Patchouli Oil Market Overview 2025–2034: $66.6 Million Market Size in 2025 Growing at 3.9% CAGR Driven by Premium Fragrance Reformulation and Sustainable Sourcing

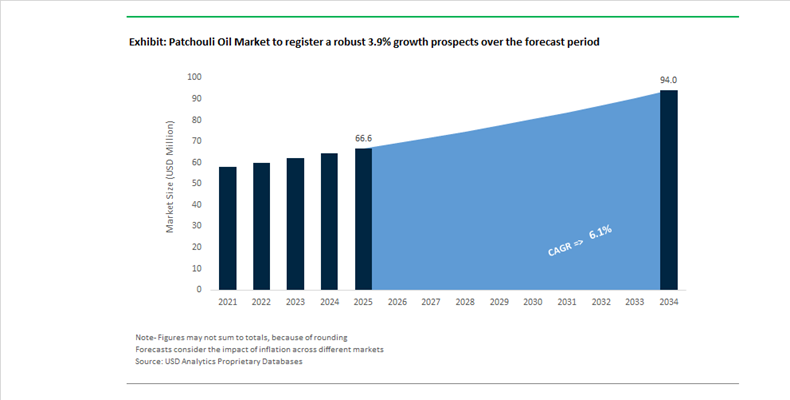

The Patchouli Oil Market is valued at $66.6 million in 2025 and is projected to reach $94 million by 2034, expanding at a CAGR of 3.9%. Patchouli oil remains a critical natural aromatic ingredient within the global fragrance, personal care, aromatherapy, and active beauty industries. Market momentum is being shaped by three structural drivers: premiumization of fine fragrances, biotechnology-enabled patchouli substitutes, and supply chain digitization in Indonesia, which accounts for the majority of global production. Demand growth is particularly strong in luxury perfumery, niche artisanal fragrances, and functional beauty formulations that leverage patchouli’s fixative properties and anti-inflammatory bioactivity.

Trade data in September 2024 showed a 69% year-over-year surge in Indonesian patchouli oil exports, reflecting strong forward ordering by European fragrance houses for 2025 launch cycles. Importers increasingly opted for air freight rather than sea logistics to secure just-in-time delivery despite elevated transport costs. Throughout 2024 and 2025, the Givaudan Foundation expanded renewable distillation programs in Sulawesi, introducing high-efficiency boilers and sustainable firewood systems to reduce deforestation linked to traditional distillation. In July 2024, Symrise AG received recognition for its regenerative agriculture blueprint, which stabilizes farmer incomes and reduces supply volatility through insurance and financial inclusion programs. These upstream initiatives are critical as natural patchouli remains price-sensitive and exposed to climatic variability.

Supply-side transformation accelerated in late 2024 and into 2025. Fairventures Worldwide and Good Forest Indonesia completed the first harvest of their Central Kalimantan agroforestry pilot in late 2024, scaling distribution of patchouli seedlings in January 2025 to integrate the crop into reforestation models. In August 2025, the Atsiri Research Center in Aceh reported local prices peaking at Rp 1.8 million per kilogram, up sharply from historical averages near Rp 300,000. The spike followed an ILO-supported digital marketplace integration that connected 17 producing districts directly to international buyers, improving distillation quality transparency and farmer bargaining power. Meanwhile, Van Aroma confirmed in its 2025 corporate update that it reached an annual production capacity of 850 metric tonnes, with increased focus on molecular distillation and standardized patchoulol isolates for pharmaceutical and fine fragrance applications.

Premium ingredient innovation intensified in 2025. In October 2025, Takasago International Corporation introduced “Patchouli Indonesia Molecular Distillation” at Beautyworld Middle East, refining the oil to eliminate harsh earthy facets and deliver a cleaner amber-woody signature tailored for luxury markets. In December 2025, dsm-firmenich unveiled its “Cloud Dancer” fragrance collection featuring Patchouli Heart SFE and Clearwood Prisma, a biotechnology-derived molecule replicating patchouli’s olfactory character with a reduced environmental footprint. These launches reflect a shift toward controlled extraction technologies and biotech-enabled aroma chemicals that stabilize olfactive profiles while lowering carbon intensity. In May 2025, IFF completed the divestment of its Pharma Solutions division to concentrate on scent innovation and bioactive derivatives, expanding research into patchouli-derived actives for skin-soothing and anti-inflammatory formulations.

Financial results released in February 2026 further underscored downstream demand resilience. Givaudan reported an 18.3% increase in Fine Fragrance sales for fiscal year 2025, supported by an integrated supply chain model that managed elevated natural raw material costs through coordinated pricing strategies with luxury brands. The Patchouli Oil Market is therefore characterized by sustained demand from high-end fragrance houses, rising biotechnology substitution, digital traceability integration in Indonesian supply chains, and ongoing investment in regenerative agricultural sourcing models that underpin long-term raw material security.

Structural Trends and High-Value Opportunities Shaping the Patchouli Oil Market

Strategic Shift Toward Sustainable and Certified Patchouli Supply Chains

The global patchouli oil market is undergoing a structural sourcing transformation as leading fragrance houses move away from opaque bulk procurement toward fully traceable, direct-to-origin supply models. This shift is driven by tightening deforestation-free requirements in Europe and North America, rising ESG scrutiny, and the need to stabilize supply in a market historically exposed to climate and yield volatility. Sustainable sourcing has effectively become a prerequisite for long-term supplier qualification rather than a brand differentiator.

A prominent example is Givaudan, which has established an integrated patchouli collection network in Sulawesi, Indonesia. As of December 2025, this network supports more than 1,000 smallholder farmers under a shared-value framework that combines full traceability with agronomic training. By improving harvesting and post-harvest handling through field schools, the initiative has delivered more consistent oil quality while reducing farmer exposure to price shocks.

Parallel progress is visible in regenerative agriculture. Programs such as Sourcing4Good have accelerated the transition away from patchouli crop migration, a practice historically linked to deforestation. By introducing green manure systems and soil cover crops, growers have reported measurable improvements in soil fertility and biodiversity across key Indonesian cultivation zones. Sustainability efforts are also extending into processing. In partnership with Swisscontact, energy-efficiency upgrades to traditional distillation units have reduced reliance on firewood. To date, roughly 320 distillation operators in Sulawesi have been trained in low-emission techniques, lowering the carbon intensity of patchouli oil at source and strengthening compliance with buyer sustainability audits.

Premiumization and Innovation in Niche and Gender-Neutral Perfumery

Patchouli oil is experiencing a pronounced premiumization cycle as consumer preferences shift toward authenticity, longevity, and gender-neutral fragrance profiles. Once associated primarily with mass-market or counterculture scents, patchouli has re-emerged as a cornerstone ingredient in fine perfumery, particularly within the quiet luxury and niche fragrance segments. This evolution is creating a tiered market structure where oil quality, aging profile, and origin command material price differentials.

Market segmentation data from late 2025 indicates that dark patchouli oil now accounts for approximately 46% of global demand. Its deep, earthy olfactory profile and strong fixation properties make it a preferred base note in premium compositions. Light patchouli oil represents about 38% of demand and is increasingly used in transparent, skin-close fragrances aimed at younger, sustainability-focused consumers. The remaining share is composed of specialty and aged grades.

Artisanal perfumery has emerged as a powerful demand catalyst. Aged patchouli oil, matured for two to five years, develops a smoother profile with reduced camphoraceous notes, similar to the aging effect in fine spirits. Luxury fragrance houses are increasingly highlighting aged patchouli on ingredient disclosures to justify ultra-premium positioning, often exceeding USD 250 per bottle. At the same time, regulatory and environmental pressure on synthetic musks has increased reliance on natural fixatives. Patchouli oil usage as a fixative rose by an estimated 19% as brands seek biodegradable alternatives that anchor volatile top notes in clean-label formulations.

Functional Ingredient Adoption in High-End Skincare and Cosmetics

A significant growth opportunity for the patchouli oil market lies in its repositioning as a functional botanical active rather than solely a fragrance component. Clinical and dermatological validation published during 2024–2025 has expanded its appeal within premium skincare, dermocosmetics, and pharmaceutical adjacencies, particularly among clean beauty brands seeking multifunctional plant-based ingredients.

Peer-reviewed studies have demonstrated patchouli oil’s anti-inflammatory and antioxidant activity, with evidence showing its ability to mitigate UV-induced photoaging and rebalance sebum production by up to 39%. These properties have supported its inclusion in approximately 31% of new prestige skincare launches, particularly in formulations targeting acne, sensitive skin, and scalp health. High-purity patchouli fractions are also being evaluated for therapeutic applications, including dermatitis management, due to their antifungal and antimicrobial characteristics.

The wellness sector further reinforces this opportunity. Post-pandemic emphasis on emotional wellbeing has integrated aromatherapy into premium spa and hospitality experiences. Around 37% of global wellness outlets now offer patchouli-based aromatherapy treatments focused on stress reduction and mood regulation. This has increased demand for CO2-extracted patchouli oil, which preserves a more complete phytochemical profile and delivers a truer therapeutic aroma compared with conventional steam-distilled grades.

Natural Insect Repellent and Premium Pet Care Applications

The growing consumer aversion to synthetic repellents and the rapid expansion of the pet care industry are opening new, high-margin niches for patchouli oil. Rising concerns over the neurotoxicity and environmental persistence of conventional insecticides have accelerated the shift toward plant-based alternatives, positioning patchouli oil as a viable active ingredient in DEET-free formulations.

Patchouli’s high patchoulol content has demonstrated efficacy as a natural deterrent against several mosquito and fly species, aligning with the estimated 54% of global consumers now actively seeking fully natural household products. This has led to increased formulation activity in personal insect repellents, outdoor lifestyle products, and home care sprays marketed on safety and sustainability credentials.

In parallel, the premium pet care segment is adopting aromatherapy-inspired solutions. Patchouli oil is increasingly incorporated into pet shampoos, deodorizing sprays, and calming treatments, valued for its mild antimicrobial action and soothing effect on anxious animals. Importantly, its plant-based origin reduces the risk of toxic ingestion compared with synthetic fragrance additives.

Supply dynamics are adapting to this diversification. Indonesia, which supplies more than 73% of global patchouli oil, is encouraging intercropping strategies that combine patchouli with other high-value botanicals to stabilize farmer incomes. Agricultural bodies, including GAPKI, noted in October 2025 that such diversification is strengthening supply resilience and ensuring consistent availability of patchouli oil for non-fragrance applications. Together, these developments position patchouli oil as a multifunctional botanical with expanding relevance across fragrance, wellness, personal care, and household markets.

Patchouli Oil Market Share and Segmentation Insights

Light Patchouli Oil Leads Global Demand in Modern Fragrance and Personal Care Formulations

Light patchouli oil accounted for 48.60% of the Patchouli Oil Market by type in 2025, reflecting its widespread adoption in fragrance formulations and cosmetic products. Derived from younger patchouli leaves or shorter distillation processes, light patchouli oil delivers a cleaner and more balanced fragrance profile with reduced earthy and camphoraceous notes. This scent profile makes it particularly suitable for perfumes, skincare products, and aromatherapy blends where a refined fragrance character is preferred. In 2025, premiumization of fractionated patchouli oil products is influencing the market, with producers isolating specific light fractions that deliver targeted olfactory characteristics sought by perfumers and cosmetic formulators in high-end fragrance development.

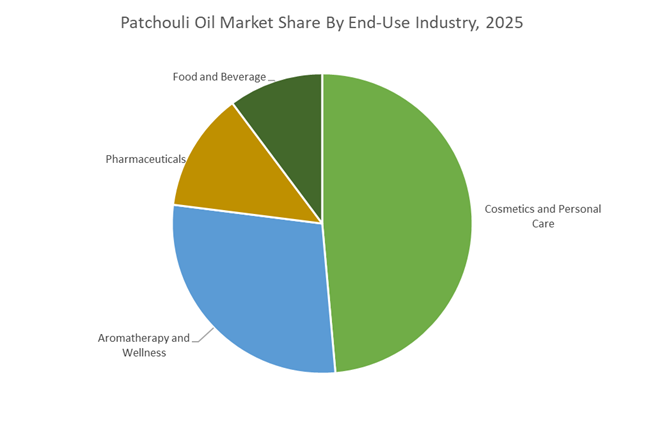

Cosmetics and Personal Care Sector Drives Patchouli Oil Demand in Natural Fragrance Formulations

The cosmetics and personal care sector represented 48.60% of the Patchouli Oil Market by end-use industry in 2025, reflecting strong demand for natural fragrance ingredients used in perfumes, skincare products, soaps, and hair care formulations. Patchouli oil is valued for its distinctive aroma and fixative properties that help stabilize fragrance compositions in cosmetic products. Growth in global personal care markets continues to support consistent demand for essential oils used in fragrance development. In 2025, the rise of natural fragrance preferences in clean beauty products is increasing the adoption of patchouli oil as brands seek plant derived scent ingredients that align with consumer expectations for natural, sustainable, and transparent cosmetic formulations.

Patchouli Oil Market Competitive Landscape

The Patchouli Oil Market is evolving toward blockchain-enabled traceability, molecular distillation, and direct farmer integration. Leading fragrance houses and Indonesian producers are focusing on supply chain transparency, odor consistency, and bio-based innovation to meet regulatory pressures and premium demand across fine fragrance, cosmetics, and wellness applications.

Givaudan scales origin-direct sourcing and sustainable patchouli innovation under 2030 strategy

Givaudan is strengthening its leadership in the patchouli oil market through its 2030 strategy focused on responsible sourcing and high-value natural innovation. With 69% of materials sourced responsibly, the company is expanding Origin-Direct programs to ensure traceability and improve income for Indonesian smallholders. Patchouli remains a critical base note in fine fragrances, supporting double-digit growth in this segment and contributing to CHF 7.47 billion in 2025 sales. Givaudan has reduced Scope 1 and 2 emissions by 50% since 2015 and is advancing FLAG targets for sustainable land use in patchouli-producing regions. Leadership transition in 2026 reinforces its long-term focus on transparency and sustainable growth. This integration of sourcing, sustainability, and fragrance innovation strengthens its global dominance.

dsm-firmenich integrates biotech patchouli alternatives with advanced extraction technologies

dsm-firmenich is redefining the patchouli oil market by combining biotechnology with advanced extraction methods to ensure supply stability and olfactory consistency. Its Patchouli Heart SFE, derived using supercritical fluid extraction, eliminates undesirable earthy notes, enhancing fragrance quality. The company is scaling Clearwood Prisma, a biotech-derived patchouli alternative that mitigates supply volatility caused by climate impacts. Through its Naturals Together program, nearly 55% of its patchouli output now utilizes advanced steam distillation for improved purity. The company is also targeting the wellness fragrance segment with data-driven formulations leveraging patchouli’s therapeutic benefits. This combination of biotech innovation, sustainability, and sensory optimization positions dsm-firmenich as a market disruptor.

IFF enhances premium patchouli extracts with agronomic innovation and digital fragrance production

International Flavors & Fragrances (IFF) is strengthening its position through premium natural extracts and digital transformation in fragrance formulation. Its LMR Naturals expansion in Grasse increases capacity for high-purity patchouli extracts, including next-generation variants like Patchouli Indonesia LMR. The company is deploying agronomic programs in Indonesia to improve yield efficiency and reduce carbon footprint through optimized cultivation practices. With $10.89 billion in 2025 sales, IFF continues to benefit from strong demand for oriental and woody fragrance profiles. Its smart dosing technology reduces waste by approximately 10%, enhancing cost efficiency for high-value naturals. This integration of innovation at source and digital precision strengthens IFF’s competitive edge.

Van Aroma expands Indonesian supply chain to stabilize global patchouli oil volumes

Van Aroma is a key supply chain player in the patchouli oil market, acting as a bridge between Indonesian farmers and global fragrance companies. Its expansion into Mamuju, West Sulawesi enhances direct access to high-yield cultivation zones, improving traceability and consistency. With an annual production capacity of approximately 850 metric tonnes, the company plays a critical role in stabilizing global supply. Strategic partnerships, including its alliance with Jandico Limited, strengthen distribution across Europe and the UK. Through the Nilampedia platform, developed with Symrise, Van Aroma supports farmer education in regenerative agriculture practices. This combination of scale, proximity, and farmer integration strengthens its global relevance.

Indesso advances fractionated patchouli oils with digital traceability and molecular distillation

PT. Indesso Aroma is a leading producer of high-value patchouli oil derivatives, leveraging vertical integration and advanced fractionation technologies. Its molecular distillation capabilities enable production of specialty grades such as Light Patchouli Oil, essential for cosmetics requiring low discoloration. The company offers customized fractions with 30% to 40% patchoulol content, catering to pharmaceutical and detergent applications. Through participation in the MyNilam digital ERP initiative, Indesso is enhancing supply chain transparency and financial inclusion for farmers. Its role in policy advocacy has elevated essential oils as a strategic industrial priority in Indonesia. This integration of technology, traceability, and specialization positions Indesso strongly in premium segments.

Indonesia – Structural Supply Dominance Under Sustainability and Compliance Pressure

Indonesia continues to anchor the global patchouli oil industry, supplying over 80% of worldwide volumes of Pogostemon cablin. However, late 2025 exposed structural fragilities in this dominance. Extreme weather events and landslides across Sulawesi and Aceh disrupted harvesting cycles, triggering temporary supply tightness and renewed price volatility in fine fragrance and personal care supply chains. These climate-linked disruptions have reinforced the strategic importance of resilience planning, stockpiling, and long-term sourcing agreements for international buyers that remain heavily dependent on Indonesian origin oil.

Regulatory and sustainability dynamics are simultaneously reshaping the Indonesian patchouli value chain. Under Government Regulation PP 42 of 2024, mandatory Halal certification for cosmetics and chemical products will be enforced by October 2026, extending compliance obligations deep into upstream distillation. This has accelerated facility audits, processing-aid certification, and traceability investments. On the sustainability front, Givaudan expanded its Patchoubest Sourcing4Good Advanced Level program in 2025, addressing soil depletion and allelopathy that previously drove crop migration into forest land. Parallel investments by Van Aroma in iron-free fractionation enabled the production of Sulawesi grades exceeding 30% patchoulol content, aligning Indonesian output with the purity thresholds demanded by European fine perfumery. Despite agronomic risks, export shipments still rose 22% year-on-year through September 2024 as global brands rebuilt inventories depleted during prior supply shocks.

India – Strategic Import Substitution Through Agronomic Scale-Up

India is rapidly repositioning itself from a net importer toward a structurally relevant secondary producer of patchouli oil. Under the Aroma Mission 2025, the CSIR-North East Institute of Science and Technology inaugurated its Incubation and Innovation Complex in January 2025, accelerating the rollout of patchouli cultivation across more than 5,000 hectares in the North East. This expansion has already benefited over 10,000 farmers, creating a new income stream in regions traditionally excluded from high-value aromatic crops.

Infrastructure and enterprise development are reinforcing this agronomic push. A state-of-the-art essential oil production unit commissioned in Assam in 2025 introduced advanced steam distillation to reduce India’s estimated 220 metric ton annual dependency on Indonesian imports. At the North East Aroma Conclave 2025, government-backed agreements were awarded to 25 startups and MSMEs, granting access to 27 advanced distillation and quality-control technologies. In parallel, import monitoring mechanisms and cultivation subsidies are being used to stabilize domestic pricing and advance the Atmanirbhar agenda, positioning India as a medium-term supply stabilizer for regional fragrance and flavor manufacturers.

China – Demand-Led Expansion Driven by Wellness and Clean-Label Preferences

China’s role in the patchouli oil industry is demand-centric rather than supply-dominant, shaped by the rapid expansion of its aromatherapy, wellness, and cosmetics sectors. In late 2025, greenhouse-based cultivation of patchouli accelerated, allowing controlled, year-round harvesting independent of tropical weather volatility. This production model supports consistency and traceability, two attributes increasingly required by domestic brands serving premium urban consumers.

Consumer behavior is the primary catalyst. Market assessments from late 2025 indicate that more than 32% of patchouli oil sales in China are now organic-certified, reflecting strong Gen-Z and millennial preferences for clean-label and sustainable fragrances. Industrial e-commerce platforms and direct-to-consumer channels have amplified demand further, particularly for patchouli-infused wellness accessories and household products. Adoption of such products by global brands rose sharply in 2025, reinforcing China’s position as a critical demand-growth engine for certified and differentiated patchouli oil grades.

Switzerland – Biotechnological Substitution and Olfactive Innovation

Switzerland functions as the innovation nucleus of the global patchouli ecosystem, shaping demand through biotechnology rather than agricultural output. In 2025, DSM-Firmenich introduced Clearwood® Prisma under its Sharing Innovation Collection. This biotechnology-derived ingredient delivers a dark, woody, patchouli-like profile while being ISO 9235 compliant and fully carbon-renewable. Such solutions are increasingly used to manage supply volatility, reduce land-use pressure, and provide consistent olfactive performance.

Strategic direction across the Swiss fragrance sector reinforces this trend. Givaudan announced its next strategy cycle in late 2025, effective March 2026, prioritizing high-value adjacencies in biotech beauty actives and wellbeing formulations. Within this framework, natural patchouli oil remains a core mood-harmonizing ingredient, while biotech analogs are positioned as complementary tools for formulation flexibility rather than outright replacements.

Madagascar – Ethical Sourcing and Luxury Differentiation

Madagascar has emerged as a high-integrity, low-volume origin tailored to luxury fragrance houses. In 2025, Symrise expanded its Madagascar portfolio to 36 products, designating patchouli as a flagship oil. The company employs both CO₂ extraction and traditional distillation to produce Grand Cru grades with distinctive olfactive signatures aimed at premium applications.

Traceability and compliance underpin Madagascar’s strategic value. All Symrise-sourced patchouli from the region is certified Organic, COSMOS, and Fair For Life, ensuring alignment with Nagoya Protocol benefit-sharing requirements. This positioning makes Madagascar-origin patchouli particularly attractive for luxury brands facing increasing scrutiny around ethical sourcing, biodiversity protection, and transparent supplier relationships.

Comparative Snapshot – Patchouli Oil Industry by Country

Patchouli Oil Market County Level Snapshot

|

Country

|

Strategic Role

|

Key Driver

|

Structural Impact

|

|

Indonesia

|

Global supply backbone

|

Climate resilience and Halal compliance

|

Supply volatility with rising certification costs

|

|

India

|

Import substitution challenger

|

Aroma Mission scale-up

|

Gradual reduction in import dependency

|

|

China

|

Demand-growth engine

|

Clean-label and wellness consumption

|

Premium demand for organic-certified oils

|

|

Switzerland

|

Innovation hub

|

Biotechnology and olfactive design

|

Supply-risk mitigation via biotech adjacencies

|

|

Madagascar

|

Ethical luxury origin

|

Certified traceability and CO₂ extraction

|

High-value differentiation for niche brands

|

Patchouli Oil Market Report Scope

Patchouli Oil Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$66.6 Million

|

|

Market Size (2034)

|

$94 Million

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Type (Dark Patchouli Oil, Light Patchouli Oil, Synthetic Patchouli Oil), By Nature (Conventional Patchouli Oil, Organic Patchouli Oil), By Extraction Process (Steam Distillation, Hydro Distillation, CO₂ Extraction), By Function (Fragrance and Fixative, Therapeutic, Deodorizing and Insecticidal), By End-Use Industry (Cosmetics and Personal Care, Aromatherapy and Wellness, Food and Beverage, Pharmaceuticals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Givaudan, DSM-Firmenich, Symrise, International Flavors and Fragrances, Takasago International Corporation, Mane, Robertet, Van Aroma, Indesso, Aarti Industries, Ultra International, Young Living Essential Oils, dōTERRA International, Falcon Essential Oils, Shiv Sales Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Patchouli Oil Market Segmentation

By Type

- Dark Patchouli Oil

- Light Patchouli Oil

- Synthetic Patchouli Oil

By Nature

- Conventional Patchouli Oil

- Organic Patchouli Oil

By Extraction Process

- Steam Distillation

- Hydro Distillation

- CO₂ Extraction

By Function

- Fragrance and Fixative

- Therapeutic

- Deodorizing and Insecticidal

By End-Use Industry

- Cosmetics and Personal Care

- Aromatherapy and Wellness

- Food and Beverage

- Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Patchouli Oil Industry

- Givaudan

- DSM-Firmenich

- Symrise

- International Flavors and Fragrances

- Takasago International Corporation

- Mane

- Robertet

- Van Aroma

- Indesso

- Aarti Industries

- Ultra International

- Young Living Essential Oils

- dōTERRA International

- Falcon Essential Oils

- Shiv Sales Corporation

*- List not Exhaustive