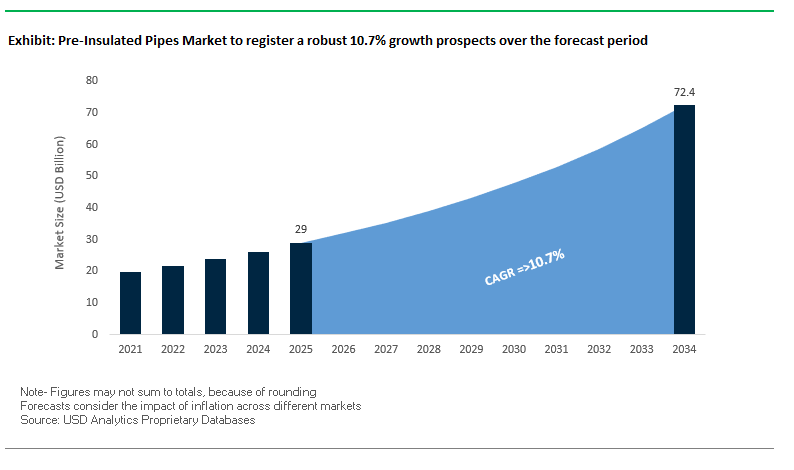

The global pre-insulated pipes market is projected to grow from $29 billion in 2025 to $72.4 billion by 2034, at a CAGR of 10.7%, propelled by the rising demand for energy-efficient infrastructure and district heating and cooling networks. Pre-insulated pipes minimize heat loss by up to 60%, making them ideal for urban heat distribution systems, industrial applications, and large-scale utility networks. The use of polyurethane insulation ensures durability, thermal efficiency, and cost-effectiveness, while the robust outer jacket protects against moisture, corrosion, and physical damage, extending product lifespan and reducing maintenance costs.

Recent developments in the pre-insulated pipes industry highlight a blend of innovation, large-scale project deployment, and material advancements. In August 2025, a Nano Letters study introduced an ALD-based nanocoating strategy, which could enhance high-performance insulation in next-generation pipe systems. That same month, SP Group secured a USD 16.7 million, 10-year contract for Chengdu Future Medical City, leveraging pre-insulated pipes with smart control systems for district heating and cooling.

The Middle East continues to emerge as a strategic market. In May 2025, Perma-Pipe International Holdings announced a contract in Qatar, strengthening its footprint in the region’s district cooling infrastructure. Meanwhile, April 2025 witnessed a U.S. district heating provider installing flexible pre-insulated pipes, modernizing aging urban networks and reducing energy loss by over 15%. Pre-insulated pipes with Vacuum Insulated Panels (VIP) technology, such as Uponor’s Ecoflex VIP 2.0, showcased in March 2025 at ISH Frankfurt, demonstrate cutting-edge thermal performance with reduced jacket sizes.

Infrastructure modernization projects are also shaping market growth. In January 2025, Memphis Light, Gas, and Water announced a USD 30 million gas infrastructure upgrade, involving the replacement of old pipelines with pre-insulated solutions. Earlier initiatives include ORBIS Corporation’s November 2024 manufacturing expansion in Ohio and Brugg Pipes’ September 2024 delivery of specialized stainless steel pipes for a mobile LNG platform in the Gulf of Mexico.

The pre-insulated pipes market is increasingly shaped by government-led investments in district heating networks as part of broader decarbonization strategies. The UK’s Heat Network Transformation Programme (HNTP), which includes over £500 million in capital funding through the Green Heat Network Fund (GHNF), is a prime example. This program is designed to accelerate the transition to low-carbon heating, creating consistent demand for high-performance pre-insulated pipe systems. Beyond the UK, Copenhagen serves as a global benchmark—its district heating network supplies 98% of buildings with heat derived from biomass and energy-from-waste facilities. The city’s pathway to becoming carbon-neutral by 2025 demonstrates the long-term potential of district heating as a cornerstone of climate policy. These initiatives reinforce pre-insulated pipes as critical enablers of large-scale, sustainable energy distribution systems in urban environments.

Rising demand for resilient infrastructure is driving major investments in manufacturing capacity for pre-insulated pipes. Leading producers are expanding production lines to support high-temperature applications such as geothermal and biomass-based heating, where transporting steam and hot water requires robust insulation and structural integrity. The Middle East is a focal point for growth, with district cooling emerging as a large-scale application. Mega projects in Dubai and Riyadh are requiring large-diameter pipes, in some cases up to 1,200mm, to efficiently deliver chilled water across urban districts. This shift highlights how climate conditions and rapid urbanization are creating parallel demand streams for both heating and cooling infrastructure. By investing in new facilities, manufacturers are positioning themselves to capture growth across a diverse range of geographies and applications.

The integration of advanced monitoring technologies presents a significant opportunity to enhance operational efficiency and reliability. Traditional acoustic leak detection systems have limitations in noisy or low-pressure environments, whereas new approaches such as time-domain reflectometry (TDR) enable highly precise, real-time localization of leaks using embedded wires in pipe insulation. This not only reduces downtime but also minimizes environmental damage. Complementing TDR, IoT sensors are being deployed to continuously measure flow, pressure, and temperature across networks. When combined with AI-driven predictive analytics, these sensors enable operators to anticipate failures before they occur, shifting maintenance from a reactive to a proactive model. This technological evolution enhances pipeline longevity, improves safety, and reduces costs, making advanced monitoring a central opportunity for pre-insulated pipe system providers.

The transition to a low-carbon economy is creating new, high-value applications for pre-insulated pipes in hydrogen transport and carbon capture systems. Hydrogen pipelines face the challenge of embrittlement, where small hydrogen molecules penetrate and weaken steel. Research into low-alloy steels with specialized heat treatments is helping overcome this issue, offering pipe manufacturers a pathway into the emerging hydrogen economy. Similarly, carbon dioxide transport introduces corrosion risks, particularly when impurities such as water are present. High-Density Polyethylene (HDPE) has emerged as a promising solution, with potential applications as a corrosion-resistant liner inside carbon steel pipelines. This hybrid design leverages the strength of steel with the chemical resistance of HDPE, making it suitable for CCS infrastructure. These material innovations position pre-insulated pipe suppliers to play a critical role in advancing hydrogen and CCS networks that underpin global decarbonization strategies.

The global pre-insulated pipes market is dominated by companies that excel in energy efficiency, thermal performance, and installation efficiency, supported by innovative materials and strategic project deployments.

Uponor offers the Ecoflex system, featuring flexible, pre-insulated pipes for district heating and cooling. In March 2025, the company showcased Ecoflex VIP 2.0, integrating Vacuum Insulated Panels (VIP) technology to reduce jacket size by 70% while minimizing heat loss by up to 60%. Uponor focuses on sustainable, energy-efficient systems and circular PEX pipes made from 100% chemically recycled material, providing seamless integration with low-temperature heat sources like heat pumps.

GF Piping Systems provides plastic and metal pre-insulated pipes and fittings for industrial, chemical, and district cooling applications. Its Strategy 2030 emphasizes becoming a global leader in flow solutions while focusing on core business areas. The company’s integrated systems, including pipes, valves, and automation, ensure reliability and system integrity. Strategic partnerships, including the 2023 acquisition of Uponor, have strengthened GF’s global footprint in the pre-insulated pipe market.

Perma-Pipe specializes in advanced insulation solutions for district heating, cooling, oil and gas, and industrial projects. Recent expansions include a new manufacturing facility in Fujairah, UAE, supporting megaprojects like NEOM and Lusail City. Beyond standard pipes, the company provides containment systems, anti-corrosion coatings, custom fabrication, and leak detection technologies, ensuring safety, reliability, and long-term performance.

Logstor’s product line includes rigid and flexible pre-insulated pipes, joints, and fittings. The company recently launched PertFlextra, enhancing installation efficiency, and developed ReCase, a recycled plastic pipe casing solution. Logstor is recognized for inventing the pre-insulated pipe and flexible pipe, delivering low heat loss, long service life, and solutions for major projects like heat distribution to 6,900 homes in Denmark.

Thermaflex offers the Flexalen system, a flexible pre-insulated plastic piping system made from 100% recyclable Polybutylene (PB). Its single-piece design reduces joints and installation time, supporting energy-efficient heating and cooling networks. Thermaflex also provides engineering support and training services, ensuring optimal system performance and durability while meeting growing demand for eco-friendly, sustainable solutions.

Flexible pre-insulated pipes capture 65% of the market share, highlighting their superior installation and operational advantages in district heating, cooling, and retrofit projects. Their ability to be transported on reels, bent around obstacles, and installed with fewer joints significantly reduces labor costs and energy losses, making them the preferred option in dense urban infrastructure and complex retrofitting scenarios. By contrast, rigid pre-insulated pipes, while essential for long straight runs and high-pressure, high-temperature applications, command a smaller share at 35%. Their resilience makes them indispensable in industrial plants, power stations, and large-scale greenfield DHC projects, but the industry-wide shift toward energy efficiency, speed of installation, and urban adaptability favors flexible solutions. This segmentation reflects the structural shift toward flexible, modular, and cost-efficient systems as global cities expand DHC networks to meet decarbonization goals.

District heating and cooling systems account for a commanding 45% market share, underscoring their pivotal role in the decarbonization of urban energy infrastructure. The demand is fueled by large-scale government initiatives promoting energy-efficient networks powered by geothermal, biomass, and waste heat recovery systems. Pre-insulated pipes are essential to minimizing thermal losses in these networks, making them a cornerstone of long-term carbon reduction strategies. Oil & gas follows with a significant share, leveraging pre-insulated solutions for temperature-controlled crude transport and offshore pipelines, where durability and thermal stability are critical. Industrial processes, representing 15%, sustain demand through their use in steam, process heating, and cooling lines where efficiency and worker safety are paramount. Infrastructure and utilities—including snow-melting and recirculating hot water systems—remain smaller but strategic markets, while food processing and water treatment occupy specialized niches where hygiene and freeze protection are critical. The dominance of district heating and cooling illustrates how urban energy transition policies are the central growth driver, with oil & gas and industrial processes providing resilience and diversification for the pre-insulated pipes market.

The European Union pre-insulated pipes market is expanding rapidly, fueled by the European Green Deal and the region’s Net Zero carbon reduction targets. District heating and cooling networks are central to the EU’s decarbonization strategy, and pre-insulated pipes are vital in ensuring minimal heat loss and maximum energy efficiency. The Energy Performance of Buildings Directive (EPBD) is another major driver, as it requires member states to strengthen building codes, mandating the use of high-performance insulation materials in both new construction and renovation projects.

Governments and utilities are incentivizing infrastructure projects that incorporate cutting-edge insulation schemes to reduce energy transmission losses. Manufacturers are responding with innovations such as BRUGG Pipes’ CALPEX PUR-KING system, which has consistently achieved top thermal efficiency ratings from the Danish Technological Institute (DTI) for seven consecutive years. To enhance reliability, producers are integrating IoT-enabled monitoring systems with fiber optic sensors, offering real-time diagnostics for proactive maintenance and early leak detection. These regulatory and technological advancements are positioning the EU as a leader in sustainable and smart district heating solutions.

The United States pre-insulated pipes market is supported by the Department of Energy (DOE), which is funding energy-efficient infrastructure and district energy systems to modernize urban and industrial networks. Advancements in insulation are evident through collaborations such as Huntsman’s partnership with BRUGG Pipes, which developed new polyurethane foam systems to improve thermal performance and flexibility in pre-insulated pipes.

Federal and state-level regulations also promote modernization of aging infrastructure, while organizations like the U.S. Plastics Pact are advocating recyclability and sustainability for plastic-based systems. Beyond urban energy use, pre-insulated pipes are gaining traction in industrial applications such as oil and gas, pharmaceuticals, and food processing, where they play a crucial role in maintaining process stability and reducing heat loss. Additionally, the growth of smart city projects is creating demand for integrated pre-insulated pipe systems equipped with digital monitoring technologies, driving innovation in urban infrastructure development.

China is witnessing rapid growth in its district heating and cooling infrastructure, with urban areas increasingly dependent on pre-insulated pipes for efficient energy transmission. The government is promoting adoption through financial incentives and regulations aimed at advancing energy efficiency in construction and utilities. Local manufacturers are responding with flexible and modular piping systems that simplify retrofits and minimize excavation in congested city environments.

The adoption of embedded sensors and fiber optic monitoring systems is enabling real-time diagnostics, supporting proactive maintenance and safety in large-scale energy networks. At the materials level, Chinese producers are exploring eco-friendly insulation alternatives such as polyisocyanurate (PIR) foams and recyclable jacket materials to align with green building standards. Strategic industry moves, such as PERMA-PIPE’s alliance with local distributors, are strengthening China’s supply capabilities for industrial and district energy applications. These efforts underline China’s commitment to a circular economy and advanced infrastructure modernization.

Canada’s pre-insulated pipes market is shaped by strict regulatory oversight under the Canadian Energy Regulator Act, which ensures that pipelines meet Canadian Standards Association (CSA) specifications for safety and durability. A major application of pre-insulated pipes in Canada is in municipal water and wastewater systems, particularly in remote northern regions, where pipes must withstand extreme conditions to prevent freezing.

Examples such as the Tataskweyak Cree Nation project, which installed over 25,000 feet of HDPE factory-insulated pipe, showcase the importance of these systems in challenging environments. Provincial regulations, such as the Oil and Gas Activities Act in British Columbia, further emphasize emergency management and pipeline integrity programs, driving adoption of advanced monitoring systems. In addition to energy pipelines, Canada is seeing increased demand for district energy networks for both heating and chilled water, reinforcing the country’s reliance on pre-insulated pipe solutions for urban and remote infrastructure resilience.

Germany remains a leading market for pre-insulated pipes, supported by its extensive district heating systems and commitment to carbon reduction goals. Compliance with the Energy Performance of Buildings Directive (EPBD) is a major driver, as new and retrofitted buildings require high-performance insulation to meet efficiency standards. German companies are actively scaling their manufacturing footprint—Armacell’s acquisition of IZOLIR expands its capabilities in pre-insulated pipe production, strengthening supply within Europe.

Technological innovation is a hallmark of the German market, with manufacturers offering integrated monitoring systems and developing advanced insulation materials. Moreover, the shift toward renewable energy sources such as biomass and solar thermal is increasing demand for efficient pre-insulated pipe networks to transport renewable heat. Germany’s role as a technology innovator and renewable energy adopter ensures its dominance in shaping best practices for pre-insulated pipe systems across Europe.

India’s pre-insulated pipes market is gaining momentum due to the government’s focus on smart city projects and rapid urbanization, both of which require efficient district cooling and heating networks. The “Make in India” initiative is encouraging domestic manufacturing, leading to investments in local production facilities for pre-insulated pipes and components, reducing reliance on imports.

Local companies such as Zeco Aircon are innovating with high-density polyurethane foams and UV-resistant outer jackets, designed for durability and long-term performance in diverse climatic conditions. Additionally, demand is growing in industrial process piping for pharmaceuticals, chemicals, and food processing, where temperature stability is critical. The adoption of PIR foams for high-temperature applications demonstrates the market’s shift toward more durable, efficient insulation solutions. With rising industrial needs and government-backed infrastructure projects, India is emerging as a key growth hub for pre-insulated pipe adoption in Asia.

|

Parameter |

Details |

|

Market Size (2025) |

$29 Billion |

|

Market Size (2034) |

$72.4 Billion |

|

Market Growth Rate |

10.7% |

|

Segments |

By Pipe Type (Flexible, Rigid), By Material (Carrier Pipe, Insulation, Outer Casing), By Application (District Heating & Cooling, Oil & Gas, Industrial Processes, Infrastructure & Utility, Water Treatment, Food Processing), By Installation Type (Below Ground, Above Ground) |

|

Study Period |

2019- 2024 and 2025-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Uponor Corporation, Logstor A/S, Thermaflex International Holding B.V., Brugg Pipes Systems AG, Perma-Pipe International Holdings, Inc., Zeco Aircon Limited, Kingspan Group plc, Ineos Group Ltd., Armacell International S.A., Insul-Tek Piping Systems, LLC, RPR Products, Inc., Polypipe Group plc, GF Piping Systems (Georg Fischer AG), Nan Ya Plastics Corporation, CPV Ltd. |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

* List Not Exhaustive

The research methodology for the Pre-Insulated Pipes Market combines both primary and secondary approaches to ensure data reliability, accuracy, and actionable insights. Primary research involved detailed interviews with industry executives, infrastructure planners, energy efficiency experts, pipeline engineers, and supply chain stakeholders across key regions, including North America, Europe, Asia-Pacific, and the Middle East. Secondary research encompassed analysis of company annual reports, regulatory filings, patents, sustainability disclosures, and verified industry publications, focusing on trends in polyurethane insulation, flexible versus rigid pipes, district heating and cooling projects, and smart monitoring integration. Advanced data triangulation validated market sizing, growth projections, and segment analysis, integrating macroeconomic trends, urbanization rates, energy efficiency initiatives, material costs, and technological adoption. Forecasts were derived using top-down and bottom-up approaches, while regional insights were contextualized against local regulations, decarbonization policies, infrastructure modernization projects, and smart city developments. This rigorous, multi-layered methodology by USDAnalytics ensures that the report delivers precise, fact-based, and industry-relevant intelligence for professionals operating in the global pre-insulated pipes market.

Table of Contents: Pre-Insulated Pipes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Pre-Insulated Pipes Market Landscape & Outlook (2025–2034)

2.1. Introduction to Pre-Insulated Pipes Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Drivers: Energy Efficiency and Infrastructure Modernization

2.4. Challenges: Material, Installation, and Regulatory Barriers

2.5. Future Outlook: Smart City Integration and Decarbonization Efforts

3. Innovations Reshaping the Pre-Insulated Pipes Market

3.1. Trend: ALD-Based Nanocoating and Vacuum Insulation Panels (VIP)

3.2. Trend: Flexible and Modular Pre-Insulated Pipe Systems

3.3. Opportunity: Advanced Monitoring and Leak Detection Systems (IoT & TDR)

3.4. Opportunity: Material Innovation for Hydrogen and Carbon Capture & Storage (CCS) Transport

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers, Acquisitions and Strategic Alliances

4.2. R&D and Material Innovation

4.3. Sustainability and Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Pre-Insulated Pipes Market

5.1. By Pipe Type

5.1.1. Flexible (65%)

5.1.2. Rigid (35%)

5.2. By Material

5.2.1. Carrier Pipe

5.2.2. Insulation

5.2.3. Outer Casing

5.3. By Application

5.3.1. District Heating & Cooling (45%)

5.3.2. Oil & Gas

5.3.3. Industrial Processes

5.3.4. Infrastructure & Utility

5.3.5. Water Treatment

5.3.6. Food Processing

5.4. By Installation Type

5.4.1. Below Ground

5.4.2. Above Ground

6. Country Analysis and Outlook of Pre-Insulated Pipes Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Pre-Insulated Pipes Market Size Outlook by Region (2025–2034)

7.1. North America Pre-Insulated Pipes Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Application

7.1.3. By Installation Type

7.2. Europe Pre-Insulated Pipes Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Application

7.2.3. By Installation Type

7.3. Asia Pacific Pre-Insulated Pipes Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Application

7.3.3. By Installation Type

7.4. South America Pre-Insulated Pipes Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Application

7.4.3. By Installation Type

7.5. Middle East and Africa Pre-Insulated Pipes Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Application

7.5.3. By Installation Type

8. Company Profiles: Leading Players in the Pre-Insulated Pipes Market

8.1. Uponor Corporation

8.2. Logstor A/S

8.3. Thermaflex International Holding B.V.

8.4. Brugg Pipes Systems AG

8.5. Perma-Pipe International Holdings, Inc.

8.6. Zeco Aircon Limited

8.7. Kingspan Group plc

8.8. Ineos Group Ltd.

8.9. Armacell International S.A.

8.10. Insul-Tek Piping Systems, LLC

8.11. RPR Products, Inc.

8.12. Polypipe Group plc

8.13. GF Piping Systems (Georg Fischer AG)

8.14. Nan Ya Plastics Corporation

8.15. CPV Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

The global pre-insulated pipes market is expected to grow from $29 billion in 2025 to $72.4 billion by 2034, at a CAGR of 10.7%. Growth is driven by energy-efficient infrastructure, district heating and cooling networks, and the adoption of durable polyurethane insulation with high thermal performance.

Flexible pre-insulated pipes dominate with 65% market share due to easier installation, reduced joints, and adaptability in urban infrastructure and retrofitting projects. Rigid pipes, accounting for 35%, are preferred for high-pressure, high-temperature, and long-straight-run applications, particularly in industrial and greenfield projects.

Advanced monitoring systems, including IoT sensors and time-domain reflectometry (TDR), enable real-time leak detection, flow measurement, and predictive maintenance. These technologies reduce downtime, prevent energy loss, and enhance operational efficiency, making smart pre-insulated pipes critical for urban energy networks and industrial systems.

Government-led programs such as the UK’s Heat Network Transformation Programme, EU Green Deal incentives, and U.S. DOE funding are accelerating district heating and cooling adoption. Such initiatives promote energy-efficient infrastructure, support smart city projects, and create long-term demand for pre-insulated pipes.

Material innovations, including polyurethane foam, high-density polyethylene (HDPE) liners, vacuum insulation panels (VIP), and corrosion-resistant steel, enhance thermal efficiency, durability, and suitability for hydrogen and carbon capture transport. These developments expand applications across energy, industrial, and sustainable infrastructure projects.