Market Analysis: Breakthroughs in AI and Connected Devices Transform the Sensor-Based Healthcare Market

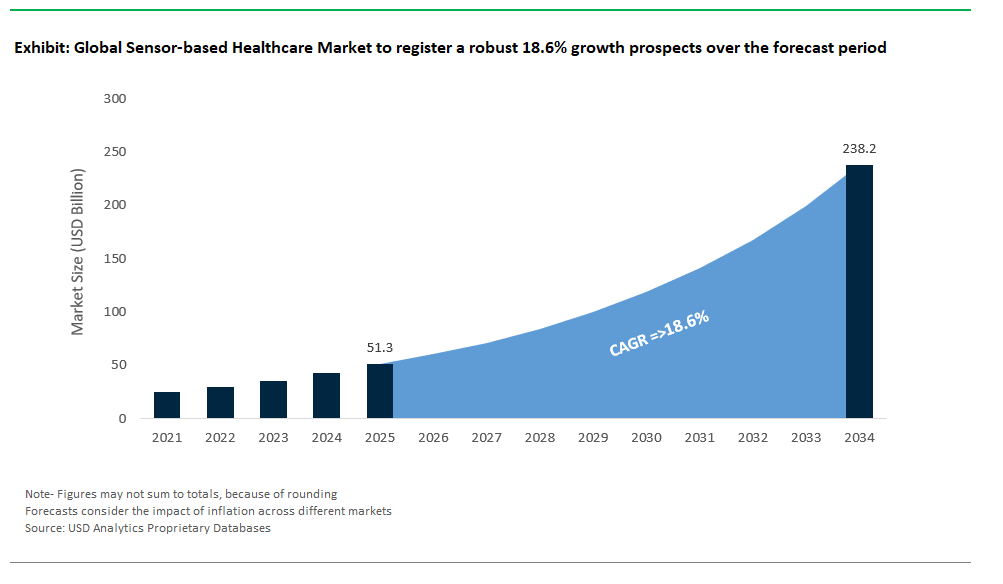

The Global Sensor-based Healthcare Market Size is estimated at $51.3 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 18.6% to reach $238.2 Billion by 2034.

The sensor-based healthcare market is advancing rapidly as global leaders and innovators introduce smarter, more connected medical solutions powered by artificial intelligence and advanced sensor technologies. In March 2025, GE HealthCare partnered with NVIDIA to revolutionize diagnostic imaging, launching autonomous X-ray and ultrasound systems that use AI and high-precision sensors to enhance accuracy and efficiency in clinical settings. Meanwhile, Roche achieved CE Mark approval for its AI-driven Accu-Chek SmartGuide continuous glucose monitoring (CGM) solution, which anticipates hypoglycemia events hours ahead highlighting the growing role of predictive analytics in diabetes management.

A trend toward holistic and interoperable health tracking is accelerating across the industry. Dexcom’s investment in Oura signals a convergence of metabolic sensing with broader wellness monitoring, as smart rings and wearable CGM sensors together provide comprehensive views of health, from glucose levels to sleep quality and physical activity. Major diabetes care players like Abbott and Medtronic are pushing the boundaries of interoperability, developing platforms that link CGM sensor data with insulin pumps to create closed-loop, automated diabetes management systems. These advances are making chronic disease care more integrated and responsive, setting new standards in personalized medicine.

Sensor innovation is also improving access, imaging, and product quality in global healthcare. India’s C3 Med-Tech secured funding in 2024 to bring AI-powered, portable eye checkup devices to underserved areas, leveraging sensors for remote diagnostics. Stryker’s expanded medical device testing lab in India supports innovation and quality for sensor-based surgical tools and implants. In medical imaging, OmniVision Technologies’ OVMed OCHTA Cable Module for single-use endoscopes enables sharper, less invasive visualization. Meanwhile, Sensirion AG joined the STMicroelectronics Partner Program, integrating state-of-the-art humidity and temperature sensors into a broader range of healthcare devices. Together, these advancements are rapidly transforming the sensor-based healthcare market, driving a future where precision, accessibility, and interoperability are at the core of patient care.

Breakthrough Innovations in the Sensor-Based Healthcare Market

Trend: Multi-Omic Wearables for Gut-Brain Axis Monitoring

The sensor-based healthcare market is entering a transformative phase with the introduction of multi-omic wearables aimed at monitoring the gut-brain axis. These cutting-edge devices continuously track biomarkers such as cortisol levels and microbiome-derived metabolites, providing early predictive insights into conditions like inflammatory bowel disease (IBD). Clinical studies indicate that these wearables can predict IBD flare-ups several days in advance, offering a critical advantage in proactive disease management and patient care optimization. This early-warning capability represents a paradigm shift in chronic disease management, reducing hospital admissions and improving quality of life for patients.

Regulatory agencies are actively fostering this innovation, granting expedited review status to multiple gut-sensing wearable solutions. These designations validate the clinical relevance of such devices as novel digital biomarkers and accelerate their time-to-market. The strong regulatory push underscores a broader industry movement toward integrating continuous patient-generated health data into clinical workflows. With the rising prevalence of gastrointestinal and autoimmune disorders, multi-omic wearables for gut-brain monitoring are poised to become an essential tool in personalized medicine, significantly driving market growth in the coming years.

Opportunity: Sepsis Prediction Sensors for Post-Op Care

A major opportunity within the sensor-based healthcare market lies in the deployment of advanced sepsis prediction sensors for post-operative care. These next-generation wearable devices, often nurse-worn or integrated into patient monitoring systems, detect early biochemical markers such as volatile organic compounds (VOCs) from surgical wounds critical indicators of infection onset. By identifying sepsis risk in its earliest stages, these sensors enable timely intervention, reducing ICU stays and significantly lowering mortality rates in high-risk patients.

This opportunity is further strengthened by evolving reimbursement frameworks. Medicare and other major healthcare payers are introducing incentive programs to encourage hospitals to adopt technology that improves recovery outcomes and reduces readmissions. These reimbursement-driven initiatives, combined with the growing emphasis on value-based care, are creating a multi-billion-dollar addressable market for sepsis monitoring solutions in surgical and critical care settings. As hospitals seek innovative methods to enhance patient safety and operational efficiency, the integration of predictive sepsis sensors represents a strategic priority with far-reaching clinical and economic benefits.

Competitive Landscape: Sensor-based Healthcare Market

Dexcom: Redefining Continuous Glucose Monitoring in the Sensor-Based Healthcare Market

Dexcom stands out as a pioneering force in the sensor-based healthcare market, continually advancing the field of continuous glucose monitoring (CGM) and empowering patients with diabetes to achieve greater control and insight. Dexcom’s latest generation, the Dexcom G7 CGM system, elevates the standard for wearable glucose monitoring with its compact, all-in-one sensor, faster 30-minute warm-up, and direct-to-smartphone connectivity enabling truly real-time, actionable glucose data without fingersticks or scanning. With the launch of the Stelo Glucose Biosensor in June 2025, Dexcom is further democratizing access by introducing an over-the-counter CGM for people not on insulin, broadening the reach of sensor-based health monitoring. The G6 Pro CGM system, designed for professional use, and the powerful Dexcom Clarity software platform together offer robust data analytics for personalized diabetes management in both home and clinical settings. Recent partnerships and expanded device integrations have solidified Dexcom’s reputation for interoperability and digital health ecosystem leadership. Their ongoing innovations, focus on patient comfort, and dedication to accuracy have not only strengthened their competitive position but have also set new industry benchmarks in sensor-driven remote patient monitoring and AI-powered disease management.

Abbott: Global Leader in Accessible and Affordable Sensor-Based Glucose Monitoring

Abbott is a global powerhouse in the sensor-based healthcare market, primarily through its FreeStyle Libre product family, which has transformed glucose monitoring for millions worldwide. The FreeStyle Libre 2 and 3 systems offer patients a discreet, easy-to-use solution for continuous glucose tracking, with the FreeStyle Libre 3 distinguished as the world’s smallest and most discreet sensor, sending real-time readings directly to smartphones. Abbott’s affordability and broad access strategy have made CGM technology attainable for a wider population, while their commitment to regulatory approvals, including recent FDA clearances and expanded pediatric indications, demonstrates their ongoing drive for inclusivity in sensor-based diabetes care. Supporting digital tools such as LibreView and MyFreeStyle App enable both patients and clinicians to interpret glucose trends, optimize therapy, and personalize treatment. Real-world evidence and global leadership confirm Abbott’s pivotal role in reducing HbA1c, improving clinical outcomes, and shaping the future of non-invasive, wearable health technology.

Medtronic: Advancing Integrated Sensor-Based Diabetes Management and AI Automation

Medtronic brings decades of expertise and continuous innovation to the sensor-based healthcare market, with a focus on fully integrated diabetes management systems. The MiniMed™ 780G system exemplifies the fusion of CGM and automated insulin delivery, powered by advanced algorithms for real-time adjustments and auto-corrections every five minutes, effectively reducing the burden on users and advancing the promise of closed-loop therapy. The recent FDA approval of the Simplera Sync™ sensor and the standalone Simplera™ CGM reflect Medtronic’s dedication to expanding sensor-based solutions for all stages of the diabetes journey. Medtronic’s strategic decision to establish MiniMed as a standalone diabetes-focused company, and its partnership with Abbott for interoperable pump/CGM integration, mark bold steps toward enhancing patient choice and driving the next era of diabetes tech interoperability. Backed by CareLink™ software and a robust pipeline of sensor innovations, Medtronic’s AI-driven approach is setting new standards in precision, safety, and remote management of chronic disease through sensor-based healthcare.

BioIntelliSense: Transforming Remote Patient Monitoring with Medical-Grade Wearable Sensors

BioIntelliSense is at the cutting edge of continuous health monitoring in the sensor-based healthcare market, delivering high-frequency, medical-grade insights across care settings. The BioButton® a discreet, FDA-cleared wearable sensor captures vital signs such as heart rate, respiratory rate, skin temperature, and activity, supporting up to 1,440 measurements daily for comprehensive remote patient monitoring (RPM). Their ecosystem, which includes the multi-patient BioButton, BioDashboard™ for clinical intelligence, and BioCloud™ data services, leverages advanced analytics and algorithmic alerts to enable early detection of patient deterioration and support timely clinical interventions. Recent FDA clearances, published research on improved clinical outcomes, and high-profile hospital partnerships underscore BioIntelliSense’s leadership in scalable, continuous patient monitoring. Strategic alliances with Medtronic and other health systems, along with the acquisition of the AlertWatch® clinical intelligence platform, position BioIntelliSense as a critical enabler of AI-powered, sensor-based healthcare delivery, transforming both inpatient and outpatient monitoring.

Propeller Health (ResMed): Digital Therapeutics and Sensor-Driven Management of Chronic Respiratory Disease

Propeller Health, a ResMed company, is revolutionizing chronic respiratory disease management with its sensor-based digital health platform, specifically tailored for asthma and COPD. By attaching small sensors to patients’ inhalers, Propeller Health automatically tracks medication usage and environmental factors, integrating this data into an intuitive smartphone app for personalized feedback and actionable insights. The platform's clinical impact is proven, with research demonstrating improvements in medication adherence, reduced rescue inhaler use, and fewer hospitalizations. As part of ResMed’s vast digital health ecosystem, Propeller leverages cloud connectivity and real-time analytics to support patients and clinicians alike. Continued innovation in sensor attachment design and digital therapeutics, combined with active participation in clinical research, keep Propeller Health at the forefront of respiratory sensor-based healthcare. Its focus on digital engagement, patient adherence, and data-driven care is transforming outcomes for patients managing chronic respiratory conditions through the power of connected sensors.

Market Share and Segmentation Insights: Sensor-based Healthcare Market

By Sensor Type: Biosensors Dominate, Optical Sensors Accelerate

The sensor-based healthcare market is spearheaded by biosensors, which hold the largest market share at 34.6% in 2025. Biosensors are at the heart of diabetes management (glucose monitors) and wearable health devices, making them foundational to both chronic disease care and real-time patient data collection. Optical sensors are the fastest-growing segment, expanding at a CAGR of 19.2%, fueled by the adoption of pulse oximeters, advanced endoscopic imaging, and non-invasive diagnostics in both hospital and home care settings. Physical sensors such as accelerometers and pressure sensors remain vital for patient monitoring applications, offering critical data for vital signs, mobility, and fall detection. Chemical sensors are also important, particularly in advanced drug delivery and metabolic analysis, though their market share remains comparatively modest.

.png)

By Application: Patient Monitoring Leads, Fitness & Wellness Surges

When analyzed by application, patient monitoring holds the top share at 38.9% in 2025, reflecting the continued focus on chronic disease management and the proliferation of ECG and SpO₂ sensors across clinical and home environments. The fitness and wellness segment is the fastest-growing, with a CAGR of 19.1%, as health-conscious consumers increasingly adopt wearables like the Apple Watch and Fitbit for daily activity tracking and wellness insights. Diagnostic imaging and in vitro diagnostics (IVD) follow closely, supported by the integration of smart sensors into medical imaging and lab diagnostics. The market also sees robust growth in therapeutic and drug delivery applications, where sensors enable precision dosing and adherence monitoring. Meanwhile, personalized medicine though still emerging shows significant momentum, leveraging AI-driven analytics from sensor data for individualized care.

United States: Surge in Remote Patient Monitoring and AI-Enabled Sensor Devices

The United States is leading global adoption of sensor-based healthcare, especially through Remote Patient Monitoring (RPM) technologies. In 2025, over 70 million Americans are expected to use RPM devices an annual growth of 16.4%. The adoption surge is powered by widespread integration of connected in-home medical devices that relay patient data directly to healthcare providers, improving chronic disease management and reducing unnecessary hospital visits. This trend is reinforced by notable device launches, such as Prevounce Health’s Pylo GL1-LTE, a cellular-connected glucose meter tailored for RPM programs, and Smart Meter’s expansion of its cellular blood pressure and glucose monitoring platform to over 350,000 patients. Strategic partnerships like Circadian Health and Tenovi integrating medication adherence with vital sign tracking demonstrate a coordinated industry effort to leverage sensor data for better patient outcomes and operational efficiencies.

AI is another engine of growth in the U.S. sensor-based healthcare market. The FDA approved 950 AI/ML-enabled medical devices as of August 2024, up from just 91 in 2022, highlighting rapid technological integration. AI is being embedded into sensor-equipped devices for enhanced diagnostics, early disease detection, and continuous monitoring. Companies are also expanding Electronic Health Record (EHR) integration, as shown by Smart Meter’s new Tampa facility and collaborations with platforms like eClinicalWorks. As the regulatory environment matures, and as digital health platforms proliferate, the U.S. market will see even greater adoption of sensor-enabled, AI-powered health management solutions setting benchmarks for both scalability and clinical impact.

Germany: National ePA Rollout and Strategic Investment in Sensor-Based Health Technologies

Germany is making substantial advances in sensor-based healthcare through a mix of digital infrastructure, startup investment, and policy. The national rollout of the Electronic Patient Record (ePA) in January 2025 ensures all insured citizens have access to digital health files, facilitating the integration and exchange of sensor-generated data across care providers. The government’s High-Tech Strategy 2025 places “Health and Care” as a priority, supporting R&D for sensor innovations that improve disease management, medication adherence, and remote diagnostics. Venture capital funding for digital health startups soared by 50% in Q3/2024, with over €2.5 billion invested and 42 healthcare startups backed, many focused on sensor-driven applications. This influx of capital supports robust product development pipelines and enhances Germany’s reputation as a medtech innovation hub.

Further strengthening the ecosystem, Germany is leveraging AI to streamline medical device approval and to enhance the performance of sensor-based technologies. Projects like “GenAI-Med” are investigating the use of generative AI in regulatory workflows, while the pharmaceutical sector’s €7 billion investment wave since late 2023 creates synergies between pharma and medtech. These investments often lead to new drug delivery and monitoring devices powered by advanced sensors. As German clinics, startups, and established companies work together to meet rising demand for data-driven care, Germany is cementing itself as a leader in safe, interoperable, and patient-centered sensor-based healthcare solutions.

India: Digital Health Scale-Up, Telemedicine, and AI-Powered Diagnostics

India’s sensor-based healthcare market is undergoing a dramatic transformation, propelled by the Ayushman Bharat Digital Mission (ABDM) and the surge in telemedicine adoption. As of January 2025, more than 730 million unique Ayushman Bharat Health Accounts (ABHA) have been issued, creating a digital backbone for storing and sharing health data including that collected by sensor-equipped devices. The e-Sanjeevani telemedicine platform, with over 371 million teleconsultations as of June 2025, is crucial for connecting rural populations to specialists and enabling real-time data transmission from remote diagnostics. The Digital Health Incentive Scheme (DHIS) further incentivizes healthcare providers to integrate sensor data into digital health records, fostering rapid expansion of connected diagnostics and continuous monitoring.

India is also seeing significant advancements through AI-powered healthcare and public-private partnerships. In 2024, the National Health Authority and IIT Kanpur initiated a federated learning platform to develop robust, benchmarked AI models for healthcare analytics, including those using sensor inputs. The private sector is equally active: Evalyn Healthcare and Renu Electronics have teamed up to develop Intel-based diagnostic devices, while Tricog and Omron aim to conduct 100 million cardiac screenings by 2030 using sensor-rich cardiac monitoring solutions. With this digital-first momentum, India is positioning itself as a high-growth, innovation-driven market for both mass and specialty sensor-based healthcare technologies.

Japan: Wearable Biosensor R&D and Leadership in Preventive Health Diagnostics

Japan stands out in the sensor-based healthcare market for its cutting-edge R&D in wearable biosensors and focus on early diagnostics. Japanese researchers are making breakthroughs in flexible graphene-based biosensors, which are ideally suited for monitoring mental health biomarkers and stress in real time. Such next-generation wearables align with Japan’s strategic focus on preventive health, enabling early detection of cancer, allergies, diabetes, and other chronic conditions. The robust R&D environment has propelled the global biosensors market where Japan is a manufacturing and research leader to a forecast CAGR of over 7% from 2023 to 2032.

Electrochemical biosensors, a segment in which Japan excels, are rapidly advancing in terms of sensitivity, selectivity, and miniaturization, allowing for highly accurate, point-of-care diagnostics. The country’s continued innovation in biochips, biosensors, and miniaturized analytical devices is enhancing the precision and speed of medical testing. These advancements support both clinical settings and consumer wellness, reflecting Japan’s commitment to integrated, technology-driven healthcare that empowers early intervention and effective disease management through real-time sensor data.

United Kingdom: Virtual Wards, 5G Rollout, and Sensor-Driven Chronic Disease Management

The United Kingdom is pioneering the use of sensor-based healthcare through initiatives such as NHS England’s Virtual Wards, designed to deliver hospital-level care at home and reduce inpatient pressure. These programs leverage a spectrum of remote patient monitoring (RPM) sensors covering vitals, medication adherence, and symptom tracking to enable clinicians to intervene proactively and personalize care plans. The nationwide rollout of 5G networks is accelerating the adoption and performance of real-time monitoring systems by ensuring seamless, low-latency data transfer between patients and providers.

The RPM market in the UK is expected to triple from $810 million in 2024 to $2.45 billion by 2035, at a robust CAGR of over 10%. Government funding for innovative health tech and a rising prevalence of chronic diseases (cancer, diabetes, cardiovascular conditions) are key drivers. The emphasis on continuous monitoring for chronic disease management is pushing healthcare providers to adopt an ecosystem of interoperable sensors enabling early intervention, improved patient outcomes, and reduced healthcare costs. This focus on digital-first, home-based care is positioning the UK as a leader in modern, sensor-enabled healthcare delivery.

Canada: Wearables Boom, Telehealth Integration, and Multi-Functional Sensor Devices

Canada is witnessing explosive growth in wearable health technology, with the market projected to surge from $4.18 billion in 2024 to $57.1 billion by 2035, reflecting a CAGR of nearly 27%. Wearable sensors are being rapidly adopted for tracking vitals, activity, sleep, and even mental health, as nearly 60% of Canadians report greater health consciousness than in prior years. The “Wristwear” segment including smartwatches and fitness trackers is a leading category, driving widespread adoption of wrist-based sensors for continuous health management and lifestyle optimization.

This growth is supported by a strong telehealth infrastructure: over 40% of Canadian healthcare providers now use wearables to facilitate remote monitoring of patient health. Consumers are demanding more multifunctional wearables such as smart textiles and advanced trackers that blend health, wellness, and fashion. The integration of wearable data with telehealth and virtual care platforms is enabling more personalized care and supporting a shift toward preventative and holistic health management. With ongoing innovation and consumer demand, Canada is poised to be at the forefront of sensor-enabled digital health.

Brazil: Accelerated CGM Market, Government Diabetes Initiatives, and Sensor Innovation

Brazil’s sensor-based healthcare market is expanding rapidly, particularly in diabetes care. The continuous glucose monitoring (CGM) market is expected to grow from $307 million in 2025 to over $573 million by 2030, driven by Brazil’s rising diabetes prevalence and a strong push toward non-invasive, real-time monitoring. Manufacturers are focusing on technological advancements to improve device accuracy, convenience, and affordability, reflecting a consumer preference for pain-free, low-maintenance health solutions.

The Brazilian government is actively promoting diabetes awareness and management, further fueling adoption of sensor-based solutions. Research and development are exploring new frontiers in non-invasive monitoring, such as optical sensors and skin patches, indicating the next wave of innovation in medical sensing. As demand for chronic disease management rises, Brazil’s market for sensor-equipped devices especially for glucose and cardiovascular monitoring will continue to expand, transforming disease management for millions and reinforcing Brazil’s role as a Latin American leader in healthcare technology.

France (EU Context): EU MDR Compliance, In-House Device Regulation, and Digital Transformation

France’s sensor-based healthcare market is being shaped by new and stringent EU medical device regulations, notably Regulation (EU) 2024/1860. From January 2025, manufacturers must comply with enhanced requirements for supply chain transparency, documentation, and quality management impacting both imported and in-house-produced sensor medical devices. French clinics and labs can now only manufacture in-house devices if no CE-certified alternative exists, prompting a shift toward certified, commercially available sensor solutions and raising the bar for device quality and safety.

This regulatory landscape dovetails with France’s broader push for digital transformation in healthcare, including major investments in digital health records and telehealth platforms. While not directly related, the rise of battery gigafactories (such as those from ACC and Stellantis) supports advanced manufacturing ecosystems that can benefit sensor production as well. The cumulative effect is a robust infrastructure for integrating sensor-based technologies, improving patient safety, and ensuring compliance with the latest European standards a crucial step for scaling innovation in the French and broader European sensor healthcare market.

Sensor-based Healthcare Market Report Scope

Sensor-based Healthcare Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$51.3 Billion

|

|

Market Size (2034)

|

$238.2 Billion

|

|

Market Growth Rate

|

18.6%

|

|

Segments

|

By Sensor Type (Physical Sensors, Biosensors, Chemical Sensors, Optical Sensors), By Device (Wearable Sensors, Implantable Sensors, Ingestible Sensors, Medical Sensor-Integrated Devices, Point-of-Care Testing (PoCT) Devices), By Application (Patient Monitoring, Diagnostic Imaging & In-vitro Diagnostics (IVD), Therapeutic & Drug Delivery, Surgical & Minimally-Invasive Procedures, Fitness & Wellness, Personalized Medicine), By End User (Hospitals & Clinics, Home Healthcare Settings, Diagnostic Centers, Ambulatory Surgical Centers, Research & Academic Institutes), By Technology (MEMS (Micro-Electro-Mechanical Systems) Technology, Nano/Graphene Sensors, Fiber Optic Sensors, IoT-enabled Sensors, AI-powered Sensors)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Medtronic plc., GE HealthCare Technologies Inc., Koninklijke Philips N.V., Abbott Laboratories, Honeywell International Inc., TE Connectivity, Analog Devices, Inc., STMicroelectronics, Texas Instruments (TI), NXP Semiconductors, OMRON Corporation, Siemens AG, Infineon Technologies AG, Sensirion AG, Apple Inc., Bosch Sensortec GmbH, Amphenol Corporation, Dexcom, Inc., Sotera Wireless, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sensor-based Healthcare Market Segmentation

By Sensor Type

- Physical Sensors

- Temperature Sensors

- Pressure Sensors

- Flow Sensors

- Force Sensors

- Motion Sensors

- Image Sensors

- Touch Sensors

- coustic Sensors

- Radiation Sensors

- Biosensors

- Glucose Biosensors

- Cardiac Biosensors

- Blood Oxygen Sensors

- Enzyme-based Biosensors

- Immunosensors

- DNA Biosensors

- Thermal Biosensors

- Piezoelectric Biosensors

- Chemical Sensors

- Optical Sensors

By Device

- Wearable Sensors

- Implantable Sensors

- Ingestible Sensors

- Medical Sensor-Integrated Devices

- Point-of-Care Testing (PoCT) Devices

By Application

- Patient Monitoring

- Diagnostic Imaging & In-vitro Diagnostics (IVD)

- Therapeutic & Drug Delivery

- Surgical & Minimally-Invasive Procedures

- Fitness & Wellness

- Personalized Medicine

By End User

- Hospitals & Clinics

- Home Healthcare Settings

- Diagnostic Centers

- Ambulatory Surgical Centers

- Research & Academic Institutes

By Technology

- MEMS (Micro-Electro-Mechanical Systems) Technology

- Nano/Graphene Sensors

- Fiber Optic Sensors

- IoT-enabled Sensors

- AI-powered Sensors

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sensor-based Healthcare Market

- Medtronic plc.

- GE HealthCare Technologies Inc.

- Koninklijke Philips N.V.

- Abbott Laboratories

- Honeywell International Inc.

- TE Connectivity

- Analog Devices, Inc.

- STMicroelectronics

- Texas Instruments (TI)

- NXP Semiconductors

- OMRON Corporation

- Siemens AG

- Infineon Technologies AG

- Sensirion AG

- Apple Inc.

- Bosch Sensortec GmbH

- Amphenol Corporation

- Dexcom, Inc.

- Sotera Wireless, Inc.

* List Not Exhaustive

Research Coverage

This USDAnalytics report provides in-depth market sizing, CAGR, and future value projections for the global sensor-based healthcare market, placing recent developments such as AI-driven diagnostics, multi-omic wearables, and digital health reimbursement initiatives at the center of analysis. The study delivers a structured review of market dynamics, innovation trends, and opportunities shaping the adoption of connected medical sensors across healthcare systems.

The report covers comprehensive segmentation by sensor type (physical, biosensors, chemical, optical), device (wearable, implantable, ingestible, PoCT devices), application (patient monitoring, diagnostics, fitness, therapy, surgery, personalized medicine), technology (MEMS, nano/graphene, IoT-enabled, AI-powered), and end-user (hospitals, home healthcare, diagnostics, ambulatory, research). It features detailed company profiles and strategies of leading players such as Medtronic, GE HealthCare, Philips, Abbott, Honeywell, Dexcom, STMicroelectronics, Texas Instruments, Siemens, and Apple.

Geographic analysis includes North America, Europe, Asia Pacific, South America, and Middle East & Africa. The report offers historic data (2021–2024) and forecast data (2025–2034), supporting industry professionals with actionable insights into regulatory trends, category growth, adoption barriers, and the evolving global sensor-based healthcare landscape.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.