Medical Protective Clothing Market Overview: Size, Growth, and Key Insights

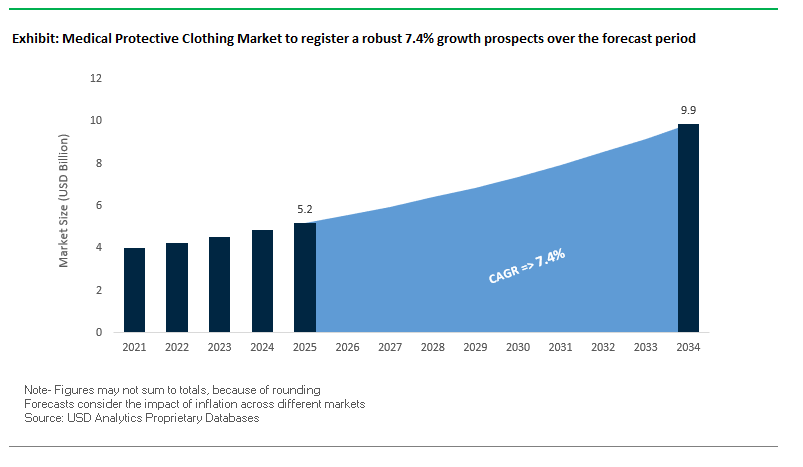

The global medical protective clothing market is forecast to reach $5.2 billion in 2025 and expand to $9.9 billion by 2034, growing at a CAGR of 7.4%. This strong growth trajectory reflects the indispensable role of protective apparel in safeguarding healthcare workers and patients, particularly in light of stringent infection control protocols and rising awareness of hospital-acquired infections (HAIs). For buyers and industry professionals, the market provides answers to key questions: How are disposable versus reusable garments influencing procurement strategies? Which advanced materials are shaping next-generation protective clothing? And how are ergonomics and sustainability influencing adoption rates among hospitals and surgical centers?

The market is being reshaped by four defining dynamics. First, infection control has become a non-negotiable priority, driving demand for sterile, single-use apparel across surgical and clinical environments. Second, the rise of disposable protective clothing is simplifying infection prevention by reducing cross-contamination risks. Third, advanced material innovations—such as microporous films and nanofibers—are enhancing barrier protection while improving comfort and breathability. Finally, manufacturers are addressing comfort and ergonomics, introducing designs with user-centric features to increase compliance among professionals who wear protective gear for long hours.

Key Insights for Industry Professionals:

- Infection control protocols are the primary demand driver for medical protective clothing.

- Single-use protective garments dominate due to their ability to eliminate cross-contamination risks.

- Advanced materials like microporous films and nanofibers offer superior barrier protection and comfort.

- Ergonomic design features are increasingly important to improve compliance among healthcare staff.

Market Analysis: Recent Developments Reshaping the Medical Protective Clothing Industry

The medical protective clothing industry is experiencing a wave of strategic investments, mergers, and innovations that are reshaping its competitive landscape. In September 2025, Roots Analysis highlighted Asia as a dominant region for medical protective clothing, driven by rapid industrialization and rising healthcare expenditure. The region’s scale of production and consumption reinforces its position as a global growth hub. In August 2025, Medline Industries enhanced its perioperative optimization program by introducing Pack 360 Analysis, a supply chain efficiency tool that optimizes usage of surgical apparel and helps hospitals reduce waste. The same month, Ansell announced a milestone in its sustainability journey by committing to net-zero greenhouse gas emissions across its value chain by 2045, underscoring how ESG initiatives are becoming integral to strategic roadmaps.

Earlier in July 2025, Ansell expanded its presence in Asia-Pacific by launching its KIMTECH™ product line in Japan and other regional markets, a move aimed at strengthening its position in one of the fastest-growing demand centers for protective clothing. On the innovation side, Dymax introduced a hybrid light-curable adhesive platform in June 2025, which, while not a clothing product itself, impacts production processes in device assembly that necessitate specialized protective gear. Meanwhile, corporate restructuring and portfolio optimization remain ongoing: in May 2025, Honeywell divested its PPE business to Protective Industrial Products (PIP) for $1.325 billion, signaling a strategic pivot to core operations while positioning PIP as a larger global PPE player.

The market is also seeing moves that indirectly support protective clothing demand. In April 2025, Integer Holdings acquired Precision Coating, strengthening capabilities in advanced coatings that require protective apparel in manufacturing settings. In March 2025, the merger between DS Smith and Mondi Group gained approval, creating a packaging powerhouse with downstream implications for medical clothing packaging and logistics. Further back, in January 2025, H.B. Fuller reinforced its focus on the healthcare market with high-performance adhesives and skin solutions—product categories that intersect with protective apparel usage.

Key Trends and Opportunities Transforming the Medical Protective Clothing Market

Strategic Reshoring and Capacity Expansion for Supply Chain Resilience

The COVID-19 pandemic exposed major vulnerabilities in global PPE supply chains, forcing governments and companies to prioritize reshoring and nearshoring strategies. In the United States, the “Make PPE in America Act” is being advanced by the American Medical Manufacturers Association (AMMA) to ensure hospitals procure domestically produced protective clothing. Federal incentives under CMS and large-scale HHS investments—such as the $250 million funding to reduce dependency on imported raw materials like nitrile and synthetic fibers— are bolstering local production capacity.

Private companies are responding with significant capital projects, including new medical gown manufacturing facilities across the U.S. South to secure faster distribution channels and mitigate international shipping delays. Globally, India’s Production Linked Incentive (PLI) scheme under the “Make in India” initiative is encouraging domestic expansion, enabling the country to emerge as a strategic supplier of medical textiles. This reshoring trend not only reduces geopolitical risks but also ensures resilient supply continuity for critical protective equipment.

Transition from Disposable to Reusable and Sustainable Fabrics

Healthcare systems are rapidly shifting from single-use disposables to durable, eco-friendly reusable gowns and drapes that can withstand sterilization cycles. Sustainability benefits are profound—Australia’s Peter MacCallum Cancer Centre pilot in 2025 reduced hospital solid waste by 9.2 tonnes annually, while studies confirm reusable medical textiles can cut greenhouse gas emissions by 66% and waste generation by 84% compared to disposable alternatives.

The economic case is equally compelling. A 30-hospital network saved $1.4 million annually by switching to reusable gowns, highlighting cost-efficiency at scale. Additionally, research from the National Center for Biotechnology Information underscores superior durability and barrier performance of reusable garments, ensuring safety and reliability for clinicians. With rising sustainability mandates and hospital cost-optimization strategies, this transition is set to accelerate, creating strong demand for next-generation reusable medical clothing.

Integration of Smart Textiles and Sensor Technology

The fusion of digital health and medical textiles is creating a transformative opportunity for smart protective clothing. Innovations include garments with embedded sensors to track clinician vital signs—heart rate, respiration, and temperature—in real time, helping hospitals mitigate risks of fatigue and occupational illness. Emerging research also demonstrates contamination detection fabrics that send immediate alerts when a gown is punctured or compromised, offering an additional safety layer in high-risk surgical or infectious environments.

IoT-enabled PPE further allows remote monitoring and analytics of clinician workflow and hospital safety patterns. Hospitals can use this data to optimize layouts, minimize exposure hotspots, and improve emergency response. As wearable technology adoption grows in healthcare, smart gowns and scrubs present a lucrative frontier for both textile innovators and medtech firms.

Standardization and Modernization of Protection Level Testing Protocols

A second opportunity lies in upgrading PPE testing standards to meet new realities of infectious disease outbreaks. The 2023 revision of AAMI PB70 introduced extended coverage categories like “Surgical Gown-E,” reflecting evolving hospital safety needs. More rigorous requirements now mandate that staff in decontamination and sterile processing units use minimum Level 3 gowns, pushing manufacturers to innovate materials that perform in high-risk zones.

The move from synthetic blood testing (ASTM F1670) to more stringent viral penetration testing (ASTM F1671) represents another major shift. By adopting bacteriophage-based evaluations, manufacturers can prove their garments’ superior barrier properties against bloodborne pathogens. Companies investing early in meeting these advanced testing protocols will gain first-mover advantage, building trust among hospitals and regulators while setting new industry benchmarks for protective performance.

Competitive Landscape: Leading Companies in the Global Medical Protective Clothing Market

The global medical protective clothing market is highly competitive, with leadership concentrated among multinational corporations that combine advanced R&D, sustainable innovation, and extensive distribution networks. Companies are differentiating themselves through material science expertise, ergonomic designs, and strategies to meet the dual imperatives of infection control and environmental responsibility.

3M Company: Leveraging Science for Infection Control Leadership

3M is a recognized leader in healthcare PPE, offering products such as surgical gowns, drapes, and N95 respirators. The company consistently invests in R&D to improve fluid resistance, particle filtration, and wearer comfort. It is also known for publishing scientific data validating product efficacy against airborne pathogens and fluids. By focusing on innovation and healthcare collaboration, 3M maintains a competitive advantage with globally trusted protective apparel solutions.

DuPont de Nemours, Inc.: Tyvek and Tychem Products Driving Safety Innovation

DuPont is globally renowned for its Tyvek® and Tychem® protective apparel lines, widely used in medical and cleanroom environments. Its Tyvek IsoClean® products are particularly valued in controlled medical settings. DuPont emphasizes sustainability and durability, while leveraging its proprietary Thermo-Man® testing system to validate performance under extreme conditions. With its brand strength and material science leadership, DuPont remains a trusted supplier of high-performance medical protective clothing.

Ansell Limited: Expanding in Asia-Pacific with Sustainability Commitments

Ansell is a global leader in hand and body protection, with a strong portfolio of surgical and examination gloves and protective garments. In July 2025, the company expanded its KIMTECH™ product line into Japan and Asia-Pacific markets. Its long-term sustainability goal—net-zero emissions by 2045—positions Ansell as a forward-looking brand. Ongoing manufacturing expansions in Malaysia and India highlight its strategy to balance regional growth with sustainability-driven innovation.

Cardinal Health: Comprehensive Distribution with Protective Apparel Strength

Cardinal Health distributes a broad portfolio of surgical gowns, drapes, and protective clothing to hospitals worldwide. Through its extensive distribution network, it simplifies procurement and strengthens supply chain resilience for healthcare providers. Recent acquisitions in late 2024, such as GI Alliance and Advanced Diabetes Supply Group, enhance Cardinal Health’s healthcare ecosystem positioning. Its focus on trusted partnerships, product availability, and distribution scale make it a key player in medical protective clothing.

Medline Industries, LP: Driving Efficiency Through Integrated Supply Solutions

Medline Industries combines manufacturing and distribution, offering a wide range of protective apparel, gowns, and coveralls. In August 2025, it launched Pack 360 Analysis as part of its perioperative optimization program, reflecting its focus on reducing surgical waste and boosting efficiency. With over 335,000 products in its portfolio and a strong U.S. distribution presence, Medline excels at next-day delivery capabilities. Its strength lies in providing end-to-end supply chain solutions alongside protective clothing products.

Medical Protective Clothing Market Share Insights

Hand Protection Dominates Market Share by Product Type in the Medical Protective Clothing Industry

Hand protection accounts for the largest share of the medical protective clothing market, holding nearly 35% of global demand, reflecting its position as the most essential barrier in healthcare environments. Gloves are a non-negotiable component of infection control protocols, used in virtually every patient interaction, surgical procedure, and diagnostic test. The market is sustained by extremely high usage volumes, with disposable nitrile, latex, and vinyl gloves being consumed daily in hospitals, clinics, laboratories, and outpatient care facilities. Growth is further reinforced by regulatory mandates such as FDA 21 CFR Part 820 and EN 455 standards, which dictate glove performance in medical environments. The shift toward nitrile gloves due to latex allergy concerns, coupled with the increasing adoption of powder-free, accelerator-free formulations, highlights ongoing product innovation. Rising global healthcare access, higher surgical volumes, and permanently elevated post-pandemic hygiene protocols ensure hand protection maintains its leading market share.

Hospitals and Clinics Drive Market Share by End-User in the Medical Protective Clothing Industry

Hospitals and clinics dominate the end-user market share for medical protective clothing, contributing around 65% of demand, primarily due to their scale, continuous operations, and high diversity of procedures. As the frontline of healthcare delivery, hospitals dictate protective apparel specifications and consumption patterns across the ecosystem, setting standards for gloves, gowns, respirators, and face shields. Bulk procurement by integrated health systems and government-led central purchasing amplify this segment’s influence, as large-scale buyers negotiate supply chain contracts that ripple through the industry. Hospitals are also major drivers of innovation adoption, demanding AAMI Level 3 & 4 gowns for high-fluid procedures, N95 respirators for aerosol protection, and environmentally sustainable products aligned with institutional ESG targets. With rising global surgery volumes, expansion of intensive care units, and stricter infection prevention policies, hospitals and clinics will remain the anchor customer group shaping product development and supplier strategies in medical protective clothing.

United States Medical Protective Clothing Market Strengthened by Regulatory Oversight and Smart Textile Innovations

The U.S. medical protective clothing market is heavily shaped by stringent regulations from OSHA and the CDC, which drive the demand for high-performance, certified protective apparel in hospitals and clinics. Technological advancements are a key focus, with manufacturers developing lightweight, breathable fabrics, antimicrobial coatings, and wearable sensors that monitor vital signs and pathogen exposure. In May 2024, Honeywell International Inc. introduced two N95 respirators designed for healthcare professionals, emphasizing product diversification and specialization.

The market’s primary applications remain in hospitals, clinics, and surgical settings, where infection control and rising surgical procedures increase the need for gowns, coveralls, and other protective clothing. Sustainability is becoming integral, with companies adopting eco-friendly materials and manufacturing methods that reduce waste while maintaining necessary protective performance. These initiatives position the U.S. market as a leader in innovation, safety compliance, and sustainable protective clothing solutions.

Germany Medical Protective Clothing Market Driven by MDR Compliance and Advanced Textile Innovations

Germany’s medical protective clothing market operates under strict national and EU regulations, including EU 2016/425 PPE standards, mandating rigorous performance and safety testing. German manufacturers are at the forefront of high-performance textile innovation, creating materials that offer superior protection against chemicals and pathogens while enhancing comfort. In January 2025, DuPont launched Tychem 6000 SFR, a lightweight hooded garment for chemical and flash-fire protection, exemplifying Germany’s leadership in R&D-driven protective clothing.

Key applications include the healthcare, pharmaceutical, and cleanroom sectors, where hospital-acquired infection prevention and complex manufacturing processes demand advanced protective garments. The country’s robust healthcare infrastructure and MedTech ecosystem continue to fuel demand for specialized, durable, and breathable protective clothing, aligning with both regulatory compliance and technological innovation.

China Medical Protective Clothing Market Expands Through Government Initiatives and Domestic Manufacturing

China’s medical protective clothing market benefits from active government support promoting high-end domestic manufacturing. Regulatory reforms by the NMPA streamline approval processes for innovative protective equipment, and the government’s dual-carbon targets encourage sustainable, low-VOC production. Chinese manufacturers are leveraging automation and AI technologies to boost efficiency and quality, ensuring international-standard protective clothing is produced domestically.

The push for domestic substitution of imported technology is driving local companies to expand capacity and meet growing healthcare demand. This trend supports applications across hospitals, emergency services, and medical device sectors, highlighting China’s focus on high-quality, technologically advanced, and sustainable protective clothing solutions.

India Medical Protective Clothing Market Strengthened by Make in India and Advanced PPE Adoption

India’s medical protective clothing market is expanding under the Make in India initiative and the National Medical Devices Policy 2023, promoting domestic production and reducing reliance on imports. Regulatory oversight by ICMR and CDSCO ensures safety and compliance, with recent licensing of cutting-edge health technologies supporting local innovation.

The market is seeing increasing adoption of advanced protective clothing, particularly for surgical and emergency applications, driven by growing healthcare infrastructure and rising medical device usage. Corporate investments in new production facilities and R&D, supported by medical device parks, provide a favorable environment for growth. These factors collectively enhance India’s capacity to produce high-quality, compliant, and technologically advanced protective clothing.

Japan Medical Protective Clothing Market Leads with Precision Engineering and Sustainable Apparel Technologies

Japan’s medical protective clothing market leverages the country’s expertise in precision manufacturing and advanced materials. Manufacturers develop antimicrobial, highly breathable fabrics to meet rigorous quality standards. The PMDA’s May 2025 amendment to the Pharmaceuticals and Medical Devices Act strengthens supply stability, influencing production and logistics.

The market emphasizes specialty and value-added products for surgical and dental applications, where high-volume, automated manufacturing demands fast, reliable solutions. Innovations in functionality and sustainability are exemplified by the Digital Product Passport (DPP) system launched in July 2025 for the “sukui” brand, which uses blockchain to visualize CO₂ emissions and supply chain data, setting new benchmarks for transparency in protective apparel.

Brazil Medical Protective Clothing Market Advances with UDI Compliance and Sustainable Manufacturing

Brazil’s medical protective clothing market is strengthened by Anvisa’s national UDI system (Siud), implemented in July 2025, enhancing traceability and certification standards. Technological advancements focus on protective gear that is effective, comfortable, and suitable for high-temperature environments, addressing the practical needs of healthcare professionals.

Corporate investments are enhancing domestic production and reducing import dependence. For instance, Sonoco’s April 2022 acquisition of its Brazilian flexible packaging joint venture highlights strategic expansion. The market is particularly robust in pharmaceutical, healthcare, and medical device sectors, with the growth of online retail further fueling demand for high-quality, compliant, and sustainable protective clothing solutions.

Medical Protective Clothing Market Report Scope

Medical Protective Clothing Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.2 Billion

|

|

Market Size (2034)

|

$9.9 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Product Type (Protective Clothing, Head Protection, Respiratory Protection, Hand Protection, Footwear, Eye Protection), By Material (Non-woven Materials, Polyethylene, Polypropylene, Polyester, Cotton, Others), By Usage (Disposable, Reusable), By End-User (Hospitals & Clinics, Ambulatory Surgical Centers, Research & Diagnostic Laboratories, Pharmaceutical & Biotechnology Companies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, DuPont de Nemours, Inc., Ansell Limited, Kimberly-Clark Corporation, Cardinal Health, Inc., Honeywell International Inc., Medline Industries, LP, Lakeland Industries, Inc., Alpha ProTech, Inc., Molnlycke Health Care AB, Halyard Health (Owens & Minor, Inc.), Medtronic plc, Sara Healthcare Pvt. Ltd., SteriPack Group, Paul Hartmann AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Protective Clothing Market Segmentation

By Product Type

- Protective Clothing

- Head Protection

- Respiratory Protection

- Hand Protection

- Footwear

- Eye Protection

By Material

- Non-woven Materials

- Polyethylene

- Polypropylene

- Polyester

- Cotton

- Others

By Usage

By End-User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Research & Diagnostic Laboratories

- Pharmaceutical & Biotechnology Companies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Medical Protective Clothing Market

- 3M Company

- DuPont de Nemours, Inc.

- Ansell Limited

- Kimberly-Clark Corporation

- Cardinal Health, Inc.

- Honeywell International Inc.

- Medline Industries, LP

- Lakeland Industries, Inc.

- Alpha ProTech, Inc.

- Molnlycke Health Care AB

- Halyard Health (Owens & Minor, Inc.)

- Medtronic plc

- Sara Healthcare Pvt. Ltd.

- SteriPack Group

- Paul Hartmann AG

* List Not Exhaustive

Methodology

The methodology employed to analyze the global Medical Protective Clothing market integrates comprehensive primary research, secondary data analysis, and advanced market modeling to deliver actionable insights for industry professionals. Primary research involved interviews with healthcare providers, hospital procurement managers, PPE manufacturers, textile innovators, and regulatory authorities to evaluate trends in disposable versus reusable garments, advanced material adoption, ergonomic design, and sustainability initiatives. Secondary research encompassed regulatory reports from OSHA, CDC, PMDA, Anvisa, EU PPE directives, and industry publications to validate material innovations, testing protocols, and market developments. Market sizing, segmentation by product type, material, usage, and end-user, along with forecasting to 2034, was conducted using top-down and bottom-up approaches, factoring in drivers such as infection control priorities, smart textiles, reshoring of PPE production, and sustainability mandates. Competitive landscape analysis incorporated corporate filings, M&A activity, and strategic expansions by leading players to understand regional dominance and innovation pipelines. This approach ensures that USDAnalytics delivers precise, data-driven intelligence on growth dynamics, technological advancements, and emerging opportunities in the medical protective clothing market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.