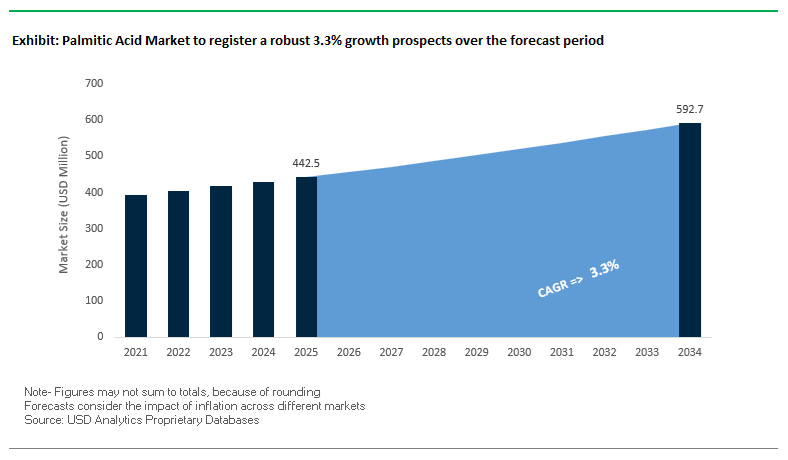

Palmitic Acid Market Valued at $442.5 Million in 2025 with 3.3% CAGR Amid Traceability Mandates and Specialty Oleochemical Expansion

The Palmitic Acid Market is valued at $442.5 Million in 2025 and is projected to reach $592.7 Million by 2034, expanding at a CAGR of 3.3%. Market growth is being shaped by tightening sustainability mandates, vertical integration across palm oil value chains, and rising demand for high-purity fatty acids in personal care, food additives, pharmaceuticals, and industrial lubricants. As one of the most commercially significant saturated fatty acids derived from palm oil and animal fats, palmitic acid remains central to soap manufacturing, surfactants, emulsifiers, metallic stearates, and cosmetic intermediates. Regulatory scrutiny around deforestation, NDPE compliance, and EU deforestation-free supply chain requirements is redefining sourcing strategies across global oleochemical producers.

In October 2024, Emery Oleochemicals expanded its USDA-certified 100% bio-based portfolio, signaling a broader certification push across its fatty acid range, including vegetable-derived palmitic acid. In 2024, Saudi Arabia launched a SR1 billion oleochemicals financing initiative under Vision 2030 to stimulate domestic production of fatty acid derivatives, strengthening regional integration beyond petrochemicals. During 2023 and 2024, Musim Mas released four high-yield oil palm seed varieties to improve plantation productivity without land expansion, directly enhancing long-term feedstock security for palmitic acid production.

Consolidation and downstream integration accelerated in 2025. In April 2025, Godrej Industries acquired the food additives business of Savannah Surfactants, integrating palmitic acid derivatives such as emulsifiers and stabilizers into its processed food ingredient chain. In July 2025, Godrej Industries announced a ₹750 crore capital expansion to double fatty acid and fatty alcohol capacity, positioning itself to achieve $1 billion in global chemicals revenue by 2030. In July 2025, Emery appointed Min Chong as Group CEO and followed in August 2025 with the appointment of its first Global Sustainability Manager to strengthen ESG governance across its certified bio-based oleochemical lines.

Traceability and premiumization are now dominant market drivers. In its 2025–2026 action plan, Wilmar International committed to achieving 100% Traceability to Plantation for its global palm oil supply chain by 2025, ensuring NDPE-compliant sourcing for palmitic acid derivatives. In late 2025, KLK OLEO refreshed its brand identity and launched a dedicated Life Science unit targeting nutraceutical-grade and cosmetic-grade palmitic acid formulations. In March 2025, a major distribution partnership was formed to expand RSPO-certified, plant-based palmitic acid across Europe and Asia in anticipation of stricter 2026 EU environmental labeling rules. In February 2026, Musim Mas achieved CDP “A List” recognition for forests and water stewardship, reinforcing its position as a preferred sustainable supplier to multinational FMCG companies. The competitive landscape is increasingly defined by certified traceable feedstocks, specialty-grade fatty acids, vertical integration, and ESG-aligned capital expansion across Asia-Pacific and the Middle East.

Palmitic Acid Market: Trends and Opportunities Shaping Demand Fundamentals

Regulatory-Driven Shift Toward RSPO-Certified and Segregated Palmitic Acid Supply

The palmitic acid market is undergoing a fundamental sourcing realignment as sustainability compliance moves from voluntary positioning to mandatory market access. The EU Deforestation Regulation has effectively redefined acceptable sourcing standards, requiring companies to prove that palm-derived products are deforestation-free with geolocation-level traceability. As enforcement for large operators begins on December 30, 2025, demand is rapidly shifting away from Mass Balance systems toward Segregated and Identity Preserved supply chains.

Certification benchmarks underline the scale of this transition. According to the RSPO Annual Communication of Progress 2024, Certified Sustainable Palm Oil uptake has exceeded 90% across Europe and North America, while globally certified volumes reached 16.2 million metric tons, accounting for 39% of total production. To operationalize compliance, the RSPO launched its prisma digital traceability platform in 2025, enabling real-time verification of certified palmitic acid flows. For downstream buyers in food, cosmetics, and oleochemicals, RSPO-certified palmitic acid has effectively become a license to operate rather than a price premium attribute.

Functional Reformulation Accelerates Use of Palmitic Acid in Plant-Based Foods

The second major demand driver for palmitic acid is emerging from the maturation of the plant-based food sector. As the industry moves into what is often described as Alternative Protein 2.0, the focus has shifted decisively toward taste, mouthfeel, and cooking performance. Palmitic acid plays a critical role in structured lipid systems due to its high melting point of approximately 63°C, closely mimicking the thermal behavior of animal fats such as tallow and lard.

Market momentum supports this shift. Global plant-based meat and dairy sales reached USD 28.6 billion in 2024, with growth increasingly dependent on fat systems that reduce oil leakage and improve juiciness. Research published in late 2025 shows that palmitic-acid-rich lipid blends significantly improve oil binding capacity, reducing oil-out during cooking and directly addressing leading consumer complaints around dryness and texture. Clean-label considerations further strengthen this trend, with roughly 44% of new bio-based chemical product launches now incorporating palmitic acid derivatives for emulsification and fat structuring, particularly in vegan dairy alternatives that recorded strong foodservice growth in 2024.

Palmitic Acid as a Strategic Feedstock for Sustainable Aviation Fuel

One of the most consequential opportunities for the palmitic acid market lies in sustainable aviation fuel production via the Hydroprocessed Esters and Fatty Acids pathway. Aviation’s Net Zero 2050 commitment has placed intense pressure on SAF availability, with the ReFuelEU Aviation Regulation mandating a 2% SAF blend from 2025, rising to 6% by 2030 and 70% by 2050. Meeting the initial 2025 mandate alone requires an estimated 1.2 million tons of SAF annually in Europe.

The HEFA pathway is expected to dominate SAF supply through 2030 due to its technological maturity, but this has created a growing feedstock gap. Palmitic-acid-rich oils are favored because of their high energy density, intensifying competition between fuel, food, and oleochemical applications. Investment signals are already emerging. Brazil, leveraging its strong oleochemical base, has advanced its National SAF Program, with late-2025 projections indicating substantially higher HEFA production potential than currently announced projects. For palmitic acid refiners, early alignment with SAF value chains represents a first-mover opportunity with long-term offtake visibility.

High-Performance Applications in Lithium-Ion Battery Materials

A newer but rapidly developing opportunity for palmitic acid is emerging in lithium-ion battery manufacturing. As the global battery separator market expands toward a projected USD 9.56 billion valuation by 2030, demand is accelerating for ceramic-coated and bio-enhanced materials that improve thermal safety and electrolyte interaction. Research published in 2024 demonstrates that palmitic acid derivatives can be incorporated into polymer binders and separator coatings to improve electrolyte wettability and electrode structural integrity.

This opportunity is reinforced by cost and regulatory dynamics. Battery component prices rose sharply in early 2024, while the EU Battery Regulation introduced mandatory carbon footprint disclosures starting in 2025. Palmitic acid offers an abundant, bio-derived alternative that can reduce both material costs and embedded emissions. As EV manufacturers prioritize safety, lifecycle sustainability, and cost control simultaneously, palmitic acid-based additives are transitioning from experimental materials to commercially viable battery components.

Palmitic Acid Market Share and Segmentation Insights

Palmitic Acid Derivatives Lead Market Value Through High-Functionality Oleochemical Applications

Palmitic acid derivatives accounted for 42.80% of the Palmitic Acid Market by type in 2025, reflecting strong demand for value-added oleochemical intermediates across cosmetics, soap manufacturing, and industrial formulations. Derivatives such as palmitate esters, palmitoyl chloride, and metal palmitates provide enhanced functionality compared to commodity palmitic acid, supporting applications as emollients, surfactant intermediates, and thickening agents. Compounds including isopropyl palmitate and ethylhexyl palmitate are widely used in personal care products due to their lightweight sensory properties and formulation compatibility. In 2025, esterification driven value addition in oleochemical processing is accelerating, with manufacturers expanding ester production capacity to meet rising demand for natural derived emollients used in advanced skincare, cosmetic formulations, and specialty industrial additives.

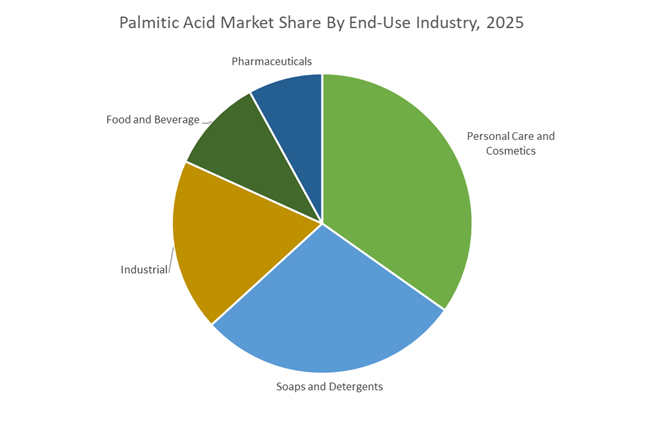

Personal Care and Cosmetics Sector Drives Palmitic Acid Demand in Natural Emollient Formulations

The personal care and cosmetics sector represented 34.80% of the Palmitic Acid Market by end-use industry in 2025, making it the largest consumer of palmitic acid and palmitate derivatives. These ingredients function as emollients, texture modifiers, surfactant intermediates, and conditioning agents in skincare, color cosmetics, and hair care formulations. The expanding global cosmetics industry continues to drive demand for plant derived fatty acids used in premium formulations. In 2025, the growing preference for natural emollients derived from vegetable oils is influencing product selection, with cosmetic manufacturers specifying sustainably sourced palmitic acid to replace petroleum derived ingredients while supporting clean beauty positioning and environmentally responsible cosmetic product development.

Palmitic Acid Market Competitive Landscape

The Palmitic Acid Market is transitioning toward high-purity fractionation, RSPO-certified supply chains, and bio-based specialty esters. Leading players are integrating blockchain traceability, low-carbon refining, and sustainable oleochemicals to meet EUDR compliance, clean beauty demand, and premium pharmaceutical and nutraceutical applications.

Wilmar drives traceability-led palmitic acid supply with integrated plantation-to-refinery model

Wilmar International Limited dominates the palmitic acid market through its fully integrated palm oil value chain and advanced Traceability to Plantation (TtP) infrastructure. By early 2026, the company achieved over 91% traceability across its palm and lauric supply, aligning with EUDR compliance requirements. Its Wilfarin portfolio delivers high-purity palmitic acid (95% and 98%), widely used in MCT production, rubber processing, and metallic soaps. Wilmar is expanding its industrial chemistry segment to include circular-ready fatty acids for biodegradable lubricants and bioplastics. Its RSPO-segregated supply chains provide premium-grade feedstock for personal care and food applications. This combination of scale, traceability, and vertical integration ensures price competitiveness and supply reliability.

KLK OLEO scales pharmaceutical-grade palmitic acid with advanced fractionation and EU footprint

Kuala Lumpur Kepong (KLK) Berhad is strengthening its position in high-value palmitic acid applications through advanced fractionation technology and life sciences integration. The company reported a 73.5% profit increase in 1Q26, driven by stabilized operations at new oleochemical facilities. Its partnership with AAK to operate the Nura refinery enhances production of specialty fats and palmitic-rich fractions for global food markets. KLK’s consolidation of European pharmaceutical operations under the Life Science division enables production of ultra-high purity palmitic acid for APIs and excipients. Its expertise in fractionation supports applications such as vitamin A synthesis and nutraceutical formulations. This focus on high-purity, high-margin segments strengthens KLK’s competitive positioning.

IOI shifts toward premium organic palmitic acid and value-added oleochemical derivatives

IOI Corporation Berhad is repositioning its palmitic acid portfolio toward high-margin, sustainability-driven products. The company is focusing on organic-certified and low-contaminant palmitic acid, which commands premiums of $400–$500 per tonne above conventional grades. Its strategy includes expanding value-added CPO derivatives while targeting 5%–8% growth in fresh fruit bunch production for 2026. Through its stake in Bunge Loders Croklaan, IOI has increased capacity for cocoa butter equivalents that rely on palmitic acid as a structuring component. Efficiency improvements through mechanization and digitalization are expected to reduce production costs by RM200 per metric tonne. This combination of premium positioning and cost optimization enhances IOI’s market competitiveness.

Musim Mas strengthens sustainable palmitic acid supply through ESG leadership and R&D innovation

Musim Mas Group differentiates itself through strong ESG performance and innovation in functional oleochemical applications. The company achieved CDP “A List” recognition for Forests and Water Security and maintains Science Based Targets initiative (SBTi)-validated emissions reduction goals. Its Novel IDEAS Center is developing palmitic acid-based formulations for low-calorie food products and shelf-life enhancement in bakery applications. Operating across 14 countries, Musim Mas ensures global distribution through its ICOF platform, delivering RSPO-certified oleochemicals. The company’s investment in smallholder programs and social sustainability strengthens its supply chain resilience. This focus on environmental transparency and application innovation enhances its competitive position.

BASF advances bio-based palmitic derivatives for clean beauty and sustainable personal care

BASF SE is leveraging its Nutrition & Care segment to convert palmitic acid into high-value bio-based ingredients for cosmetics and home care applications. Its Verdessence™ portfolio replaces microplastics with plant-based polymers derived from fatty acids, aligning with clean beauty and regulatory trends. The Zhanjiang Verbund site enhances regional production of renewable-based performance chemicals in Asia-Pacific. BASF is also prioritizing product carbon footprint transparency, enabling customers to select low-emission palmitic derivatives. Its strong R&D capabilities support the development of advanced emulsifiers and surfactants compliant with Ecocert and Cosmos standards. This integration of sustainability, innovation, and formulation expertise positions BASF as a leader in specialty oleochemicals.

Indonesia – Biodiesel Mandates Reshaping Global Palmitic Acid Balances

Indonesia remains the structural anchor of the global palmitic acid industry, with policy-driven biodiesel demand now exerting direct pressure on oleochemical availability. In late 2025, the Indonesian government confirmed its intention to advance the mandatory biodiesel blending target to B50 by the second half of 2026, materially increasing domestic palm oil absorption. The Ministry of Energy and Mineral Resources allocated 15.6 million kiloliters of biodiesel for 2026, and any acceleration toward B50 is widely expected to push the national palm oil balance toward deficit conditions by late 2026. This policy trajectory tightens feedstock availability for downstream oleochemicals, including palmitic acid, and is already influencing long-term supply contracts and pricing behavior across Asia and Europe. The Domestic Market Obligation framework continues to act as a stabilizing mechanism, requiring producers to fulfill capped-price domestic sales before securing export permits, thereby prioritizing energy security over oleochemical exports during periods of tight supply.

Sustainability governance is becoming equally decisive for Indonesian palmitic acid competitiveness. Dual certification under ISPO and RSPO is being actively expanded, with Musim Mas maintaining a leadership position as the first Indonesian producer to achieve RSPO certification and operating across 13 countries to serve regulated markets. Judicial developments also remain a risk factor. In September 2025, the Indonesian Supreme Court overturned the acquittal of Wilmar, Permata Hijau, and Musim Mas in a high-profile export permit case, an event closely monitored by global traders for potential compliance or permitting disruptions. Parallel to corporate consolidation, the government is strengthening smallholder inclusion through partnerships with APKASINDO, supporting traceability upgrades for the 40% of national output originating from smallholders and aligning supply with EU regulatory expectations.

Malaysia – Certification Density and High-Purity Differentiation

Malaysia’s palmitic acid industry is increasingly defined by certification depth and derivative innovation rather than volume expansion. As of 2025, more than half of Malaysia’s planted palm area is certified under RSPO and or MSPO, enabling Malaysian palmitic acid to command a measurable green premium in international markets. Certified grades are trading at a roughly 10% premium compared with conventional material, reflecting strong demand from European cosmetics, food additives, and pharmaceutical excipient buyers. Yield optimization remains a structural advantage, with national palm oil yields projected to reach 4.6 tons per hectare in 2026, supported by favorable weather patterns and the deployment of precision agriculture technologies.

Downstream innovation is reinforcing Malaysia’s positioning in high-specification applications. Leading producers such as KLK Oleo and IOI Oleochemical expanded their portfolios in 2026 to include fractionated palmitic acid exceeding 98% purity, directly targeting regulated European cosmetics and pharmaceutical markets. Traceability has moved from pilot to standard practice. Blockchain-enabled tools such as Farmonaut are now routinely used by major exporters to demonstrate plot-level deforestation-free compliance, while Roundtable on Sustainable Palm Oil has intensified joint initiatives with NASH and ASB United to ensure Malaysian smallholders remain integrated into certified global supply chains.

China – Transition from Volume Buyer to Sustainability-Oriented Demand

China has completed a strategic shift from being a purely price-driven importer to a value-oriented buyer of palmitic acid. The tenth anniversary of RSPO engagement in China in 2025 marked a milestone, with leading domestic manufacturers now prioritizing Certified Sustainable Palm Oil in procurement decisions. This evolution is being reinforced by consumer-facing sustainability initiatives, including RSPO’s late-2025 biodiversity partnership with the Nanjing Hongshan Forest Zoo, which reflects rising awareness of deforestation-linked risks in food, personal care, and household products.

From an industrial perspective, China remains a critical growth engine for palmitic acid demand, underpinned by its large-scale detergent and soap manufacturing base. Demand is forecast to grow steadily through 2026, with additional upside emerging from bio-based lubricant applications. Venture capital investment exceeding USD 500 million in early 2025 flowed into green chemistry startups developing palmitic acid ester-based biodegradable lubricants, positioning China as an innovation hub for next-generation oleochemical derivatives beyond traditional surfactant uses.

European Union (Germany and Netherlands) – Regulation-Driven Supply Chain Discipline

The European Union is setting the strictest compliance benchmark for palmitic acid imports, fundamentally reshaping sourcing strategies. The EU Deforestation Regulation enters full enforcement on December 30, 2025, requiring all palmitic acid imports to demonstrate that feedstocks were not sourced from land deforested after December 31, 2020. Non-compliance carries penalties of up to 4% of total EU turnover, elevating traceability from a reputational issue to a material financial risk. Germany and the Netherlands, as major import and processing hubs, are already acting as enforcement focal points for the regulation.

This regulatory rigor is translating into measurable commercial outcomes. A 2025 Bloomberg analysis indicated that EU companies with transparent, certified palmitic acid supply chains experienced 30% fewer regulatory-related supply interruptions, reinforcing the return on investment from sustainability compliance. Under RED III, the EU is also incentivizing greater use of crop-based and waste-derived fatty acids, with an estimated 60% of new bulk palmitic acid and derivative orders in 2026 explicitly mandating sustainability certification. As a result, EU buyers are consolidating supplier bases around certified Indonesian and Malaysian producers while exiting relationships with non-compliant origins.

Comparative Summary – Palmitic Acid Industry by Country

Palmitic Acid Market County Level Snapshot

|

Country / Region

|

Primary Demand Driver

|

Policy or Regulatory Lever

|

Strategic Industry Impact

|

|

Indonesia

|

Biodiesel blending (B50)

|

DMO, ISPO, RSPO

|

Supply tightening and export volatility

|

|

Malaysia

|

Certified oleochemicals

|

RSPO, MSPO

|

Premium pricing and high-purity focus

|

|

China

|

Detergents and green lubricants

|

Voluntary sustainability adoption

|

Shift to value-based procurement

|

|

European Union

|

Regulated consumer markets

|

EUDR, RED III

|

Traceability-led supplier consolidation

|

Palmitic Acid Market Report Scope

Palmitic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$442.5 Million

|

|

Market Size (2034)

|

$592.7 Million

|

|

Market Growth Rate

|

3.3%

|

|

Segments

|

By Type (Fractionated Palmitic Acid, Distilled Palmitic Acid, Palmitic Acid Derivatives), By Source (Vegetable-Based, Animal-Based), By Grade (Technical Grade, Food Grade, Pharmaceutical and Cosmetic Grade), By End-Use Industry (Personal Care and Cosmetics, Soaps and Detergents, Food and Beverage, Industrial, Pharmaceuticals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Wilmar International, KLK Oleo, IOI Oleochemicals, Musim Mas Group, Cargill, Sime Darby Plantation, Golden Agri-Resources, PT Sumi Asih Oleochemical Industry, VVF, Emery Oleochemicals, Twin Rivers Technologies, Pacific Oleochemicals, Caila & Pares, PMC Biogenix, Acme-Hardesty

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Palmitic Acid Market Segmentation

By Type

- Fractionated Palmitic Acid

- Distilled Palmitic Acid

- Palmitic Acid Derivatives

By Source

- Vegetable-Based

- Animal-Based

By Grade

- Technical Grade

- Food Grade

- Pharmaceutical and Cosmetic Grade

By End-Use Industry

- Personal Care and Cosmetics

- Soaps and Detergents

- Food and Beverage

- Industrial

- Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Palmitic Acid Industry

- Wilmar International

- KLK Oleo

- IOI Oleochemicals

- Musim Mas Group

- Cargill

- Sime Darby Plantation

- Golden Agri-Resources

- PT Sumi Asih Oleochemical Industry

- VVF

- Emery Oleochemicals

- Twin Rivers Technologies

- Pacific Oleochemicals

- Caila & Pares

- PMC Biogenix

- Acme-Hardesty

*- List not Exhaustive