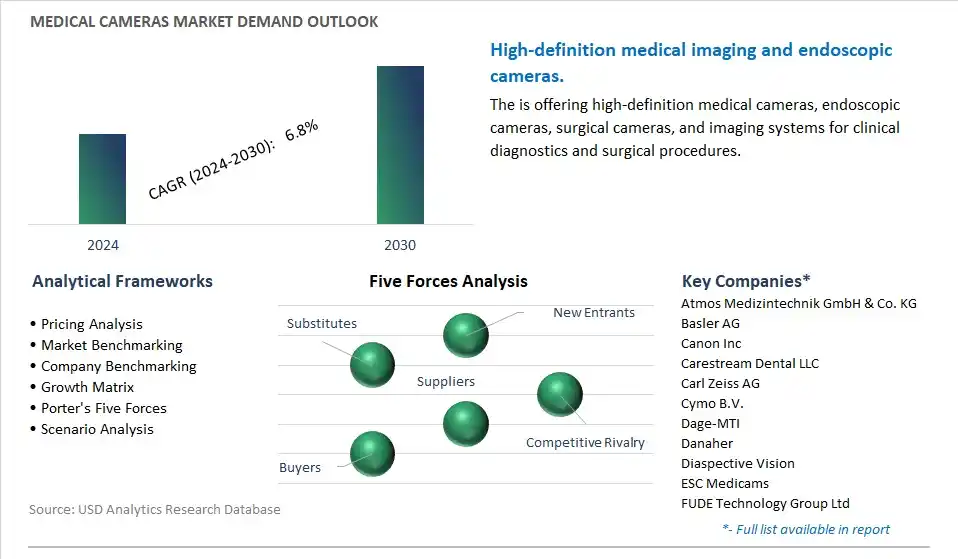

Medical Cameras Market is estimated to increase at a Compounded Annual Growth Rate of 6.8% CAGR over the forecast period from 2024 to 2030

The Medical Cameras Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By Type (Endoscopy Cameras, Dermatology Cameras, Ophthalmology Cameras, Dental Cameras, Surgical Microscopy Cameras, Others), By Sensor (CMOS Sensors, CCD Sensors), By Resolution (Standard Definition (SD) Cameras, High-definition (HD) Cameras), By End-User (Hospitals & Ambulatory Surgery Centers, Specialty Clinics).

An Introduction to Medical Cameras Market in 2024

Medical cameras are specialized imaging devices designed for capturing high-quality images and videos of anatomical structures, surgical procedures, and medical conditions for diagnostic, documentation, and educational purposes. In 2024, medical cameras continue to be indispensable tools in various medical specialties, including dermatology, ophthalmology, endoscopy, surgery, and radiology, providing healthcare professionals with detailed visual information to aid in diagnosis, treatment planning, and monitoring of patient outcomes. Medical cameras come in different forms and configurations to meet the specific needs and requirements of different medical applications. For instance, dermatological cameras are equipped with high-resolution sensors and polarized light filters to capture detailed images of the skin for the diagnosis and monitoring of skin conditions such as melanoma, psoriasis, and eczema. Ophthalmic cameras, including fundus cameras and slit-lamp cameras, are used to capture images of the eye's internal structures, such as the retina and cornea, to diagnose eye diseases like glaucoma, diabetic retinopathy, and macular degeneration. Endoscopic cameras are integrated into endoscopic instruments and used to visualize internal organs and tissues during minimally invasive procedures such as laparoscopy, arthroscopy, and colonoscopy, enabling surgeons to perform precise interventions with minimal trauma to the patient. Surgical cameras are designed to withstand sterilization and provide high-definition imaging in operating rooms, allowing surgeons to visualize the surgical field and monitor the progress of procedures such as open surgeries, microsurgeries, and robotic-assisted surgeries. Additionally, medical cameras are used in radiology for capturing medical images such as X-rays, CT scans, MRI scans, and ultrasound scans for diagnostic purposes and treatment planning. With advancements in imaging technology, medical cameras offer features such as autofocus, image stabilization, real-time video streaming, and wireless connectivity, enhancing their usability and functionality in clinical practice. By providing clear and accurate visual documentation of medical conditions and procedures, medical cameras support clinical decision-making, patient education, and interdisciplinary communication among healthcare teams, ultimately improving patient care and outcomes.

Market Trend: Increasing Adoption of High-Resolution and Specialty Cameras

A significant trend in the Medical Cameras market is the increasing adoption of high-resolution and specialty cameras for medical imaging applications. Healthcare providers and medical professionals are seeking advanced imaging solutions capable of capturing detailed and high-quality images for diagnosis, treatment planning, and surgical procedures. High-resolution cameras with enhanced image clarity and resolution enable healthcare professionals to visualize anatomical structures, pathology, and physiological processes with greater precision and accuracy. Additionally, specialty cameras designed for specific medical applications, such as endoscopy, ophthalmology, and microscopy, offer tailored imaging solutions optimized for different clinical scenarios. As medical imaging technology continues to advance, the demand for high-resolution and specialty cameras in various medical specialties is expected to grow, driving market expansion and innovation in camera design and functionality.

Market Driver: Technological Advancements and Miniaturization

A key driver fueling the Medical Cameras market is the continuous technological advancements and miniaturization of camera technologies. Innovations in sensor technology, image processing algorithms, and optical design have led to the development of smaller, lighter, and more versatile medical cameras that offer superior imaging performance and portability. Miniaturized medical cameras enable minimally invasive procedures, such as laparoscopy, arthroscopy, and endoscopy, by providing compact and maneuverable imaging solutions that can be easily integrated into surgical instruments and medical devices. Furthermore, advancements in wireless connectivity and digital imaging technologies facilitate real-time image transmission and remote viewing, enhancing collaboration between healthcare providers and enabling telemedicine applications. As technological advancements drive the development of miniaturized and connected medical cameras, the demand for these innovative imaging solutions in healthcare settings is expected to increase, propelling market growth and adoption of medical camera systems.

Market Opportunity: Integration of Artificial Intelligence (AI) and Machine Learning (ML) Algorithms

A potential opportunity in the Medical Cameras market lies in the integration of artificial intelligence (AI) and machine learning (ML) algorithms for image analysis and interpretation. AI-powered medical cameras equipped with intelligent image processing capabilities can automatically analyze and interpret medical images, detect abnormalities, and assist healthcare professionals in diagnosis and decision-making. AI algorithms can enhance image quality, remove artifacts, and highlight relevant features, improving the diagnostic accuracy and efficiency of medical imaging procedures. Additionally, ML algorithms trained on large datasets of medical images can learn to recognize patterns, predict disease outcomes, and personalize treatment plans based on individual patient characteristics. By integrating AI and ML capabilities into medical cameras, manufacturers can offer advanced imaging solutions that streamline workflow, enhance diagnostic capabilities, and improve patient outcomes. Expanding into AI-powered medical cameras presents a strategic opportunity for stakeholders to differentiate their offerings, address unmet clinical needs, and drive innovation in the rapidly evolving landscape of medical imaging technology.

Medical Cameras Market Share Analysis: Endoscopy Cameras is the fastest growing segment over the forecast period to 2030

Among the segments of the Medical Cameras Market, Endoscopy Cameras emerge as the fastest-growing category. This accelerated growth is propelled by several factors. Endoscopy cameras play a crucial role in minimally invasive surgical procedures and diagnostic examinations, allowing healthcare professionals to visualize internal organs and tissues with high clarity and precision. The increasing prevalence of minimally invasive surgeries, driven by benefits such as reduced postoperative pain, shorter recovery times, and improved patient outcomes, fuels the demand for endoscopy cameras in hospitals and ambulatory surgery centers. Additionally, advancements in endoscopic imaging technology, including high-definition (HD) cameras and CMOS sensor technology, enhance the quality and detail of endoscopic images, facilitating more accurate diagnosis and treatment. Moreover, the expansion of specialty clinics specializing in endoscopic procedures further drives the adoption of endoscopy cameras. As healthcare providers continue to prioritize minimally invasive approaches and advanced imaging capabilities, the Endoscopy Cameras segment experiences rapid growth, shaping the landscape of the Medical Cameras Market.

Medical Cameras Competitive Analysis

The market research study provides in-depth insights into leading companies including the SWOT analyses, product profile, financial details, and recent developments acrossAtmos Medizintechnik GmbH & Co. KG, Basler AG, Canon Inc, Carestream Dental LLC, Carl Zeiss AG, Cymo B.V., Dage-MTI, Danaher, Diaspective Vision, ESC Medicams, FUDE Technology Group Ltd, Haag-Streit Group, Healthtech Engineers Private Ltd, IDS Imaging Development Systems GmbH, Imperx Inc, Medicam, Olympus Corp, Optomed Plc, Richard Wolf GmbH, Schölly Fiberoptic GmbH, Smith & Nephew, Sony Corp, Stryker Corp, Tonglu Kanger Medical Instrument Co. Ltd, Topcon Corp

Medical Cameras Market Segmentation

By Type

Endoscopy Cameras

Dermatology Cameras

Ophthalmology Cameras

Dental Cameras

Surgical Microscopy Cameras

Others

By Sensor

CMOS Sensors

CCD Sensors

By Resolution

Standard Definition (SD) Cameras

High-definition (HD) Cameras

By End-User

Hospitals & Ambulatory Surgery Centers

Specialty Clinics

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Medical Cameras Market Companies

Atmos Medizintechnik GmbH & Co. KG

Basler AG

Canon Inc

Carestream Dental LLC

Carl Zeiss AG

Cymo B.V.

Dage-MTI

Danaher

Diaspective Vision

ESC Medicams

FUDE Technology Group Ltd

Haag-Streit Group

Healthtech Engineers Private Ltd

IDS Imaging Development Systems GmbH

Imperx Inc

Medicam

Olympus Corp

Optomed Plc

Richard Wolf GmbH

Schölly Fiberoptic GmbH

Smith & Nephew

Sony Corp

Stryker Corp

Tonglu Kanger Medical Instrument Co. Ltd

Topcon Corp

Reasons to Buy the Medical Cameras Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Medical Cameras Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Medical Cameras Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Medical Cameras Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Medical Cameras Market Size Outlook, $ Million, 2021 to 2030

3.2 Medical Cameras Market Outlook by Type, $ Million, 2021 to 2030

3.3 Medical Cameras Market Outlook by Product, $ Million, 2021 to 2030

3.4 Medical Cameras Market Outlook by Application, $ Million, 2021 to 2030

3.5 Medical Cameras Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Medical Cameras Industry

4.2 Key Market Trends in Medical Cameras Industry

4.3 Potential Opportunities in Medical Cameras Industry

4.4 Key Challenges in Medical Cameras Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Medical Cameras Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Medical Cameras Market Outlook by Segments

7.1 Medical Cameras Market Outlook by Segments, $ Million, 2021- 2030

By Type

Endoscopy Cameras

Dermatology Cameras

Ophthalmology Cameras

Dental Cameras

Surgical Microscopy Cameras

Others

By Sensor

CMOS Sensors

CCD Sensors

By Resolution

Standard Definition (SD) Cameras

High-definition (HD) Cameras

By End-User

Hospitals & Ambulatory Surgery Centers

Specialty Clinics

8 North America Medical Cameras Market Analysis and Outlook To 2030

8.1 Introduction to North America Medical Cameras Markets in 2024

8.2 North America Medical Cameras Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Medical Cameras Market size Outlook by Segments, 2021-2030

By Type

Endoscopy Cameras

Dermatology Cameras

Ophthalmology Cameras

Dental Cameras

Surgical Microscopy Cameras

Others

By Sensor

CMOS Sensors

CCD Sensors

By Resolution

Standard Definition (SD) Cameras

High-definition (HD) Cameras

By End-User

Hospitals & Ambulatory Surgery Centers

Specialty Clinics

9 Europe Medical Cameras Market Analysis and Outlook To 2030

9.1 Introduction to Europe Medical Cameras Markets in 2024

9.2 Europe Medical Cameras Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Medical Cameras Market Size Outlook by Segments, 2021-2030

By Type

Endoscopy Cameras

Dermatology Cameras

Ophthalmology Cameras

Dental Cameras

Surgical Microscopy Cameras

Others

By Sensor

CMOS Sensors

CCD Sensors

By Resolution

Standard Definition (SD) Cameras

High-definition (HD) Cameras

By End-User

Hospitals & Ambulatory Surgery Centers

Specialty Clinics

10 Asia Pacific Medical Cameras Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Medical Cameras Markets in 2024

10.2 Asia Pacific Medical Cameras Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Medical Cameras Market size Outlook by Segments, 2021-2030

By Type

Endoscopy Cameras

Dermatology Cameras

Ophthalmology Cameras

Dental Cameras

Surgical Microscopy Cameras

Others

By Sensor

CMOS Sensors

CCD Sensors

By Resolution

Standard Definition (SD) Cameras

High-definition (HD) Cameras

By End-User

Hospitals & Ambulatory Surgery Centers

Specialty Clinics

11 South America Medical Cameras Market Analysis and Outlook To 2030

11.1 Introduction to South America Medical Cameras Markets in 2024

11.2 South America Medical Cameras Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Medical Cameras Market size Outlook by Segments, 2021-2030

By Type

Endoscopy Cameras

Dermatology Cameras

Ophthalmology Cameras

Dental Cameras

Surgical Microscopy Cameras

Others

By Sensor

CMOS Sensors

CCD Sensors

By Resolution

Standard Definition (SD) Cameras

High-definition (HD) Cameras

By End-User

Hospitals & Ambulatory Surgery Centers

Specialty Clinics

12 Middle East and Africa Medical Cameras Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Medical Cameras Markets in 2024

12.2 Middle East and Africa Medical Cameras Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Medical Cameras Market size Outlook by Segments, 2021-2030

By Type

Endoscopy Cameras

Dermatology Cameras

Ophthalmology Cameras

Dental Cameras

Surgical Microscopy Cameras

Others

By Sensor

CMOS Sensors

CCD Sensors

By Resolution

Standard Definition (SD) Cameras

High-definition (HD) Cameras

By End-User

Hospitals & Ambulatory Surgery Centers

Specialty Clinics

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Atmos Medizintechnik GmbH & Co. KG

Basler AG

Canon Inc

Carestream Dental LLC

Carl Zeiss AG

Cymo B.V.

Dage-MTI

Danaher

Diaspective Vision

ESC Medicams

FUDE Technology Group Ltd

Haag-Streit Group

Healthtech Engineers Private Ltd

IDS Imaging Development Systems GmbH

Imperx Inc

Medicam

Olympus Corp

Optomed Plc

Richard Wolf GmbH

Schölly Fiberoptic GmbH

Smith & Nephew

Sony Corp

Stryker Corp

Tonglu Kanger Medical Instrument Co. Ltd

Topcon Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Endoscopy Cameras

Dermatology Cameras

Ophthalmology Cameras

Dental Cameras

Surgical Microscopy Cameras

Others

By Sensor

CMOS Sensors

CCD Sensors

By Resolution

Standard Definition (SD) Cameras

High-definition (HD) Cameras

By End-User

Hospitals & Ambulatory Surgery Centers

Specialty Clinics

Countries Analyzed

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)