform aligned with electrification, hydrogen systems, and low-carbon manufacturing. Vertical integration, hydrogen metallurgy, renewable energy adoption, and advanced functional applications are redefining the competitive landscape, positioning iron powders as a foundational material in the decarbonized industrial economy.

Iron Powder Market Share and Segmentation Insights

Atomized Iron Powder Leads the Market Through Superior Particle Uniformity for Powder Metallurgy

Atomized iron powder accounted for 48.60% of the Iron Powder Market share in 2025, making it the most widely used iron powder type across industrial applications. Atomized iron powders are produced through water or gas atomization processes, where molten iron is dispersed into fine droplets that rapidly solidify into uniform powder particles. This production method enables precise control of particle size distribution, improved purity levels, and consistent particle morphology, characteristics essential for high-performance powder metallurgy manufacturing. Atomized powders exhibit excellent compressibility, flowability, and sintering behavior, making them ideal for producing structural components through powder compaction and sintering techniques. In 2025, ongoing improvements in water atomization technology have significantly enhanced powder performance, enabling manufacturers to produce powders with higher green strength and improved densification during sintering. These advancements allow powder metallurgy producers to manufacture complex automotive and industrial components with higher mechanical strength and tighter dimensional tolerances, reinforcing the dominance of atomized iron powder in global metal powder supply chains.

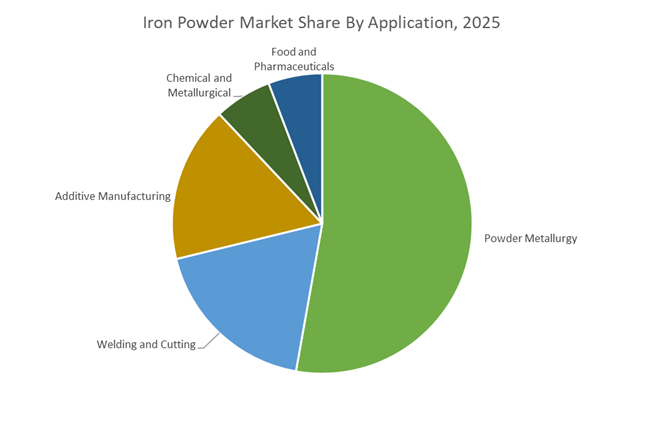

Powder Metallurgy Applications Drive the Largest Consumption of Iron Powder

Powder metallurgy accounted for 52.80% of the Iron Powder Market share in 2025, positioning it as the dominant application for iron powder consumption. Powder metallurgy manufacturing processes involve compacting metal powders into precise shapes followed by sintering, enabling production of complex metal components with minimal material waste and high dimensional accuracy. The technology is widely used for manufacturing automotive components such as gears, sprockets, connecting rods, bearings, and transmission parts, where high production volumes and consistent mechanical properties are essential. Compared with traditional casting or machining processes, powder metallurgy offers significant advantages including near-net shape manufacturing, reduced machining requirements, improved material utilization, and lower production costs. In 2025, the global transition toward electric vehicles (EVs) and electrified powertrains is reshaping demand patterns within powder metallurgy applications. While some internal combustion engine components decline, new opportunities have emerged for powder metallurgy components used in electric motor assemblies, transmission systems, and soft magnetic composite materials, supporting the evolving requirements of next-generation automotive and industrial machinery manufacturing.

Competitive Landscape in Iron Powder Market

Höganäs AB Drives Sustainable Powder Metallurgy Innovation

Höganäs AB remains the global volume leader in iron and metal powders, with a diversified portfolio spanning thousands of grades for press and sinter, brazing, surface coating, induction heating, and soft magnetic applications. In September 2025, the company launched PowdrIQ, a global university innovation challenge designed to uncover sustainable industrial applications for metal powders, reinforcing its long-term R&D pipeline. In June 2025, Höganäs introduced re-Astaloy 85 Mo, the first in its re-portfolio line, combining recycled content with low-carbon production methods while maintaining high metallurgical performance. For 2026, the company is accelerating its transition toward Soft Magnetic Composites and additive manufacturing powders, aligning with vehicle electrification, axial motor design, and lightweighting strategies. Its leadership in sustainable powder metallurgy and circular raw material sourcing underpins strong positioning in the evolving EV-driven iron powder landscape.

GKN Powder Metallurgy Expands High-Performance Atomized Powder Capabilities

GKN Powder Metallurgy, through its Hoeganaes division maintains a dominant position in North America’s press and sinter segment. Known for its Ancor series of atomized iron powders, the company supplies high-compressibility, low-impurity materials critical for high-density components in electric vehicle transmissions and industrial machinery. In 2026, GKN strengthened its additive manufacturing alignment, expanding beyond automotive into aerospace and medical powder metallurgy applications. The company is reinforcing supply chain capacity for fine powder grades below 20 microns to address rising demand in the metal injection molding segment, which is growing at approximately 7.2% annually. Its focus on advanced atomization, high-density sintering, and application engineering supports continued leadership in high-performance structural components.

JFE Steel Corporation Advances Decarbonized Iron Powder Technologies

JFE Steel Corporation is transitioning its iron powder operations from volume-based output to high-value, carbon-neutral technologies under its 8th Medium-term Business Plan. In January 2026, JFE adopted its JGreeX green steel technology in advanced automotive applications, including integration into the Nissan New LEAF platform. In February 2026, its high-alloy seamless OCTG powders were selected for casing applications in the Tomakomai Carbon Capture and Storage project, reinforcing its capability in demanding energy infrastructure environments. The company is advancing decarbonized powder metallurgy initiatives and exploring iron fuel technologies as recyclable energy carriers for heavy industry. By leveraging Japan’s advanced steelmaking expertise, JFE is positioning itself as a premium supplier of high-purity iron powders across APAC.

Kobe Steel Expands Magnetic and Environmental Iron Powder Applications

Kobe Steel, operating under the Kobelco brand, is strengthening its presence in soft magnetic and advanced materials segments. In 2026, the company expanded its MAGMEL soft magnetic iron powder range with high-heat-resistant insulated coatings that enable elevated temperature magnetic annealing, reducing iron loss in electric vehicle motors. Through its ECOMEL product line, Kobe Steel markets specialized iron powders for soil and groundwater remediation, targeting volatile organic compound degradation and heavy metal adsorption. Financially, the company is prioritizing high-value-added advanced materials to mitigate energy price volatility and improve profitability. Its strategic emphasis on three-dimensional magnetic design supports compact axial gap motor architectures, enabling lighter and more efficient mobility solutions.

Pometon S.p.A. Strengthens Circular Economy and Custom Powder Solutions

Pometon S.p.A. has established itself as a European specialist in custom iron powders and circular economy production. In 2025 and 2026, the company developed high-purity iron powders derived entirely from recycled scrap sources, supporting sustainability goals in chemical processing and magnetic component applications. In March 2026, Pometon showcased ready-to-press copper and iron powders at major trade fairs to support electric vehicle infrastructure and solar panel manufacturing growth in Europe. Its October 2025 expansion of additive manufacturing alloys introduced customized iron powder grades tailored for binder jetting and powder bed fusion technologies. The company’s capability to engineer specific particle morphology and chemistry for industrial clients differentiates it in niche high-performance metallurgical markets.

Rio Tinto Metal Powders Influences High-Purity Iron Precursor Supply

Rio Tinto has transitioned away from direct metallic powder production but remains influential in the iron powder supply chain through high-purity iron and ilmenite extraction operations in Quebec and South Africa. In December 2025, the company formalized its strategic pivot toward upstream mineral extraction while maintaining its legacy technical influence in foundry metallurgy. A $473 million investment approved in March 2026 for the Zulti South project ensures mineral sands supply continuity through 2050. Rio Tinto is advancing sustainability initiatives by extracting scandium oxide from waste streams at its Quebec operations without additional mining activity. Its Sorelmetal technical standards continue to guide ductile iron and high-purity precursor development globally.

Sweden Iron Powder Market: Biochar Transition and Fossil-Free Reduction Pathways

Sweden continues to set the global benchmark for low-carbon iron powder production, driven by early-stage infrastructure investments and science-based decarbonization targets. In 2025, Höganäs AB initiated construction of a dedicated biochar receiving and handling facility to replace approximately 20% of fossil coal used in sponge iron reduction. Full process integration is scheduled for 2026 and is designed to materially lower direct CO₂ emissions while maintaining metallurgical consistency required for powder metallurgy and additive manufacturing applications. This move aligns closely with customer demand from automotive and industrial OEMs seeking verifiable Scope 3 emission reductions in their supply chains.

Parallel R&D programs are accelerating Sweden’s long-term decarbonization roadmap. Ongoing projects are testing higher biochar substitution ratios and evaluating fossil-free hydrogen reduction routes with the explicit objective of achieving near-zero direct emissions by 2030 under Science Based Targets initiative alignment. Beyond metallurgy, Sweden is also positioning iron powder as a strategic material for future energy systems. Collaborative research programs are exploring iron powder as a recyclable energy carrier for long-duration storage, leveraging its high volumetric energy density and closed-loop recyclability. Talent development is being treated as a structural enabler, with targeted programs launched in 2025 to build expertise in soft magnetic composites, surface-engineered powders, and additive manufacturing feedstocks.

China Iron Powder Market: Policy-Driven Restructuring and Scrap-Centric Supply

China’s iron powder industry is undergoing structural realignment under coordinated industrial, environmental, and resource-efficiency policies. A joint 2025–2026 steel sector work plan issued by five ministries mandates a transition away from blast furnace dependency toward electric arc furnaces and hydrogen metallurgy. This policy shift is directly influencing iron powder production routes, favoring recycled feedstocks and cleaner reduction technologies to curb systemic overcapacity. Complementing this, the Ministry of Ecology and Environment formally expanded the national carbon market in 2025 to include steel and metals, placing iron powder producers under absolute emissions caps extending to 2030.

Material innovation is being steered from the top down. The 2026 government action plan prioritizes ultra-high purity and application-specific iron powders for electric vehicles, electronics, and information technology hardware. Scrap utilization is emerging as a decisive lever, with the National Development and Reform Commission setting a target of 300 million tonnes of scrap steel utilization by 2025–2026. This policy directly feeds high-efficiency recycling streams into recycled-grade iron powder production, improving both cost structure and carbon intensity. As a result, Chinese producers are increasingly integrating sorting, refining, and atomization systems capable of converting heterogeneous scrap into controlled particle-size powders suitable for sintering and magnetic applications.

United States Iron Powder Market: Additive Manufacturing Scale-Up and Strategic Reshoring

The U.S. iron powder landscape is being reshaped by additive manufacturing scale-up and national security-driven supply chain policies. In 2025, the Department of Energy and private-sector leaders such as GKN Additive demonstrated serial production of high-performance metal additive manufacturing components at Formnext, underscoring the readiness of iron-based powders for aerospace and advanced industrial uses. These demonstrations highlighted powder consistency and sub-micron dimensional control as critical differentiators for next-generation applications.

At the policy level, Defense Production Act mechanisms are accelerating the reshoring of iron ore processing and powder metallurgy capacity to secure domestic electric vehicle supply chains and energy-efficient transmission infrastructure. Federal financing approvals in 2025–2026 are enabling new investments across atomization, reduction, and finishing stages. While indirect, the Iofina and Western Midstream collaboration in the Permian Basin is contributing to this ecosystem by strengthening the domestic availability of chemical reagents used in powder processing, with new plant capacity scheduled for commissioning in Q3 2026. Collectively, these moves signal a strategic pivot toward vertically integrated, domestically controlled iron powder supply.

Japan Iron Powder Market: Digital Sintering Control and Electronic-Grade Precision

Japan’s iron powder sector is advancing through process digitization and a pivot toward high-purity electronic grades. In late 2025, JFE Steel began deploying Cyber-Physical System technology across its sintering operations. This integration of real-time process data and predictive control is stabilizing powder quality while simultaneously reducing greenhouse gas emissions through optimized thermal profiles. Complementary sensor deployments introduced in December 2025 enable continuous measurement of granule size on conveyors, improving feedstock consistency and sintering efficiency.

Market orientation is also shifting. Japanese producers are reallocating capacity toward spherical iron powders engineered for inductors and electromagnetic interference shielding. These materials are increasingly critical for advanced electronics and are aligned with Japan’s anticipated 2026 rollout of next-generation 6G infrastructure. The emphasis on particle morphology, purity, and magnetic performance positions Japan as a premium supplier for electronics-driven iron powder demand rather than bulk structural applications.

India Iron Powder Market: Capacity Expansion and Circular Manufacturing Models

India’s iron powder industry is scaling rapidly on the back of joint ventures, circular manufacturing practices, and policy incentives. In December 2025, JSW Steel and JFE Steel finalized an integrated steel plant joint venture that significantly expands domestic capacity for electrical steel and related iron powder components. This development strengthens India’s position as a regional hub for motor cores and energy-efficient electrical systems.

Simultaneously, domestic manufacturers are adopting abrasion-based and thermal oxidation techniques to convert machining waste into spherical iron powders, embedding circular economy principles into automotive and industrial clusters. The government’s Production-Linked Incentive Scheme 2.0 for specialty chemicals and advanced materials is accelerating investment in atomization plants capable of producing pharmaceutical- and food-grade high-purity iron powders. These combined drivers are shifting India from a primarily import-dependent market to a value-added producer with export ambitions.

Austria Iron Powder Market: Hydrogen Metallurgy as a Blueprint

Austria is emerging as a testbed for hydrogen-based ironmaking technologies with direct implications for future iron powder supply. In September 2025, a consortium including voestalpine and Rio Tinto launched a hydrogen-based ironmaking pilot plant in Linz. Designed as a pre-commercial blueprint, the facility produces low-carbon iron intermediates suitable for downstream powder metallurgy. The project is widely viewed as a reference model for scaling green hydrogen reduction routes across Europe, particularly for applications where carbon intensity thresholds are tightening under EU climate frameworks.

Iron Powder Industry: Country-Level Strategic Snapshot

Iron Powder Market County Level Snapshot

|

Country

|

Primary Strategic Focus

|

Key Industrial Lever

|

Directional Impact

|

|

Sweden

|

Biochar and hydrogen reduction

|

Sponge iron decarbonization

|

Near-zero emission powder pathways

|

|

China

|

Policy-led restructuring

|

Scrap utilization and carbon markets

|

Cleaner, recycled-grade powders

|

|

United States

|

Additive manufacturing and reshoring

|

Federal financing and AM scale-up

|

Domestic supply security

|

|

Japan

|

Digital process control

|

Electronic-grade powder precision

|

High-purity, high-value segments

|

|

India

|

Capacity expansion and circularity

|

Joint ventures and PLI incentives

|

Regional manufacturing hub

|

|

Austria

|

Hydrogen-based ironmaking

|

Pilot-scale green metallurgy

|

Blueprint for low-carbon powders

|

Iron Powder Market Report Scope

Iron Powder Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.6 Billion

|

|

Market Size (2034)

|

$21.8 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Type (Reduced Iron Powder, Atomized Iron Powder, Electrolytic Iron Powder, Carbonyl Iron Powder), By Purity Level (High Purity, Standard Purity), By Particle Shape (Spherical, Irregular, Flake), By Application (Powder Metallurgy, Additive Manufacturing, Welding and Cutting, Chemical and Metallurgical, Food and Pharmaceuticals), By End-Use Industry (Automotive and Transportation, Industrial Machinery, Electronics and Electrical, Aerospace and Defense, Healthcare and Medical Devices, Food and Beverage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Höganäs AB, GKN Powder Metallurgy, Rio Tinto Metal Powders, JFE Steel Corporation, BASF SE, Kobe Steel, Ltd., Kymera International, Makin Metal Powders, American Elements, Pometon S.p.A., Sandvik AB, Sinvat S.A., Industrial Metal Powders Pvt. Ltd., Laiwu Iron and Steel Group, CNPC Powder Group Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Iron Powder Market Segmentation

By Type

- Reduced Iron Powder

- Atomized Iron Powder

- Electrolytic Iron Powder

- Carbonyl Iron Powder

By Purity Level

- High Purity

- Standard Purity

By Particle Shape

- Spherical

- Irregular

- Flake

By Application

- Powder Metallurgy

- Additive Manufacturing

- Welding and Cutting

- Chemical and Metallurgical

- Food and Pharmaceuticals

By End-Use Industry

- Automotive and Transportation

- Industrial Machinery

- Electronics and Electrical

- Aerospace and Defense

- Healthcare and Medical Devices

- Food and Beverage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Iron Powder Industry

- Höganäs AB

- GKN Powder Metallurgy

- Rio Tinto Metal Powders

- JFE Steel Corporation

- BASF SE

- Kobe Steel, Ltd.

- Kymera International

- Makin Metal Powders

- American Elements

- Pometon S.p.A.

- Sandvik AB

- Sinvat S.A.

- Industrial Metal Powders Pvt. Ltd.

- Laiwu Iron and Steel Group

- CNPC Powder Group Co., Ltd.

*- List not Exhaustive