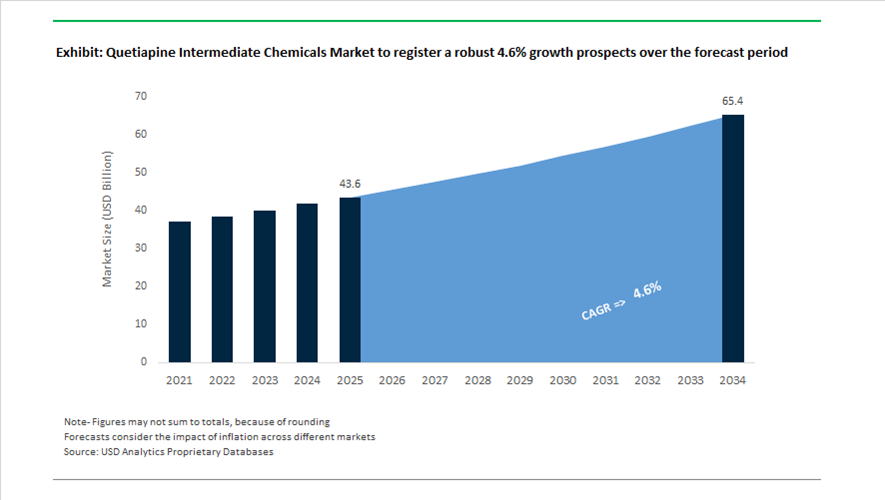

Quetiapine Intermediate Chemicals Market Valued at $43.6 Billion in 2025, Projected to Reach $65.4 Billion by 2034 at 4.6% CAGR

The global quetiapine intermediate chemicals market is valued at $43.6 billion in 2025 and is projected to reach $65.4 billion by 2034, registering a CAGR of 4.6%. Market expansion is anchored in rising demand for dibenzo[b,f][1,4]thiazepin-11(10H)-one intermediates, piperazine derivatives, quetiapine fumarate precursors, tricyclic CNS building blocks, and high-purity key starting materials (KSMs) used in psychiatric drug manufacturing. As quetiapine remains widely prescribed for schizophrenia, bipolar disorder, and major depressive disorder, intermediate suppliers are prioritizing process intensification, impurity control, and regional supply chain resilience to meet stringent pharmaceutical compliance standards.

Manufacturing innovation accelerated in late 2024. Researchers from the National Institute of Pharmaceutical Education and Research published a telescopic, metal-free reductive amidation process for synthesizing dibenzo[b,f][1,4]thiazepin-11(10H)-one, a core quetiapine intermediate. This green synthesis route eliminates traditional acidic purification stages, reduces solvent waste, and improves atom economy, aligning with global pharmaceutical sustainability mandates. In October 2024, National Resilience secured $17.5 million in U.S. federal funding to scale domestic production of essential medicine intermediates, including tricyclic CNS scaffolds critical for quetiapine. In December 2024, Allchem Lifescience filed for a ₹190 crore IPO, highlighting its specialization in piperazine derivatives and tricyclic intermediates to expand API intermediate manufacturing capacity.

Operational restructuring and self-reliance initiatives intensified through 2025. Indian pharmaceutical manufacturers expanded “import substitute” programs to reduce dependence on Chinese intermediate supply chains, which historically accounted for over 70% of certain quetiapine precursors. Companies including IOL Chemicals & Pharmaceuticals and Ami Organics announced new production lines for high-purity KSMs to strengthen domestic availability. Throughout 2025, major producers such as Aarti Pharmalabs and Aether Industries adopted continuous flow chemistry for piperazine derivative production, improving reaction control, reducing batch variability, and lowering reactor footprint. In mid-2025, updated USP and European Pharmacopoeia monographs introduced stricter limits on genotoxic impurities in halogenated intermediates used during condensation synthesis, compelling manufacturers to upgrade analytical validation and purification protocols.

Supply chain governance remains central to risk management. In 2024, AstraZeneca streamlined its global Seroquel supply chain to mitigate raw material volatility affecting branded and extended-release portfolios. In January 2026, the UK MHRA issued a Class 1 recall for quetiapine oral suspension produced by Eaststone Limited due to double-strength active ingredient concentration, underscoring the critical importance of intermediate quality control and dosage accuracy. The quetiapine intermediate chemicals market is increasingly characterized by continuous flow synthesis adoption, green telescopic reductive amidation processes, domestic KSM capacity expansion, genotoxic impurity tightening under USP and Ph. Eur. standards, pharmaceutical-grade tricyclic scaffold manufacturing, and regulatory-driven quality assurance investments. As CNS therapeutics demand remains stable, intermediate innovation and compliance rigor will continue shaping global production strategies.

Strategic Trends and Growth Opportunities in the Quetiapine Intermediate Chemicals Market

Strategic Friend-Shoring and Supply Chain Diversification for Psychiatric APIs

The quetiapine intermediate chemicals market is undergoing a structural realignment driven by national drug security priorities and risk-adjusted sourcing strategies. Mental health medications are now classified as essential therapies across most OECD markets, prompting pharmaceutical companies to move away from single-country, low-cost sourcing models toward diversified, resilience-led supply networks spanning Europe and North America.

By 2025, internal supply chain resilience benchmarks across Tier-1 pharmaceutical manufacturers show that companies relying exclusively on Indian or Chinese intermediates experienced repeated disruptions during 2024 logistics bottlenecks. In response, leading buyers are qualifying two to three alternate suppliers per critical quetiapine intermediate. While this diversification has increased Cost of Goods Sold by an estimated 2% to 3%, it has improved on-time-in-full service levels to above 95% during regional trade and transport shocks, a trade-off now widely accepted by procurement and regulatory teams.

This shift is reinforcing investment in domestic and near-shore capacity. During 2024 and 2025, the U.S. Food and Drug Administration reported a 22% increase in new drug launches, including multiple CNS therapies relying on thiazepine-based intermediates. This demand is catalyzing capacity expansion by CDMOs and specialty chemical manufacturers, with companies such as Ami Organics expanding through partnerships and regional manufacturing hubs. These investments directly support U.S. and EU expectations for traceable, auditable, and geopolitically secure pharmaceutical supply chains.

Process Intensification and Greener Synthetic Route Optimization

Margin pressure in the global generic antipsychotic market is accelerating the adoption of process intensification and continuous manufacturing technologies for quetiapine intermediates. Producers are increasingly replacing labor-intensive batch synthesis with flow chemistry and continuous crystallization to improve yield consistency and reduce environmental and operational costs.

In 2025, Dr. Reddy’s Laboratories disclosed advancements in continuous processing for key thiazepine precursors, including dibenzo[b,f][1,4]thiazepin-11(10H)-one. These methods shorten reaction cycles, minimize downtime, and significantly reduce solvent waste, enabling manufacturers to protect margins despite ongoing price erosion in mature generic markets.

At the same time, ESG-driven procurement policies are reshaping acceptable synthetic pathways. Modern routes for intermediates such as 11-(piperazin-1-yl)dibenzo[b,f][1,4]thiazepine increasingly emphasize solvent minimization, higher atom economy, and energy-efficient reaction conditions. High-pressure and high-temperature process optimization has allowed faster conversions with lower overall energy consumption, aligning quetiapine intermediate production with sustainability metrics now embedded in hospital and public healthcare tender frameworks.

Specialized Intermediates for Extended-Release and Long-Acting Formulations

A clear premium opportunity is emerging from the pharmaceutical industry’s shift away from immediate-release quetiapine toward extended-release and long-acting dosage forms. These formulations are designed to improve patient adherence and reduce relapse rates in chronic psychiatric conditions, but they impose far tighter specifications on upstream chemical intermediates.

Formulation research into quetiapine fumarate extended-release systems using hydrophilic polymer matrices has demonstrated that granule size distribution, bulk density, and surface morphology of the intermediate are critical quality attributes. Even minor deviations can trigger dose dumping, particularly in alcohol-sensitive matrix systems. As a result, pharmaceutical buyers are increasingly sourcing intermediates manufactured under controlled crystallization conditions with validated particle size control rather than relying on commodity-grade inputs.

This precision requirement is extending into novel delivery platforms such as transdermal systems and long-acting injectables. For these applications, demand is rising for ultra-low impurity grades of intermediates like 1-[2-(2-hydroxyethoxy)ethyl] piperazine. Suppliers capable of guaranteeing 99.5% purity alongside full extractable and leachable documentation are commanding material price premiums, reflecting the high regulatory and clinical risk associated with advanced CNS delivery technologies.

Regulatory Compliance, Analytical Standards, and Validation-Ready Supply

An additional structurally attractive opportunity lies in regulatory compliance support and certified analytical standards. As health authorities intensify risk-based inspections, generic drug manufacturers are investing heavily in analytical rigor across their quetiapine value chains.

During 2024 and 2025, India’s Central Drugs Standard Control Organisation tested more than 116,000 drug samples, identifying over 3,100 as not of standard quality. This heightened surveillance has pushed manufacturers to adopt stability-indicating HPLC methods and validated impurity profiling for quetiapine-related substances, including dimers and late-stage process impurities.

Regulators such as the European Medicines Agency and the U.S. FDA are now requiring deeper analytical validation within Drug Master Files, increasing demand for certified reference materials and characterized impurity standards. Chemical specialists that can supply not only the intermediate but also DMF support, pharmacopeial alignment, and high-purity reference standards such as Quetiapine Related Compound B are capturing a recurring, non-cyclical revenue stream. In this niche, pricing is driven by compliance criticality rather than volume, with certain specialty standards commanding prices as high as USD 855 per 15 mg unit.

Quetiapine Intermediate Chemicals Market Share and Segmentation Insights

Piperazine Side-Chain Intermediates Lead Quetiapine API Manufacturing Supply Chain

Piperazine side-chain intermediates accounted for 38.60% of the Quetiapine Intermediate Chemicals Market by intermediate type in 2025, reflecting their critical role in the synthesis of quetiapine active pharmaceutical ingredient. The piperazine moiety forms a key structural component responsible for the drug’s pharmacological activity, making these intermediates essential for large scale API production. Established synthesis routes and reliable chemical supply chains support consistent manufacturing for global pharmaceutical markets. These intermediates are produced through validated pharmaceutical grade processes to meet regulatory standards required by API manufacturers. In 2025, production optimization and dedicated intermediate manufacturing facilities are strengthening supply reliability, enabling large scale pharmaceutical manufacturers to secure cost efficient sourcing for generic antipsychotic drug production.

Generic Drug Manufacturing Dominates Demand for Quetiapine Intermediate Chemicals

Generic drug manufacturing represented 72.80% of the Quetiapine Intermediate Chemicals Market by end use in 2025, supported by the widespread global production of generic quetiapine following the expiration of patent protection for the original branded drug. Numerous pharmaceutical manufacturers produce quetiapine active pharmaceutical ingredient for distribution across global markets, driving significant demand for upstream intermediate chemicals. Competitive pricing pressures and large scale API production have shaped supply chain strategies for intermediates. In 2025, increasing consolidation of generic API manufacturing in India and China is influencing intermediate supply chains, with vertically integrated manufacturers producing both intermediates and finished APIs to improve cost efficiency and maintain regulatory compliance across international pharmaceutical markets.

Quetiapine Intermediate Chemicals Market Competitive Landscape

The 2026 quetiapine intermediate chemicals market is evolving toward vertically integrated production, continuous flow synthesis, and cGMP-compliant supply chains. Growth is driven by rising CNS disorder treatments, China+1 sourcing strategies, and demand for high-purity intermediates in regulated pharmaceutical markets.

Jubilant Ingrevia scales CNS intermediate CDMO capabilities with multi-purpose plant expansion

Jubilant Ingrevia Limited is strengthening its position in quetiapine intermediate chemicals through integrated pyridine and diketene chains supporting CDMO growth. Specialty Chemicals remains a key revenue driver, with CDMO income projected to rise from ₹3 billion in FY26 to ₹12 billion by FY28. Construction of a new multi-purpose plant in Gajraula targets complex pharmaceutical intermediates and advanced fine chemicals. Portfolio expansion includes 10+ new molecules added in 2025 with expected peak revenues exceeding ₹1,200 crore. Strong quarterly performance in 2026 reflects efficient large-scale production despite pricing pressures. Focus on heterocyclic intermediates supports supply of high-purity CNS drug precursors.

Divi’s Laboratories strengthens regulated market leadership with FDA-compliant custom synthesis scale

Divi’s Laboratories maintains a dominant role in quetiapine intermediate manufacturing through large-scale custom synthesis and regulatory excellence. A successful US FDA inspection with zero observations confirms compliance with stringent global standards for pharmaceutical intermediates. Long-term supply agreements signed in 2025 reinforce revenue visibility and supply chain reliability. Strong export growth, reflected in ₹545 crore PAT and rising shipment volumes, indicates robust demand from regulated markets. Advanced chemistry capabilities support production of intermediates meeting USP and EP specifications. Focus on high-volume generics and custom synthesis strengthens its role as a preferred partner for global pharma companies.

Hikal advances specialty intermediate production with recovery strategy and R&D-driven diversification

Hikal Limited is rebuilding its pharmaceutical intermediate business through operational recovery and diversification into adjacent high-value segments. Return to positive performance in FY26 follows regulatory remediation and resumed global supplies. The Pune Research and Technology Centre supports scale-up of niche molecules across oncology, anti-migraine, and CNS-linked chemistries. Revenue growth of 10% to ₹494 crore and EBITDA margin improvement to 16.8% reflect higher capacity utilization. Expansion into personal care intermediates reduces dependence on traditional API cycles. Focus on specialized intermediates enhances positioning in complex pharmaceutical supply chains.

Teva integrates intermediate production with global API network to secure quetiapine supply chain

Teva Pharmaceutical Industries Ltd. operates an integrated model combining intermediate synthesis and finished dosage manufacturing for quetiapine products. Strategic focus on high-value generics and long-acting injectables requires consistent supply of high-purity intermediates. Global API network enables one-stop solutions from precursor production to final formulation, improving cost efficiency. Backward integration ensures control over impurity profiles to meet US and EU regulatory standards. Clinical and product development platforms support expansion into advanced CNS therapies. Manufacturing scale supports supply of multiple quetiapine dosage strengths across global markets.

Sun Pharma enhances vertical integration with green chemistry and specialty CNS formulation focus

Sun Pharmaceutical Industries Ltd. is leveraging vertical integration to strengthen control over quetiapine intermediate supply and formulation quality. Emphasis on extended-release CNS formulations requires precise intermediate specifications and process optimization. Investments in green chemistry reduce waste and improve sustainability in thiazepine-based synthesis. Internal manufacturing capabilities mitigate exposure to raw material volatility and specialty catalyst pricing. Expansion into emerging markets in Latin America and Southeast Asia supports demand for affordable neuropsychiatric treatments. Integrated chemical production supports scalability and cost efficiency in global operations.

AstraZeneca optimizes legacy CNS intermediate supply with global manufacturing investments and CDMO partnerships

AstraZeneca is maintaining stability in quetiapine intermediate supply through a globally diversified manufacturing and sourcing strategy. The company reported $58.7 billion in 2025 revenue with continued growth supported by a balanced therapeutic portfolio. Large-scale investments of $50 billion in the US and $15 billion in China enhance resilience of pharmaceutical supply chains. Strategic pricing agreements in 2025 improve market access and cost stability in key regions. Collaboration with CDMOs ensures consistent production of high-purity intermediates aligned with modern regulatory and environmental standards. Legacy CNS portfolio management continues to generate steady demand for quetiapine-based therapies.

India Quetiapine Intermediate Chemicals Market: PLI-Driven API Expansion, Export Acceleration, and CNS Supply Chain Localization

India is rapidly positioning itself as a global powerhouse in the quetiapine intermediate chemicals market, leveraging the Production Linked Incentive (PLI) Scheme for bulk drugs and APIs to transition from import dependency to high-value export leadership in CNS and respiratory intermediates. As of March 2026, the commissioning of 38 greenfield pharmaceutical projects has established a domestic manufacturing capacity of approximately 56,800 metric tons per annum, significantly strengthening India’s footprint in active pharmaceutical ingredients (APIs), key starting materials (KSMs), and advanced intermediates for quetiapine synthesis. This expansion is supported by cumulative investments of ₹46,734 crore (~$5.6 billion), surpassing initial government targets and reinforcing India’s role in global pharmaceutical supply chain diversification.

Export performance is gaining strong momentum, with PLI-driven cumulative sales reaching ₹2,720 crore, including ₹527.96 crore from exports, positioning India as a reliable secondary sourcing hub for quetiapine intermediates amid global supply chain realignment. Corporate growth, exemplified by AstraZeneca Pharma India’s 39% revenue increase in Q3 FY2025-26, reflects rising domestic demand for central nervous system (CNS) therapeutics supported by localized intermediate production. Additionally, the launch of the ₹5,000 crore PRIP (Promotion of Research and Innovation in Pharma-MedTech) scheme is accelerating innovation in complex tricyclic intermediates, enhancing India’s capabilities in high-purity quetiapine precursor synthesis and process optimization.

China Quetiapine Intermediate Chemicals Market: Zero-Tolerance Regulation, Lifecycle Accountability, and High-Purity Synthesis Transition

China’s quetiapine intermediate chemicals market is undergoing a structural transformation in 2026, driven by stringent environmental laws, lifecycle accountability mandates, and a shift toward high-purity, proprietary chemical synthesis. The implementation of State Council Decree No. 828 introduces a “lifecycle accountability” framework, enforcing stricter oversight across segmented and outsourced intermediate manufacturing, thereby increasing compliance costs while elevating quality assurance standards in pharmaceutical intermediates.

The adoption of the Ecological and Environmental Code (March 2026) further intensifies regulatory scrutiny on high-effluent processes such as thiazepine ring synthesis, compelling manufacturers to invest in green chemistry technologies and waste minimization systems. Additionally, expanded data exclusivity provisions (up to six years) are incentivizing Chinese producers to shift from commoditized intermediates toward high-value, IP-driven synthesis routes for quetiapine and other CNS drugs. Inclusion of CNS therapies in the 2026 National Reimbursement Drug List (NRDL) ensures stable domestic demand, while new compliance rules requiring foreign Marketing Authorization Holders (MAHs) to appoint local legal representatives are driving rigorous supplier audits and quality system upgrades, reinforcing China’s evolution into a high-compliance, high-value pharmaceutical intermediate manufacturing hub.

United States Quetiapine Intermediate Chemicals Market: Onshoring Strategy, FDA KASA Integration, and High-Purity LAI Demand

The United States quetiapine intermediate chemicals market is being reshaped by onshoring initiatives, FDA regulatory modernization, and increasing demand for high-purity intermediates in advanced drug delivery systems. A key catalyst is the Section 232 tariff deferral agreement (2025), which provides a three-year window for pharmaceutical companies to localize intermediate and API manufacturing, targeting full supply chain onshoring by 2028–2029. This aligns with broader national priorities to reduce dependence on APAC imports and enhance supply chain security for critical medicines.

Regulatory transformation is underway with the full integration of the FDA’s KASA (Knowledge-aided Assessment & Structured Application) system in 2026, requiring intermediate manufacturers to submit structured, data-rich Drug Master Files (DMFs) in eCTD format, significantly raising the bar for process transparency, impurity profiling, and quality-by-design (QbD) compliance. Demand dynamics are also evolving, with a shift toward long-acting injectable (LAI) quetiapine formulations, necessitating ultra-low impurity intermediates and highly controlled synthesis pathways. Additionally, spillover effects from the CHIPS and Science Act are incentivizing domestic production of high-purity specialty chemicals, further strengthening the U.S. position in advanced pharmaceutical intermediate manufacturing and regulatory leadership.

European Union Quetiapine Intermediate Chemicals Market: Critical Medicines Act, Green Fine Chemicals, and CDMO-Led Localization

The European quetiapine intermediate chemicals market, particularly across Germany and France, is advancing toward strategic autonomy and sustainable pharmaceutical manufacturing, driven by the proposed Critical Medicines Act (CMA) in 2026. This legislation aims to provide financial incentives and subsidies for local production of essential APIs and intermediates, reducing reliance on external supply chains and mitigating drug shortages across the EU. Industry bodies such as the European Fine Chemicals Group (EFCG) are actively advocating for a resilient and self-sufficient European API ecosystem, positioning the region as a hub for high-value fine chemical synthesis.

Environmental compliance is a key differentiator, with manufacturers integrating green chemistry principles, including biocatalysis and solvent minimization, to meet the EU’s 2030 decarbonization targets. The Biotech Act 2026 roadmap further strengthens the role of Contract Development and Manufacturing Organizations (CDMOs) in localizing the production of complex quetiapine intermediates and derivatives, enhancing supply chain agility. Meanwhile, the expansion of generic quetiapine fumarate production in Eastern Europe (Poland, Hungary) is driving demand for cost-efficient yet high-quality intermediates, creating a balanced ecosystem of innovation-driven Western Europe and cost-competitive Eastern European manufacturing clusters.

Kuwait Quetiapine Intermediate Chemicals Market: GCC Manufacturing Expansion, Local Procurement Policies, and Regional Distribution Hub Emergence

Kuwait is emerging as a strategic growth hub in the Middle East quetiapine intermediate chemicals market, supported by government-led pharmaceutical investments, regional demand for mental health therapeutics, and supply chain localization initiatives. The Kuwaiti government’s plan to invest over USD 500 million in pharmaceutical infrastructure (2026–2029) is focused on developing domestic capabilities for essential psychiatric drug production, including quetiapine intermediates and APIs. This marks a shift toward reducing reliance on traditional suppliers such as the U.S., China, and India.

Policy reforms are also reshaping procurement strategies, with government agencies prioritizing locally manufactured chemical intermediates in national drug tenders, creating new opportunities for regional producers and contract manufacturers. Companies such as Kuwait Saudi Pharmaceutical Industries Company (KSPICO) and Julphar are expanding their manufacturing footprint to capture rising demand across the Gulf Cooperation Council (GCC). Kuwait City is simultaneously being developed as a regional logistics and distribution hub, leveraging its proximity to high-growth healthcare markets in Iraq and Jordan. Furthermore, local manufacturers are investing in GMP-compliant advanced synthesis technologies, aligning with FDA and EMA standards, which enhances Kuwait’s potential to become a competitive exporter of high-quality pharmaceutical intermediates in the Middle East.

Quetiapine Intermediate Chemicals Market Report Scope

Quetiapine Intermediate Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$43.6 Billion

|

|

Market Size (2034)

|

$65.4 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Intermediate Type (Dibenzo Thiazepine Intermediates, Piperazine Side-Chain Intermediates, Chlorinated Thiazepine Intermediates, Quetiapine Fumarate), By Synthesis Route (Batch Processing, Continuous Flow Synthesis, Green Chemistry Routes), By End-Use (Generic Drug Manufacturing, Innovative Drug Development, Contract Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AstraZeneca PLC, Merck KGaA, IOL Chemicals and Pharmaceuticals Limited, Aarti Pharmalabs Limited, Luye Pharma Group Limited, Ami Organics Limited, Zhejiang Huahai Pharmaceutical Co. Ltd., Krka dd, Allchem Lifescience Private Limited, A R Life Sciences, Shreeneel Chemicals, Aether Industries Limited, Sun Pharmaceutical Industries Limited, Teva Pharmaceutical Industries Limited, Sandoz AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Quetiapine Intermediate Chemicals Market Segmentation

By Intermediate Type

- Dibenzo Thiazepine Intermediates

- Piperazine Side-Chain Intermediates

- Chlorinated Thiazepine Intermediates

- Quetiapine Fumarate

By Synthesis Route

- Batch Processing

- Continuous Flow Synthesis

- Green Chemistry Routes

By End-Use

- Generic Drug Manufacturing

- Innovative Drug Development

- Contract Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Quetiapine Intermediate Chemicals Industry

- AstraZeneca PLC

- Merck KGaA

- IOL Chemicals and Pharmaceuticals Limited

- Aarti Pharmalabs Limited

- Luye Pharma Group Limited

- Ami Organics Limited

- Zhejiang Huahai Pharmaceutical Co. Ltd.

- Krka dd

- Allchem Lifescience Private Limited

- A R Life Sciences

- Shreeneel Chemicals

- Aether Industries Limited

- Sun Pharmaceutical Industries Limited

- Teva Pharmaceutical Industries Limited

- Sandoz AG

*- List not Exhaustive