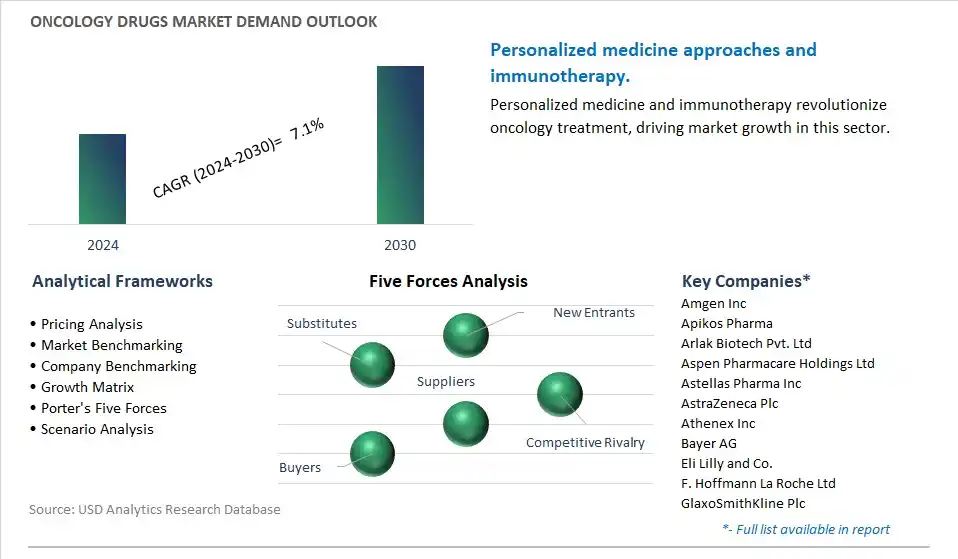

Oncology Drugs Market is estimated to increase at a growth rate of 7.1% CAGR over the forecast period from 2024 to 2030.

The global Oncology Drugs Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments including By Drug Class (Chemotherapy, Targeted Therapy, Immunotherapy, Hormonal Therapy), By Indication (Lung Cancer, Stomach Cancer, Colorectal Cancer, Breast Cancer, Prostate Cancer, Liver Cancer, Esophagus Cancer, Cervical Cancer, Kidney Cancer, Bladder Cancer, Others).

An Introduction to Oncology Drugs Market in 2024

The Oncology Drugs Market remains at the forefront of pharmaceutical innovation and therapeutic advancement in 2024, driven by the growing burden of cancer and the relentless pursuit of novel treatment modalities. With cancer incidence on the rise worldwide, fueled by aging populations, lifestyle factors, and advances in early detection, there is an urgent need for effective pharmacotherapies capable of targeting diverse tumor types and overcoming treatment resistance mechanisms. The market is characterized by a robust pipeline of oncology drugs spanning multiple therapeutic classes, including cytotoxic agents, targeted therapies, immunotherapies, and hormone therapies, with numerous agents advancing through clinical trials and regulatory approvals. Moreover, there is increasing emphasis on precision medicine approaches, biomarker-driven therapies, and combination regimens tailored to individual patient profiles and tumor biology, driving improvements in treatment outcomes and patient survival rates across various cancer indications. As oncology research continues to unravel the complexities of cancer biology and therapeutic resistance mechanisms, the oncology drugs market holds promise for transformative advancements in cancer care and improved patient outcomes in the years to come.

Oncology Drugs Market Competitive Landscape

The global Oncology Drugs Industry is highly competitive with a large number of companies focusing on niche market segments. Amidst intense competitive conditions, Oncology Drugs Companies are investing in new product launches and strengthening distribution channels. Key companies operating in the Oncology Drugs Industry include- Amgen Inc, Apikos Pharma, Arlak Biotech Pvt. Ltd, Aspen Pharmacare Holdings Ltd, Astellas Pharma Inc, AstraZeneca Plc, Athenex Inc, Bayer AG, Eli Lilly and Co., F. Hoffmann La Roche Ltd, GlaxoSmithKline Plc, Johnson and Johnson Services Inc, Kremedine Health Pvt Ltd, Merck and Co. Inc.

Oncology Drugs Market Trend: Personalized and Targeted Therapies

In the Oncology Drugs market, a prominent trend is the increasing focus on personalized and targeted therapies. Traditional chemotherapy has long been a mainstay in cancer treatment, but advancements in molecular biology and genomics have led to a paradigm shift towards precision medicine approaches. Oncology drugs are increasingly being developed to target specific molecular alterations and pathways driving tumor growth and progression. These targeted therapies, including small molecule inhibitors, monoclonal antibodies, and immunotherapies, offer the potential for improved efficacy and reduced toxicity compared to traditional chemotherapy. Moreover, the rise of biomarker-driven therapies enables oncologists to identify patients who are most likely to benefit from specific treatments, leading to more personalized and tailored approaches to cancer care. As the understanding of cancer biology continues to evolve and new therapeutic targets are discovered, the development and adoption of personalized and targeted oncology drugs remain a significant trend shaping the market.

Oncology Drugs Market Driver: Increasing Incidence and Prevalence of Cancer

The primary market driver for Oncology Drugs is the increasing incidence and prevalence of cancer worldwide. Cancer remains one of the leading causes of morbidity and mortality globally, with millions of new cases diagnosed each year. Factors such as population aging, lifestyle changes, environmental exposures, and the growing burden of obesity-related cancers contribute to the rising incidence and prevalence of cancer across diverse geographic regions and demographic groups. Additionally, advancements in cancer screening, early detection, and diagnostic technologies have led to the identification of cancers at earlier stages, driving the demand for effective treatment options to improve patient outcomes and survival rates. Oncology drugs play a crucial role in the management of various cancer types, including breast cancer, lung cancer, colorectal cancer, prostate cancer, and hematologic malignancies, offering patients the potential for disease control, symptom relief, and prolongation of life. As the global cancer burden continues to increase, the demand for innovative oncology drugs that address unmet medical needs and improve treatment outcomes is expected to rise, fueling market growth and investment in cancer research and drug development.

Oncology Drugs Market Opportunity: Immuno-Oncology and Combination Therapies

An emerging opportunity in the Oncology Drugs market lies in immuno-oncology and combination therapies. Immunotherapy, which harnesses the body's immune system to target and destroy cancer cells, has revolutionized cancer treatment and transformed the oncology landscape. Immune checkpoint inhibitors, chimeric antigen receptor (CAR) T-cell therapies, and cancer vaccines represent promising approaches to activate and enhance the anti-tumor immune response, leading to durable responses and improved survival outcomes in patients with various cancer types. Furthermore, there is growing interest in exploring combination therapies that leverage the complementary mechanisms of action of different classes of oncology drugs, such as combining targeted therapies with immunotherapies or chemotherapy, to enhance treatment efficacy and overcome resistance mechanisms. By combining agents that target different pathways involved in tumor growth and immune evasion, combination therapies have the potential to achieve synergistic effects, prolong progression-free survival, and extend overall survival in patients with advanced or metastatic cancers. As research continues to elucidate the complex interactions between the tumor microenvironment, immune system, and therapeutic agents, the development and clinical investigation of immuno-oncology and combination therapies represent promising avenues for advancing cancer treatment and improving patient outcomes. Collaborative partnerships between pharmaceutical companies, academic researchers, and healthcare providers are essential for driving innovation, conducting clinical trials, and translating scientific discoveries into clinically meaningful advances in Oncology Drugs.

Oncology Drugs Market Share Analysis: Immunotherapy for Lung Cancer is the fastest growing market segment over the forecast period to 2030

Among the various drug classes for oncology, immunotherapy stands out as the fastest-growing segment, particularly in the treatment of lung cancer. This growth is propelled by significant advancements in cancer immunology and the development of immune checkpoint inhibitors, which have revolutionized the treatment landscape for lung cancer patients. Immunotherapy works by harnessing the body's immune system to recognize and destroy cancer cells, offering a targeted and potentially more effective approach compared to traditional chemotherapy. In lung cancer, immunotherapy has demonstrated remarkable efficacy, particularly in patients with advanced or metastatic disease who have previously failed standard chemotherapy regimens. Immune checkpoint inhibitors, such as PD-1 and PD-L1 inhibitors, have shown durable responses and prolonged survival in subsets of lung cancer patients, leading to their widespread adoption as standard-of-care treatments in certain settings. Moreover, ongoing research efforts aimed at elucidating the mechanisms of immune evasion and identifying predictive biomarkers for immunotherapy response are further driving innovation in this field. As the understanding of tumor immunology continues to evolve and new immunotherapeutic agents and combinations emerge, immunotherapy is expected to play an increasingly prominent role in the management of lung cancer and other malignancies, offering new hope and improved outcomes for patients facing these challenging diseases.

Oncology Drugs Market Segmentation

By Drug Class

Chemotherapy

Targeted Therapy

Immunotherapy

Hormonal Therapy

By Indication

Lung Cancer

Stomach Cancer

Colorectal Cancer

Breast Cancer

Prostate Cancer

Liver Cancer

Esophagus Cancer

Cervical Cancer

Kidney Cancer

Bladder Cancer

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Oncology Drugs Companies

Amgen Inc

Apikos Pharma

Arlak Biotech Pvt. Ltd

Aspen Pharmacare Holdings Ltd

Astellas Pharma Inc

AstraZeneca Plc

Athenex Inc

Bayer AG

Eli Lilly and Co.

F. Hoffmann La Roche Ltd

GlaxoSmithKline Plc

Johnson and Johnson Services Inc

Kremedine Health Pvt Ltd

Merck and Co. Inc

* List not Exhaustive

Reasons to Buy the Oncology Drugs Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Oncology Drugs Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Oncology Drugs Industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Oncology Drugs Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Analyzed

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Oncology Drugs Market Size Outlook, $ Million, 2021 to 2030

3.2 Oncology Drugs Market Outlook by Type, $ Million, 2021 to 2030

3.3 Oncology Drugs Market Outlook by Product, $ Million, 2021 to 2030

3.4 Oncology Drugs Market Outlook by Application, $ Million, 2021 to 2030

3.5 Oncology Drugs Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Oncology Drugs Industry

4.2 Key Market Trends in Oncology Drugs Industry

4.3 Potential Opportunities in Oncology Drugs Industry

4.4 Key Challenges in Oncology Drugs Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Oncology Drugs Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Oncology Drugs Market Outlook by Segments

7.1 Oncology Drugs Market Outlook by Segments, $ Million, 2021- 2030

By Drug Class

Chemotherapy

Targeted Therapy

Immunotherapy

Hormonal Therapy

By Indication

Lung Cancer

Stomach Cancer

Colorectal Cancer

Breast Cancer

Prostate Cancer

Liver Cancer

Esophagus Cancer

Cervical Cancer

Kidney Cancer

Bladder Cancer

Others

8 North America Oncology Drugs Market Analysis and Outlook To 2030

8.1 Introduction to North America Oncology Drugs Markets in 2024

8.2 North America Oncology Drugs Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Oncology Drugs Market size Outlook by Segments, 2021-2030

By Drug Class

Chemotherapy

Targeted Therapy

Immunotherapy

Hormonal Therapy

By Indication

Lung Cancer

Stomach Cancer

Colorectal Cancer

Breast Cancer

Prostate Cancer

Liver Cancer

Esophagus Cancer

Cervical Cancer

Kidney Cancer

Bladder Cancer

Others

9 Europe Oncology Drugs Market Analysis and Outlook To 2030

9.1 Introduction to Europe Oncology Drugs Markets in 2024

9.2 Europe Oncology Drugs Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Oncology Drugs Market Size Outlook by Segments, 2021-2030

By Drug Class

Chemotherapy

Targeted Therapy

Immunotherapy

Hormonal Therapy

By Indication

Lung Cancer

Stomach Cancer

Colorectal Cancer

Breast Cancer

Prostate Cancer

Liver Cancer

Esophagus Cancer

Cervical Cancer

Kidney Cancer

Bladder Cancer

Others

10 Asia Pacific Oncology Drugs Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Oncology Drugs Markets in 2024

10.2 Asia Pacific Oncology Drugs Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Oncology Drugs Market size Outlook by Segments, 2021-2030

By Drug Class

Chemotherapy

Targeted Therapy

Immunotherapy

Hormonal Therapy

By Indication

Lung Cancer

Stomach Cancer

Colorectal Cancer

Breast Cancer

Prostate Cancer

Liver Cancer

Esophagus Cancer

Cervical Cancer

Kidney Cancer

Bladder Cancer

Others

11 South America Oncology Drugs Market Analysis and Outlook To 2030

11.1 Introduction to South America Oncology Drugs Markets in 2024

11.2 South America Oncology Drugs Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Oncology Drugs Market size Outlook by Segments, 2021-2030

By Drug Class

Chemotherapy

Targeted Therapy

Immunotherapy

Hormonal Therapy

By Indication

Lung Cancer

Stomach Cancer

Colorectal Cancer

Breast Cancer

Prostate Cancer

Liver Cancer

Esophagus Cancer

Cervical Cancer

Kidney Cancer

Bladder Cancer

Others

12 Middle East and Africa Oncology Drugs Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Oncology Drugs Markets in 2024

12.2 Middle East and Africa Oncology Drugs Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Oncology Drugs Market size Outlook by Segments, 2021-2030

By Drug Class

Chemotherapy

Targeted Therapy

Immunotherapy

Hormonal Therapy

By Indication

Lung Cancer

Stomach Cancer

Colorectal Cancer

Breast Cancer

Prostate Cancer

Liver Cancer

Esophagus Cancer

Cervical Cancer

Kidney Cancer

Bladder Cancer

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Amgen Inc

Apikos Pharma

Arlak Biotech Pvt. Ltd

Aspen Pharmacare Holdings Ltd

Astellas Pharma Inc

AstraZeneca Plc

Athenex Inc

Bayer AG

Eli Lilly and Co.

F. Hoffmann La Roche Ltd

GlaxoSmithKline Plc

Johnson and Johnson Services Inc

Kremedine Health Pvt Ltd

Merck and Co. Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise