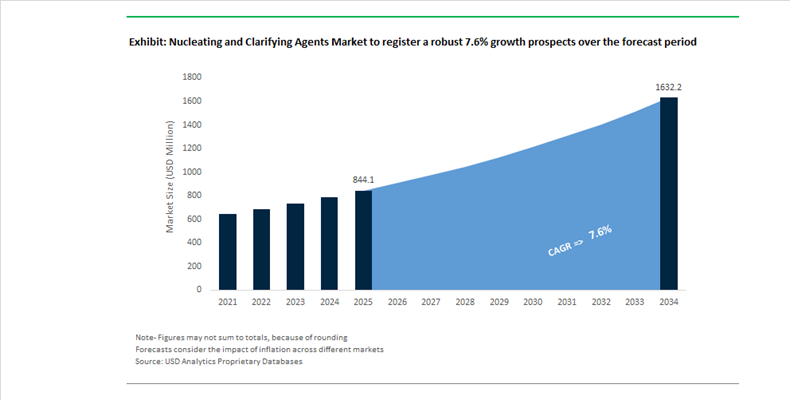

Nucleating and Clarifying Agents Market Valued at $844.1 Million in 2025, Projected to Reach $1,631.9 Million by 2034 at 7.6% CAGR Driven by PP Clarity, EV Components, and Recycled Polymer Performance

The Nucleating and Clarifying Agents Market is valued at $844.1 Million in 2025 and is projected to reach $1,631.9 Million by 2034, expanding at a CAGR of 7.6%. Growth is anchored in rising polypropylene (PP) consumption across food packaging, automotive lightweighting, battery components, and medical devices, where crystallization control directly determines transparency, stiffness, shrinkage, and cycle time. Nucleating agents accelerate polymer crystallization, while clarifying agents refine spherulite size to achieve glass-like transparency in PP. The market is shifting toward ultra-low loading clarifiers, isotropic shrinkage modifiers for thin-wall injection molding, and additives compatible with mechanically recycled resins. Regulatory scrutiny on PFAS, tariff-driven supply chain localization, and energy-efficiency mandates in polymer processing are reshaping procurement and technology strategies across resin producers and converters.

In late 2024, Clariant completed the transition of its additive portfolio to 100% PFAS-free, including nucleator synergists and polymer processing aids, enabling compliance in food-contact and medical applications. During 2024, Adeka Corporation launched its “ADX 2026” mid-term strategy prioritizing eco-friendly polymer additives that enhance recycled plastic performance, targeting ¥115 billion in eco-product sales by fiscal 2026. In February 2025, Adeka’s Fuji Plant began commercial operations of expanded high-purity facilities, strengthening supply of ultra-pure additives critical for precision crystallization in electronics housings. In early 2025, new U.S. tariff measures altered cost structures for imported nucleating agents and precursors, prompting North American producers to emphasize localized manufacturing and supply chain resilience.

Product innovation accelerated through late 2025. In September 2025, OQ partnered with Milliken & Company to launch Luban RP2251T clarified random copolymer using Millad NX 8000 ECO technology. The grade enables up to 10% lower processing temperatures and faster cycle times in food packaging and storage products, directly reducing converter energy consumption. In September 2025, Songwon Industrial Co. showcased nucleating solutions at K 2025 designed to restore stiffness and clarity in mechanically recycled plastics, supporting circular polymer mandates in consumer electronics. In November 2025, Sumitomo Chemical announced restructuring of its lithium-ion battery separator operations, consolidating production in South Korea by March 2026. Separator films require precise crystallization control, reinforcing demand for specialty nucleators in LFP and NMC battery architectures.

In early 2026, Milliken & Company introduced Millad ClearX™ 9000 at Plastindia, delivering glass-like PP transparency at significantly lower additive loadings, reducing waste during resin grade changeovers. At the same event, Milliken highlighted Hyperform® HPN® nucleating agents engineered for isotropic shrinkage in thin-wall injection molding, critical for preventing warpage in automotive bumpers and EV battery trays. Milliken also promoted LeneX™ UGN-52 technology to enhance moisture barrier properties in HDPE and LLDPE packaging, enabling downgauging without compromising shelf life. Concurrently, BASF showcased Irgastab® Cable KV 10 for high-voltage cable insulation, ensuring controlled crystallization in peroxide-crosslinked polyethylene used in renewable power grids.

Nucleating and Clarifying Agents Market Trends and Opportunities

Trend: PCR-Compatible Clarifying Technologies Reshape Circular Packaging Economics

The nucleating and clarifying agents market is undergoing a strategic inflection as packaging producers confront the optical and processing penalties associated with high post-consumer recycled content. Recycled polypropylene and polyethylene streams inherently suffer from yellowing, haze, and inconsistent crystallinity due to thermal history and contaminant residues. As brand owners commit to 2025 and 2030 recycled content targets, clarifying agents are being repositioned from optional performance enhancers to non-discretionary enablers of circular packaging. The launch of Millad ClearX 9000 in October 2025 marked a critical milestone, as it enables the use of mixed virgin and PCR streams without sacrificing transparency or requiring high additive loading. This fundamentally alters resin formulation strategies by eliminating the need for segregated processing lines, reducing inventory complexity and operating costs across large packaging converters.

Regulatory pressure is reinforcing this shift. The EU Packaging and Packaging Waste Regulation, moving toward full enforcement in 2026, places legally binding PCR incorporation thresholds on packaging formats while maintaining recyclability and consumer-facing aesthetics. Clarifiers such as Millad NX 8000 ECO are increasingly specified because they simultaneously improve optical clarity and reduce processing energy by around 10%, supporting both sustainability and margin protection. Competitive intensity has accelerated, as demonstrated by ADEKA’s TRANSPAREX clarifier, introduced in September 2025 and certified as the world’s most effective clarifier. Its ability to deliver premium-level transparency even in recycled polyolefins reflects how optical performance has become a differentiator in closed-loop packaging systems, particularly for food, beverage, and personal care brands that cannot compromise shelf appeal.

Trend: Productivity-Driven Adoption of Nucleating Agents in High-Speed Injection Molding

The rapid expansion of automated e-commerce fulfillment and thin-wall packaging is redefining performance priorities for nucleating agents. In this environment, cycle time reduction translates directly into throughput gains, energy savings, and lower unit costs. Industrial case studies from 2024–2025 show that incorporating as little as 2% of advanced nucleating systems can reduce injection molding cycle times by approximately 13%. On a standard 260-ton molding machine, this improvement equates to hundreds of additional parts per day, achieved primarily by shortening cooling time without compromising dimensional stability.

Material suppliers are responding with integrated solutions that embed nucleation, antistatic behavior, and impact resistance into single resin grades. LyondellBasell’s Pro-fax EP648R, launched in October 2025, exemplifies this approach by targeting thin-walled e-commerce crates and pails that require rapid ejection, stiffness, and process reliability. From a materials science perspective, modern nucleating agents increase the crystallization temperature of polypropylene by 15 to 20 degrees Celsius, allowing parts to be demolded while still hot but structurally rigid. This decoupling of productivity from traditional cooling curves is becoming essential for converters operating at the limits of automation and takt time optimization.

Opportunity: High-Temperature Nucleation for EV and Electrical Components

Electrification and electronics miniaturization are creating a high-margin opportunity for nucleating agents capable of stabilizing engineering plastics under extreme thermal and electrical stress. Electric vehicles built on 800-volt architectures generate sustained heat loads that exceed the performance envelope of conventional plastics. As a result, high-temperature nucleating agents are being qualified for polyamides such as PA66 and PPA to ensure rapid, uniform crystallization at processing temperatures above 250 degrees Celsius. These additives play a critical role in maintaining dielectric strength, creep resistance, and dimensional stability in high-voltage connectors and power electronics.

Beyond thermal resistance, nucleation-driven microstructural control enables further component miniaturization. Fine, homogeneous crystalline structures reduce warpage and internal stress in flame-retardant connectors and sensor housings. This capability is increasingly important for autonomous driving systems and advanced driver assistance modules, where tolerances are tight and component failure has system-level consequences. As EV production scales globally, demand for high-temperature nucleating solutions is expected to grow disproportionately faster than overall polymer volumes, positioning this segment as a strategic growth pillar for additive suppliers.

Opportunity: Bio-Based Nucleating Agents Enable Scalable Compostable Plastics

The expansion of compostable plastics into mainstream food service and industrial packaging is constrained by slow crystallization and poor processing economics. This creates a clear opportunity for bio-based nucleating agents that accelerate crystallization without compromising compostability certifications. Research published in 2025 demonstrates that biomass-derived nucleators such as cellulose nanocrystals, lignin, and amino acids can reduce the crystallization half-time of polylactic acid by more than 50%. This improvement narrows the productivity gap between bioplastics and petroleum-based resins, making high-volume processing commercially viable.

In parallel, formulation advances in PLA and PBAT blends are extending the mechanical performance envelope of compostable materials. Bio-compatible modifiers such as polyvinyl acetate and citric acid have shown measurable gains in tensile strength and toughness, enabling use in heavier-duty packaging applications previously dominated by conventional plastics. Strategic investment patterns indicate that additive producers are moving beyond single-function products toward integrated bio-circular systems that combine nucleation, stabilization, and processing aids in one-pack solutions. As regulatory and brand-driven demand for certified compostable packaging accelerates, bio-based nucleating agents are positioned to become a foundational technology rather than a niche additive.

Nucleating and Clarifying Agents Market Share and Segmentation Insights

Clarifying Agents Dominate Nucleating and Clarifying Agents Market Driven by Transparent Polypropylene Packaging Demand

Clarifying agents accounted for 58.6% of the Nucleating and Clarifying Agents Market share in 2025, establishing them as the leading product category within polypropylene performance additives. These additives, primarily sorbitol-based compounds such as DBS (dibenzylidene sorbitol), MDBS, and DMDBS, play a critical role in modifying the crystallization behavior of polypropylene, enabling the polymer to achieve high optical clarity while maintaining stiffness and processability. Unlike standard nucleating agents that primarily accelerate crystallization, clarifying agents simultaneously provide improved transparency, enhanced gloss, and better mechanical performance, making them essential for applications where product visibility and aesthetic quality are important. Clarified polypropylene is widely used in food containers, beverage cups, medical packaging, laboratory containers, and consumer product packaging, where clear plastics improve product presentation while maintaining the lightweight and cost advantages of polypropylene. In 2025, the rapid expansion of transparent polypropylene packaging for food products has further strengthened demand for clarifying agents, as brand owners increasingly prefer packaging that allows consumers to visually inspect product freshness and quality without opening the package.

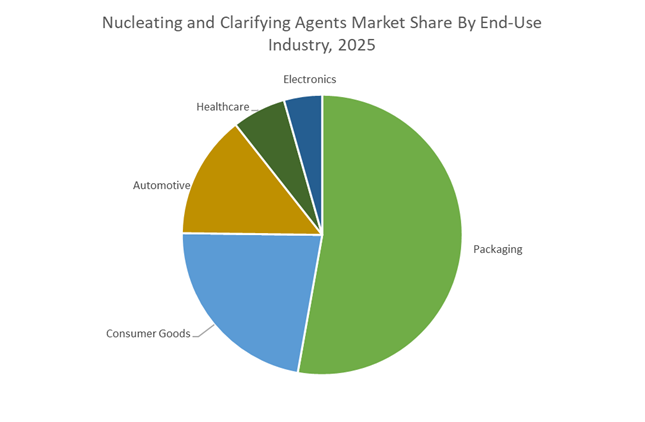

Packaging Industry Drives the Largest Demand for Nucleating and Clarifying Agents

Packaging accounted for 52.8% of the Nucleating and Clarifying Agents Market share in 2025, making it the largest end-use industry due to the widespread adoption of clarified polypropylene in modern food and consumer packaging. Packaging manufacturers rely on nucleating and clarifying additives to improve the optical transparency, mechanical stiffness, and dimensional stability of polypropylene packaging products, enabling the production of thin-walled containers, jars, lids, and deli trays with high clarity and durability. The global shift toward lightweight, recyclable plastic packaging has further increased reliance on polypropylene, where nucleating and clarifying agents enhance both processing efficiency and final product quality. In addition to improving clarity, nucleating additives accelerate polypropylene crystallization during injection molding, allowing shorter cycle times and higher production throughput for packaging manufacturers. In 2025, packaging sustainability initiatives have become a key growth driver, as nucleating agents enable downgauging of plastic packaging without compromising strength or rigidity, reducing overall polymer consumption and lowering the carbon footprint of packaging production while maintaining the transparency and structural performance required for modern food packaging applications.

Nucleating and Clarifying Agents Market Competitive Landscape

The nucleating and clarifying agents market in 2026 is driven by optical clarity enhancement, recyclate performance optimization, and thin-wall polyolefin processing. Competitive differentiation centers on crystallization control, PCR polypropylene enhancement, and EV-grade thermal stability, with innovation focused on high-transparency additives and circular polymer performance.

Milliken leads ultra-clear polypropylene innovation with advanced clarifiers and EV-grade additive integration

Milliken & Company dominates the high-performance clarifying agents market with its Millad ClearX™ 9000, delivering glass-like transparency in polypropylene at lower loading levels, optimizing cost and extraction performance for food-contact and medical packaging. Its Hyperform® HPN® 58ei enhances stiffness-impact balance and improves regrind efficiency, supporting zero-waste thermoforming. LeneX™ UGN-52 strengthens barrier properties in polyethylene, enabling mono-material packaging aligned with recyclability mandates. The RESIST XTR™ portfolio integrates EV colorant technologies with nucleation performance, ensuring thermal stability in high-voltage connectors. Milliken’s material science-driven approach positions it at the forefront of clarity, sustainability, and high-performance polymer engineering.

BASF integrates thermal stabilization and circular additives under VALERAS® platform for high-performance polymers

BASF is leveraging its Verbund model and VALERAS® portfolio to deliver integrated nucleating and stabilizing solutions with verified carbon footprint reduction. Its Irgastab® systems support long-term thermal stability in rotomolded containers and XLPE cable insulation, ensuring durability in energy and infrastructure applications. Tinuvin® NOR® stabilizers enhance UV resistance in agricultural films, supporting high-performance plasticulture solutions. BASF’s additive systems are engineered for processing efficiency and oxidation resistance in high-speed extrusion environments. The company’s focus on circularity and high-performance materials strengthens its position in sustainable polymer additives.

ADEKA accelerates high-clarity and recycling-focused additives through ADX 2026 strategy

ADEKA is advancing its specialty additives portfolio through its ADX 2026 mid-term plan, prioritizing high-value clarifiers and circular polymer solutions. Its ADK TRANSPAREX™ series delivers superior transparency and organoleptic performance for premium packaging applications. The ADK CYCLOAID™ UPR series is designed to stabilize recycled polyolefins, improving melt flow and mechanical properties across multiple processing cycles. ADEKA’s global supply chain expansion supports renewable plastic integration into consumer electronics and high-performance materials. This dual focus on clarity and recyclability positions ADEKA as a key innovator in next-generation nucleating technologies.

Songwon strengthens polymer stabilizer leadership with customized additive systems and recycling performance solutions

Songwon Industrial is enhancing its global footprint through value-based innovation and strategic investments such as its OPS facility in Saudi Arabia, enabling tailored additive packages for petrochemical hubs. Its SONGXTEND® 2124 supports lightweight automotive applications by improving performance in glass-fiber reinforced polypropylene. The SONGXTEND® 2721 stabilizer enhances long-term thermal stability in recycled PP, meeting stringent automotive OEM standards. A 12–20% global price increase reflects cost pressures and reinforces margin protection strategies. Songwon’s focus on customized solutions and recycling compatibility strengthens its competitive edge in polymer stabilization.

Clariant targets high-load stabilization and niche applications with sustainable additive technologies

Clariant is focusing on high-performance, niche additive solutions supported by ISCC PLUS-certified mass balance products. Its integration of Tonnegel™ 50 enhances suspension stability in fertilizers and coatings, demonstrating expertise in crystal growth control relevant to nucleating technologies. Dispersogen™ PSL 100 highlights its strength in dispersion efficiency and additive precision. Despite a 6% revenue decline in 2025, Clariant is targeting 4–6% growth by focusing on high-margin segments such as personal care, agriculture, and industrial additives. Its sustainability-driven approach positions it as a specialized player in advanced polymer additive systems.

United States Nucleating and Clarifying Agents Market: Advanced Recycling, UL Validation, and EV Polymer Innovation Driving Demand

The United States nucleating and clarifying agents market is undergoing a structural transformation driven by advanced recycling technologies, energy-efficient polymer processing, and stringent sustainability mandates. Under the U.S. Plastics Pact Roadmap to 2025, the requirement that 100% of plastic packaging be reusable, recyclable, or compostable is accelerating the shift toward mono-material polypropylene (PP) packaging, significantly boosting demand for high-performance clarifying agents. Industry leaders such as Milliken & Company are capitalizing on this shift, with the launch of Hyperform® HPN® 58ei nucleating agent, specifically engineered to enhance optical clarity, isotropic shrinkage control, and regrind utilization in thermoformed PP applications. These innovations are critical for achieving circular economy compliance and cost-efficient polymer recycling.

From an infrastructure standpoint, over 70 U.S. companies have adopted UL Environmental Claim Validation (ECV)-certified nucleating agents, reinforcing the role of energy-saving additives in reducing processing cycle times and carbon emissions. Additionally, technological breakthroughs such as Georgia Tech’s mechanical-collision PET recycling innovation (2025) are expected to create new demand for specialized nucleators capable of restoring mechanical integrity in recycled resins. The surge in electric vehicle (EV) manufacturing is further amplifying growth, with high-heat nucleating agents like RESIST XTR™ being deployed in EV battery connectors and high-temperature polymer components, positioning the U.S. as a leader in next-generation polymer additive adoption.

Japan High-Performance Clarifying Agents Market: Record-Breaking Transparency and Bio-Based Polymer Nucleation Leadership

Japan continues to dominate the global clarifying agents market through its focus on ultra-high purity additives, optical performance innovation, and bio-based polymer nucleation technologies. At K 2025, ADEKA Corporation achieved a milestone with its TRANSPAREX™ clarifier, officially recognized for delivering record-breaking polypropylene transparency, targeting premium medical packaging and high-end cosmetic applications. This reinforces Japan’s leadership in high-clarity polypropylene (PP) applications, where aesthetic precision and regulatory compliance are paramount.

The country’s ADX 2026 strategic roadmap emphasizes the expansion of environment-friendly polymer additives, particularly sorbitol-based clarifiers that enable lower processing temperatures and reduced energy consumption. Concurrently, cutting-edge R&D from Japan-affiliated institutions has demonstrated that boron nitride (BN) and polyhydroxyalkanoate (PHB)-based nucleating systems can achieve nucleation efficiencies up to 46.2%, significantly enhancing injection molding productivity and crystallization kinetics in bio-polymers. Supported by METI’s Green Innovation Fund, Japanese manufacturers are also pioneering low-dust granular nucleating agent formulations, improving process safety, dosing precision, and automation compatibility across advanced compounding facilities.

Germany Nucleating Agents Market: REACH Compliance, Smart Additives, and AI-Driven Polymer Processing

Germany represents the epicenter of Europe’s nucleating and clarifying agents market, characterized by strict regulatory compliance, high R&D intensity, and rapid adoption of smart additive technologies. Under the EU Circular Economy Action Plan, Germany is enforcing aggressive 2030 recyclability targets, driving demand for non-migratory nucleating agents that ensure food-contact safety and recyclability without chemical contamination. This regulatory push is reshaping additive chemistry toward low-migration, high-performance nucleation systems compatible with closed-loop recycling streams.

Innovation remains a key differentiator, with BASF SE introducing Tinuvin® NOR 600, a next-generation stabilizer that works synergistically with nucleating agents to enhance weatherability and durability in polyolefins and PVC applications such as roofing and artificial turf. The German plastics industry’s €3 billion annual R&D investment is accelerating the development of smart additives enabling downgauging, reducing material consumption while maintaining mechanical strength. At K 2025 in Düsseldorf, the emergence of AI-powered dosing platforms marked a paradigm shift, where real-time sensor data dynamically adjusts nucleating agent concentrations, optimizing processing efficiency, recycled content utilization, and product consistency.

China Nucleating and Clarifying Agents Market: Localization, Specialty Chemical Expansion, and Carbon Footprint Optimization

China’s nucleating agents market is rapidly evolving from volume-driven production to high-value specialty chemical manufacturing, supported by aggressive localization strategies and government-backed industrial ecosystems. The commissioning of BASF’s advanced additive production facility in Nanjing (2025), leveraging Controlled Free Radical Polymerization (CFRP) technology, highlights China’s focus on high-performance dispersants and nucleating agents that enhance polymer stability and color performance.

With over 2,000 plastic product manufacturers transitioning to β-crystal nucleating agents, China is witnessing strong demand in automotive lightweighting and impact-resistant interior components. Government-led initiatives such as the “Green Transformation” policy in Jiangbei New Material Technology Park are prioritizing low Product Carbon Footprint (PCF) additives, aligning domestic production with EU sustainability standards for export competitiveness. Furthermore, Chinese companies like GCH Technology and Shandong Rainwell are aggressively expanding their phosphate ester-based nucleating agent patent portfolios, intensifying competition with global Tier-1 suppliers. The country’s extensive chemical infrastructure and integrated clusters are solidifying its position as a global powerhouse in polymer additive innovation and supply chain resilience.

India Nucleating and Clarifying Agents Market: PLI-Driven Manufacturing, Plastic Parks Expansion, and High-Growth Packaging Applications

India is emerging as a strategic growth hub for nucleating and clarifying agents, fueled by Production Linked Incentive (PLI) schemes, expanding plastic processing infrastructure, and rising domestic demand for high-performance polymers. The ₹41,920 crore investment under the PLI scheme (2025) has significantly boosted the pharmaceutical and medical packaging sectors, increasing demand for high-clarity polypropylene containers enabled by advanced clarifying agents. This aligns with India’s broader push toward self-reliance in specialty chemicals and polymer additives.

Infrastructure development through 9 government-approved Plastic Parks is enabling downstream manufacturers to adopt advanced masterbatch and nucleation technologies, enhancing processing efficiency and product performance. Increased FDI inflows in specialty chemicals, coupled with participation from companies like Plastiblends India and HPL Additives, are fostering customized nucleating solutions tailored to the “Make in India” initiative. Additionally, the rapid expansion of the food packaging sector, particularly microwaveable and high-heat resistant PP containers, is driving demand for β-crystal nucleating agents that improve heat deflection temperature (HDT). With institutions like CIPET establishing Centers of Excellence in polymer applications, India is also advancing R&D in plasticulture and UV-stabilized greenhouse films, reinforcing its role in the global nucleating agents market value chain.

Nucleating and Clarifying Agents Market Report Scope

Nucleating and Clarifying Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$844.1 Million

|

|

Market Size (2034)

|

$1631.9 Million

|

|

Market Growth Rate

|

7.6%

|

|

Segments

|

By Type (Nucleating Agents, Clarifying Agents), By Polymer (Polypropylene, Polyethylene, Polyethylene Terephthalate, Polybutylene Terephthalate, Polyamides), By Form (Powder, Granules, Masterbatch), By End-Use Industry (Packaging, Consumer Goods, Automotive, Healthcare, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Milliken, ADEKA, BASF, Songwon Industrial, Clariant, Evonik Industries, Palmarole, New Japan Chemical, GCH Technology, Zibo Rainwell Chemical, Bruggemann Chemical, Shanxi Provincial Institute of Chemical Industry, H.B. Fuller, LyondellBasell Industries, Stepan

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nucleating and Clarifying Agents Market Segmentation

By Type

- Nucleating Agents

- Clarifying Agents

By Polymer

- Polypropylene

- Polyethylene

- Polyethylene Terephthalate

- Polybutylene Terephthalate

- Polyamides

By Form

- Powder

- Granules

- Masterbatch

By End-Use Industry

- Packaging

- Consumer Goods

- Automotive

- Healthcare

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Nucleating and Clarifying Agents Industry

- Milliken

- ADEKA

- BASF

- Songwon Industrial

- Clariant

- Evonik Industries

- Palmarole

- New Japan Chemical

- GCH Technology

- Zibo Rainwell Chemical

- Bruggemann Chemical

- Shanxi Provincial Institute of Chemical Industry

- H.B. Fuller

- LyondellBasell Industries

- Stepan

*- List not Exhaustive