Middle East & Africa (MEA) Water Treatment Chemicals Market: Growth Outlook, Analysis, and Forecast to 2034

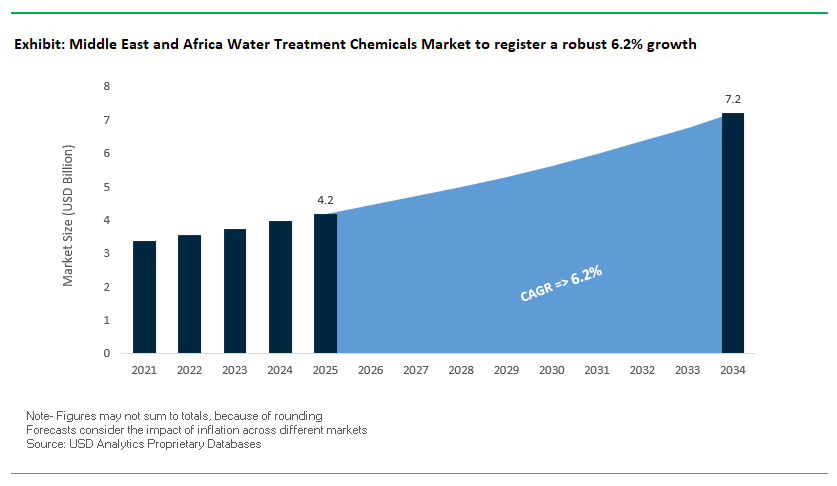

Middle East and Africa Water Treatment Chemicals Market Size is estimated at $4.2 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 6.2% to reach $7.2 Billion by 2034.

The Middle East & Africa (MEA) water treatment chemicals market is uniquely shaped by the region’s acute water scarcity, high-salinity feedwaters, and a growing emphasis on desalination, industrial water reuse, and zero liquid discharge (ZLD) strategies. Seawater reverse osmosis (SWRO) continues to dominate municipal and industrial freshwater generation, necessitating advanced chemical protocols to address scaling and membrane fouling risks. Antiscalants based on phosphonate-polyacrylate blends dosed at 3–8 ppm are routinely used to suppress calcium sulfate saturation and manage silica concentrations, conforming to GCC Standardization Organization (GSO) 149/2014 requirements. Boron removal, a critical challenge in SWRO permeate, is addressed through double-pass RO with sodium hydroxide (NaOH) pH adjustment (>10.5), achieving permeate boron levels below 0.5 ppm in line with WHO drinking water guidelines.

In Gulf countries, thermal desalination technologies such as multi-stage flash (MSF) and multi-effect distillation (MED) still retain significant capacity. These systems rely on carbohydrazide as an oxygen scavenger and silicone-polyether antifoams to manage corrosion and prevent carryover under elevated temperatures, consistent with ASTM D4519 standards. High-total dissolved solids (TDS) groundwater (>5,000 ppm) across parts of Saudi Arabia, Egypt, and Libya has driven the adoption of nanofiltration (NF) pretreatment with acid dosing to reduce hardness and mitigate membrane scaling. Industrial cooling systems in MEA face elevated silica loads often exceeding 350 ppm necessitating the use of silica dispersants and stabilizers validated under ASTM D511 protocols adopted by national authorities like SASO and ESMA.

Environmental conditions, including frequent dust storms and high ambient temperatures, heighten microbial risks. This has increased the use of chlorine dioxide for routine microbial control, along with monthly dosing of tetrakis(hydroxymethyl)phosphonium sulfate (THPS) to prevent biofilm formation in distributed systems. Sustainability initiatives are also taking root: solar-powered ZLD systems piloted by Saudi Aramco incorporate electrodialysis reversal (EDR) as a brine minimization step. Furthermore, research by KAUST into brine mining has demonstrated cost-offset models for recovering magnesium hydroxide from SWRO reject streams, used in struvite-based fertilizer production achieving over 60% chemical recovery and reducing brine disposal costs.

As regional governments accelerate climate adaptation strategies and aim for freshwater independence, the MEA water treatment chemicals market is undergoing a fundamental shift. New chemical regimes are increasingly designed to support circular water use, tolerate extreme salinity conditions, and align with broader energy-efficiency and environmental goals across the desalination, industrial, and municipal segments.

Market Trend: Decarbonized Desalination and Industrial Reuse Redefine Chemical Strategies Across MEA

The MEA water treatment chemicals market is transitioning from compliance-oriented practices to a performance- and sustainability-driven model, anchored in decarbonized desalination and industrial water reuse. With more than 83% of the region experiencing extreme water stress (World Bank, 2024), large-scale initiatives like Saudi Arabia’s NEOM and Oman’s Hydrogen Valley are embracing next-generation water treatment strategies. This includes a move away from legacy chlorine- and phosphate-based chemistries toward greener, non-toxic alternatives. At NEOM Oxagon, Veolia’s deployment of phosphonate-free antiscalants has achieved 98% water recovery and reduced brine discharge by 40%. Meanwhile, AI-optimized dosing systems at the Taweelah IWP in the UAE operated by ACWA Power have trimmed chemical consumption by up to 30%, marking a broader shift toward digitally enabled, precision dosing strategies.

Industrial users are also adopting sustainable solutions. South African mining operations and Nigeria’s oil & gas producers are replacing traditional metal salts with chitosan-based coagulants and integrating advanced oxidation processes (AOPs) to manage persistent organics and reduce sludge volumes. Regulatory reforms, such as South Africa’s 2024 update to the National Water Act (NWA), are further incentivizing adoption of low-impact, closed-loop chemical systems. The region is fast evolving into a testbed for green chemistry, driven by ESG-aligned megaprojects and cross-sectoral efforts to decouple water treatment performance from carbon and waste intensity.

Market Opportunity: Hydrogen, Battery Recycling & Data Center Cooling Create $1B+ Specialty Chemical Demand

MEA’s accelerating investment in clean energy, resource recovery, and digital infrastructure is unlocking a new class of specialty water treatment chemical opportunities exceeding $1 billion in value. The region’s hydrogen megaprojects including Oman’s 25 GW Hydrom initiative and Saudi Arabia’s electrolyzer clusters within NEOM require ultrapure water (UPW) systems capable of achieving <0.1 µS/cm conductivity. This is driving strong demand for PFAS-free antiscalants, high-capacity ion exchange resins, and low-silica formulations tailored to protect sensitive membranes and electrodes. In tandem, battery recycling hubs in Morocco and Zimbabwe are expanding, necessitating selective chelating agents and pH-conditioned flocculants to extract cobalt, lithium, and manganese from acidic process streams with minimal reagent waste.

The rise of hyperscale data centers across the UAE, Egypt, and Saudi Arabia is also catalyzing demand for precision biocides and silica control agents in closed-loop cooling systems. Facilities such as KAUST’s solar-powered data center now require biocidal programs aligned with both Legionella prevention and NEOM’s net-zero targets. These applications prioritize non-oxidizing, biodegradable agents that maintain microbial control without generating toxic residuals. In parallel, sovereign funds like Saudi Arabia’s PIF are deploying over $1.1 billion through dedicated water innovation funds, offering scale-up capital for ESG-compliant suppliers and favoring chemical technologies compatible with ZLD and carbon credit frameworks.

As MEA countries embed water sustainability within their national climate and industrial strategies, early-stage suppliers of niche chemistries particularly those aligned with regional compliance, ESG scoring, and digital dosing platforms are poised to gain lasting competitive advantages in one of the world’s fastest-evolving water treatment markets.

Middle East and Africa Water Treatment Chemicals Market Competitive Analysis

The competitive landscape of the Middle East and Africa (MEA) water treatment chemicals market shows a varied distribution influenced by regional differences, resource availability, and government-supported infrastructure projects. At the top, Tier 1 multinational companies, such as Ecolab (Nalco), Solenis, BASF, and Veolia, hold a large share of the GCC market. They achieve this through partnerships with government projects, long-term operations and maintenance contracts, and technology innovations. Ecolab leads due to its strong presence in industrial areas like NEOM and TAQA, where its IoT-based brine management solutions tackle high-salinity wastewater issues. Solenis and BASF are making progress with zero-discharge and solar-integrated dosing systems, respectively, which are important for utility projects in the UAE and Qatar. Veolia, known for its complete EPC services, is the preferred vendor for fully integrated projects, such as those with ACWA Power. This reflects the GCC’s preference for bundled engineering, procurement, and operation service models.

In contrast, Tier 2 regional players dominate Africa's fragmented markets with price-sensitive and locally focused operations. Guardian Chemicals in Southern Africa offers cost-effective mining solutions tailored for the SADC region. BEWAC in Nigeria secures a strong position in municipal contracts as Africa’s largest coagulant producer. Elixir in Egypt benefits from its location near the Nile Basin to create agriculture-specific treatment solutions. Tatweer in the UAE has established a regulatory niche in ballast water treatment, supported by global certifications. These regional champions succeed by utilizing local raw materials, development bank funding, and culturally rooted distribution networks, including tribal partnerships and local cooperatives.

Emerging disruptors, such as Israel’s Desalitech, Oman’s Majis, and Kenya’s WaterKiosk, are introducing innovative delivery models. They focus on closed-loop reverse osmosis systems, sulfate-selective treatments, and mobile or pay-as-you-go units, targeting underserved or remote areas. Their growth indicates a shift toward modular and decentralized systems, especially in areas with weak grid infrastructure or funding challenges.

The competitive landscape splits geographically and by sector. In the GCC, urban mega-projects like Qiddiya, the Dubai 2040 Plan, and Lusail City create significant demand for high-quality, sustainable solutions. Companies with local credentials, like Ecolab’s Marafiq joint venture and suppliers in line with Saudi Arabia’s IKTVA program, are well-positioned to win public-sector contracts. In Africa, water-heavy sectors such as mining (Anglo American), energy (Eskom), and agriculture (NOOR solar complex irrigation) show increasing demand. The preference in these sectors leans toward mobile units, barter procurement, and cost-efficient dosing systems, suggesting that affordability and operational flexibility are more important than technological complexity.

Looking ahead, GCC markets will focus more on integration with energy desalination facilities, especially SWCC plants, and financing that aligns with environmental, social, and governance (ESG) standards. This shift will favor global players with strong compliance records. In Africa, competition will focus on cost efficiency, local manufacturing, and flexibility for off-grid conditions. Chinese companies, while not yet leaders, may create pricing challenges with state-supported entry strategies, pushing existing firms to innovate or consolidate.

Middle East & Africa (MEA) Water Treatment Chemicals Market– Segmentation Insights (2025–2034)

By Type of Chemical: Corrosion Inhibitors Lead, Membrane Cleaners Accelerate

In the MEA water treatment chemicals market, corrosion and scale inhibitors are projected to hold the largest market share of 29.7% in 2025, driven by their indispensable role in high-salinity environments such as desalination plants and oilfield water systems. These chemicals are critical for protecting infrastructure from damage caused by scale buildup and corrosion in boilers, pipelines, and cooling towers. Countries like Saudi Arabia, the UAE, and Nigeria are among the largest consumers due to expansive oil and gas operations and widespread brine-intensive desalination activities.

On the growth front, membrane cleaning chemicals are set to record the highest CAGR of 7.8% through 2034, fueled by the rapid rollout of reverse osmosis (RO) desalination and water reuse projects across the Gulf and Sub-Saharan Africa. These agents are crucial for maintaining the operational efficiency of RO and nanofiltration systems, which are increasingly deployed to tackle chronic freshwater scarcity in arid regions. With mega-projects like NEOM and Jubail in Saudi Arabia, alongside South Africa's industrial wastewater reuse mandates, membrane cleaner adoption is expected to surge significantly across both municipal and industrial water management.

By End-User Industry: Oil & Gas Sector Dominates, Mining Emerges as Fastest-Growing

In terms of end-use, the oil and gas sector leads the MEA market with a projected 2025 share of 34.1%, anchored by massive upstream and midstream infrastructure in the GCC, Nigeria, and Algeria. Water treatment chemicals such as biocides, scale inhibitors, and hydrogen sulfide (H₂S) scavengers are essential for managing produced water, corrosion control, microbial contamination, and water injection systems in sour gas fields. The sector’s stringent operational requirements, coupled with regulatory compliance, sustain strong chemical demand across exploration, production, and refining activities.

Meanwhile, the mining and metallurgy industry is forecast to grow at the fastest CAGR of 8.2% between 2025 and 2034, driven by mineral-rich regions in Sub-Saharan Africa especially the Democratic Republic of Congo, Zambia, and South Africa. These countries are scaling up water treatment in copper, gold, and platinum tailings management, requiring large volumes of coagulants, flocculants, and specialty reagents. Additionally, increased interest in sustainable mining practices and water reuse technologies is accelerating the adoption of advanced treatment chemicals. The growth potential in mining is reinforced by global demand for battery and energy transition minerals, positioning it as a key growth driver in the MEA chemical treatment landscape.

Water Treatment Chemicals Market By End-User Industry (2025).png)

Middle East and Africa Water Treatment Chemicals Market Report Scope

Middle East and Africa Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.2 Billion

|

|

Market Size (2034)

|

$7.2 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Softeners, Oxygen Scavengers, Defoamers and Antifoaming Agents, Membrane Cleaning Chemicals, H2S Scavengers, Other Specialty Chemicals), By Application (Municipal Water Treatment, Industrial Water Treatment, Commercial Water Treatment), By End-User Industry (Oil and Gas, Power Generation, Municipal, Mining and Metallurgy, Chemical and Petrochemical, Food and Beverage, Manufacturing, Other Industrial Sectors), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Floerger (France), BASF SE (Germany), Kurita Water Industries Ltd. (Japan), Veolia Water Technologies (France), SUEZ S.A. (France), The Dow Chemical Company (U.S.), Nouryon (The Netherlands), Buckman (U.S.), REDA Chemicals (UAE), Metito (Overseas) Limited (UAE), WETICO (Saudi Arabia), Al Jazira Water Treatment Chemicals (UAE),

|

|

Countries

|

Saudi Arabia, UAE, Qatar, Oman, Kuwait, Iran, Egypt, Africa, South Africa, Algeria, Morocco, Nigeria, Kenya

|

Middle East and Africa Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Corrosion and Scale Inhibitors

- Biocides and Disinfectants

- pH Adjusters and Softeners

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- Membrane Cleaning Chemicals

- H2S Scavengers

- Other Specialty Chemicals

By Application

- Municipal Water Treatment

- Drinking Water Treatment

- Municipal Wastewater Treatment

- Industrial Water Treatment

- Cooling Water Treatment

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Water Reuse and Recycling

- Industrial Desalination

- Sludge Treatment

- Commercial Water Treatment

By End-User Industry

- Oil and Gas

- Power Generation

- Municipal

- Mining and Metallurgy

- Chemical and Petrochemical

- Food and Beverage

- Manufacturing

- Other Industrial Sectors

By Form of Chemical

By Country/Sub-Region

- Middle East

- Saudi Arabia

- UAE

- Qatar

- Oman

- Kuwait

- Iran

- Egypt

- Africa

- South Africa

- Algeria

- Morocco

- Nigeria

- Kenya

- Rest of Africa

Top Companies in Middle East and Africa Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Floerger (France)

- BASF SE (Germany)

- Kurita Water Industries Ltd. (Japan)

- Veolia Water Technologies (France)

- SUEZ S.A. (France)

- The Dow Chemical Company (U.S.)

- Nouryon (The Netherlands)

- Buckman (U.S.)

- REDA Chemicals (UAE)

- Metit(Overseas) Limited (UAE)

- WETIC(Saudi Arabia)

- Al Jazira Water Treatment Chemicals (UAE)

* List Not Exhaustive

Research Coverage

This report investigates the Middle East and Africa (MEA) Water Treatment Chemicals Market, offering detailed analysis reviews on key chemical segments, including corrosion and scale inhibitors, coagulants, biocides, and membrane cleaning agents, alongside emerging solutions for PFAS-free formulations and sustainable desalination. It highlights breakthroughs in AI-based dosing, ZLD adoption, and green chemistry initiatives, providing critical insights for stakeholders navigating compliance, ESG priorities, and industrial water reuse strategies. This report is an essential resource for utilities, industrial operators, and investors seeking a comprehensive understanding of the MEA region’s unique water challenges and market opportunities. Developed by USDAnalytics, this report delivers strategic intelligence to support decision-making across desalination, industrial reuse, and municipal water projects.

Key Research Details:

- Segmentation:

- By Type of Chemical: Coagulants & Flocculants, Corrosion & Scale Inhibitors, Biocides & Disinfectants, pH Adjusters, Oxygen Scavengers, Membrane Cleaning Chemicals, H₂S Scavengers, Other Specialty Chemicals.

- By Application: Municipal Water Treatment (Drinking Water, Wastewater), Industrial Water Treatment (Cooling, Boiler, Process Water, Reuse, Desalination, Sludge), Commercial Water Treatment.

- By End-User: Oil & Gas, Power Generation, Municipal, Mining, Chemical & Petrochemical, Food & Beverage, Manufacturing, Other Sectors.

- By Form: Liquid, Powder/Solid.

- Geographic Scope: Middle East (Saudi Arabia, UAE, Qatar, Oman, Kuwait, Iran, Egypt), Africa (South Africa, Algeria, Morocco, Nigeria, Kenya, Rest of Africa).

- Study Period: Historic data from 2021–2024 and forecast data from 2025–2034.

- Top Companies: Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Floerger (France), BASF SE (Germany), Kurita (Japan), Veolia (France), SUEZ S.A. (France), Dow Chemical (U.S.), Nouryon (Netherlands), Buckman (U.S.), REDA Chemicals (UAE), Metit Overseas (UAE), WETIC (Saudi Arabia), Al Jazira Water Treatment Chemicals (UAE).

Methodology

USDAnalytics applies a rigorous research methodology, blending primary interviews with regional utility operators, EPC contractors, and chemical suppliers, alongside secondary research sourced from governmental frameworks, industry databases, and technical standards (ASTM, GSO, WHO). Market sizing adopts a bottom-up approach based on chemical dosage norms, project pipelines, and plant-level procurement data for municipal and industrial facilities. Forecasting leverages econometric modeling that factors in desalination capacity expansions, sustainability mandates, and infrastructure funding flows from initiatives such as NEOM and Africa Water Vision 2030. Data validation through triangulation ensures accuracy, enabling actionable insights for stakeholders focused on compliance, circular economy practices, and low-carbon water treatment solutions.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements