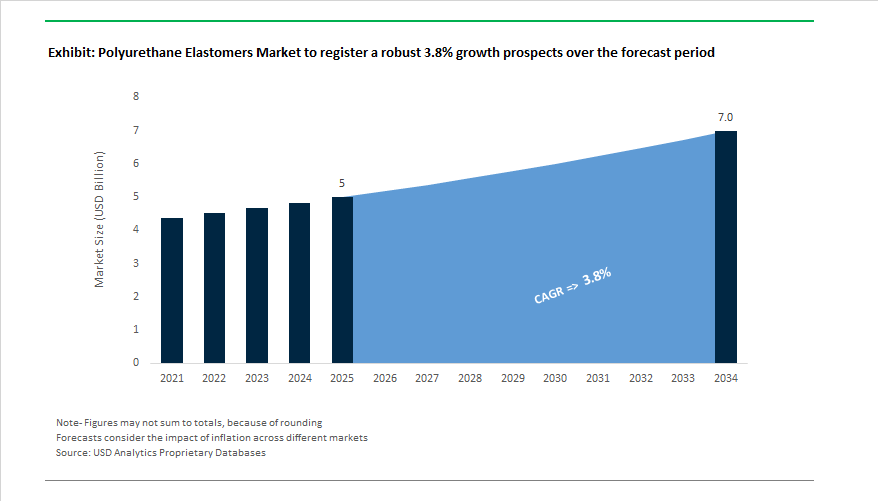

The Global Polyurethane Elastomers Market is projected to expand from USD 5.0 billion in 2025 to USD 7 billion by 2034, at a CAGR of 3.8%, reflecting a market shaped less by volume acceleration and more by where polyurethane elastomers remain structurally irreplaceable. Growth is anchored in applications where cyclic loading, abrasion, oil exposure, and dimensional recovery must coexist—conditions under which conventional rubber compounds and engineering plastics reach their performance limits.

Polyurethane elastomers continue to occupy a critical mechanical niche between elastomeric flexibility and thermoplastic strength. In automotive and industrial systems, they are increasingly specified not for cost efficiency, but for fatigue life extension, noise attenuation, and energy loss control in components subjected to millions of load cycles. Bushings, suspension isolators, seals, rollers, and wheels are being redesigned around polyurethane’s ability to maintain modulus and tear resistance under sustained dynamic stress—particularly relevant as EV architectures introduce higher torque, different vibration signatures, and heavier battery loads.

Electrification and automation are quietly recalibrating material specifications. In EV platforms, polyurethane elastomers are gaining importance in NVH management, cable protection, and drivetrain isolation, where traditional rubber compounds struggle with thermal aging and chemical exposure. At the same time, industrial automation is increasing demand for high-rebound, wear-resistant elastomers in conveyor systems, robotic rollers, and precision handling equipment, where uptime and dimensional consistency directly affect throughput.

A notable structural shift is occurring within product chemistry. Thermoplastic polyurethane (TPU) is emerging as the most strategically flexible segment, not simply due to recyclability, but because it aligns with multi-process manufacturing ecosystems. TPU’s compatibility with injection molding, extrusion, and additive manufacturing is enabling faster iteration cycles in footwear, electronics housings, medical components, and customized industrial parts. In performance footwear and consumer electronics, TPU is increasingly selected for its ability to deliver thin-wall flexibility without creep, supporting lightweight design without sacrificing durability.

Sustainability considerations are influencing feedstock and process choices, but largely within performance constraints. Rather than wholesale material substitution, leading producers are advancing mass-balanced and chemically recycled TPU systems, integrating post-consumer and bio-based inputs while maintaining mechanical specifications demanded by automotive and industrial customers. Initiatives by major manufacturers—including capacity expansions and recycling investments across China and Southeast Asia—reflect a strategy focused on supply security for MDI-based systems, regional proximity to OEMs, and incremental decarbonization without compromising elastomer performance.

In October 2025, BASF SE launched its Elastollan® 1400 TPU series, an ether-based thermoplastic polyurethane engineered for enhanced hydrolysis resistance and microbial protection. Designed for rail pads, cable sheathings, and footwear soles, this launch underscores BASF’s continued push toward durable, high-performance TPU systems with superior long-term mechanical integrity. The same month, BASF announced new capacity additions in Shanghai and Chongqing, focusing on Modified MDI (MMDI) production to strengthen its footprint in Asia’s construction and elastomers sectors.

Also in October 2025, Huntsman Corporation expanded its TPU distribution network through collaboration with WOBATEK GmbH, enhancing accessibility of its AVALON®, IROGRAN®, and IROSTIC® product lines across Austria, Poland, and Southern Germany. This strategic move bolsters Huntsman’s European supply chain resilience and ensures greater market penetration for its high-durability TPU elastomers in industrial and footwear applications.

Sustainability-driven innovation dominated 2025, as BASF introduced its Elastopan® SpringPURe portfolio at SIMAC in September 2025, showcasing advanced recycling methods through ChemCycling® and depolymerization technologies. These processes enable the transformation of post-industrial and post-consumer waste into new polyurethane soles, marking a major milestone in circular footwear production.

Regional expansions also accelerated. Lubrizol strengthened its Southeast Asia presence (July 2025) by opening a new Jakarta office and an Innovation Center in Singapore, focusing on co-innovation in mobility and infrastructure. The company’s earlier ESTANE® TPU Empowerment Ecosystem (April 2024) campaign reinforced its market positioning as a quality benchmark provider for Paint Protection Film (PPF) manufacturers in China.

Meanwhile, Covestro AG and Dow Inc. continued to invest heavily in Asia. Covestro’s Shanghai plant (August 2023) boosted regional elastomer system production capacity, ensuring a faster response to Asia-Pacific customer needs. Dow focused on lightweight EV composites and NVH solutions, reinforcing its reputation for integrated polyurethane systems in automotive, oil & gas, and industrial machinery.

In a notable divestiture, SKC sold SK Pucore in October 2023 to Glenwood Private Equity, signaling industry consolidation and portfolio optimization among Asian chemical producers. The move reflects a growing industry trend of focusing on core polyurethane competencies and performance materials.

The polyurethane elastomers industry is dominated by global chemical leaders with deep integration across the polyols, isocyanates, and TPU manufacturing value chain. The competition is primarily driven by product innovation, circular economy alignment, and strategic geographic expansion into Asia-Pacific and emerging markets.

Dow leads with its VORALAST™ Polyurethane Elastomer Systems, widely used across coatings, adhesives, mining, and oil & gas applications. As an integrated producer of polyols and isocyanates (MDI/TDI), Dow offers unmatched supply chain stability and cost advantages. The company’s recent innovations target mobility applications, focusing on Noise, Vibration, and Harshness (NVH) control components for EVs. Additionally, Dow emphasizes sustainability in its polyurethane systems, developing solutions for lightweight structures and energy-efficient insulation, aligning with net-zero goals.

Covestro maintains a strong market position with its Desmopan® TPU and Bayflex® PU product families, catering to footwear, automotive, and textile industries. Its expertise extends to anti-microbial, high-comfort materials, and mass-balanced TPU grades (Desmopan® CQ MBC) that reduce carbon footprints by up to 30%. The company continues to drive circular economy initiatives by utilizing bio-based polyols and developing recyclable TPU compounds. Covestro’s ongoing expansion in Shanghai further strengthens its influence in Asia’s high-growth polyurethane sector.

BASF dominates the polyurethane elastomers industry with its Cellasto® microcellular PU elastomers. Its Elastollan® 1400 series, introduced in October 2025, provides superior hydrolysis resistance and dynamic load-bearing properties for industrial and transportation uses. BASF is also pioneering circularity through its ChemCycling® and SpringPURe technologies, enabling the recovery and reuse of post-consumer waste into new PU soles. With new MMDI production capacity in China, BASF ensures steady regional supply for the growing automotive and construction markets.

Huntsman continues to expand its polyurethane leadership through AVALON®, IROGRAN®, and IROSTIC® elastomer product lines. Known for exceptional abrasion resistance and versatility, these TPUs serve demanding industrial and mining sectors. In October 2025, Huntsman expanded its distribution with WOBATEK GmbH, strengthening its presence across Central and Eastern Europe. With a global MDI supply network reaching 90+ countries, Huntsman is increasingly focused on automation, mobility, and sustainable polyurethane composites.

Lubrizol, a Berkshire Hathaway subsidiary, leads in thermoplastic polyurethane innovation through its ESTANE® TPU brand. The company’s Empowerment Ecosystem, launched in 2024, promotes 100% authentic ESTANE® TPU usage in Paint Protection Film (PPF) manufacturing—addressing quality and sustainability concerns in China’s growing automotive sector. With a new Jakarta office and Singapore Innovation Center (2025), Lubrizol is expanding its Southeast Asian footprint. Its TPUs offer exceptional chemical resistance, flexibility, and durability, serving medical, mobility, and infrastructure markets.

Country Analysis: Regional Developments and Strategic Advancements in the Global Polyurethane Elastomers Industry

China: Accelerating Renewable Energy and Automotive Growth Through Specialty Polyurethane Elastomers

China remains the global leader in polyurethane elastomer production and innovation, driven by aggressive industrial expansion, renewable energy investments, and a fast-growing automotive ecosystem. In August 2023, Covestro AG inaugurated a new polyurethane elastomer systems facility in Shanghai, strategically designed to meet the surging Asia-Pacific demand for high-durability elastomers used in renewable energy applications. The facility produces specialized PU components for offshore cable protection and silicon wafer cutting rollers—critical elements in photovoltaic (PV) panel manufacturing—demonstrating China’s deep integration of PU elastomers in the solar energy value chain.

In June 2025, Wanhua Chemical Group introduced the world’s first 100% bio-based Thermoplastic Polyurethane (TPU) elastomer derived from corn-stover PDI, setting a new industry benchmark for sustainable material development. Parallelly, the nation’s thriving Electric Vehicle (EV) industry, bolstered by government support through the New Energy Vehicle (NEV) mandate, is propelling demand for lightweight polyurethane components such as suspension bushings, bumpers, and vibration-damping seals. Large-scale infrastructure projects in high-speed rail and smart construction continue to fuel consumption of high-load-bearing cast polyurethane elastomers used for rollers, linings, and anti-vibration components. Moreover, China’s strong presence in 3D printing polyurethane materials, including photo-curable resins and TPU powders, underscores its role as a technology hub for advanced elastomeric prototyping and end-use parts manufacturing.

United States: High-Performance Polyurethane Elastomers Powering EV and Industrial Advancements

The United States polyurethane elastomers market is witnessing a paradigm shift toward electrification, sustainability, and advanced manufacturing, driven by both industrial innovation and federal policy support. In 2025, Huntsman Corporation unveiled SHOKLESS™ polyurethane systems, designed to enhance EV battery protection through lightweight, flexible foam elastomers with superior impact resistance. The innovation aligns closely with the Inflation Reduction Act (IRA) of 2022, which provides long-term tax incentives for renewable energy and electrification projects, directly boosting demand for polyurethane materials in wind turbine blade coatings, cable sheathing, and thermal insulation.

The U.S. maintains a stronghold in casting polyurethane elastomers, serving heavy-duty applications in mining, oil and gas, and manufacturing machinery. Industry players such as American Urethane and Hapco (ISO 9001:2015 certified) specialize in custom thermoset and cast urethane systems for power generation, vibration damping, and mechanical linings, showcasing the country’s leadership in precision elastomer engineering. Additionally, North America’s dominance in 3D printing materials is expanding the adoption of polyurethane-based elastomers for functional prototyping and complex industrial geometries. Supported by cutting-edge innovation and a robust regulatory framework, the U.S. is setting global standards in durable, sustainable, and high-performance polyurethane elastomer applications across EVs, renewables, and heavy industry.

Germany: Sustainable Polyurethane Elastomers Driving Premium Automotive and Material Science Innovation

Germany continues to spearhead the European polyurethane elastomers market, leveraging its technological expertise, automotive precision engineering, and sustainability mandates. BASF SE is leading the industry transition toward bio-based and recycled polyurethane solutions, unveiling new product lines in 2024–2025 to meet automotive lightweighting and footwear performance demands. Germany’s premium automotive manufacturers, operating under EU CO₂ emission regulations, are driving high consumption of lightweight, vibration-resistant polyurethane elastomers for chassis components, suspension systems, and NVH (Noise, Vibration, Harshness) reduction.

Strategic partnerships are also reshaping regional distribution dynamics. In July 2023, Nordmann partnered with Era Polymers to expand elastomer distribution across Europe, strengthening Germany’s access to specialty grades for construction, industrial tooling, and offshore engineering applications. The nation’s strong focus on energy-efficient construction, backed by the European Green Deal, is increasing adoption of PU-based sealants and insulating systems for high-performance building envelopes. Companies like Covestro and LANXESS continue to invest in R&D for next-generation polyurethane material science, emphasizing durability, resilience, and recyclability. With its advanced infrastructure and regulatory leadership, Germany remains the epicenter of innovation for sustainable, high-performance polyurethane elastomer systems in Europe.

India: Expanding Automotive Manufacturing and Renewable Energy Fueling Polyurethane Elastomer Growth

India is rapidly emerging as a high-growth market for polyurethane elastomers, supported by accelerating industrialization, automotive production, and renewable energy expansion. In early 2025, BASF SE announced the construction of a new Cellasto® microcellular polyurethane plant in Dahej, designed to serve the automotive suspension, bushing, and NVH segment. The project enhances BASF’s localization strategy, enabling faster delivery and greater cost efficiency for domestic OEMs. The country’s growing automotive output, particularly in light commercial vehicles (LCVs) and heavy-duty trucks, is driving large-scale consumption of abrasion-resistant PU elastomers for seals, tires, and vibration control applications.

India’s national commitment to achieving 500 GW of renewable energy capacity by 2030 is creating additional opportunities for high-performance polyurethane casting elastomers used in wind turbine blade coatings, cable protection systems, and industrial insulation. Events like PU TECH 2025 in Greater Noida showcase India’s role as a global meeting point for PU technology and sustainability, where leading firms, including BASF, unveiled bio-based and recycled polyurethane solutions. Supported by rising local manufacturing, policy-driven investment, and export potential, India is positioning itself as a regional powerhouse for industrial-grade and automotive polyurethane elastomer production.

Japan: Advanced Polyurethane Material Science and Mobility Innovations

Japan remains a global innovator in polyurethane elastomer research and application, particularly in automotive, industrial, and consumer design sectors. Mitsui Chemicals, Inc. continues to lead through significant R&D investment in functional PU materials, targeting improvements in mechanical resilience, temperature resistance, and long-term flexibility. Its Mobility Solutions division focuses on developing high-performance PU elastomers for vehicle weight reduction, impact absorption, and safety enhancement, aligning with Japan’s automotive innovation roadmap toward carbon neutrality.

In March 2025, Mitsui Chemicals’ open-lab collaboration showcased next-generation polymer innovations at Milan Design Week, emphasizing aesthetic and functional TPU elastomers for consumer and design applications. Japan also maintains strong industrial demand for casting and thermoplastic polyurethane elastomers in rollers, conveyor belts, and precision parts, where reliability and wear resistance are crucial. Combining precision manufacturing, robotics integration, and a culture of continuous improvement, Japan remains at the forefront of functional polyurethane elastomer innovation, shaping global advancements in mobility, robotics, and industrial materials.

European Union: Regulatory Push Accelerating Sustainable Polyurethane Elastomer Transformation

The European Union is playing a pivotal role in transforming the polyurethane elastomers industry through aggressive climate targets and circular economy mandates. Under the ‘Fit for 55’ legislative initiative, the EU aims to cut CO₂ emissions from new cars by 55% by 2030 and achieve full carbon neutrality by 2035. The regulatory framework is fueling demand for lightweight, high-resilience polyurethane elastomers used in EV battery housings, chassis components, and structural adhesives, supporting both safety and energy efficiency.

The Renewable Energy Directive and EU Green Deal are propelling the adoption of bio-based, recyclable, and circular-content polyurethane materials, prompting leading producers such as Covestro and BASF to expand their sustainable elastomer portfolios. Furthermore, international partnerships—such as the Canada-EU Strategic Raw Materials Agreement (2020) and collaboration with Chile—strengthen supply chain resilience for essential chemical precursors like isocyanates and polyols. The Nordmann–Era Polymers partnership, covering multiple European countries, further enhances regional distribution for specialty polyurethane elastomers. Through cohesive industrial collaboration and regulatory enforcement, the EU continues to lead the global shift toward sustainable polyurethane elastomer production and circular material innovation.

Polyurethane Elastomers Market Report Scope

Polyurethane Elastomers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5 Billion

|

|

Market Size (2034)

|

$7 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Type (Thermoplastic Polyurethane, Thermoset/Cast Polyurethane, Microcellular, Millable, Two-Component Systems), By Processing Method (Casting, Injection Molding, Extrusion, Reaction Injection Molding, Compression Molding, 3D Printing), By End-Use Industry (Automotive & Transportation, Construction & Infrastructure, Consumer Goods & Footwear, Energy & Power, Medical, Electronics & Electrical

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Covestro AG, BASF SE, The Dow Chemical Company, Huntsman International LLC, Wanhua Chemical Group Co., Ltd., Mitsui Chemicals, Inc., LANXESS AG, The Lubrizol Corporation, American Urethane, Inc., TSE Industries, Inc., Era Polymers Pty Ltd, Chemtura Corporation (LANXESS), Hapco, Inc., Argonics, Inc., H.B. Fuller Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type

- Thermoplastic Polyurethane

- Thermoset/Cast Polyurethane

- Microcellular

- Millable

- Two-Component Systems

By Processing Method

- Casting

- Injection Molding

- Extrusion

- Reaction Injection Molding

- Compression Molding

- 3D Printing

By End-Use Industry

- Automotive & Transportation

- Construction & Infrastructure

- Consumer Goods & Footwear

- Energy & Power

- Medical

- Electronics & Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polyurethane Elastomers Market

- Covestro AG

- BASF SE

- The Dow Chemical Company

- Huntsman International LLC

- Wanhua Chemical Group Co., Ltd.

- Mitsui Chemicals, Inc.

- LANXESS AG

- The Lubrizol Corporation

- American Urethane, Inc.

- TSE Industries, Inc.

- Era Polymers Pty Ltd

- Chemtura Corporation (LANXESS)

- Hapco, Inc.

- Argonics, Inc.

- H.B. Fuller Company

*- List not Exhaustive

Research Coverage

This report investigates the Global Polyurethane Elastomers Market, delivering analysis reviews on demand drivers, technology shifts, and procurement dynamics across mobility, construction, industrial machinery, and consumer applications; it highlights breakthroughs in TPU processing, circular feedstock integration, and NVH-optimized formulations while benchmarking regional capacity moves and raw-material security—making this report an essential resource for executives, product managers, sourcing leaders, and R&D teams. Developed by USDAnalytics, the study maps policy and sustainability impacts on elastomer selection, compares cost-to-serve across casting, injection, extrusion, and 3D printing lines, and quantifies mix shifts between thermoplastic and thermoset systems. It further evaluates competitive strategies, pricing risks (MDI/TDI, energy), and end-use performance metrics (abrasion, hydrolysis, resilience) to support capital planning, supplier rationalization, and market-entry playbooks.

Scope Highlights

Segmentation:

- By Type: Thermoplastic Polyurethane; Thermoset/Cast Polyurethane; Microcellular; Millable; Two-Component Systems.

- By Processing Method: Casting; Injection Molding; Extrusion; Reaction Injection Molding; Compression Molding; 3D Printing.

- By End-Use Industry: Automotive & Transportation; Construction & Infrastructure; Consumer Goods & Footwear; Energy & Power; Medical; Electronics & Electrical.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.