Plastic Restaurant Furniture Market Driving Hospitality Design with Durability, Affordability, and Sustainability

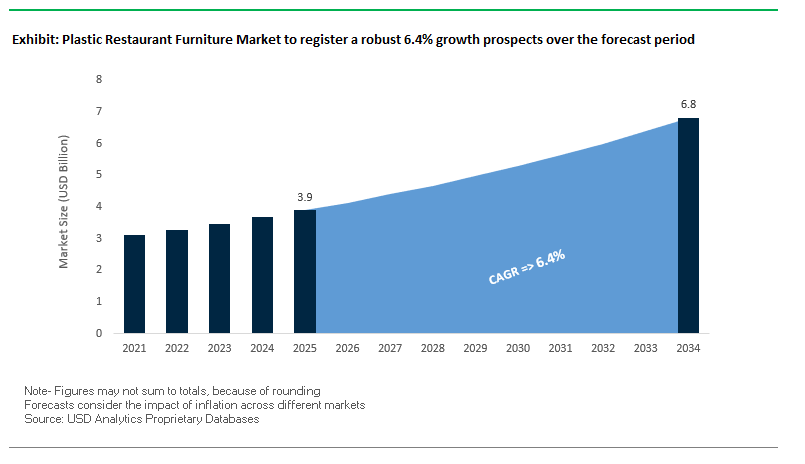

The global plastic restaurant furniture market is anticipated to expand from $3.9 billion in 2025 to $6.8 billion in 2034 at a CAGR of 6.4%. The market has emerged as a leading category in the commercial furniture market due to cost-effectiveness, design flexibility, and low maintenance, making it an ideal choice for the evolving needs of restaurants, cafes, and hospitality businesses around the world. As the need for furniture that is both functional and hygienic but attractive keeps growing, plastic-based furniture is becoming a favorite for indoor dining rooms and outdoor sitting areas.

Plastic restaurant furniture presents unique competitive benefits light weight construction, cleanability, and durability against moisture, stains, and UV degradation, making it best suited for high-traffic hospitality settings. Advances in polymer science and injection molding have greatly expanded design potential, allowing brands to provide high-end finishes, striking color choices, and custom branding. Furthermore, green considerations are also affecting purchasing decisions, with recycled plastic furniture becoming increasingly popular among environmentally conscious hospitality operators.

Key Insights for Industry Professionals:

- Durability & Weather Resistance: UV-stable, impact-resistant designs allow furniture to perform in both indoor and outdoor spaces.

- Cost & Maintenance Efficiency: Low production and upkeep costs help restaurants allocate budgets to core operations.

- Hygiene Priority: Non-porous surfaces enable fast, effective sanitization critical in post-pandemic operations.

- Design Flexibility: Advanced molding technology supports custom styles and branding.

- Sustainability Shift: Increasing use of recycled plastics supports ESG goals in hospitality procurement.

Recent Developments and Strategic Moves in Plastic Restaurant Furniture Industry

Recent changes in plastic restaurant furniture market is characterized by a collective push toward sustainability, functional innovation, and expanding channels of distribution for plastic restaurant furniture. In August 2024, Tesco teamed up with Veolia to recycle consumer plastics such as bread bags and yogurt lids into functional products such as benches and tables, pointing out the potential of circular economy models in furniture making. A short while after the same period, Bali-based Potato Head Group launched its "N*thing Is Possible" exhibition, with designer furniture composed wholly of recycled polystyrene, demonstrating that recycled material can meet both durability and aesthetic specifications.

In July 2025, UN Tourism indicated global visitor arrivals in 2024 had hit 99% of pre-COVID levels, a growth that directly drove demand for low-maintenance, long-life seating in hospitality use. Makers obliged with stackable and portable solutions for flexible dining spaces and event-driven seating requirements. Iconic brand Vitra, in May 2025, further heightened the industry's sustainability profile with the production of the Eames Plastic Chair produced from post-consumer recycled polypropylene that minimizes carbon emissions without sacrificing design integrity.

Indian companies have been very aggressive in the market. Petals Furniture introduced the "Leo" Virgin Plastic Chair in September 2024, supported by a three-year warranty and for both residential and commercial buyers. Supreme Industries broadened its product line in November 2024, leveraging state-of-the-art R&D to improve eco-friendliness. In August 2025, several Indian companies used aggressive wholesale pricing and logistics support, specifically targeting small hospitality operators and quick-service chains looking to furnish multiple outlets in an efficient manner.

Trends and Opportunities Reshaping the Plastic Restaurant Furniture Market

Recycled Ocean-Plastic Furniture Becomes a QSR Sustainability Standard

Market-share-leading fast-food QSR brands are replacing virgin resin with ocean-recycled plastic (e.g., discarded fishing nets and hard PP) to meet circular-economy commitments and enhance brand ESG credentials. The closed-loop sourcing model rewards good net recovery, supports UN SDG 14 ("Life Below Water"), and offers a stable feedstock for marine-plastic furniture at scale. Above all, frontier manufacturing compounding delivers virgin-polymer-equivalent durability and colorfastness, enabling sleek, long-lifespan chairs and tables (e.g., "Ocean Collection" designs) resistant to UV, spill, and normal wear. Beyond carbon and waste reductions, in-store visibility storytelling about ocean-plastic seating boosts customer affinity among eco-conscious diners turning front-of-house furniture into a high-impact sustainability touchpoint.

Modular, Stackable Designs Power Ghost-Kitchen Efficiency

As ghost and delivery-only concepts grow, operators require high-density designs, rapid reconfigurability, and lowest TCO. Stackable, modular plastic furniture light-weight break-room sets, nesting stools, and adjustable storage cubes maximizes available space, streamlines daily resets, and saves capex over metal/wood solutions. Easy-to-clean, non-porous surfaces streamline sanitation cycles and solve back-of-house SOPs, and modular, swap-out components (à la modular systems such as "stacked" storage) allow operators to adapt to menu or workflow changes without costly refits. The result is a space-maximized, flexible environment optimized to delivery throughput and multi-brand kitchen pods.

Antimicrobial Additives Meet Post-Pandemic Hygiene Expectations

Restaurants can differentiate with antimicrobial plastic restaurant furniture that bakes protection into the polymer matrix. Silver-ion, copper-ion, or organic biocidal additives prevent bacteria, fungi, and algae on high-touch surfaces (table edges, chair backs), minimizing cross-contamination risk between turns and maximizing the cleanliness between wipe-downs. These built-in additives compare favorably to dissipating topical sprays in offering long-term hygiene, backing "hospitality-grade" safety claims, and enhancing guest confidence. Clear labeling (e.g., "antimicrobial surfaces") and third-party test data bolster procurement arguments for chains standardizing on health-first fixtures.

Urbanization in Emerging Markets Accelerates Volume Growth

Rapid QSR rollouts in Southeast Asia and Africa are fueling demand for low-cost, durable, easy-to-ship plastic furniture. Light-weight chairs and fold-flat/stackable tables save logistics cost, and UV- and moisture-resistant grades endure diverse climate and outdoor exposure. Localized molding and regional distribution centers reduce lead times and import duties, supporting aggressive franchise timetables. As operators enlarge patios and micro-footprints, space-saving, modular SKUs (benches, nesting stools) capture incremental share where municipalities encourage outdoor dining and street-food precincts.

Plastic Restaurant Furniture Market Share Insights: Product Leadership Shifts with Outdoor Expansion and Modular Design

Product Mix: Chairs Lead on Replacement Cycles; Tables Gain with Modular Formats

Chairs, with 40% market share, are the biggest category in the plastic restaurant furniture market due to high turn-rate replacements, wide color/finish selection, and stackability for storage. Tables, at 35%, remain standard on wipe-clean, scratch-resistant surfaces and clip-on bases, with expansion directed toward modular/stackable designs that enable fast patio flips and flexible seating plans. Stools are increasing in casual and bar-service areas for footprint efficiency, and benches/booths are a niche but upscale category where operators desire maximum covers per square meter and durable, easy-sanitize surfaces. Throughout SKUs, recycled content (ocean-plastic combinations, PCR PP/HDPE) and antimicrobial offerings are becoming base RFP requirements for multi-unit chains.

.png)

Application Mix: Outdoor Seating Dominates; Indoor Upgrades Focus on Ergonomics and Aesthetics

Outdoor seating (45% share) leads the way as restaurants invest in weather-resistant, recycled-plastic patio seating to drive extended service hours, increased covers, and signal sustainability. UV-stable pigments, drainage-friendly shapes, and hose-down cleanability make plastic the material of choice for terraces and sidewalks. Indoor seating focuses on ergonomic silhouettes, matte finishes, and acoustic friendliness to drive ambiance while ensuring cleanability often pairing antimicrobial additives with PCR content for ESG reporting. Bars & lounges (15%) feature reinforced stools and small tables that meet durability, slip resistance, and modern styling needs, enabling high throughput in small footprints. In all, operators are standardizing on configurable, stackable SKUs that minimize storage, speed resets, and enable brand-consistent design indoors and outdoors.

Plastic Restaurant Furniture Market Competitive Landscape – Leading Manufacturers and Strategic Profiles

The plastic restaurant furniture market is shaped by manufacturers who combine large-scale production capabilities with design innovation and sustainability-focused practices. Key players included are Nilkamal Ltd., Supreme Industries Ltd., Cello Industries Ltd., Grosfillex S.A.S, Keter Group, Siesta Exclusive, Nardi S.p.A., Resol S.A., Fermob, Chairigami, Plastecnic S.p.A., Emu Group S.p.A., Vondom S.L., Ohio Outdoor Furniture, Shelby Williams, Others.

Nilkamal Ltd. – Global Leader in Molded Furniture

Nilkamal is a world leader in molded furniture production, supported by a distribution network of over 20,000 dealers in India. Nilkamal distributes a wide range of products from plastic chairs, tables, and storage systems to be used mainly in restaurants and cafes. The company's strength is in providing high-quality, low-price solutions with the latest styling. Nilkamal is concentrating on product diversification and omnichannel sales practices in order to combat bulk orders of hospitality and retail orders.

The Supreme Industries Limited – Scale and R&D-Driven Innovation

Being India's largest plastic processor, Supreme Industries enjoys leadership in terms of manufacturing size and a wide-ranging product portfolio. Its furniture segment provides long-lasting, fashionable chairs, tables, and stools for commercial purposes. The company's emphasis on world-class technology and aggressive R&D fuels innovation that addresses restaurants' changing needs like weather-resistant and light-weight designs.

Cello Industries Ltd. – Blending Style and Functionality

Cello has made its name on producing plastic furniture combining modern design with ergonomic functionality. The business caters to hospitality operators who seek stylish yet practical solutions. With its product range from stackable chairs to light tables, Cello is placing its portfolio on par with the fast operational needs of restaurants.

Keter Group B.V. – Sustainability Pioneer in Plastic Furniture

Keter is a global outdoor and storage furniture brand with a strong hospitality market position through patio and garden seating. Its commitment to recycling and circular economy values attracts environmentally conscious consumers. Keter furniture is designed to be simple to install and low in maintenance, enabling restaurant owners to optimize operating efficiency more conveniently.

AVRO India Limited – High-Volume, Cost-Competitive Production

AVRO India applies volume manufacturing and cost reduction to provide competitively priced molded furniture. AVRO addresses small- and medium-sized hospitality firms with low-cost, long-life tables and chairs. As a public company, AVRO is able to access capital for growth, enabling it to venture into new product categories and geographic markets.

United States: Smart Furniture Innovation and Sustainable Manufacturing Practices

The United States plastic restaurant furniture market is evolving rapidly through technological advancements, smart furniture integration, and sustainability-driven design. Manufacturers are embracing AI-powered design optimization, enabling them to create ergonomically engineered chairs and tables that balance comfort, durability, and visual appeal for both indoor and outdoor dining settings. The adoption of IoT-enabled seating solutions is emerging as a niche yet impactful trend, allowing restaurants to gather real-time data on seating patterns, occupancy, and dwell time to optimize floor layouts and improve operational efficiency. This integration of technology into commercial furniture is giving U.S. manufacturers a competitive advantage in delivering data-driven hospitality solutions.

Sustainability is an equally powerful driver, with many companies shifting toward post-consumer recycled plastics such as HDPE from milk jugs or PET from detergent bottles. Brands like Ovation Outdoor are setting benchmarks by producing upscale, weather-resistant furniture entirely from recycled content. Additionally, hygiene innovations are shaping purchasing decisions, with antimicrobial-infused surfaces becoming a sought-after feature for high-traffic restaurants aiming to reassure health-conscious customers. This combination of functional innovation, eco-conscious materials, and hygiene enhancements positions the U.S. market as a leader in shaping the next generation of plastic restaurant furniture globally.

Germany: Circular Economy Compliance and Advanced Material Engineering

Germany’s plastic restaurant furniture market is defined by strict sustainability regulations and material science innovation. The EU’s Ecodesign for Sustainable Products Regulation (ESPR), enforced from July 2024, is a major catalyst, requiring manufacturers to incorporate recyclability, durability, and repairability into every product. This regulatory framework is pushing German companies to develop designs for disassembly, enabling restaurants to replace or recycle components with minimal waste. In material innovation, German manufacturers are leading with fiber-reinforced polypropylene, bio-based PET, and UV-stabilized compounds, extending the life cycle of outdoor furniture exposed to sunlight and heavy usage.

The German market is characterized by a discerning customer base that values engineering precision, aesthetic minimalism, and long-term durability. This has resulted in products that blend traditional European craftsmanship with cutting-edge performance features. Additionally, the shift toward closed-loop manufacturing systems is helping brands reduce their environmental footprint while enhancing their sustainability credentials. These practices, supported by Germany’s strong export capacity, are solidifying the country’s position as a premium supplier of eco-certified, high-performance plastic restaurant furniture within Europe and beyond.

China: High-Volume Production and Customization-Driven Export Growth

China remains the world’s largest producer and exporter of plastic restaurant furniture, supported by an extensive supply chain capable of delivering both mass-market and custom-designed solutions. Advanced techniques such as gas-assist injection molding are enabling Chinese manufacturers to create lightweight yet structurally strong products with intricate detailing, appealing to restaurants seeking a balance of affordability and visual appeal. This manufacturing agility allows China to cater to global orders, from standardized bulk shipments for fast-food chains to customized branding and color schemes for upscale dining venues.

The market’s strength also lies in its global e-commerce integration, with platforms like Alibaba and Made-in-China.com facilitating direct-to-restaurant procurement worldwide. Chinese manufacturers are also expanding into eco-conscious production, incorporating recycled resin blends and low-VOC finishing processes to appeal to environmentally aware buyers. With competitive pricing, design flexibility, and rapid turnaround times, China continues to dominate as a global supplier of plastic restaurant furniture while steadily moving upmarket through enhanced design and material innovations.

India: Design-Centric Growth and Sustainable Manufacturing Shift

India’s plastic restaurant furniture market is transitioning from basic utility products to design-oriented, ergonomically engineered solutions. Local manufacturers are investing in improved lumbar support designs, flexible frame constructions, and stackable configurations to meet the needs of modern cafes, quick-service restaurants, and high-volume banquet operations. This design upgrade is coupled with the use of advanced molding technologies that enable intricate patterns, structural reinforcement, and smooth finishes previously achievable only with premium imports.

Sustainability is gaining momentum, with Indian producers increasingly integrating post-industrial recycled plastics and biodegradable additives into their manufacturing processes. This aligns with the country’s broader eco-conscious movement and growing consumer preference for environmentally responsible dining environments. As the restaurant and café culture expands across urban and tier-2 cities, demand for stylish, durable, and sustainable plastic furniture is expected to grow steadily, making India an emerging force in the global market.

Japan: Regulatory Sustainability Push and Space-Saving Design Solutions

Japan’s plastic restaurant furniture market is being influenced by stringent plastic waste management policies under the Plastic Resource Circulation Promotion Law (2025), which, although focused on single-use plastics, has prompted manufacturers across the sector to adopt more eco-friendly production materials and recycling programs. This shift is fostering the development of recycled polymer-based restaurant furniture that meets Japan’s high durability and safety standards. The market’s technological precision ensures that products are engineered to withstand heavy daily use without compromising comfort or aesthetics.

Urban density has also driven demand for space-efficient, modular designs, including stackable chairs, foldable tables, and lightweight multi-functional seating options. These features cater to small urban cafés and restaurants where floor space optimization is essential. Combined with Japan’s reputation for meticulous craftsmanship and innovative engineering, the country’s market is well-positioned to serve both domestic hospitality venues and international buyers seeking high-quality, compact plastic restaurant furniture solutions.

Plastic Restaurant Furniture Market Report Scope

Plastic Restaurant Furniture Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$6.8 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Product Type (Chairs, Tables, Stools, Benches, Booths), By Material (Polypropylene (PP), Polyethylene (PE), Polycarbonate (PC), Recycled Plastic), By Application (Indoor Seating, Outdoor Seating, Bars and Lounges), By End-User (Full-Service Restaurants, Quick-Service Restaurants, Cafes & Bistros, Hotels & Resorts), By Distribution Channel (Wholesalers & Distributors, Direct-to-Consumer, E-commerce Platforms)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nilkamal Ltd., Supreme Industries Ltd., Cello Industries Ltd., Grosfillex S.A.S, Keter Group, Siesta Exclusive, Nardi S.p.A., Resol S.A., Fermob, Chairigami, Plastecnic S.p.A., Emu Group S.p.A., Vondom S.L., Ohio Outdoor Furniture, Shelby Williams, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Restaurant Furniture Market Segmentation

By Product

- Chairs

- Tables

- Stools

- Benches

- Booths

By Material

- Polypropylene (PP)

- Polyethylene (PE)

- Polycarbonate (PC)

- Recycled Plastic

By Application

- Indoor Seating

- Outdoor Seating

- Bars and Lounges

By End-User

- Full-Service Restaurants

- Quick-Service Restaurants

- Cafes & Bistros

- Hotels & Resorts

By Distribution Channel

- Wholesalers & Distributors

- Direct-to-Consumer

- E-commerce Platforms

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Restaurant Furniture Market

- Nilkamal Ltd.

- Supreme Industries Ltd.

- Cello Industries Ltd.

- Grosfillex S.A.S

- Keter Group

- Siesta Exclusive

- Nardi S.p.A.

- Resol S.A.

- Fermob

- Chairigami

- Plastecnic S.p.A.

- Emu Group S.p.A.

- Vondom S.L.

- Ohio Outdoor Furniture

- ShelBy Williams

* List not Exhaustive

Research Coverage

This report investigates the global Plastic Restaurant Furniture Market in depth, delivering a comprehensive evaluation of industry breakthroughs, strategic developments, and emerging opportunities across the hospitality sector. Compiled by USDAnalytics, the analysis reviews competitive positioning, innovation pipelines, and sustainability trends that are reshaping procurement strategies in restaurants, cafés, and outdoor dining venues. It highlights technological advancements in polymer engineering, evolving consumer preferences, and regulatory frameworks that influence material choices and design formats. By integrating industry case studies and real-world applications, this report is an essential resource for decision-makers seeking to optimize investments, reduce lifecycle costs, and align with ESG commitments while maintaining operational flexibility and aesthetic appeal. Scope includes-

- Segmentation:

- By Product: Chairs, Tables, Stools, Benches, Booths

- By Material: Polypropylene (PP), Polyethylene (PE), Polycarbonate (PC), Recycled Plastic

- By Application: Indoor Seating, Outdoor Seating, Bars & Lounges

- By End User: Full-Service Restaurants, Quick-Service Restaurants, Cafés & Bistros, Hotels & Resorts

- By Distribution Channel: Wholesalers & Distributors, Direct-to-Consumer, E-commerce Platforms

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic & Forecast Range: Historic data from 2021–2024 and forecasts from 2025–2034.

- Companies: Profiles and strategic analysis of 15+ leading players.

Methodology

The study follows a hybrid research approach combining primary and secondary methodologies to ensure accuracy and actionable insights. Primary research involved interviews with senior executives, procurement managers, and R&D heads from leading plastic furniture manufacturers and hospitality operators. Secondary research encompassed the review of company reports, trade publications, patents, and regulatory databases to validate market size, technology adoption rates, and competitive strategies. Data triangulation was applied to reconcile information from multiple sources, ensuring that forecasts and strategic recommendations reflect both current market realities and anticipated developments. Analytical models assessed supply chain dynamics, pricing structures, and innovation adoption curves to produce a forward-looking outlook for the 2025–2034 period.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.