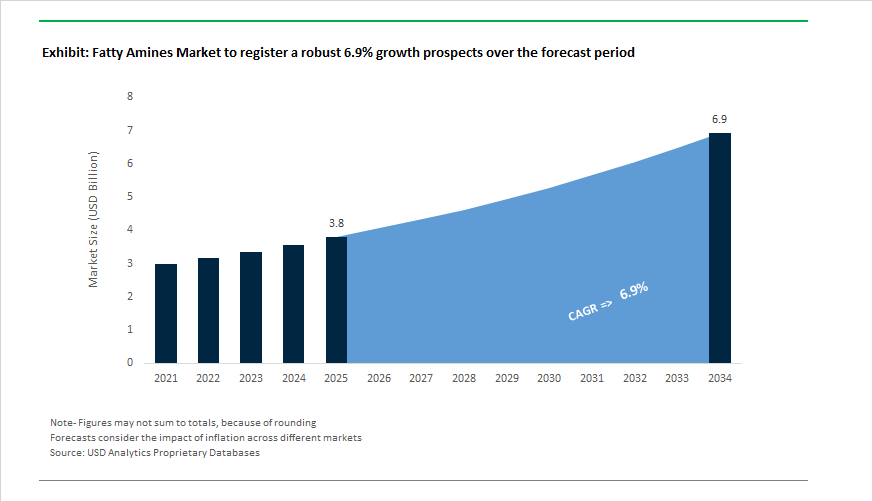

Fatty Amines Market to Reach $6.9 Billion by 2034 from $3.8 Billion in 2025 at 6.9% CAGR Supported by Bio-Based Intermediates, Agrochemical Adjuvants and Polyurethane Catalysts

The global Fatty Amines Market is projected to expand from $3.8 billion in 2025 to $6.9 billion by 2034, advancing at a CAGR of 6.9%. Growth is being driven by rising consumption of primary, secondary, and tertiary fatty amines across agrochemicals, water treatment chemicals, personal care surfactants, oilfield chemicals, polyurethane catalysts, epoxy curing agents, and pharmaceutical intermediates. Regulatory pressure to reduce carbon intensity in chemical manufacturing, expansion of renewable feedstocks, and increasing demand for high-purity amine derivatives in disinfectants and specialty coatings are accelerating capital investment in capacity additions and bio-attributed production systems. Market participants are focusing on regional production hubs to reduce logistics emissions and secure supply chains amid growing demand in North America, Europe, India, and Southeast Asia.

In November 2025, Tosoh Corporation achieved ISCC PLUS certification for its Yokkaichi Complex, enabling mass-balance production of circular and bio-attributed ethylene derivatives that serve as certified sustainable feedstocks for downstream fatty amine synthesis aligned with European Green Deal compliance. In August 2025, Kao Corporation inaugurated a new 20,000-ton annual capacity tertiary amine production plant in Pasadena, Texas, completing its three-site global supply system across the United States, Europe, and Asia under its Mid-term Plan 2027. In May 2025, Nouryon disclosed that 74% of its R&D pipeline now qualifies as Eco-Premium Solutions, including biodegradable fatty amine derivatives designed for lower aquatic toxicity in municipal water treatment applications. In April 2025, Eastman began production of renewable DMAPA ES in Louisiana, a dimethylaminopropylamine grade manufactured using renewable raw materials that reportedly lowers Global Warming Potential by up to 50%, serving as a key intermediate for betaines used in mild personal care formulations. In February 2025, KLK OLEO established KLK OLEO India in Mumbai to strengthen its footprint in fatty acids and fatty amines for home care, pharmaceutical, and industrial chemical sectors across the Indian Subcontinent.

Strategic expansions and restructuring throughout 2024 reinforced regional manufacturing capabilities. In December 2024, Arkema finalized the acquisition of Dow’s flexible packaging laminating adhesives business, strengthening its Specialty Materials segment where fatty amine-based surfactants and performance additives enhance packaging durability and sustainability. In November 2024, Evonik broke ground on the expansion of its specialty amine facility in Nanjing, China, targeting polyurethane catalysts and epoxy curing agents for Asia’s construction and automotive sectors under its Tailor Made program. In August 2024–2025, Huntsman advanced expansion at its Pétfürdő, Hungary site to increase specialty amine and polyurethane catalyst output for European insulation and high-performance automotive materials. In Q3 2024, Nouryon reorganized into three strategic segments to accelerate innovation and capital allocation in Consumer & Life Sciences and Resource Solutions, where fatty amines are essential for agrochemical adjuvants and industrial water treatment. In FY 2024–25, Balaji Amines commissioned a 40,000 TPA methylamines plant to address supply bottlenecks in agricultural chemicals and pharmaceutical active ingredient production. In March 2024, BASF launched a bio-based fatty amine portfolio for personal care and agrochemical applications, delivering drop-in sustainable alternatives to fossil-based amines without compromising surfactant performance metrics.

Trends and Opportunities in the Fatty Amines Market

Strategic Transition to Bio-Based and Mass-Balance Carbon Feedstocks

- Global fatty amine producers are rapidly shifting away from fossil-derived olefins toward renewable and mass-balance-certified carbon sources. This transition is being driven by Scope 3 emission targets, the EU Renewable Carbon Initiative, and procurement requirements from multinational home and personal care brands.

- Between 2024 and 2025, major producers including BASF and Clariant accelerated commercialization of bio-attributed fatty amines using ISCC PLUS-certified mass-balance methodologies. These C12 to C18 fatty amines, derived from sustainably sourced palm kernel and coconut oils, enable downstream customers to claim up to a full reduction in fossil carbon attribution at the molecular level without changing formulation performance.

- In September 2025, Clariant reported that its Care Chemicals division was advancing a CHF 80 million operational excellence and decarbonization program. A central pillar of this initiative is the hydrogenation of fatty nitriles produced from renewable vegetable oils rather than petrochemical intermediates. This shift improves carbon intensity while preserving the consistency required for surfactants, fabric softeners, and conditioning agents.

- Feedstock security is reinforcing this trend in Asia. Indonesia’s implementation of the B40 biodiesel mandate in 2025 has strengthened domestic oleochemical value chains by ensuring stable demand for palm-based fatty acids. For regional fatty amine producers, this has reduced exposure to global petrochemical price volatility while improving long-term raw material availability.

Engineering of Enhanced Quaternary Ammonium Compounds for Persistent Disinfection

- Innovation in fatty amine-based quaternary ammonium compounds is increasingly focused on durability, formulation efficiency, and regulatory alignment rather than simple antimicrobial strength. This evolution reflects the post-pandemic normalization of disinfection across healthcare, food processing, and public infrastructure.

- As of late 2025, more than 200 disinfectant products listed by the U.S. Environmental Protection Agency rely on quaternary ammonium compounds as their primary active ingredient. The market is consolidating around dialkyldimethylammonium compounds, particularly didecyl and dioctyl variants, which maintain biocidal efficacy in hard water and high organic load environments where earlier generations of actives underperformed.

- A major formulation breakthrough has been achieved in wipe-based disinfection. Traditional Quats often adsorb onto cellulose or viscose nonwoven substrates, reducing the amount of active delivered to surfaces. R&D efforts in 2025 produced low-adsorption fatty amine derivatives capable of releasing more than 95% of the active ingredient from the wipe matrix. This has become a critical requirement for hospitals and long-term care facilities seeking reproducible surface hygiene.

- Regulatory history continues to support Quat-based systems. Following the U.S. FDA ban on 19 antimicrobial actives in consumer soaps, fatty amine-derived compounds such as benzalkonium chloride became the default antibacterial standard. Industry usage volumes of these materials remain significantly elevated compared with pre-2020 levels, supporting stable long-term demand.

High-Performance Cationic Asphalt Emulsifiers for Road Recycling

- Infrastructure decarbonization and cost control are creating a strong growth pathway for fatty amine-based asphalt emulsifiers. These materials are essential to cold-mix and recycling technologies that reduce energy use and extend pavement life.

- By November 2025, the Federal Highway Administration had allocated large portions of a USD 591 billion U.S. transportation budget toward roadway rehabilitation. This funding environment has accelerated adoption of cold-in-place recycling and high reclaimed asphalt pavement content mixes, both of which depend on cationic fatty amines such as tallow diamines and imidazolines.

- The global recycled asphalt market is valued at approximately USD 9.0 billion in 2025. Fatty amine emulsifiers enable ionic bonding between bitumen and aggregate at ambient temperatures, allowing up to full reuse of existing road surfaces. This chemistry delivers early strength development, enabling roads to reopen within hours and minimizing traffic disruption.

- Product innovation is reinforcing durability. Nouryon expanded its Redicote® emulsifier portfolio during 2024–2025 to address moisture sensitivity and stripping issues in high-RAP formulations. These advances are particularly relevant for municipal and secondary road networks, where recycled materials historically underperformed.

Critical Processing Aids in Lithium-Ion Battery Component Manufacturing

- Fatty amine derivatives are emerging as high-value enablers in lithium-ion battery manufacturing, particularly in electrode slurry preparation and coating processes.

- In NMC cathode production, quaternary ammonium surfactants derived from fatty amines are used to disperse conductive carbon black and carbon nanotubes in N-methyl-2-pyrrolidone-based slurries. These dispersants prevent agglomeration, ensuring uniform electrode coatings and consistent electrochemical performance.

- Pilot-scale manufacturing data from 2024–2025 indicates that amine-based dispersants can improve active material loading by approximately 2 to 3%. This translates directly into higher energy density at the cell level. In addition, these materials act as secondary binders that enhance adhesion between the electrode layer and the current collector, improving cycle stability under repeated charge-discharge expansion.

- Environmental pressures are shaping the next phase of opportunity. With growing regulatory scrutiny on NMP toxicity, battery manufacturers are accelerating development of water-based electrode processing. Fatty amine derivatives are being actively evaluated as compatible dispersants and binders in aqueous systems, positioning them at the center of the industry’s transition toward safer and lower-emission battery manufacturing platforms.

Competitive Landscape of the Fatty Amines Market

The global Fatty Amines Market is defined by vertically integrated oleochemical leaders and specialty chemical majors competing on sustainable surfactants, tertiary amines capacity, ultra-low-color grades, and application-driven innovation across personal care, agrochemicals, oilfield chemicals, and water treatment.

Nouryon advances premium fatty amines through specialization and ultra-low-color innovation

Nouryon holds a top-tier global position in fatty amines in 2026, with a significant revenue contribution from its Armeen® portfolio covering primary, secondary, and tertiary amines. Following its separation from AkzoNobel, the company shifted toward “specialization over volume,” optimizing its global production network to meet rising demand for sustainable surfactants in Europe and North America. In 2025 to 2026, Nouryon introduced ultra-low-color fatty amines aimed at premium personal care formulations where visual clarity is critical. Its core strength lies in deep application expertise in oilfield chemicals, supplying corrosion inhibitors and emulsifiers for deep-water drilling, reinforcing its leadership in high-performance industrial intermediates.

Global Amines Company builds RSPO-certified scale with the world’s largest integrated oleochemical complex

Global Amines Company (GAC), a 50:50 joint venture between Clariant and Wilmar, fully operationalized its third world-scale tertiary amines plant in Gresik, Indonesia in 2026, now the largest integrated oleochemical complex globally. Leveraging Wilmar’s palm oil feedstock dominance, GAC delivers total vertical integration and stable pricing even during commodity volatility. In late 2025, the JV acquired Clariant’s Quats and Esterquats business for over $110 million, transforming GAC into a one-stop supplier for amine-based fabric softeners and biocides. Its 2026 strategy centers on fully segregated, RSPO-compliant fatty amines aligned with EU Deforestation Regulation requirements.

Kao Corporation expands tertiary amines in Texas to capture North American hygiene demand

Kao Corporation strengthened its fatty amines footprint by commissioning a world-scale tertiary amines plant in Pasadena, Texas in late 2025, targeting hygiene and industrial cleaning growth in North America. Its Farmin® series supplies high-purity tertiary amines used as precursors for betaines and amine oxides in mild detergents and shampoos. In 2026, Kao launched “Precision Selective Cleansing,” a formulation approach that optimizes amine chain length to enhance cleaning while minimizing skin irritation. Under its K27 mid-term plan, Kao is aggressively scaling specialty amines outside Japan, aiming for double-digit operating margins by 2027 through value-added chemical derivatives.

BASF SE lowers product carbon footprint while scaling epoxy and agrochemical amine intermediates

BASF SE leverages its Verbund integration at Ludwigshafen and Antwerp to efficiently synthesize specialty and fatty amines from ammonia and alcohols. In 2025, BASF committed to converting its entire European amines portfolio to 100% renewable electricity by 2026, materially reducing Product Carbon Footprint for B2B customers. The company also launched Baxxodur® EC 151 in late 2025, a novel amine building block for sustainable industrial flooring epoxies. BASF dominates the agrochemical segment, supplying critical amine intermediates for modern herbicides and fungicides, while maintaining cost leadership through deep backward integration and energy-efficient cross-plant operations.

Evonik Industries AG accelerates bio-based tertiary amines for Asia-Pacific growth and EV applications

Evonik Industries AG expanded its specialty amines plant in Nanjing, China in early 2026, strengthening its presence in Asia-Pacific, the fastest-growing fatty amines market. The company targets EBITDA margins of 18 to 20% in 2026 across specialty additives, driven by high-purity amines for EV battery cooling fluids and pharmaceutical synthesis. Evonik’s “Next Generation Solutions” strategy aims to unlock over €1 billion in innovation-led sales, including bio-based amines for circular economy applications. It also specializes in tertiary fatty amines for municipal and industrial water treatment, supplying high-performance flocculants and anti-scaling agents for wastewater systems worldwide.

Fatty Amines Market Share and Segmentation Insights

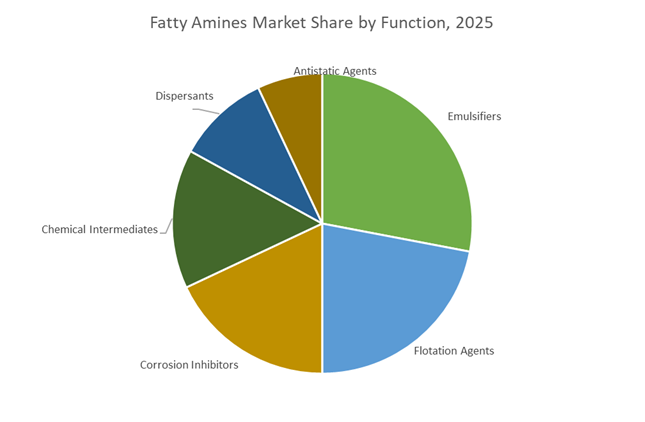

Emulsifier Functions Lead Adoption Across Agrochemical and Industrial Formulations

Emulsifiers account for 28% of total fatty amines market share in 2025, reflecting their critical role in stabilizing oil–water systems across agrochemicals, personal care, and industrial formulations. Fatty amines are widely used in pesticide concentrates, herbicide emulsions, and cosmetic creams due to their cationic surface activity and ability to reduce interfacial tension. Flotation agents form the second-largest functional segment, driven by mineral beneficiation in potash, phosphate, and iron ore processing where primary amines and ether amines act as selective collectors. Corrosion inhibitors maintain strong demand in oil and gas, water treatment, and metalworking fluids, forming protective films on steel surfaces. Chemical intermediates support downstream production of quaternary ammonium compounds and specialty surfactants, while dispersants are gaining momentum in paints, coatings, inks, and drilling fluids. Antistatic agents remain niche, serving plastics and textiles where static control improves handling and product quality.

Agrochemicals Drive Core Demand Supported by Energy and Water Infrastructure

Agrochemicals represent 32% of global fatty amines consumption in 2025, making agriculture the largest end-use sector. Fatty amines function as emulsifiers and adjuvants in herbicides, fungicides, and insecticides, enhancing spray coverage and active ingredient penetration to support global crop productivity. Oil and gas follow as a major segment, utilizing fatty amines for corrosion inhibition, crude oil demulsification, and oil sands flotation to protect critical assets. Water treatment maintains significant uptake through corrosion control, flocculation, and biocidal applications in municipal and industrial systems. Chemical processing relies on fatty amines as intermediates for surfactants and performance additives, while personal care and cosmetics represent a fast-growing segment using amine derivatives as conditioning agents and emulsifiers. Infrastructure applications remain steady, spanning asphalt emulsifiers, mining operations, and construction materials.

United States Fatty Amines Market: Tertiary Amine Capacity Expansion, Renewable Energy Transition, and High-Purity Conditioning Agents

The United States Fatty Amines Market is undergoing a structural transformation centered on tertiary fatty amine capacity expansion and high-margin specialty derivatives for personal care, pharmaceuticals, and energy applications. In Aug 2025, Kao Corporation inaugurated a large-scale tertiary amine production facility in Pasadena, Texas, targeting surging demand for high-purity amines across North American beauty and healthcare sectors. This investment reinforces the U.S. as a strategic hub for tertiary amines used in conditioning agents, emulsifiers, and specialty surfactants.

Eastman Chemical Company completed multi-million $ upgrades to its DIMLA 1214 tertiary amine production lines in Pace, Florida and Ghent, Belgium, enhancing supply reliability and operational flexibility. In June 2025, Nouryon launched an Innovation Center for Oilfield Solutions in Texas, focusing on amine-based corrosion inhibitors and demulsifiers for shale gas extraction. Sustainability initiatives include transitioning Texas ethoxylation and amination sites to 100% renewable electricity, reducing Scope 2 emissions across domestic surfactant production. Rapid adoption of fatty amines as rain-fast agrochemical adjuvants and conditioning agents supported a 9.7% increase in related chemical service expenditure in late 2024, underscoring strong end-use momentum in both agriculture and premium personal care formulations.

China Fatty Amines Market: Integrated Oleochemical Clusters, 5% Output Growth Target, and Catalyst Optimization

China’s Fatty Amines Market is shifting from commodity output toward high-value oleochemical derivatives under its 15th Five-Year Plan framework. The Ministry of Industry and Information Technology of China has implemented a 2025–2026 strategy targeting ≥5% annual growth in chemical industry value-added output, specifically incentivizing high-purity primary, secondary, and tertiary fatty amines.

In Nov 2024, Evonik Industries allocated several million € to expand its amine product line in China using locally sourced raw materials to strengthen North Asian supply chains. Nouryon finalized expansions of its organic peroxide and amine-related facilities to support domestic polymer and surfactant growth. China maintains global dominance in fatty amine-based flotation agents used in phosphate beneficiation, critical for fertilizer self-sufficiency. Stricter 2025 VOC regulations are driving demand for low-odor, high-purity amines in paints and coatings. Additionally, Chinese producers are deploying AI-driven catalyst optimization in fatty nitrile hydrogenation processes, improving tertiary amine yields by up to 3% annually, enhancing competitiveness and production efficiency.

Germany Fatty Amines Market: Bio-Based Surfactants, Circular Carbon Strategy, and Continuous Amination Efficiency

Germany sets the global benchmark in green chemistry and circular carbon integration within the Fatty Amines Market. Evonik Industries launched the world’s first industrial-scale rhamnolipid plant during 2024–2025, introducing bio-surfactants that partially replace conventional petrochemical surfactants in cleaning applications. Infrastructure optimization under SYNEQT at the Marl and Wesseling chemical parks is enhancing energy and steam integration for large-scale amine synthesis facilities.

In Feb 2026, Evonik announced a revised dividend policy to prioritize Next Generation innovation, including membrane-based amine separation and carbon-neutral processing. Germany is harmonizing its national Supply Chain Due Diligence Act with the EU CSDDD, compelling fatty amine producers to implement stringent ESG traceability for palm and tallow feedstocks. German manufacturers are transitioning to continuous amination processes, reducing energy consumption per tonne by approximately 15% compared to batch systems. The country remains Europe’s strategic hub for potash flotation reagents, where cationic fatty amines are essential for maximizing KCl recovery in mining operations, reinforcing Germany’s technological leadership in specialty amine chemistry.

India Fatty Amines Market: ₹2.16 Lakh Crore PLI Momentum, Export Surplus, and Agrochemical Growth

India’s Fatty Amines Market is accelerating under the Production Linked Incentive framework, with realized investments surpassing ₹2.16 lakh crore, equivalent to $26B+, by Dec 2025. This capital inflow is expanding domestic production of bulk amine-based surfactants and specialty intermediates. India recorded a net trade surplus of ₹2,280 crore in FY 2024–25 across pharmaceuticals and specialty chemicals, driven in part by global demand for amine catalysts, curing agents, and agrochemical intermediates.

Nouryon partnered with Atul Ltd to strengthen supply of high-purity amines for India’s fast-growing agrochemical and home care markets. Dedicated Bulk Drug Parks in Andhra Pradesh are centralizing demand for fatty amines used in API synthesis. Late 2025 environmental clearance approvals in Gujarat for Monochloroacetic Acid and related amine derivative expansions further enhance backward integration. A 12% increase in fatty amine-based asphalt additives under the Gati Shakti infrastructure initiative highlights strong domestic demand in road construction and bitumen modification applications.

Brazil Fatty Amines Market: 100% Renewable Power, Bio-Based Feedstock Leadership, and Agricultural Adjuvant Dominance

Brazil commands a strategic position in the Fatty Amines Market through integration of vegetable oil and tallow-based feedstocks. In Aug 2025, Nouryon expanded South American sodium chlorate and related chemical capacity by 20% to support the Brazilian pulp and paper industry, where amine-based biocides and process aids are critical.

Nouryon’s Brazilian network transitioned to 100% renewable electricity in 2025, setting a global benchmark for decarbonized fatty amine production. Long-term supply agreements with Suzano reinforce Brazil’s leadership in eucalyptus pulp processing, where amine-based defoamers and corrosion inhibitors are essential. Unlike gas-dependent hubs in North America and Europe, Brazilian amine production benefits from biomass-derived energy and feedstocks, reducing exposure to natural gas volatility. Mato Grosso do Sul has emerged as a key integrated oleochemical cluster serving the MERCOSUR region. Brazil also dominates agricultural adjuvant consumption for soybean and sugarcane cultivation, where amine-based wetting agents and surfactants are indispensable for large-scale aerial spraying efficiency.

Fatty Amines Market Report Scope

Fatty Amines Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.8 Billion

|

|

Market Size (2034)

|

$6.9 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Type (Primary Fatty Amines, Secondary Fatty Amines, Tertiary Fatty Amines), By Product Form (Coco Amines, Tallow Amines, Oleyl Amines, Soya Amines, Stearyl Amines), By Function (Emulsifiers, Flotation Agents, Corrosion Inhibitors, Dispersants, Chemical Intermediates, Antistatic Agents), By End-Use Industry (Agrochemicals, Oil and Gas, Water Treatment, Personal Care and Cosmetics, Infrastructure, Chemical Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nouryon, Evonik Industries AG, Kao Corporation, Clariant AG, Huntsman International LLC, BASF SE, Solvay S.A., Arkema S.A., Eastman Chemical Company, India Glycols Limited, Balaji Amines Limited, Indo Amines Limited, Global Amines Company, KLK Oleo, Ecogreen Oleochemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fatty Amines Market Segmentation

By Type

- Primary Fatty Amines

- Secondary Fatty Amines

- Tertiary Fatty Amines

By Product Form

- Coco Amines

- Tallow Amines

- Oleyl Amines

- Soya Amines

- Stearyl Amines

By Function

- Emulsifiers

- Flotation Agents

- Corrosion Inhibitors

- Dispersants

- Chemical Intermediates

- Antistatic Agents

By End-Use Industry

- Agrochemicals

- Oil and Gas

- Water Treatment

- Personal Care and Cosmetics

- Infrastructure

- Chemical Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Fatty Amines Industry

- Nouryon

- Evonik Industries AG

- Kao Corporation

- Clariant AG

- Huntsman International LLC

- BASF SE

- Solvay S.A.

- Arkema S.A.

- Eastman Chemical Company

- India Glycols Limited

- Balaji Amines Limited

- Indo Amines Limited

- Global Amines Company

- KLK Oleo

- Ecogreen Oleochemicals

*- List not Exhaustive