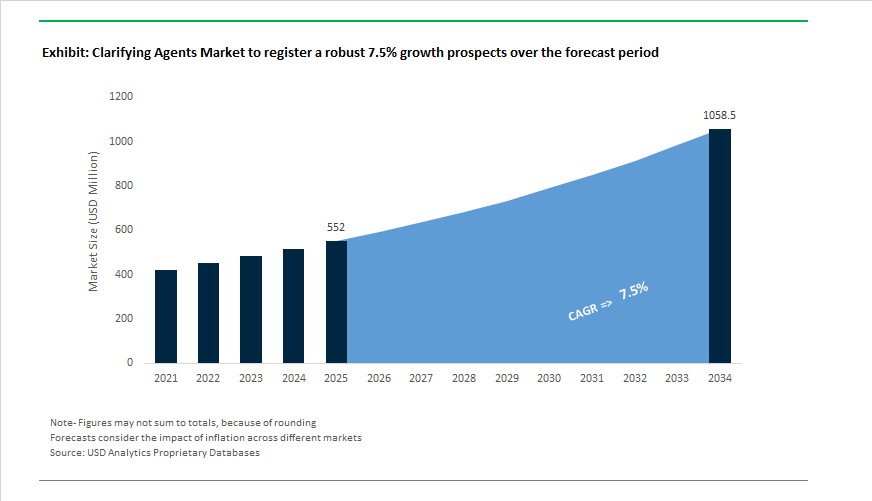

Clarifying Agents Market Outlook 2025–2034: $552 Million to $1,058.3 Million at 7.5% CAGR Driven by High-Clarity Polypropylene and Sustainable Additive Innovation

The global Clarifying Agents Market is projected to expand from $552 Million in 2025 to $1,058.3 Million by 2034, registering a CAGR of 7.5%. Growth is being driven by rising demand for high-transparency polypropylene, nucleating additives for faster cycle times, and sustainable clarifying chemistries aligned with circular packaging mandates. Clarifying agents are increasingly critical in thin-wall food packaging, medical-grade containers, consumer goods, and lightweight automotive components, where optical clarity, reduced haze, improved crystallization kinetics, and energy-efficient processing are essential performance parameters.

Innovation momentum accelerated in 2024–2025. In November 2024, ADEKA launched ADK TRANSPAREX™, which achieved a haze value of 2.2 compared to the 3.2 industry average. In September 2025, this product was certified by Guinness World Records as the most effective clarifier for polypropylene transparency, enabling PP to replace glass and high-cost clear plastics in premium packaging. In October 2025, ADEKA announced a target to expand its clarifier market share to over 60% by 2030, positioning Transparex™ as a tool for monomaterialization strategies that support recyclable PP structures. Milliken reinforced competitive intensity at the K 2025 trade fair in October 2025, showcasing Hyperform® HPN® 58ei, engineered to enhance optical clarity and reduce cycle times in food-contact polypropylene applications compliant with 2025 extraction standards.

Strategic partnerships and energy efficiency validation further strengthened the clarifying agents ecosystem. During October 2025, Milliken highlighted collaborations with resin producers OQ and PolyChim to integrate clarifiers directly into base polypropylene formulations, ensuring consistent optical performance in medical and food packaging. Underwriters Laboratories provided updated Environmental Claim Validation in the 2024–2025 period for Milliken’s Millad® NX® 8000 ECO, confirming average energy savings of 10% for injection molders due to lower processing temperatures. In February 2026, Milliken introduced Millad ClearX™ 9000 at PLASTINDIA 2026, delivering ultra-clear transparency at reduced additive loading levels and minimizing downtime in high-speed injection molding. In the 2025–2026 period, Milliken expanded into polyethylene clarity enhancement through LeneX™ UGN-52, improving barrier properties and enabling downgauging in pharmaceutical and food packaging films.

Sustainability, regulatory reporting, and portfolio restructuring reshaped industry priorities in 2025. BASF launched Trilon® G in April 2025, a 56% bio-based GLDA-derived chelating and clarifying agent designed for home care and industrial applications, signaling broader adoption of biodegradable additive chemistries. In late 2025, BASF accelerated restructuring to concentrate investment on core materials and industrial solutions segments, strengthening focus on plastic additives and clarification technologies. Clariant reported high single-digit growth in its Additives unit in October 2025, driven by pricing performance and operational efficiency programs despite broader macroeconomic softness. In March 2025, Clariant introduced Clarita, an AI-driven tool to manage sustainability reporting under European Sustainability Reporting Standards, improving transparency around chemical additive labeling. Avient expanded its Cesa™ Clarifier and Nucleant portfolio in 2025, targeting faster crystallization rates in polypropylene components used in electric vehicles, aligning clarifying agent innovation with lightweight mobility demand.

Clarifying Agents Market Trends and Drivers

Shift Toward High-Efficiency Clarifiers Enabling Thin-Wall Injection Molding (TWIM) and Energy-Optimized Production

One of the most impactful structural trends in the clarifying agents market is the widespread adoption of next-generation clarifiers engineered for Thin-Wall Injection Molding (TWIM)—a manufacturing priority as converters seek lighter packaging, faster cycle times, and lower energy use.

Data from 2024–2025 industry benchmarks demonstrates that Millad® NX® 8000 ECO enables processing at 190–200°C versus 230°C, delivering ~10% energy savings and 15% faster cycle time reductions—validated by UL Environmental Claim Certification, which enables sustainability-labeling on finished plastic products.

Recent 2025 nucleation research further advances optical performance: solubilized nucleating agent chemistry now produces high-density fibrous crystallites too small to scatter light, achieving <15% haze in 0.5-mm thin-wall parts—a breakthrough aligned with fast-growing shelf-ready clear retail packaging, where visual appeal directly influences sell-through rates and brand placement.

Rise of Multifunctional Masterbatches to Standardize Medical-Grade PP and High-Speed BOPP Production Lines

Manufacturers are consolidating additive packages into single-pellet One-Pack masterbatch systems—reducing compounding error, stabilizing optical quality, and improving compliance in regulated markets.

In late 2025, NX® UltraClear™ medical-grade PP became the industry standard for pre-filled syringes, diagnostic vials, and specimen systems, as converters adopted integrated clarifier-plus-gamma-stabilizer masterbatches to guarantee clarity retention post-sterilization—a known industry challenge.

Meanwhile, the Asia-Pacific packaging sector is rapidly transitioning toward integrated clarifier-and-slip-agent masterbatch systems for BOPP film, driven by line-speed economics. Solutions from Avient and LyondellBasell have demonstrated ~20% reduction in coefficient-of-friction (COF) variation, enabling smoother, uninterrupted high-speed labeling and wrapping across food and personal-care brands.

High-Clarity Polypropylene (PP) Positioned as a Sustainable Substitute for PET and Glass

Clarifying agents are directly shaping material substitution economics as brands face 2025–2030 packaging reduction mandates, such as Lidl’s 20% plastic-reduction goal and EU waste-minimization frameworks.

Comparative studies (2025) demonstrate that clarified PP delivers up to 20% weight savings versus PET—with 1 kg of PP producing ~45 bottles compared to 38 PET bottles. This yield advantage translates into lower transportation emissions per liter of product shipped—a critical KPI measured in corporate ESG reporting. Importantly, clarified PP retains integrity during hot-fill at 90–100°C without heat-set modification, outperforming PET while also offering a lower water-vapor transmission rate, extending shelf life for sauces, condiments, and dry-good packaging without additional barrier coatings.

This creates a procurement-level opportunity for packaging owners to replace multi-material systems (PET + coatings) with single-material clarified PP, simplifying recycling streams and strengthening circular-economy compliance.

Clarifying & Nucleating Agents for High-Temperature Engineering Plastics (PA/PBT/PPS) in EV and Miniaturized Electronics

Beyond polyolefins, clarifying and nucleating agents are expanding into engineering-grade resin systems that fuel EV electrification, high-heat electronics, and compact sensor technologies.

In April 2025, ACS Omega published findings showing that branched copolyesters (PBAT/PBT) leveraging trifunctional nucleating additives exhibit improved melt elasticity and heat resistance above 120°C, enabling structural stability for EV battery housings where thermal distortion and dimensional creep must be minimized.

For polyamide (PA) and polyphenylene sulfide (PPS) in consumer electronics, inorganic nucleating agents have demonstrated ~25% cooling-time reduction during molding—critical to enabling ultra-thin, high-complexity geometries in smartphones, ADAS components, and automotive sensor housings, while maintaining the water-white clarity needed for optical-grade parts.

Clarifying Agents Market Share and Segmentation Insights

Type-Based Segmentation: Sorbitol-Based Clarifiers Dominate While High-Temperature Alternatives Gain Ground

Sorbitol-based clarifying agents account for 68% of market share in 2025, reinforcing their position as the industry standard for polypropylene clarification. Grades such as DBS, MDBS, and DMDBS are widely adopted due to their exceptional haze reduction, FDA food-contact approval, and optimal balance between cost efficiency and optical performance. These agents are critical for producing crystal-clear PP used in packaging and consumer applications. Non-sorbitol-based clarifiers, including trisamide and benzene trisamide chemistries, represent a fast-growing segment as processors seek higher thermal stability for elevated-temperature molding environments where traditional sorbitols may volatilize or degrade. Carboxylic acid salts occupy a specialized niche, often serving dual roles as nucleating and clarifying agents in engineering plastics. Organophosphates continue to lose relative share due to regulatory scrutiny over environmental persistence and toxicity, accelerating the transition toward safer, next-generation sorbitol technologies.

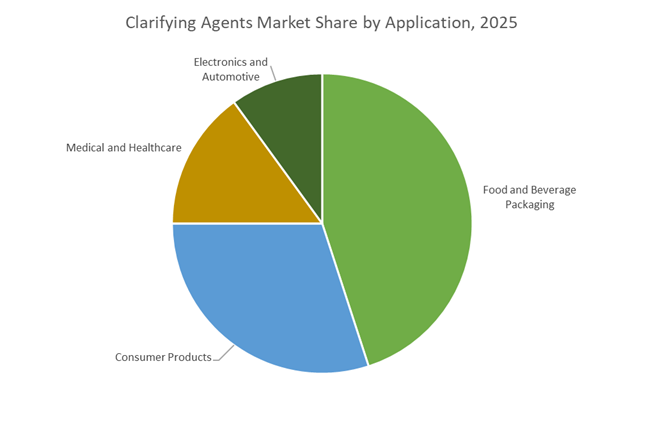

Application Landscape: Food Packaging Leads Demand as Medical and Electronics Drive High-Purity Grades

Food and beverage packaging dominates clarifying agent consumption with 45% market share, driven by rising use of clarified polypropylene in clear containers, deli cups, and microwaveable meal trays. These applications benefit from PET-like transparency combined with superior heat resistance and lower material costs. Consumer products form the second-largest segment, where visual clarity in storage bins, cosmetic jars, and household organizers enhances perceived quality and usability. Medical and healthcare applications rely on ultra-pure clarifying agents for syringes, IV components, and diagnostic devices, where optical clarity enables fluid inspection and patient monitoring under strict biocompatibility standards. Electronics and automotive represent a smaller but expanding segment, supported by demand for transparent housings, display components, and interior trim parts that require both dimensional stability and premium aesthetics. Collectively, these applications underpin steady growth across packaging, medical plastics, and advanced polymer markets.

Competitive Landscape of the Clarifying Agents Market

The Clarifying Agents Market is led by polymer additive specialists and global chemical majors advancing transparency enhancement, nucleating technologies, and sustainability-driven plastic formulations. Competitive differentiation centers on ultra-low loading clarifiers, metal-free organic nucleators, PCR-compatible masterbatches, and Zero Product Carbon Footprint additives for polypropylene and high-melt-flow random copolymers. Market leaders are expanding capacity in Asia, accelerating renewable plastics adoption, and integrating clarifiers with antioxidants and flow modifiers. Strategic priorities increasingly focus on food-contact compliance, energy-efficient processing, and maintaining virgin-like clarity in recycled packaging, medical, and premium consumer applications.

Milliken sets the global benchmark with fifth-generation Millad ClearX transparency

Milliken is the undisputed global leader in clarifying agents, commanding majority market share through its foundational Millad® platform. Its portfolio includes Millad® NX® 8000 and the newly launched Millad ClearX™ 9000, unveiled at Plastindia 2026, delivering ultra-clear transparency at significantly lower additive loadings while improving compatibility for faster production changeovers. Milliken’s clarifiers are UL-certified for energy savings, enabling polypropylene processing at around 200°C and cutting energy consumption by up to 15%. Strategically, the company is prioritizing India as a core growth market, shifting from commodity grades toward premium high-melt-flow random copolymers aligned with its Sustainability through Transparency vision.

ADEKA accelerates high-end polymer clarity through metal-free nucleating chemistry

ADEKA is a major force in high-performance polymer additives, with strong penetration across Asian and European automotive and electronics markets. Its ADK STAB series and upgraded Adeka Transparex clarifiers deliver ultimate-performance transparency for demanding applications. Under its ADX 2026 Mid-Term Management Plan, ADEKA is scaling global specialty chemicals through its Materials as Treasure strategy. In early 2026, ADEKA helped establish the world’s first renewable plastics supply chain for high-performance electronics in partnership with Sony, maintaining recycled plastic clarity via its additives. The company’s core strength lies in metal-free organic nucleating agents fully compliant with stringent REACH and global safety standards.

BASF expands ZeroPCF polymer additives with integrated clarifier solutions in India

BASF integrates clarifying agents within its broader Plastic Additives portfolio, combining Iraclear® clarifiers with Irganox® antioxidants as one-pack solutions for industrial-scale durability and cost efficiency. In February 2026, BASF announced a major expansion in Mangalore, India, adding new production lines for high-performance dispersions and polymer additives to serve the rapidly growing packaging sector. The company is advancing ZeroPCF products to support customer Green Transformation goals, particularly improving recyclability of multilayer films. BASF also strengthened integration via its Global Business Services hub in India, streamlining supply chain coordination and regulatory reporting for global polymer producers.

Clariant targets premium and healthcare plastics with Safe-by-Design clarifiers

Clariant focuses on specialized, high-margin clarifying applications in healthcare and premium consumer goods. Its Licoclear® and Licocene® additives combine clarity enhancement with improved polymer flow properties. Following a leadership transition in January 2026, Marcelo Lu assumed presidency of Care Chemicals, prioritizing sustainable portfolio integration. At CAC 2026, Clariant showcased nano-emulsion coatings and bio-based nanowax emulsions under Synergen Guard to improve surface clarity and protection of agricultural and consumer plastics. Clariant’s competitive edge is its Safe-by-Design chemistry platform, ensuring all clarifiers comply with the strictest FDA and EU food-contact regulations.

Avient customizes medical-grade clarified masterbatches for PCR-ready plastics

Avient, formerly PolyOne, is among the top three suppliers of clarified masterbatches in North America, with a strong focus on medical and pharmaceutical plastics. The company provides medical-grade clarifying systems for pre-filled syringes and diagnostic vials, where particulate visibility is mission-critical. Avient is expanding its CycleWorks™ innovation centers to help brands incorporate higher levels of post-consumer recycled content while retaining virgin-like clarity. Its core strength is custom formulation, delivering single-pellet masterbatches that integrate clarifiers, UV stabilizers, and slip agents, optimizing end-use performance rather than supplying standalone additives.

New Japan Chemical advances sorbitol-based nucleators and low-odor food packaging solutions

New Japan Chemical holds a significant share of the global patent landscape for sorbitol-based clarifying agents through its GEL ALL series of D-sorbitol derivatives, widely used as building blocks in third-party formulations. The company is developing low-odor clarifiers for food containers, addressing the historic almond-like scent associated with high-temperature nucleation. Strategically, it is expanding capacity for high-purity hydrogenated bisphenol A, a key precursor for clear resins in high-voltage electrical insulators. With deep expertise in organic crystal nucleators, New Japan Chemical often operates as an OEM technology partner to global polymer additive leaders.

United States: Scale-Up of Recycling-Compatible Clarifiers and Energy-Efficient Packaging

The United States clarifying agents industry is being reshaped by large-scale capacity expansion, recycling compatibility validation, and downstream energy efficiency mandates across packaging value chains. A defining structural development occurred in late 2024 when Milliken & Company achieved full-scale operations at its largest clarifier manufacturing facility in South Carolina. By 2025, this site increased global output of Millad NX 8000 by 50 %, directly supporting the accelerating adoption of thin-wall injection molded packaging in food, beverage, and household applications. The expansion strengthens supply resilience for clarified polypropylene used in high-speed molding lines where optical clarity and mechanical strength must coexist.

Regulatory and sustainability alignment is reinforcing demand. In 2025, Milliken’s clarifying agents received Critical Guidance Recognition from the Association of Plastic Recyclers, remaining the only polypropylene clarifier validated as fully compatible with existing commercial recycling streams. This recognition has materially influenced converter specifications, particularly as U.S. brand owners respond to extended producer responsibility frameworks. Energy efficiency has emerged as an additional adoption lever. Clarified polypropylene produced using Millad NX 8000 ECO enables average injection molding energy savings of around 10% due to lower processing temperatures, supported by UL Environmental Claim Validation. Market pull is further amplified by a sharp rise in food delivery services during 2025, prompting brand owners to replace PET and polystyrene with clarified polypropylene that offers a superior strength-to-clarity ratio and lower carbon intensity. Strategic partnerships are also shaping resin innovation. In September 2025, Milliken partnered with OQ to launch Luban RP2251T, a random copolymer grade engineered for high-transparency, reusable household products.

Japan: Performance Benchmarking and Monomaterial Design Acceleration

Japan’s clarifying agents landscape is defined by extreme performance differentiation and rapid downstream substitution trends. In October 2025, ADEKA Corporation announced that its TRANSPAREX clarifier achieved Guinness World Records certification as the most effective polypropylene clarifier, delivering a haze value of 2.2 compared with the prevailing industry benchmark of 3.2. This independently verified performance milestone has significantly strengthened customer confidence in clarifier-enabled transparency as a functional replacement for more complex polymers.

Following certification, ADEKA outlined an aggressive growth roadmap aimed at establishing long-term leadership in global clarifying agent revenues by 2030. This ambition aligns closely with Japan’s monomaterialization agenda. During late 2025, electronics and automotive manufacturers increasingly adopted TRANSPAREX-enhanced polypropylene to replace polycarbonate in interior and functional components, supporting the country’s Circular Economy Roadmap targets for 2026. Beyond product innovation, distribution and technical support structures are being streamlined. Effective January 2026, Mitsui Chemicals consigned marketing operations for its high-performance polyamides to Polyplastics Co., Ltd., consolidating additive and polymer expertise across the Asia-Pacific region and improving application development support for specialty polymer additives.

European Union: Purity Regulation, Circular Additives, and Digital R&D

The clarifying agents industry across Germany and the Benelux region is being redefined by stringent additive purity regulation and accelerated circular economy integration. Regulation (EU) 2025/351, effective from March 2025, introduced significantly tighter thresholds for Non-Intentionally Added Substances migration, requiring additive suppliers to demonstrate migration levels below 0.00015 mg per kilogram by September 2026. This regulatory shift has forced clarifying agent manufacturers to redesign formulations, strengthen analytical validation, and prioritize traceability across the polypropylene value chain.

Circularity-driven innovation is advancing in parallel. At the K 2025 trade fair in Düsseldorf, BASF highlighted the evolution of its VALERAS portfolio, emphasizing clarifying and additive solutions that enhance the optical clarity of recycled polypropylene. This capability is increasingly critical as brand owners seek food-contact compliant recycled materials without compromising aesthetics. BASF further reinforced its sustainability positioning by inaugurating a commercial loopamid production facility in early 2025, enabling textile-to-textile recycling of polyamide 6 with a substantial reduction in carbon emissions. R&D processes are also undergoing digital transformation. German chemical clusters integrated the QKnows knowledge management platform during 2025, using artificial intelligence to accelerate the discovery of non-phthalate, sorbitol acetal-based clarifiers that meet both regulatory and performance benchmarks.

India: Policy-Led Capacity Build-Up and Export-Grade Standardization

India’s clarifying agents industry is expanding rapidly under the combined influence of industrial policy, polymer conversion intensity, and export-oriented manufacturing. Under the Production Linked Incentive Scheme 2.0, cumulative investments reached ₹1.76 lakh crore by March 2025, with targeted allocations for downstream specialty chemicals. This policy framework is explicitly aimed at reducing India’s specialty chemical trade deficit while building domestic capabilities in high-purity polymer additives.

Structural demand is reinforced by India’s propylene conversion profile. A 2025 NITI Aayog assessment revealed that approximately 95% of domestic propylene is converted into polypropylene, far exceeding the global average. This creates a large, localized captive market for clarifying and nucleating agents. Infrastructure readiness is improving through the Dahej Petroleum, Chemical and Petrochemical Investment Region in Gujarat, which reached 90% occupancy in 2025 and now hosts multiple production lines for sorbitol-based clarifiers. Export dynamics are further shaping quality expectations. As India transitioned to a net exporter of bulk chemicals in FY 2024–25, domestic manufacturers increasingly adopted global-grade clarifying agents to meet European and U.S. food-contact and medical packaging standards.

China: Localization Mandates and Medical-Grade Polymer Demand

China’s clarifying agents market is entering a consolidation and localization phase driven by industrial policy and healthcare standards. Under the final phase of the Made in China 2025 program, the State Council’s February 2025 Action Plan prioritized domestic production of high-end polymer additives, particularly for medical devices and food packaging applications where import dependence had been structurally high. This policy direction has accelerated investments in indigenous clarifier technologies.

Process innovation is strengthening formulation compatibility. In November 2025, BASF commissioned a high-performance dispersant production line in Nanjing using Controlled Free Radical Polymerization. This technology improves the dispersion and performance consistency of clarifying agents in complex polymer blends. Demand-side regulation is also intensifying. China’s National Health Commission of China updated its Green Hospital guidelines in late 2025, mandating the use of clarified, BPA-free plastics for syringes and laboratory ware. This directive has directly increased domestic demand for high-performance nucleating and clarifying agents compliant with medical-grade polymer specifications.

Comparative Summary: Country-Level Strategic Direction in Clarifying Agents

Clarifying Agents Market County Level Snapshot

|

Country / Region

|

Primary Strategic Driver

|

Industrial Focus

|

Direction of Clarifying Agent Demand

|

|

United States

|

Recycling validation and energy efficiency

|

Packaging and e-commerce

|

Recycling-compatible, low-energy clarifiers

|

|

Japan

|

Ultra-low haze performance

|

Electronics and automotive

|

Monomaterial polypropylene substitution

|

|

EU (Germany & Benelux)

|

Additive purity regulation

|

Circular plastics

|

NIAS-compliant, rPP-optimized clarifiers

|

|

India

|

Industrial policy and propylene intensity

|

Polypropylene conversion

|

Export-grade sorbitol-based additives

|

|

China

|

Localization and healthcare standards

|

Medical and food packaging

|

Domestic, BPA-free nucleating agents

|

Clarifying Agents Market Report Scope

Clarifying Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$552 Million

|

|

Market Size (2034)

|

$1058.3 Million

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Type (Sorbitol-based Clarifying Agents, Organophosphates, Non-Sorbitol-based Clarifying Agents, Carboxylic Acid Salts), By Polymer Type (Polypropylene, Polyethylene, Polyethylene Terephthalate, Polyvinyl Chloride), By Application (Food and Beverage Packaging, Consumer Products, Medical and Healthcare, Electronics and Automotive), By Process (Injection Molding, Extrusion Blow Molding, Thermoforming)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Milliken & Company, ADEKA Corporation, BASF SE, Clariant AG, Evonik Industries AG, Songwon Industrial Co., Ltd., Mitsui Chemicals, Inc., New Japan Chemical Co., Ltd., Rianlon Corporation, Shandong Jiahong Chemical Co., Ltd., GCH Technology, Starchem Enterprises Limited, HPL Additives Limited, Avient Corporation, Fine Organics

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Clarifying Agents Market Segmentation

By Type

- Sorbitol-based Clarifying Agents

- Organophosphates

- Non-Sorbitol-based Clarifying Agents

- Carboxylic Acid Salts

By Polymer Type

- Polypropylene

- Polyethylene

- Polyethylene Terephthalate

- Polyvinyl Chloride

By Application

- Food and Beverage Packaging

- Consumer Products

- Medical and Healthcare

- Electronics and Automotive

By Process

- Injection Molding

- Extrusion Blow Molding

- Thermoforming

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Clarifying Agents Industry

- Milliken & Company

- ADEKA Corporation

- BASF SE

- Clariant AG

- Evonik Industries AG

- Songwon Industrial Co., Ltd.

- Mitsui Chemicals, Inc.

- New Japan Chemical Co., Ltd.

- Rianlon Corporation

- Shandong Jiahong Chemical Co., Ltd.

- GCH Technology

- Starchem Enterprises Limited

- HPL Additives Limited

- Avient Corporation

- Fine Organics

*- List not Exhaustive