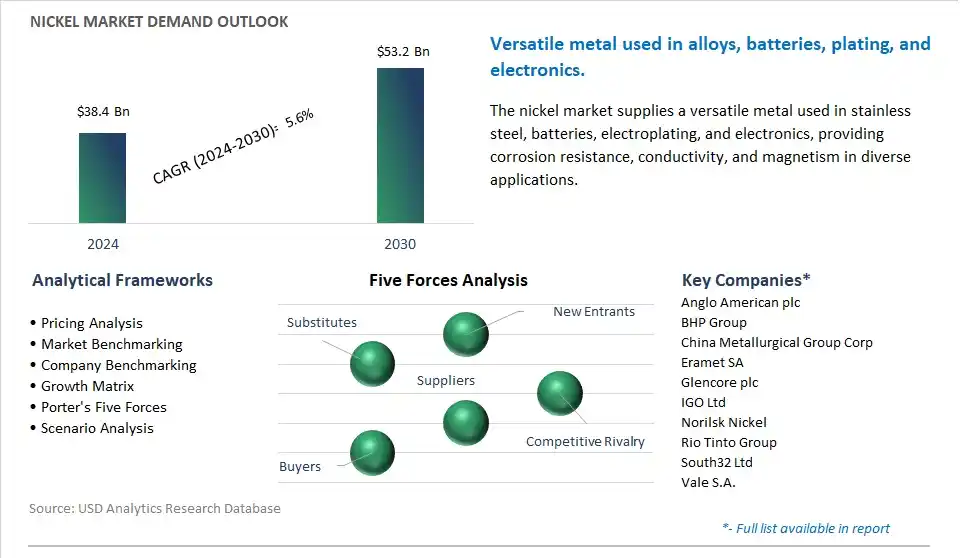

The global Nickel Market is poised to register a 5.6% CAGR from $38.4 Billion in 2024 to $53.2 Billion in 2030.

The global Nickel Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Application (Stainless-steel, Non-ferrous Alloys, Plating, Batteries, Others).

An Introduction to Global Nickel Market in 2024

The nickel market is experiencing dynamic growth driven by its indispensable role in various industries including stainless steel production, electric vehicle batteries, aerospace alloys, and electronics manufacturing. Key trends shaping the future of this industry include the rising demand for nickel in lithium-ion batteries for electric vehicles and energy storage systems, driven by the global shift towards clean energy and electrification. Additionally, advancements in nickel processing technologies are improving efficiency, yield, and environmental sustainability, enabling producers to meet growing demand while minimizing environmental impact. With stainless steel accounting for a significant portion of nickel consumption, the expanding construction, infrastructure, and automotive sectors are driving market growth, particularly in emerging economies with robust urbanization and industrialization trends. Furthermore, the increasing adoption of nickel-based superalloys in aerospace and defense applications for their high strength, corrosion resistance, and temperature stability is fueling market expansion, as aerospace manufacturers seek lightweight and high-performance materials for aircraft engines and components. As industries continue to innovate and invest in sustainable solutions, the nickel market is poised for continued growth, offering opportunities for market players to capitalize on emerging applications, technological advancements, and shifting consumer preferences.

Nickel Market Competitive Landscape

The market report analyses the leading companies in the industry including Anglo American plc, BHP Group, China Metallurgical Group Corp, Eramet SA, Glencore plc, IGO Ltd, Norilsk Nickel, Rio Tinto Group, South32 Ltd, Vale S.A..

Nickel Market Dynamics

Nickel Market Trend: Increased Demand for Electric Vehicles (EVs)

The rise in demand for electric vehicles (EVs) is a significant market trend driving the nickel industry. As the world transitions towards greener transportation solutions to combat climate change and reduce dependence on fossil fuels, the demand for nickel, a key component in lithium-ion batteries used in EVs, continues to surge. The trend is fueled by government incentives, stringent emissions regulations, and growing consumer awareness of environmental issues. As major automotive manufacturers pledge to electrify their fleets, the demand for nickel is expected to remain robust, driving growth in the nickel market.

Nickel Market Driver: Infrastructure Development in Emerging Economies

One of the primary drivers propelling the nickel market forward is the infrastructure development in emerging economies. Countries like China, India, and Brazil are undergoing rapid urbanization and industrialization, leading to a surge in infrastructure projects such as roads, bridges, and buildings. Nickel is essential for stainless steel production, which is widely used in construction due to its durability and corrosion resistance. The increasing investment in infrastructure projects, particularly in Asia-Pacific regions, is fueling the demand for nickel and driving market growth. Moreover, initiatives like China's Belt and Road Initiative are further boosting infrastructure development, creating a favorable environment for the nickel market.

Nickel Market Opportunity: Recycling and Circular Economy Initiatives

A promising opportunity in the nickel market lies in recycling and circular economy initiatives. With growing concerns over resource depletion and environmental sustainability, there is a shift towards adopting circular economy models that emphasize recycling and reuse of materials. Nickel, being a valuable and versatile metal, can be recycled from various sources such as used batteries, stainless steel scrap, and industrial waste. Investing in advanced recycling technologies and establishing efficient recycling infrastructures present an opportunity for stakeholders in the nickel industry to not only meet the growing demand sustainably but also reduce dependency on primary nickel production. Embracing recycling initiatives not only aligns with environmental goals but also opens up new revenue streams and enhances the resilience of the nickel market against supply chain disruptions.

Nickel Market Share Analysis: Stainless-Steel Segment generated the highest revenue in 2024

The Stainless-Steel segment is the largest in the Nickel Market. Nickel is a crucial alloying element in stainless steel production, where it imparts essential properties such as corrosion resistance, strength, and durability. Stainless steel is widely used in various industries, including construction, automotive, aerospace, and household appliances, due to its superior performance and versatility. The demand for stainless steel continues to rise globally, driven by urbanization, infrastructure development, and the growing preference for durable and hygienic materials in consumer goods. Further, advancements in stainless steel manufacturing processes, such as electric arc furnaces and vacuum induction melting, enable the production of high-quality stainless steel with precise nickel content to meet diverse application requirements. Additionally, the recyclability of stainless steel ensures a sustainable supply chain for nickel, further bolstering its dominance in the Stainless-Steel segment of the Nickel Market. Hence, the Stainless-Steel segment is the largest in the Nickel Market, driven by the extensive applications, superior properties, and growing demand for stainless steel in various industries globally.

Nickel Market Report Segmentation

By Application

Stainless-steel

Non-ferrous Alloys

Plating

Batteries

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Nickel Companies Profiled in the Market Study

Anglo American plc

BHP Group

China Metallurgical Group Corp

Eramet SA

Glencore plc

IGO Ltd

Norilsk Nickel

Rio Tinto Group

South32 Ltd

Vale S.A.

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Nickel Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Nickel Market Size Outlook, $ Million, 2021 to 2030

3.2 Nickel Market Outlook by Type, $ Million, 2021 to 2030

3.3 Nickel Market Outlook by Product, $ Million, 2021 to 2030

3.4 Nickel Market Outlook by Application, $ Million, 2021 to 2030

3.5 Nickel Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Nickel Industry

4.2 Key Market Trends in Nickel Industry

4.3 Potential Opportunities in Nickel Industry

4.4 Key Challenges in Nickel Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Nickel Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Nickel Market Outlook by Segments

7.1 Nickel Market Outlook by Segments, $ Million, 2021- 2030

By Application

Stainless-steel

Non-ferrous Alloys

Plating

Batteries

Others

8 North America Nickel Market Analysis and Outlook To 2030

8.1 Introduction to North America Nickel Markets in 2024

8.2 North America Nickel Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Nickel Market size Outlook by Segments, 2021-2030

By Application

Stainless-steel

Non-ferrous Alloys

Plating

Batteries

Others

9 Europe Nickel Market Analysis and Outlook To 2030

9.1 Introduction to Europe Nickel Markets in 2024

9.2 Europe Nickel Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Nickel Market Size Outlook by Segments, 2021-2030

By Application

Stainless-steel

Non-ferrous Alloys

Plating

Batteries

Others

10 Asia Pacific Nickel Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Nickel Markets in 2024

10.2 Asia Pacific Nickel Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Nickel Market size Outlook by Segments, 2021-2030

By Application

Stainless-steel

Non-ferrous Alloys

Plating

Batteries

Others

11 South America Nickel Market Analysis and Outlook To 2030

11.1 Introduction to South America Nickel Markets in 2024

11.2 South America Nickel Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Nickel Market size Outlook by Segments, 2021-2030

By Application

Stainless-steel

Non-ferrous Alloys

Plating

Batteries

Others

12 Middle East and Africa Nickel Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Nickel Markets in 2024

12.2 Middle East and Africa Nickel Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Nickel Market size Outlook by Segments, 2021-2030

By Application

Stainless-steel

Non-ferrous Alloys

Plating

Batteries

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Anglo American plc

BHP Group

China Metallurgical Group Corp

Eramet SA

Glencore plc

IGO Ltd

Norilsk Nickel

Rio Tinto Group

South32 Ltd

Vale S.A.

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Application

Stainless-steel

Non-ferrous Alloys

Plating

Batteries

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)