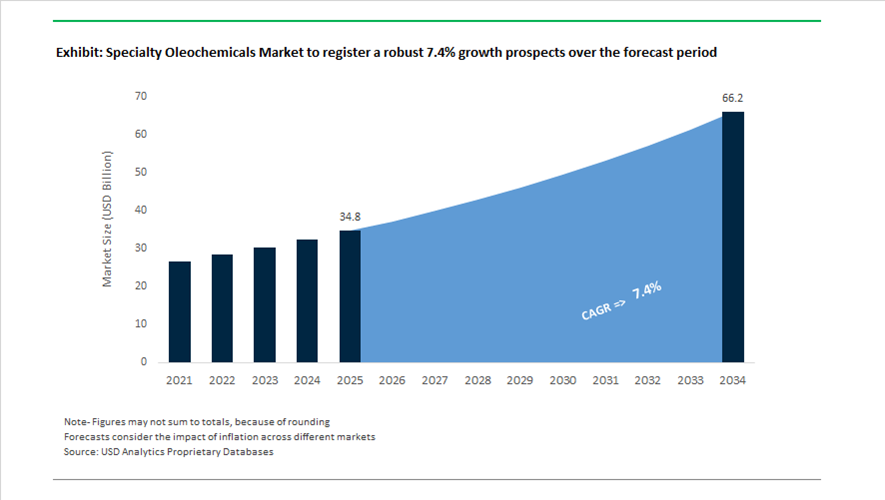

Specialty Oleochemicals Market Valuation 2025–2034: $34.8 Billion to $66.2 Billion at 7.4% CAGR Driven by Bio-Based Esters, High-Purity Life Science Grades, and Sustainable Additives

The global specialty oleochemicals market is valued at $34.8 billion in 2025 and is projected to reach $66.2 billion by 2034, expanding at a robust CAGR of 7.4%. Growth is fueled by accelerating demand for bio-based surfactants, specialty fatty acid esters, oleochemical derivatives, renewable emulsifiers, green solvents, and high-purity phytonutrients across personal care, nutraceuticals, lubricants, EV thermal fluids, coatings, and oilfield chemicals. Specialty oleochemicals derived from palm oil, coconut oil, tallow, and other renewable feedstocks are increasingly replacing petrochemical intermediates due to carbon reduction mandates, ISCC certification requirements, and brand-driven sustainability commitments. The market is witnessing structural migration toward mass-balanced, bio-attributed, and green electricity-based production models aligned with Scope 3 emission targets.

In November 2024, Wilmar International received a silver innovation award at in-cosmetics Asia for its WILSOL SPF Booster, a specialty oleochemical derivative engineered to enhance sunscreen performance while maintaining sustainability credentials. Throughout 2024, Emery Oleochemicals intensified R&D into advanced ester technologies tailored for electric vehicle fluids, focusing on high thermal conductivity and oxidation stability for next-generation battery cooling systems. In December 2024, Wilmar entered a definitive agreement to acquire additional shares in Adani Wilmar Limited, consolidating its leadership position in India’s specialty fats and oleochemical sector. During 2024 and 2025, Oleon N.V. operationalized its $50 million Baytown, Texas plant, scaling North American production of specialty esters and surfactants for lubricant and oilfield applications.

Strategic portfolio expansion and bio-attributed product launches accelerated in 2025. In March 2025, Evonik Coating Additives introduced TEGO® Wet 270 eCO and TEGO® Foamex 812 eCO, its first mass-balanced, ISCC-certified oleochemical additives designed to reduce fossil carbon content in high-performance coatings and inks. In May 2025, Arlanxeo and TSRC opened their expanded Nantong facility in China, serving as a key hub for high-performance additives derived from oleochemical feedstocks for automotive and industrial elastomer applications. In June 2025, Wilmar announced the acquisition of PZ Cussons’ 50% stake in the PZ Wilmar joint venture for $70 million, enabling full integration of its African specialty oleochemical and consumer operations. In October 2025, KLK OLEO launched a dedicated Life Science business unit to centralize high-purity oleochemicals and phytonutrients for nutraceutical and pharmaceutical markets. In the same month, Croda International introduced Natrineo™ CR8, a plant-based specialty emulsifier that secured a silver award at the Pure Beauty Awards, reinforcing demand for natural, high-performance cosmetic stabilizers.

Industry realignment continued into 2026. In February 2026, BASF launched AdBlue® GE produced entirely with renewable electricity, significantly lowering the carbon footprint of this urea-based oleochemical derivative used in diesel emission control systems. In the same month, dsm-firmenich agreed to divest its Animal Nutrition & Health unit to CVC Capital Partners for €2.2 billion, signaling a broader industry pivot toward high-margin human nutrition, beauty, and pharmaceutical-grade specialty chemicals. These developments, including mass-balanced coatings additives, EV-focused ester innovation, green electricity production, life science portfolio specialization, and vertical integration across emerging markets, are reshaping the specialty oleochemicals market landscape through 2034.

Key Trends and Opportunity Hotspots in the Specialty Oleochemicals Market

CPG-Led Renewable Carbon Mandates Accelerating Bio-Surfactant Substitution

The Specialty Oleochemicals Market is experiencing a structural demand inflection as global Consumer Packaged Goods players convert sustainability pledges into enforceable formulation mandates. What was previously a discretionary ESG initiative has become a non-negotiable procurement criterion, particularly for home care, laundry, and personal care applications. Bio-surfactants such as Alkyl Polyglucosides and fatty alcohol ethoxylates are now being specified as direct replacements for fossil-derived linear alkylbenzene sulfonates, driven by lifecycle carbon accounting rather than short-term cost parity.

This shift is most visible in the execution of large-scale climate strategies by multinational brands. Unilever continues to advance its Climate Transition Action Plan with a clear focus on eliminating fossil carbon from cleaning formulations through its Clean Future initiative. By late 2025, renewable carbon sourcing from oleochemical feedstocks had moved from pilot SKUs into core product lines, creating sustained volume pull rather than episodic demand. Importantly, this transition prioritizes supply chain resilience and traceability, favoring oleochemical producers with global, vertically integrated assets.

Supply-side investment has scaled in parallel. BASF expanded its APG production footprint in Bangpakong, Thailand, in November 2025, complemented by planned capacity additions in Cincinnati. These investments are designed to standardize bio-surfactant supply across regions, enabling CPG formulators to deploy uniform recipes globally without exposure to petroleum price volatility. This trend embeds specialty oleochemicals directly into long-term formulation roadmaps, reinforcing durable demand growth through 2030.

Automotive Decarbonization Driving Bio-Based Polyol Qualification

The automotive industry’s transition toward circular vehicle architectures is reshaping material selection for interiors, seating, and coatings. Bio-based polyols derived from epoxidized vegetable oils are now being qualified as functional equivalents to petrochemical polyols, not as niche alternatives. This shift is primarily driven by Scope 3 emissions accounting, where interior materials represent a measurable and addressable carbon reduction lever for OEMs.

At the system level, bio-polyols enable automakers to decarbonize without altering core vehicle design or safety performance. Covestro showcased this strategy at K 2025 through its Circular Intelligence portfolio, which includes polyurethane foams containing at least 25% alternative raw materials. Collaborations with OEMs such as NIO and Volkswagen demonstrate that bio-based foams can meet durability, comfort, and flame-retardancy standards while materially lowering embedded carbon.

Traceability and certification are becoming critical enablers of adoption. ISCC PLUS mass-balance frameworks are now widely used to validate renewable feedstock integration. In July 2025, AGC’s Southeast Asian operations achieved certification to support automotive and construction customers seeking audited low-carbon inputs. This formalization of bio-content verification is accelerating the shift of specialty oleochemicals from optional sustainability upgrades to baseline material requirements in automotive supply chains.

Dielectric Ester Fluids for Data Center and EV Thermal Management

The rapid escalation of AI workloads and ultra-fast EV charging is pushing thermal management beyond the limits of air cooling. This has created a high-margin opportunity for specialty ester fluids derived from oleochemical feedstocks, particularly polyol esters and diesters engineered for dielectric performance. These fluids combine high flash points, electrical insulation, and biodegradability, aligning technical performance with environmental compliance.

In the EV domain, Shell reached a notable milestone in November 2025 by demonstrating a single-circuit thermal management system for an entire battery electric vehicle powertrain. Its EV-Plus Thermal Fluid, formulated using natural and synthetic esters, enabled sub-10-minute charging without compromising battery safety. This achievement underscores how specialty oleochemicals are transitioning from passive lubricants to active enablers of next-generation electrification architectures.

Data center cooling represents a parallel growth vector. Oleon partnered with MIDAS Immersion to certify its Qloe™ bio-based fluids for immersion cooling of high-density servers. As global AI infrastructure faces constraints around energy efficiency and water usage, biodegradable dielectric esters offer a differentiated solution that aligns with both performance and regulatory expectations, positioning oleochemical producers at the center of digital infrastructure investment cycles.

Oleochemical Adjuvants Powering Precision and Biological Agriculture

Agriculture is undergoing a shift from broad-spectrum chemical intensity toward precision delivery and biological efficacy. Specialty oleochemicals are emerging as critical adjuvants and encapsulation agents that enhance the performance of biostimulants, bio-pesticides, and controlled-release fertilizers. Their amphiphilic structure improves wetting, adhesion, and penetration on plant surfaces while maintaining biodegradability.

This opportunity is reinforced by the commercial momentum of biological crop protection platforms. Corteva Agriscience reported double-digit organic growth in 2025, driven largely by demand for its biologicals portfolio. Oleochemical-derived surfactants and oils play a central role in these formulations by stabilizing active ingredients and improving uptake efficiency, directly linking oleochemical demand to yield optimization rather than input volume expansion.

Regulatory pressure further strengthens this pathway. European policy emphasis on reducing synthetic pesticide load per hectare is accelerating interest in oleochemical-based controlled-release coatings. These systems respond to environmental triggers such as moisture and temperature, releasing actives only when agronomically necessary. As a result, specialty oleochemicals are positioned not just as formulation aids, but as strategic tools enabling compliance, sustainability, and productivity in modern agriculture.

Specialty Oleochemicals Market Share and Segmentation Insights

Specialty Esters Lead the Specialty Oleochemicals Market for Personal Care and Industrial Formulations

Specialty esters accounted for 24.80% of the specialty oleochemicals market in 2025, making them the largest product category across bio-based chemical applications. These esters, including isopropyl palmitate, octyl stearate, cetyl esters, and glyceride derivatives, serve as versatile emollients, emulsifiers, and lubricating agents in various formulations. Their properties can be tailored through ester chemistry to deliver specific sensory characteristics, viscosity control, and formulation stability. A significant 2025 market trend is the growing premiumization of personal care formulations, where specialty esters provide lightweight textures, silky skin feel, and high compatibility with plant-derived ingredients, enabling brands to develop high-performance cosmetic products aligned with natural and sustainable ingredient trends.

Personal Care and Cosmetics Sector Drives Global Specialty Oleochemical Consumption

Personal care and cosmetics represent the largest application segment in the specialty oleochemicals market, accounting for 34.80% of total demand in 2025 due to the extensive use of bio-based ingredients in modern cosmetic formulations. Specialty oleochemicals function as emollients, conditioning agents, emulsifiers, and surfactants in skincare, haircare, and color cosmetic products. Their renewable origin and compatibility with natural formulations make them increasingly attractive to brands pursuing sustainable product development. A major 2025 industry trend is the increasing focus on clean beauty and natural formulation strategies, where manufacturers rely on plant-derived esters, fatty alcohols, and bio-based surfactants to replace synthetic ingredients while maintaining product performance, sensory quality, and formulation stability.

Specialty Oleochemicals Market Competitive Landscape

The global specialty oleochemicals market in 2026 is defined by bio-based surfactants, high-purity esters, and biotechnology-driven actives. Leading players are prioritizing RSPO-certified feedstocks, low-carbon manufacturing, and regional expansion in Asia to serve high-growth consumer care, pharmaceutical, and performance materials applications.

Croda Expands High-Purity Oleochemical Portfolio with India Manufacturing Hub and Clean-Label Emulsifier Innovation

Croda International is strengthening its specialty oleochemicals leadership through high-performance bio-based ingredients and strategic expansion in Asia. The inauguration of its Dahej, India facility enhances supply of sustainable oleochemical derivatives for consumer care and pharmaceuticals. Its partnership with Amino GmbH strengthens lipid-based drug delivery and biopharma capabilities. Natrineo™ CR8, a clean-label emulsifier, supports high-stability cosmetic formulations and premium skincare applications. Croda reported 6.6% sales growth in 2025, led by strong consumer care demand. Its net-zero commitment and increased non-fossil raw material usage reinforce its sustainability-driven specialty chemicals strategy.

Wilmar Strengthens Downstream Oleochemical Integration with $1.28 Billion Profit and Strategic JV Consolidation

Wilmar International is leveraging its global palm and lauric oil processing scale to expand into high-margin specialty oleochemicals. The company reported $1.28 billion core net profit in 2025, with strong growth in its Feed and Industrial Products segment. Acquisition of full control in the PZ Wilmar joint venture enhances its consumer chemical portfolio in emerging markets. Its WILSOL SPF Booster highlights innovation in plant-based functional ingredients for sun care applications. Reduced capital expenditure in 2026 signals a strategic shift toward margin optimization and operational efficiency. Wilmar’s integrated supply chain ensures feedstock security and cost competitiveness.

Evonik Accelerates Bio-Based Specialty Additives with SPHINOX® Innovation and Streamlined Global Operations

Evonik Industries is focusing on high-margin oleochemical derivatives through its Custom Solutions and Advanced Technologies segments. The SPHINOX® Vively launch highlights its biotechnology-driven approach to specialty lipid actives in personal care. The "Evonik Tailor Made" program improves operational efficiency and accelerates commercialization of specialty additives. Expansion of hydroxyl-terminated polybutadiene production supports growth in aerospace and industrial specialty fluids. The company achieved €1.87 billion EBITDA in 2025, maintaining strong financial stability. Its focus on beauty, performance materials, and advanced additives strengthens its oleochemical value proposition.

Emery Oleochemicals Advances Green Polymer Additives with Bio-Based Portfolio Expansion and Asia-Pacific Production Shift

Emery Oleochemicals is transitioning toward high-value sustainable oleochemicals through strategic portfolio optimization and regional expansion. Divestment of commodity assets supports its focus on green polymer additives and eco-friendly polyols. Its USDA-certified bio-based pelargonic acid products target lubricants and agricultural applications. ISO 50001 certification at its Cincinnati plant enhances energy efficiency and reduces carbon intensity. The company is developing advanced binder systems for 3D printing metals and ceramics. Its planned Asia-Pacific production complex supports long-term growth in specialty oleochemical markets.

IOI Oleochemicals Enhances Clinical-Grade Oleochemical Production with Energy Optimization and Vitamin E Portfolio Expansion

IOI Oleochemicals is strengthening its specialty oleochemical capabilities through energy-efficient production and high-purity product development. The commissioning of a co-generation plant reduces emissions by 9,000 MT CO2 annually, supporting carbon neutrality goals. Its structured R&D process ensures cGMP-compliant production for pharmaceutical and personal care applications. Solar PV integration enhances energy savings and supply security for specialty derivatives. The DAVOSLIFE E3 portfolio targets high-value nutraceutical and neurocosmetic markets. IOI’s focus on clinical-grade oleochemicals and sustainability strengthens its competitive positioning.

BASF Expands Biomass Balance Oleochemicals with North America Production and India Capacity Growth

BASF SE is advancing its specialty oleochemicals portfolio through biomass balance (BMB) production and global capacity expansion. Commercialization of BMB polyether polyols in North America supports low-carbon automotive and consumer applications. Expansion of dispersions capacity in India strengthens its presence in high-growth construction and coatings markets. Portfolio optimization through divestments allows BASF to focus on high-margin surfactants and performance polymers. Its Care 360° sustainability approach enables customers to reduce carbon footprint without altering manufacturing processes. BASF’s integrated Verbund model ensures efficiency and resilience in specialty oleochemical production.

Malaysia Specialty Oleochemicals Market Advancing into Pharmaceutical and High-Purity Cosmetics

Malaysia has moved decisively up the value chain in specialty oleochemicals by prioritizing pharmaceutical-grade and high-purity cosmetic ingredients. In January 2025, KLK OLEO launched a pharmaceutical-grade portfolio engineered to comply with EU and North American regulatory frameworks, positioning Malaysia as a credible supplier for drug formulation excipients. Parallel portfolio deepening is visible in cosmetics, where KL-Kepong Oleomas introduced DAVOSLIFE E3 DVL 503 during 2024–2025, targeting professional hair care and decorative cosmetics that demand narrow impurity profiles and consistent sensorial performance.

Policy and infrastructure are reinforcing this shift. Under the National Agricommodity Policy 2030, incentives favor conversion of palm kernel oil into high-value esters and alkoxylates, with tax exemptions for firms achieving over 50% local value addition. By late 2025, producers implemented blockchain-based traceability across palm-derived specialty chemicals to comply with EUDR provenance rules, enabling seamless EU market access. The B20 biodiesel mandate has also created a steady crude glycerin surplus, now diverted into domestic glycerol esters and propylene glycol lines, tightening integration between energy policy and specialty oleochemical capacity.

Indonesia Specialty Oleochemicals Market Scaling Upstream Feedstocks and Next-Gen Surfactants

Indonesia’s specialty oleochemicals trajectory is anchored in upstream feedstock expansion and downstream surfactant specialization. The $3.6 billion Cilegon complex by PT Lotte Chemical Indonesia is scheduled to begin production in late 2025, supplying critical intermediates for detergents and surfactants. Complementing this, Chandra Asri advanced construction of its Chlor Alkali–EDC plant, adding 400,000 tons per year of caustic soda, a key reagent for oleochemical refining.

Export performance underscores the pivot. Government data for 2024–2025 shows specialty products rising to 17.35% of chemical exports, with growth concentrated in hair care preparations and natural rubber mixtures derived from palm fatty acids. Industrial policy now targets import substitution of specialty esters and fatty amines by 35%, while Cilegon and Banten are designated hubs for ethoxylates and alkyl polyglycosides. This marks a transition from soap noodles toward higher-margin, application-specific surfactants.

United States Specialty Oleochemicals Market Driven by Bio-Based Expansion and Regulatory Alignment

The United States is strengthening domestic specialty oleochemical capacity through bio-based expansion and regulatory-driven reformulation. In March 2025, Emery Oleochemicals expanded its Cincinnati facility to increase output of bio-based polyols and esters for industrial lubricants and automotive uses. Shortly thereafter, TCL Specialties commenced construction of a New Martinsville plant focused on food ingredients and petro-food intermediates derived from renewable feedstocks.

Regulation is shaping demand profiles. EPA updates to TSCA in 2025 have accelerated the shift toward low-VOC, biodegradable esters for industrial cleaning. Concurrently, pharmaceutical manufacturing growth has driven record demand for USP-grade glycerin, prompting investments in advanced distillation achieving 99.7% purity. Producers are also evaluating refinery upgrades to convert low-value agricultural residues into high-value intermediates, expanding the addressable North American oleochemicals base beyond traditional fats and oils.

Germany Specialty Oleochemicals Market Centered on Circularity and EV Applications

Germany’s specialty oleochemicals sector is aligned with circular economy goals and advanced mobility applications. In early 2025, BASF outlined plans to generate €10 billion in sales from circular Loop Solutions by 2030, including bio-based surfactants for cleaning and cosmetics. Capacity additions are already visible. Vantage Specialty Chemicals expanded METAUPON NMT output at Leuna in 2024 to meet demand for sulfate-free personal care formulations.

Process innovation is another differentiator. German research hubs, collaborating with Novonesis, commissioned industrial-scale enzymatic fat splitting in 2025, reducing energy use by 15% versus thermal hydrolysis. Downstream, automotive suppliers are adopting oleochemical-based dielectric fluids for EV battery immersion cooling, valued for high flash points and biodegradability, reinforcing Germany’s role in specialty esters for electrified mobility.

Thailand Specialty Oleochemicals Market Leveraging Distribution and EEC Incentives

Thailand is positioning itself as a regional specialty oleochemicals distribution and investment hub. In May 2024, Corbion partnered with IMCD to distribute specialty oleochemicals and bio-based ingredients across Thailand, targeting functional food and beverage applications. This alliance accelerates market access and application development for niche oleochemical derivatives.

Investment incentives are catalyzing capacity announcements. Under Eastern Economic Corridor programs, Level 5 tax incentives for bio-chemicals have led to multiple fatty acid methyl ester projects slated for 2026. These incentives are drawing capital toward integrated bio-plastics and bio-chemicals, strengthening Thailand’s midstream role in ASEAN specialty oleochemicals.

Japan Specialty Oleochemicals Market Focused on Non-Palm Feedstocks and Advanced Adhesives

Japan’s specialty oleochemicals market is characterized by innovation in alternative feedstocks and performance-driven derivatives. At SUSMA 2025, Tsuno Oleo debuted specialty chemicals derived from rice bran and used cooking oil, targeting fine-chemical applications that require consistent molecular profiles without palm inputs. This diversification addresses supply resilience and sustainability expectations in Japanese manufacturing.

Product development is extending into advanced materials. In late 2025, Tsuno Oleo accelerated development of bio-based hydrogenated dimer acid, a critical input for high-performance adhesives and surface coatings. These initiatives reinforce Japan’s focus on precision, performance, and feedstock optionality rather than commodity scale.

Comparative Snapshot: Specialty Oleochemicals Industry by Country

Specialty Oleochemicals Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Enablers

|

Market Positioning

|

|

Malaysia

|

Pharma-grade and traceable palm derivatives

|

NAP 2030, EUDR compliance, B20 glycerin

|

High-purity export leader

|

|

Indonesia

|

Upstream feedstocks and next-gen surfactants

|

Cilegon hub, CA–EDC capacity

|

Scale with value migration

|

|

United States

|

Bio-based expansion and low-VOC reformulation

|

TSCA updates, pharma demand

|

Innovation-led domestic growth

|

|

Germany

|

Circular chemistry and EV esters

|

Loop Solutions, enzymatic splitting

|

Premium circular supplier

|

|

Thailand

|

Distribution and bio-chemical incentives

|

EEC tax benefits, alliances

|

ASEAN application hub

|

|

Japan

|

Alternative feedstocks and advanced materials

|

Rice bran oils, dimer acids

|

Precision specialty innovator

|

Specialty Oleochemicals Market Report Scope

Specialty Oleochemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34.8 Billion

|

|

Market Size (2034)

|

$66.2 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Product Type (Specialty Esters, Fatty Acid Methyl Esters, Alkoxylates, Fatty Amines, Specialty Fatty Acids, Bio-Based Surfactants, Bio-Based Solvents and Polyols), By Source (Plant-Based, Animal-Based, Alternative and Microbial), By Application (Personal Care and Cosmetics, Consumer Goods, Food Processing, Healthcare and Pharmaceuticals, Industrial and Lubricants, Polymers and Plastics, Textiles and Leather Chemicals, Paints, Inks and Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Wilmar International Ltd., KLK OLEO, Emery Oleochemicals Group, Evonik Industries AG, Kao Corporation, Cargill, Incorporated, Croda International Plc, IOI Oleochemical, Vantage Specialty Chemicals, Corbion N.V., Godrej Industries Limited, Oleon NV, Stepan Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Oleochemicals Market Segmentation

By Product Type

- Specialty Esters

- Fatty Acid Methyl Esters

- Alkoxylates

- Fatty Amines

- Specialty Fatty Acids

- Bio-Based Surfactants

- Bio-Based Solvents and Polyols

By Source

- Plant-Based

- Animal-Based

- Alternative and Microbial

By Application

- Personal Care and Cosmetics

- Consumer Goods

- Food Processing

- Healthcare and Pharmaceuticals

- Industrial and Lubricants

- Polymers and Plastics

- Textiles and Leather Chemicals

- Paints, Inks and Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Oleochemicals Industry

- BASF SE

- Wilmar International Ltd.

- KLK OLEO

- Emery Oleochemicals Group

- Evonik Industries AG

- Kao Corporation

- Cargill, Incorporated

- Croda International Plc

- IOI Oleochemical

- Vantage Specialty Chemicals

- Corbion N.V.

- Godrej Industries Limited

- Oleon NV

- Stepan Company

*- List not Exhaustive